Reports

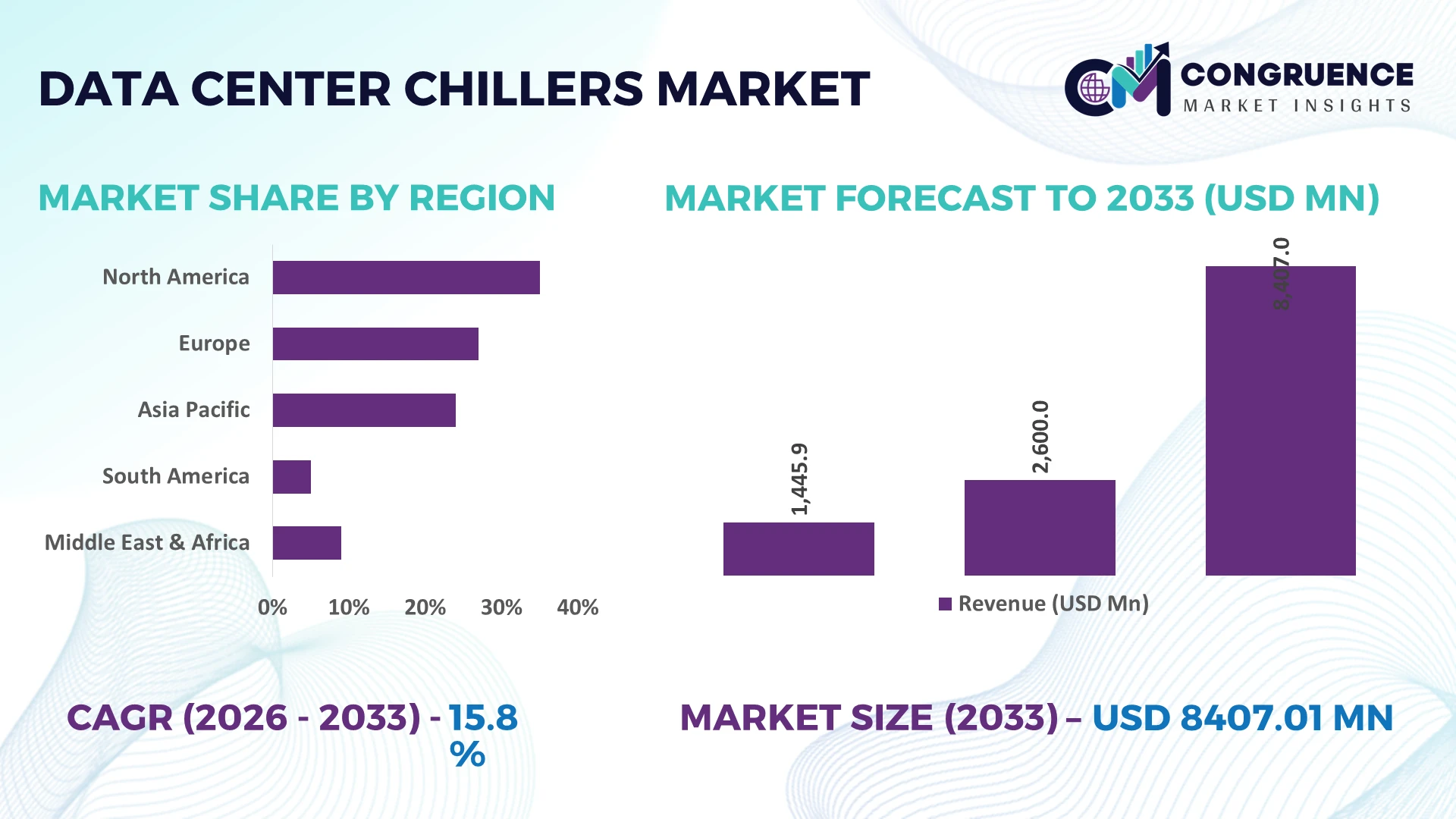

The Global Data Center Chillers Market was valued at USD 2600 Million in 2025 and is anticipated to reach a value of USD 8407.01 Million by 2033 expanding at a CAGR of 15.8% between 2026 and 2033. AI-ready hyperscale facilities, rising rack power densities, and the transition toward energy-efficient cooling architectures are accelerating investments in advanced data center chillers across cloud, colocation, and enterprise infrastructure.

The United States accounts for nearly 38% of global hyperscale data center capacity, supported by sustained investments in AI computing, cloud expansion, and semiconductor manufacturing. In comparison, Germany leads Europe in sustainable cooling deployment through strict energy-efficiency standards, with over 70% of new large-scale facilities integrating low-GWP refrigerant technologies and intelligent cooling controls. Geopolitical supply chain diversification since recent semiconductor trade realignments has further accelerated regional manufacturing and infrastructure investments.

Organizations investing in scalable, high-efficiency chiller technologies are strengthening long-term operational resilience while reducing energy intensity and supporting next-generation AI infrastructure expansion.

Market Size & Growth: USD 2,600 Million (2025) to USD 8,407.01 Million (2033) at 15.8% CAGR, driven by AI infrastructure expansion and high-density data center construction.

Top Growth Drivers: AI server deployments (42%), hyperscale capacity expansion (31%), and energy-efficient cooling upgrades (28%) continue driving global market growth.

Short-Term Forecast: By 2028, advanced chiller technologies are projected to lower cooling energy consumption by 18% while improving operational efficiency by 20%.

Emerging Technologies: AI-powered thermal optimization, digital twins, and liquid-ready cooling architectures improve cooling performance by over 25% while enhancing predictive maintenance.

Regional Leaders: North America exceeds USD 3.2 Billion, Asia-Pacific reaches nearly USD 2.6 Billion, and Europe surpasses USD 1.7 Billion, supported by rapid hyperscale expansion and sustainability initiatives.

Consumer/End-User Trends: Nearly 62% of newly commissioned hyperscale facilities prioritize high-efficiency chillers using low-GWP refrigerants and intelligent monitoring systems.

Pilot/Case Example: 2026: AI-driven cooling optimization in large enterprise data centers reduced cooling electricity consumption by approximately 22% while improving thermal stability.

Competitive Landscape: The top five manufacturers collectively account for nearly 48% of global market share, supported by product innovation, regional manufacturing expansion, and AI-ready cooling portfolios.

Regulatory & ESG Impact: Refrigerant transition programs and stricter energy-efficiency regulations improve facility sustainability performance by approximately 15% while supporting lower operating costs.

Investment & Funding: More than USD 30 Billion has been committed to hyperscale digital infrastructure expansion, with investments focused on manufacturing capacity, regional production, and strategic partnerships.

Innovation & Future Outlook: Modular high-capacity chillers, predictive analytics, and integrated intelligent cooling platforms are reshaping competitive differentiation across the global data center cooling ecosystem.

The Data Center Chillers Market is witnessing strong demand from hyperscale cloud campuses, AI computing clusters, and colocation facilities requiring higher cooling precision and energy optimization. Manufacturers are introducing oil-free magnetic bearing compressors, low-GWP refrigerants, and AI-enabled monitoring platforms, improving cooling efficiency by nearly 25%. Ongoing refrigerant transition regulations and regional supply-chain localization initiatives are accelerating product innovation, setting the foundation for the strategic market analysis that follows.

The Data Center Chillers Market has become strategically important as AI computing, cloud expansion, and high-density digital infrastructure redefine cooling requirements across modern facilities. Infrastructure modernization and refrigerant transition policies are reshaping procurement strategies, while supply-chain localization is reducing dependence on single-country manufacturing. More than 65% of newly planned hyperscale facilities are being designed with advanced cooling systems capable of supporting significantly higher thermal loads, making efficient chiller deployment a critical factor for operational competitiveness.

Modern oil-free magnetic bearing chillers consume nearly 30% less energy and reduce maintenance requirements by approximately 40% compared with conventional screw-based systems, delivering measurable lifecycle savings. The United States focuses on large-scale AI-ready campuses with high-capacity cooling infrastructure, whereas Japan emphasizes compact, energy-efficient chiller technologies for space-constrained facilities. During the next two to three years, intelligent cooling platforms are expected to exceed 55% adoption across newly commissioned hyperscale data centers as operators prioritize predictive thermal management.

Leading cloud providers are expanding partnerships with cooling technology specialists to deploy modular chiller plants that enable rapid capacity expansion without disrupting ongoing operations. Companies are increasing investments in digital monitoring, localized manufacturing, and integrated cooling ecosystems to strengthen operational resilience, improve energy performance, and secure long-term competitive positioning in the evolving digital infrastructure landscape.

Rapid deployment of AI servers and hyperscale facilities is transforming cooling infrastructure requirements, with rack power densities increasing by nearly 45% over conventional enterprise environments. Approximately 68% of newly commissioned hyperscale campuses now prioritize intelligent chiller systems designed for high-density computing workloads. In the United States, semiconductor manufacturing expansion and AI infrastructure investments continue accelerating demand for scalable cooling technologies, while stricter energy-performance standards encourage adoption of low-GWP refrigerants. Chiller manufacturers are responding through production expansion, strategic technology partnerships, and AI-enabled monitoring platforms that optimize thermal performance and reduce operational downtime. This structural shift positions advanced cooling systems as a strategic infrastructure asset rather than a supporting utility.

Advanced magnetic bearing chillers and intelligent cooling platforms require 25–35% higher upfront investment than conventional systems, creating financial constraints for mid-sized operators. Critical compressor components and power electronics continue experiencing lead times exceeding 20 weeks across several manufacturing segments, delaying infrastructure deployment schedules. Germany's refrigerant transition requirements have also increased engineering complexity and product certification costs for suppliers. To reduce operational risks, manufacturers are expanding localized production, securing multi-supplier procurement agreements, and increasing inventory for strategic components. These initiatives improve supply resilience but continue placing pressure on project timelines, installation costs, and deployment scalability.

AI-powered cooling optimization, digital twins, and predictive maintenance platforms are creating measurable operational advantages for advanced data center infrastructure. Intelligent thermal management systems reduce cooling energy demand by approximately 20% while improving equipment utilization by nearly 18% through continuous real-time optimization. India is emerging as a strategic deployment market as hyperscale investments and digital infrastructure programs accelerate adoption of intelligent cooling technologies. Manufacturers are expanding research into modular chiller architectures, low-GWP refrigerants, and integrated building management platforms to improve lifecycle performance. Partnerships between cooling specialists and cloud operators are creating service-driven business models that extend beyond traditional equipment supply.

Supporting next-generation AI clusters requires precise thermal balancing across facilities operating at rack densities exceeding 100 kW, significantly increasing integration complexity compared with conventional data centers. More than 60% of operators identify interoperability between cooling equipment, building management software, and AI infrastructure as a major operational challenge. Singapore's strict energy-efficiency and water-management requirements further increase deployment complexity for large-scale facilities operating within limited land availability. Companies must strengthen workforce capabilities, intelligent control systems, modular infrastructure design, and long-term technology partnerships to maintain consistent cooling performance, improve sustainability outcomes, and preserve operational competitiveness as digital infrastructure continues advancing.

AI-Ready Cooling Expansion: AI computing clusters are increasing average rack densities by nearly 45%, prompting over 60% of newly commissioned hyperscale facilities to deploy high-capacity chiller systems with intelligent thermal controls. Operators are redesigning cooling workflows around predictive monitoring and modular expansion while equipment suppliers scale production and engineering partnerships to shorten deployment cycles. Growing semiconductor investments in the United States continue reinforcing demand for advanced cooling infrastructure.

Low-GWP Refrigerant Transition: More than 55% of newly specified chiller installations now incorporate low-GWP refrigerants as environmental regulations accelerate equipment replacement strategies. Modern compressor technologies reduce energy consumption by approximately 20% while lowering maintenance frequency by nearly 18%. Manufacturers are restructuring product portfolios, expanding compliant manufacturing capacity, and strengthening supplier networks to support refrigerant transitions without disrupting enterprise deployment schedules.

Modular Deployment Strategies: Modular chiller adoption has increased by approximately 35% across enterprise and colocation projects because prefabricated systems reduce installation time by nearly 30% compared with conventional plant construction. Data center operators increasingly deploy scalable cooling modules that match phased infrastructure expansion, reducing stranded capacity. Equipment vendors are expanding localized assembly operations and standardizing modular product platforms to improve project execution and supply-chain resilience.

Digital Thermal Intelligence: AI-enabled analytics and digital twin technologies are improving cooling asset utilization by approximately 25% while reducing unexpected maintenance events by nearly 22%. Rather than replacing equipment, operators are extracting additional efficiency from existing cooling infrastructure through continuous optimization and automated diagnostics. Technology providers are expanding software partnerships and integrated service offerings, creating recurring operational value beyond traditional equipment sales.

Water-Cooled Chillers remain the dominant segment because they deliver superior cooling efficiency, stable thermal performance, and lower operating costs across hyperscale and enterprise data centers. Nearly 58% of large-scale facilities continue selecting water-cooled systems where reliable water infrastructure is available, making them the preferred choice for continuous high-density operations. Centrifugal Chillers strengthen this segment through high-capacity performance, while Screw Chillers remain widely deployed in medium-sized facilities requiring operational flexibility and proven reliability. Manufacturers continue enhancing compressor efficiency, intelligent controls, and refrigerant technologies to improve lifecycle performance and reduce energy consumption.

Modular Chillers are the fastest-growing segment, with adoption increasing by approximately 34% as operators prioritize phased capacity expansion, faster deployment, and simplified maintenance. Air-Cooled Chillers continue gaining traction in water-constrained locations despite lower efficiency than water-cooled alternatives, supporting broader deployment flexibility. Companies are expanding modular product portfolios, investing in digital monitoring capabilities, and strengthening manufacturing partnerships to address diverse customer requirements while aligning product strategies with evolving AI infrastructure needs.

Hyperscale Data Centers represent the largest application segment because AI computing, cloud expansion, and large-scale digital services require continuous high-capacity cooling infrastructure. Approximately 64% of newly commissioned hyperscale campuses integrate intelligent chiller systems to improve thermal efficiency and maximize infrastructure utilization. Cloud Facilities remain a major demand contributor through ongoing capacity expansion, while Enterprise Data Centers continue replacing conventional cooling systems with intelligent, energy-efficient technologies to reduce operational costs and improve reliability.

Edge Data Centers are the fastest-growing application as distributed computing and low-latency digital services accelerate localized infrastructure deployment. Installation activity has increased by nearly 32%, encouraging manufacturers to develop compact modular chiller solutions optimized for smaller facilities. Colocation Data Centers continue strengthening their strategic role by supporting multi-tenant environments with scalable cooling infrastructure. Equipment suppliers are expanding partnerships with cloud providers, increasing automation capabilities, and introducing standardized cooling platforms to meet evolving operational requirements across diverse deployment models.

Cloud Providers remain the dominant end-user segment as hyperscale infrastructure expansion and AI computing continue increasing demand for high-performance cooling systems. Nearly 66% of newly deployed large-scale cooling capacity is associated with cloud infrastructure projects requiring continuous thermal optimization and high operational reliability. IT & Telecom organizations continue investing in advanced chiller upgrades to improve network resilience and support expanding digital traffic, while BFSI institutions are modernizing mission-critical facilities to strengthen operational continuity and regulatory compliance.

Healthcare represents the fastest-growing end-user segment as digital diagnostics, AI-enabled healthcare platforms, and electronic medical record infrastructure require secure, high-availability data centers. Cooling infrastructure deployment across healthcare facilities has increased by approximately 28%, encouraging manufacturers to develop customized, energy-efficient solutions for critical operations. Government organizations continue expanding sovereign digital infrastructure, while Manufacturing enterprises adopt advanced cooling technologies to support industrial digitalization and edge computing. Companies are responding through sector-specific solutions, strategic partnerships, flexible service agreements, and integrated monitoring platforms to strengthen competitive positioning.

North America accounted for the largest market share at 39.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 17.6% between 2026 and 2033.

AI Infrastructure and Hyperscale Expansion Strengthen Cooling Investments

North America maintains the leading position in the Data Center Chillers Market due to its dense concentration of hyperscale campuses, cloud infrastructure, and AI computing facilities. The region contributes nearly 39% of global deployment activity, supported by continuous investments from major cloud operators and colocation providers. Rack densities exceeding 100 kW are accelerating demand for advanced water-cooled and modular chiller systems capable of maintaining thermal stability. Equipment manufacturers are expanding localized production and service capabilities while integrating AI-based monitoring into cooling infrastructure. Recent multi-campus expansion projects have increased advanced cooling equipment deployment by approximately 24%, reinforcing North America's leadership in high-performance digital infrastructure.

United States Market Outlook: The United States remains the regional growth engine through sustained hyperscale expansion, semiconductor manufacturing investments, and AI infrastructure deployment. More than 38% of the world's hyperscale data center capacity is located in the country, driving continuous demand for high-efficiency chiller technologies. Operators increasingly prioritize modular cooling plants, predictive maintenance platforms, and low-GWP refrigerants to improve operational resilience while supporting next-generation AI workloads without compromising energy efficiency.

Sustainability Regulations Accelerate Cooling Modernization

Europe continues strengthening its position through strict environmental regulations, high-efficiency infrastructure upgrades, and modernization of enterprise data centers. Approximately 26% of newly commissioned facilities integrate intelligent cooling controls and advanced refrigerant technologies to comply with evolving energy standards. Growing investments in sustainable digital infrastructure encourage replacement of conventional cooling systems with high-efficiency centrifugal and magnetic bearing chillers. Equipment suppliers continue expanding regional engineering capabilities and localized manufacturing to support regulatory compliance while improving deployment flexibility across major enterprise markets.

Germany Market Outlook: Germany leads the European market through strong industrial infrastructure, advanced engineering expertise, and a rapidly expanding colocation ecosystem. More than 70% of newly developed enterprise facilities prioritize energy-efficient cooling equipment incorporating low-GWP refrigerants and digital monitoring technologies. Continuous investment in green infrastructure and industrial automation enables manufacturers to introduce high-performance cooling systems aligned with evolving environmental requirements and long-term operational efficiency goals.

Large-Scale Digital Infrastructure Drives Deployment Momentum

Asia-Pacific is emerging as the fastest-expanding regional market as cloud providers, telecom operators, and governments accelerate digital infrastructure development. Nearly 34% of global hyperscale projects under construction are concentrated across major Asia-Pacific economies, increasing demand for scalable cooling technologies. Manufacturers are expanding regional production facilities while introducing modular chiller platforms designed for rapid deployment and high-density computing environments. Continuous investment in AI infrastructure and semiconductor manufacturing strengthens long-term equipment demand and encourages strategic partnerships across the regional supply chain.

China Market Outlook: China remains the largest national market in Asia-Pacific because of extensive cloud infrastructure expansion, domestic manufacturing strength, and large-scale digital transformation initiatives. More than 30% of new hyperscale capacity additions across the region are concentrated in China, creating sustained demand for advanced cooling equipment. Domestic manufacturers continue expanding intelligent manufacturing capabilities while operators invest in energy-efficient cooling systems supporting large AI computing clusters and enterprise digitalization.

Digital Infrastructure Investment Expands Regional Demand

South America is experiencing steady market development as cloud infrastructure investments and enterprise digital transformation increase cooling equipment requirements. Brazil and neighboring economies continue expanding colocation facilities and regional cloud availability zones, encouraging adoption of modular and energy-efficient chiller technologies. Infrastructure constraints remain evident in selected markets, yet strategic partnerships between global technology providers and local operators continue improving deployment capabilities. Recent infrastructure modernization programs have increased advanced cooling system installations by approximately 18%, supporting gradual market expansion while improving operational reliability.

Brazil Market Outlook: Brazil leads the regional market through its established colocation ecosystem, expanding enterprise cloud adoption, and growing financial technology sector. The country continues attracting international digital infrastructure investments that require reliable, high-capacity cooling systems. Operators increasingly deploy intelligent monitoring solutions and modular cooling platforms to improve scalability, reduce maintenance interruptions, and support continuous expansion of mission-critical facilities.

Strategic Infrastructure Investments Transform Cooling Demand

The Middle East & Africa market is advancing through government-led digital transformation initiatives, hyperscale investments, and smart city developments requiring resilient cooling infrastructure. Modern data center construction increasingly emphasizes high-efficiency chiller technologies capable of operating under extreme climatic conditions. Regional operators continue investing in intelligent cooling controls, water optimization technologies, and modular equipment to improve operational performance. Strategic infrastructure programs have increased deployment of advanced cooling systems by nearly 20%, encouraging international manufacturers to strengthen regional partnerships and technical support capabilities.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the regional technology hub through strong digital infrastructure investment, cloud adoption, and smart city development programs. Large-scale enterprise campuses increasingly deploy advanced water-cooled and modular chiller systems to maintain operational stability under demanding environmental conditions. Continuous investment in AI infrastructure, renewable-powered data centers, and intelligent facility management strengthens long-term demand for high-performance cooling technologies while supporting regional digital transformation objectives.

Global leaders including Vertiv, Trane Technologies, Johnson Controls, Carrier, and Daikin primarily compete against regional HVAC manufacturers and specialized cooling solution providers through technology leadership, while OEMs challenge component suppliers by expanding integrated cooling portfolios. The top five companies collectively control approximately 48% of the market, creating moderate consolidation with strong technological differentiation. Competition centers on energy efficiency, deployment speed, supply-chain resilience, and customized cooling architectures, with advanced magnetic bearing systems reducing energy consumption by nearly 30% and predictive maintenance lowering service requirements by approximately 25%. Manufacturers are strengthening market positions through localized production, AI-enabled monitoring platforms, strategic partnerships with hyperscale operators, and selective vertical integration of critical components. The competitive landscape is shifting toward intelligent cooling ecosystems rather than standalone equipment, increasing pressure on suppliers lacking digital capabilities. High engineering requirements, refrigerant compliance, and long qualification cycles remain significant entry barriers. Sustainable innovation, rapid deployment, integrated digital services, and reliable global manufacturing networks define lasting competitive advantage.

Vertiv

Trane Technologies

Johnson Controls

Carrier

Daikin Industries

Mitsubishi Electric

Rittal

STULZ

Schneider Electric

Airedale International Air Conditioning

Smardt Chiller Group

GEA Group

Climaveneta

Baltimore Aircoil Company

AI-enabled thermal optimization, magnetic bearing compressors, and oil-free centrifugal chillers define current technology leadership in the Data Center Chillers Market. More than 60% of newly commissioned hyperscale facilities integrate intelligent cooling controls that improve thermal efficiency by approximately 20% while reducing unplanned maintenance by nearly 25%. Compared with conventional screw chillers, modern magnetic bearing systems consume around 30% less energy and deliver quieter, lubrication-free operation, lowering lifecycle operating costs and increasing system reliability for mission-critical facilities.

Emerging technologies are centered on digital twins, predictive maintenance, modular cooling plants, and low-GWP refrigerants integrated with direct-to-chip and liquid cooling environments. Nearly 45% of AI-ready facilities now deploy modular cooling architectures that shorten installation schedules by approximately 30% while improving expansion flexibility. Intelligent building management integration enables real-time workload balancing, allowing operators to optimize cooling capacity without oversizing infrastructure. Manufacturers offering integrated thermal management platforms gain stronger competitive positioning over suppliers focused solely on standalone chiller equipment.

Between 2026 and 2028, intelligent automation, hybrid liquid-air cooling ecosystems, and AI-driven predictive controls will become standard across high-density data centers. Early adopters are expected to achieve 15–20% lower operating energy intensity and faster deployment cycles, while technology leaders with scalable digital platforms, localized manufacturing, and integrated service capabilities will secure long-term advantages as hyperscale infrastructure continues evolving.

June 2024: Johnson Controls established its dedicated Global Data Centre Solutions organization, expanding manufacturing capacity and reducing delivery lead times for mission-critical cooling solutions supporting hyperscale operators. The initiative strengthened global deployment capabilities for rapidly growing AI infrastructure. Source: johnsoncontrols.com

March 2025: Trane Technologies introduced new Magnetic Bearing and Ascend air-cooled chiller platforms engineered for high-density data centers, improving thermal performance for next-generation facilities while addressing increasing rack power requirements through advanced cooling technologies. Source: trane.com

March 2025: Johnson Controls expanded the YORK YVAM magnetic bearing chiller across Europe, delivering up to 40% lower annual power consumption than comparable systems while supporting zero on-site water usage and faster deployment for hyperscale and colocation data centers.

June 2025: Trane Technologies expanded its liquid cooling portfolio with scalable Coolant Distribution Units supporting capacities from 2.5 MW to 10 MW, enabling hyperscale operators to deploy integrated thermal management solutions for AI-ready infrastructure with greater operational flexibility.

The report provides comprehensive coverage of the Data Center Chillers Market across major product types, including Air-Cooled, Water-Cooled, Screw, Centrifugal, and Modular Chillers. It evaluates demand across Hyperscale Data Centers, Enterprise Data Centers, Colocation Data Centers, Edge Data Centers, and Cloud Facilities, together with key end-user industries including IT & Telecom, Cloud Providers, BFSI, Government, Healthcare, and Manufacturing. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while tracking adoption patterns, deployment strategies, and technology integration across more than 10 leading industry participants.

The analysis examines advanced cooling technologies, AI-enabled thermal management, magnetic bearing compressors, digital monitoring platforms, and low-GWP refrigerants shaping infrastructure modernization between 2026 and 2033. It highlights segment-wise deployment trends, competitive positioning, investment priorities, operational benchmarks, and emerging application opportunities, enabling stakeholders to strengthen expansion strategies, evaluate technology investments, identify high-growth deployment segments, and support informed long-term business decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 2600 Million |

Market Revenue in 2033 | USD 8407.01 Million |

CAGR (2026 - 2033) | 15.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Vertiv, Trane Technologies, Johnson Controls, Carrier, Daikin Industries, Mitsubishi Electric, Rittal, STULZ, Schneider Electric, Airedale International Air Conditioning, Smardt Chiller Group, GEA Group, Climaveneta, Baltimore Aircoil Company |

Customization & Pricing | Available on Request (10% Customization is Free) |