Reports

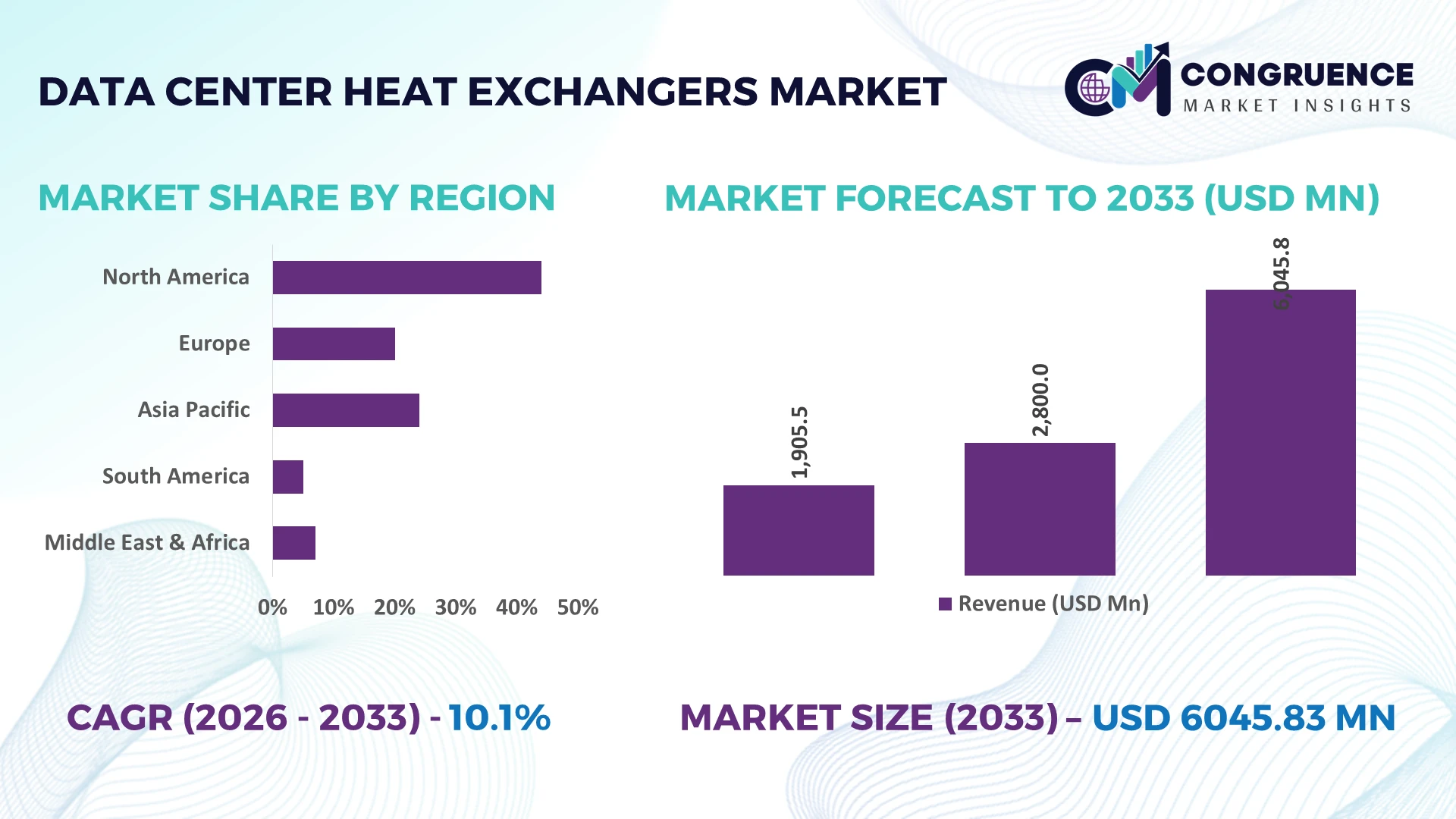

The Global Data Center Heat Exchangers Market was valued at USD 2800 Million in 2025 and is anticipated to reach a value of USD 6045.83 Million by 2033 expanding at a CAGR of 10.1% between 2026 and 2033. Rising deployment of AI-ready hyperscale data centers, accelerated liquid cooling adoption, and stricter energy-efficiency regulations are driving sustained investment in advanced data center heat exchanger technologies.

The United States leads the global Data Center Heat Exchangers Market, accounting for approximately 38% of installed hyperscale cooling capacity, supported by multi-billion-dollar AI infrastructure investments and widespread deployment across cloud, colocation, and enterprise facilities. Over 62% of newly commissioned large-scale data centers integrate advanced liquid-assisted thermal management solutions. Compared with Germany, where sustainability-driven modernization dominates, the U.S. benefits from faster hyperscale expansion despite ongoing semiconductor supply-chain adjustments linked to global geopolitical trade realignments.

Organizations prioritizing scalable, energy-efficient heat exchange infrastructure secure stronger operational resilience, lower cooling costs, and long-term competitive advantages in high-density computing environments.

Market Size & Growth: USD 2800 Million (2025) to USD 6045.83 Million (2033) at 10.1% CAGR, driven by AI server deployment and liquid cooling expansion.

Top Growth Drivers: AI workloads (+42%), hyperscale expansion (+35%), energy-efficiency upgrades (+29%).

Short-Term Forecast: By 2028, cooling energy consumption declines by 18% through advanced heat recovery and optimized thermal management.

Emerging Technologies: AI-driven cooling controls, microchannel heat exchangers, and liquid cooling improve thermal efficiency by over 20%.

Regional Leaders: North America (~USD 2.4 Billion), Asia-Pacific (~USD 1.9 Billion), Europe (~USD 1.3 Billion), supported by hyperscale and sustainability investments.

Consumer/End-User Trends: Nearly 58% of new hyperscale facilities adopt liquid-assisted cooling for high-density AI racks.

Pilot/Case Example: 2026 deployment of advanced heat exchanger systems reduced cooling energy use by 24% in large AI-focused data centers.

Competitive Landscape: Top players hold nearly 48% combined share alongside Vertiv, Alfa Laval, Kelvion, Modine, and Schneider Electric.

Regulatory & ESG Impact: Energy-efficiency standards improve cooling performance by approximately 15% while supporting lower carbon emissions.

Investment & Funding: More than USD 9 Billion supports capacity expansion, strategic partnerships, and regional manufacturing diversification amid supply-chain shifts.

Innovation & Future Outlook: Next-generation immersion-compatible heat exchangers and intelligent thermal optimization strengthen high-density computing infrastructure.

The Data Center Heat Exchangers Market continues to expand as hyperscale cloud providers, AI infrastructure developers, and colocation operators prioritize higher rack densities with lower energy intensity. Compact liquid-cooled heat exchangers, corrosion-resistant materials, and intelligent thermal monitoring improve cooling effectiveness by nearly 20% while supporting stricter efficiency regulations and resilient component sourcing. These developments establish a strong foundation for the strategic market analysis that follows.

The Data Center Heat Exchangers Market has become a strategic investment priority as AI computing, hyperscale expansion, and high-density server deployments reshape digital infrastructure planning. Organizations increasingly view advanced thermal management as a competitive differentiator because cooling efficiency directly influences operating costs and computing capacity. Infrastructure modernization and localized manufacturing are restructuring global supply chains, reducing procurement risks while supporting faster deployment of next-generation facilities. This structural shift is strengthening investment confidence across enterprise and colocation environments.

Modern liquid-assisted heat exchangers provide nearly 24% higher thermal efficiency than conventional air-cooled systems while lowering cooling energy consumption by approximately 18% in high-density environments. The United States leads large-scale hyperscale deployment, whereas Japan emphasizes compact, high-efficiency thermal systems for space-constrained facilities. During the next 2–3 years, more than 60% of newly commissioned AI-ready data centers are expected to integrate liquid-enabled heat exchange technologies as rack densities continue increasing.

A hyperscale operator upgrading rear-door heat exchangers with direct-to-chip cooling can expand computing capacity without enlarging its facility footprint, improving operational utilization and energy performance. Manufacturers are responding through regional production expansion, technology partnerships, and modular product development to accelerate deployment schedules. Companies establishing scalable thermal management ecosystems today secure stronger operational resilience, improved infrastructure flexibility, and sustainable competitive positioning.

The rapid deployment of AI servers and high-performance computing clusters is accelerating adoption of advanced data center heat exchangers. More than 65% of newly planned hyperscale facilities now incorporate liquid-assisted cooling architectures, while optimized heat exchangers improve thermal transfer efficiency by approximately 22% and reduce cooling electricity consumption by nearly 18%. The United States continues expanding domestic AI infrastructure following semiconductor manufacturing investments, creating sustained demand for advanced thermal technologies. Equipment manufacturers are expanding production capacity, strengthening engineering partnerships, and introducing modular heat exchanger platforms that shorten installation cycles. This structural transition enables operators to support higher rack densities while improving facility reliability and long-term operating efficiency.

Production of advanced heat exchangers depends on specialized copper alloys, stainless steel, and precision fabrication, exposing manufacturers to persistent cost fluctuations. Raw material prices have varied by nearly 15%, while procurement timelines for critical thermal components remain around 20% longer than historical averages across several industrial supply chains. Germany continues experiencing elevated industrial energy costs, increasing manufacturing expenses for thermal equipment suppliers. These structural pressures reduce project profitability and delay infrastructure deployment schedules. Companies are addressing these constraints through localized sourcing strategies, long-term supplier agreements, component standardization, and alternative material engineering to improve procurement stability and maintain consistent product availability.

The integration of AI-driven thermal monitoring, predictive maintenance, and direct-to-chip cooling is creating high-value opportunities across existing and new data center infrastructure. Intelligent cooling platforms improve system utilization by approximately 17%, while predictive maintenance reduces unexpected equipment downtime by nearly 24%. India is expanding domestic digital infrastructure at an accelerated pace, generating strong demand for efficient thermal management across hyperscale and enterprise facilities. Manufacturers are increasing investment in intelligent monitoring software, modular cooling solutions, and ecosystem partnerships with automation providers. Retrofitting legacy facilities with advanced heat exchangers offers operators a cost-efficient pathway to support AI workloads without constructing entirely new data center campuses.

Deploying advanced heat exchangers within existing facilities requires extensive engineering coordination as computing densities continue increasing. Nearly 40% of enterprise data centers require significant mechanical modifications before liquid cooling integration, while commissioning periods typically increase by around 18% due to interoperability and infrastructure redesign requirements. Japan faces additional implementation challenges because many urban facilities operate within highly constrained building footprints. These technical complexities affect deployment consistency, operational continuity, and long-term scalability. Leading companies are investing in modular engineering, workforce training, digital commissioning tools, and standardized integration frameworks to simplify implementation while ensuring reliable performance across diverse high-density computing environments.

Liquid Cooling Becomes Mainstream: Liquid-assisted heat exchangers are becoming the preferred thermal management approach for AI-ready facilities, with adoption exceeding 58% across newly commissioned hyperscale projects. Cooling energy consumption declines by nearly 18%, while rack density improves by approximately 25% through direct liquid circulation. Semiconductor manufacturing expansion and AI infrastructure investments are encouraging suppliers to localize production, increase manufacturing capacity, and establish engineering partnerships that shorten deployment timelines and improve component availability.

Microchannel Technology Expands Rapidly: Compact microchannel heat exchangers reduce coolant requirements by around 30% while increasing heat transfer efficiency by nearly 20% compared with conventional designs. Operators in Japan are deploying these systems to maximize cooling performance within space-constrained facilities. Manufacturers are redesigning production lines, introducing lightweight materials, and increasing automation to reduce fabrication time and improve product consistency for high-density computing environments.

Intelligent Thermal Management Advances: AI-enabled monitoring platforms now support nearly 46% of new enterprise cooling installations, reducing unexpected maintenance by approximately 21% and improving cooling asset utilization by around 17%. Rather than replacing existing equipment, operators are integrating predictive diagnostics into installed heat exchanger systems. Companies are expanding software capabilities, strengthening automation partnerships, and combining thermal analytics with facility management platforms to improve operational efficiency.

Heat Recovery Gains Commercial Focus: Advanced heat exchangers capable of recovering nearly 20% of usable thermal energy are becoming integral to sustainable facility operations, reducing overall cooling energy demand by approximately 14%. Stricter energy-efficiency regulations and infrastructure modernization programs are accelerating deployment across Northern Europe. Equipment manufacturers are developing dual-purpose heat exchanger systems, expanding collaboration with engineering firms, and optimizing product designs for waste-heat utilization in commercial and district energy applications.

Liquid-Cooled heat exchangers remain the leading segment because they provide superior thermal performance for AI servers, hyperscale computing, and high-density rack environments. Around 60% of newly designed AI-focused facilities prioritize liquid-cooled architectures due to improved heat dissipation, lower operating temperatures, and greater scalability. Plate Heat Exchangers continue holding a significant share through compact construction, easier maintenance, and flexible integration across enterprise environments. Shell & Tube systems retain importance for large industrial facilities requiring high-pressure operation, while Air-Cooled solutions remain suitable for lower-density deployments where infrastructure simplicity remains a priority.

Microchannel heat exchangers represent the fastest-growing segment as operators seek compact solutions that improve thermal efficiency by nearly 20% while reducing coolant consumption by approximately 30%. Manufacturers are expanding production capacity, investing in lightweight materials, and introducing modular product platforms optimized for AI-ready infrastructure. Investment priorities continue shifting toward advanced liquid cooling technologies that balance long-term reliability, deployment flexibility, and operational efficiency across next-generation data centers.

Hyperscale Data Centers account for the largest application segment because continuous AI infrastructure expansion and cloud computing growth require advanced thermal management capable of supporting dense computing environments. Approximately 65% of newly deployed hyperscale facilities integrate advanced heat exchanger technologies to improve cooling efficiency and maintain operational stability. Enterprise Data Centers continue modernizing existing cooling infrastructure, while Colocation Data Centers focus on flexible thermal platforms capable of supporting diverse customer workloads without major infrastructure redesign.

Edge Data Centers are emerging as the fastest-growing application as distributed computing expands across telecommunications, manufacturing, and digital public infrastructure. Deployment activity has increased by approximately 24%, driving demand for compact, modular heat exchangers that simplify installation and maintenance. Cloud Facilities continue strengthening market demand through continuous AI infrastructure expansion. Manufacturers are responding by developing standardized cooling platforms, expanding deployment partnerships, and improving modular system compatibility across multiple facility configurations.

Hyperscale Data Centers represent the dominant end-user segment because they operate the largest concentration of AI infrastructure, cloud computing platforms, and high-density processing environments requiring advanced thermal management. More than 62% of new thermal infrastructure investments originate from hyperscale operators expanding AI-ready campuses. Cloud Facilities maintain strong procurement activity through continuous infrastructure upgrades, while Colocation Data Centers invest in adaptable cooling systems capable of supporting varied customer performance requirements.

Edge Data Centers are the fastest-growing end-user group as distributed digital infrastructure expands across industrial automation, connected mobility, and smart city applications. Deployment activity has increased by nearly 22%, encouraging manufacturers to introduce standardized modular heat exchanger solutions for rapid implementation. Enterprise Data Centers continue investing through phased retrofit programs instead of complete facility replacement. Companies are strengthening engineering support, expanding regional service capabilities, and developing customized thermal solutions to improve deployment efficiency and strengthen long-term customer relationships.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.6% between 2026 and 2033.

North America remains the leading regional market as hyperscale cloud expansion, AI infrastructure deployment, and large-scale colocation investments accelerate demand for advanced heat exchanger technologies. The region contributes nearly 39% of global deployment activity, supported by extensive hyperscale campuses and continuous modernization of enterprise facilities. More than 64% of newly commissioned high-density data centers integrate liquid-assisted cooling systems to improve thermal efficiency and support AI workloads exceeding conventional rack power limits. Strategic partnerships between thermal equipment manufacturers and cloud infrastructure providers continue shortening deployment timelines while expanding domestic production capabilities. Infrastructure investment and engineering standardization further strengthen regional competitiveness.

United States Market Outlook: The United States leads regional demand through aggressive expansion of AI computing campuses, cloud infrastructure, and semiconductor manufacturing investments. More than 68% of North American hyperscale construction activity is concentrated in the country, encouraging widespread deployment of advanced liquid cooling and high-performance heat exchangers. Domestic manufacturers continue expanding production capacity, strengthening engineering partnerships, and introducing modular thermal systems that reduce commissioning complexity while supporting higher rack densities across enterprise and hyperscale environments.

Europe continues strengthening its position through sustainability-driven modernization, advanced engineering capabilities, and stricter energy-efficiency requirements. The region accounts for approximately 27% of global deployment activity as operators replace conventional cooling infrastructure with energy-efficient thermal management systems. Waste-heat recovery integration and liquid cooling adoption continue expanding across hyperscale and enterprise facilities. More than 42% of new projects incorporate heat recovery technologies to improve operational efficiency while meeting environmental objectives. Equipment manufacturers are strengthening regional engineering partnerships and localized manufacturing to support evolving infrastructure standards.

Germany Market Outlook: Germany remains the region's most influential market through its advanced industrial manufacturing ecosystem, established colocation sector, and strong engineering expertise. Enterprise modernization projects continue driving demand for compact and efficient heat exchanger systems, with nearly 45% of large data center upgrades incorporating advanced liquid-compatible cooling technologies. Manufacturers are investing in precision production, digital monitoring integration, and localized supply networks to improve deployment efficiency while supporting national sustainability objectives.

Asia-Pacific represents the fastest-growing regional market as cloud adoption, AI investment, and digital infrastructure construction expand across major economies. The region contributes nearly 30% of global deployment activity while recording the highest volume of new hyperscale developments. Approximately 57% of newly announced large-scale facilities incorporate advanced heat exchanger technologies designed for high-density computing. Regional manufacturers continue increasing production capacity, improving export capabilities, and expanding engineering partnerships to satisfy accelerating infrastructure demand while strengthening supply-chain resilience.

China Market Outlook: China dominates the regional market through large-scale hyperscale construction, domestic manufacturing capacity, and continuous investment in digital infrastructure. More than 60% of newly developed AI-oriented facilities utilize advanced liquid-assisted cooling architectures, increasing demand for high-performance heat exchangers. Domestic producers continue expanding automated manufacturing, strengthening component localization, and investing in thermal innovation to improve production efficiency while supporting rapid infrastructure deployment.

South America is steadily expanding its presence in the Data Center Heat Exchangers Market as enterprise digital transformation, cloud migration, and colocation investments increase across major economies. The region accounts for nearly 5% of global deployment activity, with Brazil leading hyperscale and enterprise infrastructure development. Approximately 35% of newly commissioned facilities now integrate advanced heat exchanger technologies to improve thermal efficiency and reduce operating costs. Although grid reliability and imported equipment dependency remain operational constraints, suppliers are expanding regional partnerships, localized engineering support, and service capabilities to improve deployment consistency and reduce implementation timelines.

Brazil Market Outlook: Brazil represents the largest market in South America through expanding cloud infrastructure, enterprise modernization, and growing colocation investments. More than 60% of regional hyperscale capacity is concentrated in Brazil, supporting increasing adoption of liquid-compatible heat exchangers across new facilities. Equipment suppliers are strengthening local distribution, engineering collaboration, and after-sales support while operators continue upgrading cooling infrastructure to accommodate higher-density computing environments and improve long-term operational efficiency.

The Middle East & Africa market is expanding through government-backed digital infrastructure initiatives, hyperscale investment, and increasing demand for energy-efficient cooling technologies. The region contributes approximately 4% of global deployment activity while experiencing rapid construction of cloud and colocation facilities. Around 38% of newly planned data centers incorporate advanced liquid-assisted heat exchangers to address high ambient temperatures and improve cooling performance. Equipment manufacturers are establishing regional partnerships, expanding technical support networks, and developing solutions optimized for demanding climatic conditions and large-scale infrastructure projects.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional development through sustained investment in smart infrastructure, hyperscale facilities, and digital economy initiatives. Nearly half of the region's large-scale commercial data center projects are concentrated in the country, accelerating deployment of advanced thermal management technologies. Operators continue investing in high-efficiency liquid cooling systems, while manufacturers strengthen local engineering partnerships and service capabilities to support reliable operation under extreme environmental conditions.

The Data Center Heat Exchangers Market is led by Alfa Laval, Vertiv, Kelvion, Modine Manufacturing, and Schneider Electric, competing directly with specialized thermal engineering companies and regional heat exchanger manufacturers. The top five players collectively account for nearly 47% of the market, while regional suppliers compete through faster delivery, localized engineering, and customized cooling solutions. Technology leadership remains the primary competitive factor, with advanced liquid cooling improving thermal efficiency by approximately 20% and modular platforms reducing installation time by nearly 18%. Global manufacturers are expanding production facilities, strengthening engineering partnerships, investing in AI-enabled thermal monitoring, and increasing vertical integration to secure critical components and shorten supply chains. Market competition is shifting toward integrated cooling ecosystems combining hardware, automation, and predictive maintenance rather than standalone equipment. High engineering complexity, qualification requirements, and long customer validation cycles remain significant entry barriers. Sustained success depends on thermal innovation, manufacturing scale, deployment speed, and long-term technical support.

Alfa Laval

Vertiv

Kelvion

Modine Manufacturing Company

Schneider Electric

Danfoss

API Heat Transfer

Boyd Corporation

Lytron (Boyd)

Rittal

STULZ GmbH

Johnson Controls

Airedale International Air Conditioning

Hisaka Works Ltd.

Advanced plate heat exchangers, rear-door heat exchangers, and liquid-cooled thermal loops dominate current deployments as AI-driven rack densities continue increasing. More than 60% of newly designed hyperscale facilities now integrate liquid-assisted cooling, improving thermal efficiency by approximately 22% while reducing cooling energy consumption by nearly 18%. Compared with conventional air-cooled systems, modern liquid heat exchangers deliver around 25% greater heat-transfer performance and support significantly higher rack power densities. Hyperscale cloud operators gain the greatest operational advantage through lower energy intensity and improved infrastructure utilization.

Emerging technologies include microchannel heat exchangers, AI-enabled thermal optimization, and direct-to-chip liquid cooling integrated with intelligent monitoring platforms. Microchannel architectures reduce coolant volume by nearly 30%, while predictive thermal analytics improve cooling asset utilization by approximately 17%. Around 45% of enterprise facilities deploying new cooling infrastructure now integrate digital monitoring with automated thermal controls. Equipment manufacturers are strengthening software partnerships and modular product development to simplify deployment while reducing maintenance complexity across high-density computing environments.

Disruptive innovation is shifting toward warm-water cooling, integrated coolant distribution systems, and modular cooling ecosystems capable of supporting next-generation AI infrastructure. Between 2026 and 2028, liquid-compatible thermal platforms are expected to exceed 65% of new hyperscale deployments, supported by automated commissioning and intelligent energy management. Companies investing in scalable heat exchanger platforms, advanced materials, and integrated thermal software will strengthen competitive positioning through faster deployment, higher operational resilience, and lower lifecycle cooling costs.

March 2025: Vertiv launched the CoolLoop RDHx chilled-water rear-door heat exchanger for AI and high-performance computing, supporting rack cooling capacities up to 80 kW while complementing direct-to-chip liquid cooling. The launch strengthens high-density deployment flexibility for hyperscale operators. Source: vertiv.com

January 2026: Modine introduced the Airedale TurboChill 3+MW hybrid chiller platform for AI data centers, delivering more than 3 MW of heat rejection with expanded free-cooling capability. The innovation improves energy efficiency while enabling larger GPU-based infrastructure deployments.

February 2026: Danfoss launched the B3-260C brazed plate heat exchanger for coolant distribution units, supporting capacities up to 1 MW with optimized low-pressure-drop performance. The solution enhances cooling efficiency and improves power usage effectiveness in mission-critical data center operations. Source: danfoss.com

March 2026: Alfa Laval introduced the FreeWaterLoop integrated liquid cooling system for data centers, combining pumping, filtration, and high-performance heat exchangers into a single platform. The system reduces facility footprint while supporting high-density computing with lower net water consumption. Source: alfalaval.com

The report provides comprehensive analysis across Plate Heat Exchangers, Shell & Tube, Air-Cooled, Liquid-Cooled, and Microchannel technologies, evaluating performance trends, deployment strategies, and operational competitiveness. It examines applications spanning Hyperscale Data Centers, Enterprise Data Centers, Colocation Data Centers, Edge Data Centers, and Cloud Facilities while assessing purchasing patterns across major end-user groups. Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with more than 60% of demand concentrated in high-density digital infrastructure projects.

The study evaluates technology adoption, liquid cooling integration, supply-chain developments, competitive positioning, and infrastructure modernization expected between 2026 and 2033. It analyzes deployment patterns, innovation pipelines, and enterprise investment priorities while comparing established and emerging cooling architectures. Strategic insights support capacity planning, product development, expansion decisions, partnership strategies, and competitive benchmarking across global thermal management ecosystems, enabling organizations to identify high-potential opportunities and strengthen long-term market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2800 Million |

Market Revenue in 2033 | USD 6045.83 Million |

CAGR (2026 - 2033) | 10.1% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Alfa Laval, Vertiv, Kelvion, Modine Manufacturing Company, Schneider Electric, Danfoss, API Heat Transfer, Boyd Corporation, Lytron (Boyd), Rittal, STULZ GmbH, Johnson Controls, Airedale International Air Conditioning, Hisaka Works Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |