Reports

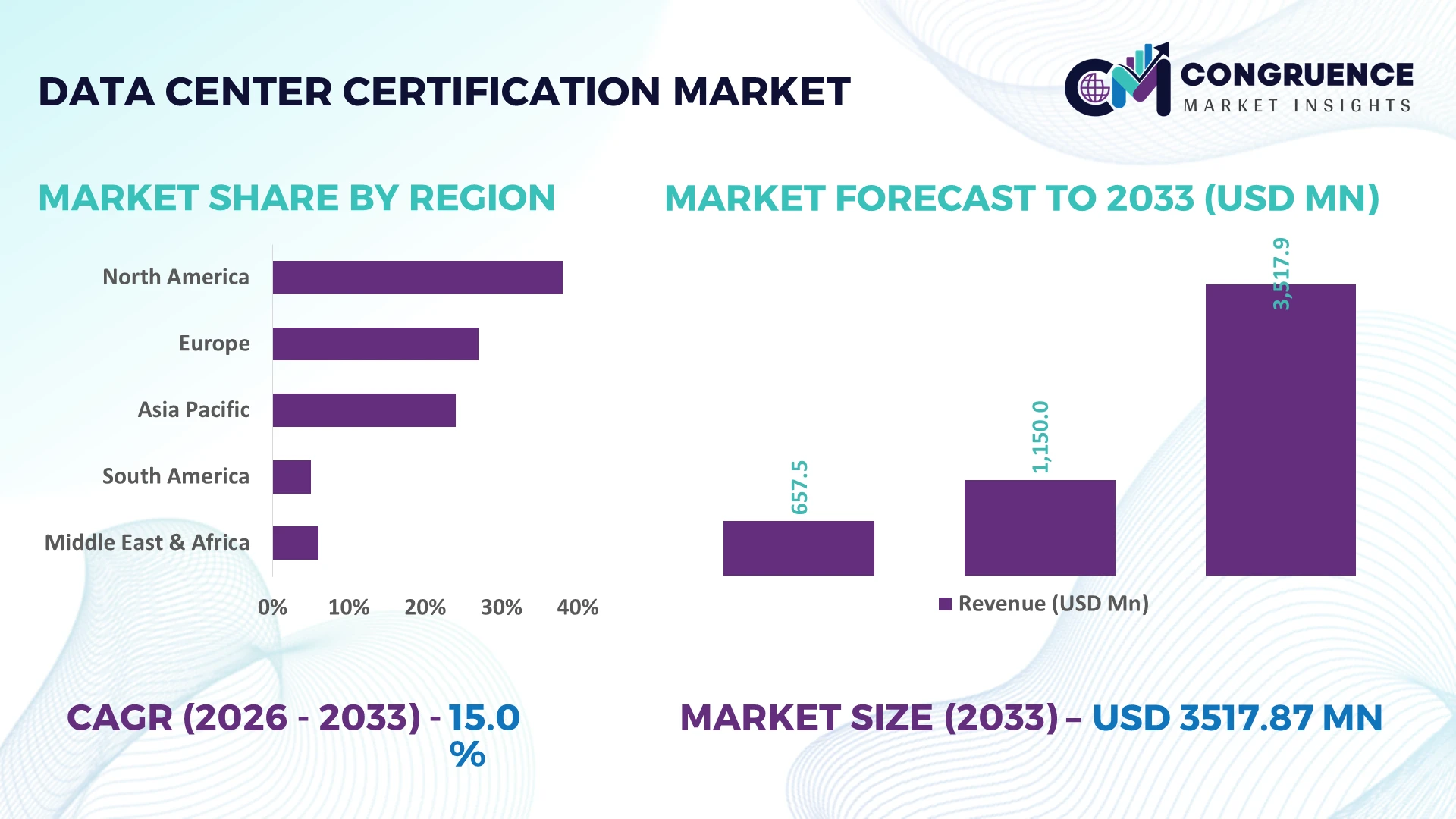

The Global Data Center Certification Market was valued at USD 1150 Million in 2025 and is anticipated to reach a value of USD 3517.87 Million by 2033 expanding at a CAGR of 15% between 2026 and 2033. Rising hyperscale AI infrastructure, stricter sustainability compliance, and enterprise adoption of globally recognized operational certification frameworks are accelerating certification demand across new and upgraded data center facilities.

The United States leads the global market with approximately 38% of certified data center capacity, supported by over USD 80 billion in AI and cloud infrastructure investments, large-scale hyperscale deployments, and financial services adoption. Compared with Germany's compliance-driven expansion, the U.S. maintains stronger certification penetration through advanced digital infrastructure and energy-efficiency programs. Growing AI infrastructure policies following global semiconductor supply-chain realignments further reinforce certification priorities across mission-critical facilities.

Organizations investing in internationally recognized certification programs gain stronger operational resilience, regulatory readiness, and competitive positioning as enterprise digital infrastructure becomes increasingly performance-driven.

Market Size & Growth: USD 1150 Million in 2025, reaching USD 3517.87 Million by 2033 at 15% CAGR, driven by AI-ready infrastructure and sustainability compliance.

Top Growth Drivers: AI data center expansion (+32%), ESG compliance adoption (+27%), and hyperscale cloud deployments (+24%) accelerate certification demand.

Short-Term Forecast: By 2028, certified facilities improve operational efficiency by 18% while reducing audit preparation time by 25%.

Emerging Technologies: AI monitoring, digital twins, and automated compliance platforms increase certification accuracy by over 30%.

Regional Leaders: North America exceeds USD 1.45 billion, Europe reaches USD 0.98 billion, and Asia-Pacific surpasses USD 0.82 billion, supported by regional digital infrastructure expansion.

Consumer/End-User Trends: Nearly 68% of enterprise operators prioritize certified facilities for cloud, colocation, and mission-critical workloads.

Pilot/Case Example: In 2026, an AI-ready hyperscale certification program reduced compliance validation cycles by 22% through automated assessment tools.

Competitive Landscape: Leading providers hold about 42% combined share alongside Uptime Institute, BICSI, TÜV organizations, SGS, and Bureau Veritas.

Regulatory & ESG Impact: Energy-efficiency standards reduce operational emissions by up to 20%, strengthening compliance across global facilities.

Investment & Funding: More than USD 9 billion supports certification-enabled digital infrastructure through strategic partnerships and facility modernization.

Innovation & Future Outlook: Next-generation AI-driven auditing, predictive compliance, and continuous digital certification strengthen resilience amid evolving global supply-chain requirements.

Growing investment in hyperscale campuses, edge computing facilities, and AI-ready infrastructure continues to expand certification opportunities across enterprise, government, and colocation environments. Automated compliance platforms, digital auditing, and sustainability assessment tools improve certification efficiency by nearly 30%, while stricter operational resilience requirements and evolving energy regulations strengthen demand. These developments establish a solid foundation for the strategic market discussion.

Data center certification has become a strategic differentiator as enterprises prioritize operational resilience, regulatory compliance, and AI-ready digital infrastructure. Certification increasingly influences investment decisions, colocation selection, and procurement standards across financial services, healthcare, and public-sector deployments. Infrastructure modernization and stricter energy-efficiency regulations are reshaping certification requirements, while global semiconductor supply-chain restructuring continues to encourage standardized facility design and resilient operational practices.

Modern AI-enabled compliance platforms complete documentation reviews and continuous monitoring nearly 35% faster than traditional manual audit processes while reducing recurring compliance costs by approximately 20%. The United States leads large-scale deployment through hyperscale infrastructure and advanced operational frameworks, whereas Singapore emphasizes high-density, sustainability-focused certified facilities supported by strict environmental standards. Over the next two to three years, automated compliance validation is expected to exceed 50% of new certification workflows, improving deployment consistency and reducing recertification timelines.

A practical example is hyperscale operators integrating digital monitoring, predictive maintenance, and sustainability reporting into certification programs before commissioning new facilities. Leading organizations are expanding partnerships with certification bodies, infrastructure consultants, and digital compliance technology providers while increasing investment in continuous assessment platforms. Companies embedding certification into infrastructure planning secure stronger operational resilience, faster enterprise customer acquisition, and a durable competitive advantage in an increasingly compliance-driven digital ecosystem.

Rapid expansion of AI computing infrastructure and enterprise compliance requirements is strengthening demand for advanced data center certification. More than 70% of newly planned hyperscale facilities incorporate certification targets during design, while AI workloads increase power-density requirements by over 30%, requiring validated operational standards. The United States continues expanding certified mission-critical infrastructure following accelerated cloud and semiconductor investments, encouraging standardized facility performance. Certification providers are responding through digital audit platforms, strategic partnerships, and continuous compliance services that reduce assessment cycles by nearly 25%. A key strategic insight is that certification is increasingly influencing procurement qualification, making compliance capability a competitive asset rather than a post-construction requirement.

Certification programs require significant investment in documentation, testing, energy optimization, and operational validation, creating barriers for mid-sized operators. Initial compliance preparation can increase project implementation costs by 12–18%, while recertification activities consume nearly 15% more operational resources than conventional facility audits. Germany's increasingly stringent sustainability requirements add additional engineering complexity for older facilities requiring modernization. Companies are reducing exposure through standardized design templates, localized engineering partners, and long-term compliance contracts that improve implementation efficiency. The principal operational constraint lies in balancing certification quality with project timelines without delaying customer onboarding or infrastructure expansion.

AI-powered compliance management, digital twins, and continuous infrastructure monitoring are creating new opportunities beyond conventional certification services. Automated operational analytics improve compliance accuracy by approximately 30%, while predictive maintenance reduces audit-related corrective actions by nearly 22%. India is emerging as a strategic certification opportunity as large-scale digital infrastructure projects and cloud campuses adopt internationally aligned operational frameworks. Organizations are increasing R&D spending, developing integrated software platforms, and partnering with infrastructure specialists to deliver lifecycle certification services. An important strategic opportunity lies in subscription-based continuous certification models that strengthen customer retention while reducing long-term compliance costs.

Maintaining certification consistency across increasingly complex AI-enabled facilities requires specialized engineering expertise, cybersecurity integration, and standardized operational governance. Nearly 40% of operators report shortages of qualified compliance professionals, while integrated infrastructure environments increase assessment complexity by approximately 28%. Japan's high-density digital infrastructure highlights the challenge of aligning advanced cooling, power resilience, and sustainability objectives within evolving certification frameworks. Companies must strengthen workforce development, invest in automated verification technologies, and expand technical partnerships with engineering and cybersecurity specialists. Long-term competitive positioning will depend on scalable certification capabilities that maintain operational quality without slowing infrastructure deployment.

AI-Driven Compliance Automation: AI-enabled compliance platforms are replacing manual audit workflows, reducing documentation time by nearly 35% and improving validation accuracy by around 28%. Tightening operational standards for AI-ready infrastructure are accelerating digital assessment adoption in the United States. Certification providers are integrating predictive analytics, automated evidence collection, and workflow orchestration through technology partnerships, enabling faster certification cycles while lowering administrative overhead and improving audit consistency across large multi-site data center portfolios.

Continuous Certification Monitoring: Enterprises are shifting from periodic certification toward continuous compliance monitoring, with approximately 55% of newly commissioned facilities implementing real-time operational dashboards and automated performance tracking. Increasing cybersecurity expectations and evolving resilience regulations are driving this transition. Companies are restructuring service portfolios around subscription-based compliance management, allowing operators to detect deviations earlier, shorten corrective action timelines by nearly 20%, and improve long-term operational reliability.

Energy Performance Validation Expansion: Energy-focused certification has gained momentum as operators seek measurable efficiency improvements, with advanced monitoring reducing cooling-related energy consumption by up to 18% and improving power utilization tracking by 25%. Singapore and Nordic countries are strengthening operational benchmarks for sustainable facilities. Organizations are deploying digital energy management systems, collaborating with specialist engineering firms, and integrating carbon reporting into certification workflows to strengthen enterprise procurement competitiveness.

Integrated Multi-Standard Assessments: Organizations increasingly pursue combined operational, security, and sustainability certifications through unified assessment frameworks, reducing duplicate audit activities by approximately 30% and shortening project completion timelines by nearly 22%. Growing labor shortages among qualified compliance professionals are accelerating process consolidation. Certification bodies are expanding digital platforms and strategic alliances to deliver integrated assessment services, creating a non-obvious competitive advantage through standardized global governance and simplified enterprise compliance management.

Operational Certification remains the leading segment because enterprises increasingly prioritize continuous operational resilience, infrastructure reliability, and standardized management practices after facility commissioning. Nearly 42% of certification engagements now focus on operational performance, reflecting stronger demand from hyperscale operators and colocation providers managing mission-critical environments. Design Certification maintains strategic importance by embedding compliance requirements during planning, while Facility Certification continues supporting physical infrastructure validation for new developments. Security Certification gains importance as cybersecurity governance becomes integrated into infrastructure operations, encouraging certification providers to expand digital verification capabilities and compliance partnerships.

Energy Certification represents the fastest-growing segment as operators respond to stricter efficiency targets and sustainability requirements. Adoption has increased by approximately 26% across newly developed AI-ready facilities, while integrated certification packages improve audit efficiency by almost 20%. Companies are expanding technology partnerships, developing digital assessment platforms, and offering combined certification services to strengthen long-term customer retention. Investment priorities increasingly favor lifecycle certification models that integrate operational, energy, and security performance into a unified compliance framework.

Hyperscale Data Centers account for the largest application segment because large AI clusters, cloud infrastructure, and mission-critical digital services require internationally recognized operational validation. Approximately 46% of new hyperscale projects include certification objectives during infrastructure planning, strengthening deployment consistency and enterprise procurement confidence. Enterprise Data Centers continue investing in operational modernization to support hybrid IT strategies, while Colocation Data Centers leverage certification to differentiate service quality and attract regulated industries with demanding compliance requirements.

Edge Data Centers represent the fastest-growing application as distributed digital infrastructure expands closer to industrial sites and urban demand centers. Deployment activity has increased by roughly 30% over recent planning cycles, supported by automation and remote infrastructure management. Cloud Facilities continue integrating continuous compliance technologies to streamline operations across geographically distributed assets. Companies are scaling digital monitoring, expanding regional deployment partnerships, and integrating automated compliance tools, reflecting a strategic shift toward standardized certification across both centralized and distributed infrastructure ecosystems.

Data Center Operators represent the dominant end-user group because they manage the largest concentration of mission-critical facilities requiring ongoing operational validation, resilience assessments, and customer assurance. More than 48% of certification demand originates from operators expanding hyperscale and colocation capacity while standardizing compliance across multiple facilities. Cloud Providers are increasing certification investments to support AI services and multi-region infrastructure consistency. IT & Telecom organizations continue strengthening network resilience through certified operational frameworks, while Government agencies emphasize compliance for national digital infrastructure programs.

Cloud Providers are the fastest-growing end-user segment as AI computing, sovereign cloud initiatives, and enterprise migration accelerate infrastructure expansion. Certification adoption among large cloud operators has increased by approximately 29%, while BFSI organizations continue prioritizing certified facilities to strengthen operational continuity and regulatory readiness. Certification providers are responding through customized compliance frameworks, strategic alliances with infrastructure partners, and scalable digital audit services tailored to sector-specific operational requirements, improving customer retention and long-term ecosystem competitiveness.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 17.2% CAGR between 2026 and 2033.

Advanced Compliance Integration Across Hyperscale Infrastructure

North America remains the largest regional market as hyperscale expansion, AI infrastructure deployment, and enterprise compliance requirements continue accelerating certification activity. The region contributes nearly 39% of global certification demand, supported by mature cloud ecosystems and large-scale colocation investments. More than 65% of newly commissioned hyperscale facilities integrate certification targets during the planning stage, improving operational resilience and procurement readiness. Digital compliance automation, continuous operational monitoring, and integrated sustainability verification are becoming standard practices. Certification providers are strengthening consulting capabilities, expanding digital assessment platforms, and forming strategic partnerships with infrastructure engineering firms to shorten implementation timelines while improving audit consistency.

United States Market Outlook: The United States leads the regional market through its concentration of hyperscale campuses, cloud providers, financial institutions, and AI computing infrastructure. More than 45% of large enterprise data center projects include internationally recognized certification requirements before commissioning. Federal cybersecurity priorities, corporate sustainability initiatives, and extensive digital infrastructure modernization continue strengthening certification demand. Operators increasingly integrate automated compliance platforms and predictive operational monitoring, allowing standardized governance across multi-site facilities while improving infrastructure reliability and customer confidence.

Sustainability Standards Reshape Infrastructure Strategy

Europe maintains a strong position through rigorous operational governance, sustainability targets, and advanced digital infrastructure policies. Approximately 28% of global certification activity originates from the region, where operators increasingly align facilities with energy-efficiency and resilience standards. Modernization programs across enterprise and colocation infrastructure encourage integrated operational and environmental certification. Around 58% of newly developed facilities include advanced energy performance validation as part of commissioning activities. Certification organizations continue expanding digital assessment services and technical partnerships to support standardized compliance while reducing administrative complexity across multinational operations.

Germany Market Outlook: Germany remains Europe's strategic certification hub due to its advanced industrial ecosystem, enterprise digitalization, and emphasis on operational reliability. Large financial institutions, manufacturing enterprises, and cloud providers continue investing in certified mission-critical facilities. More than 60% of newly upgraded enterprise data centers incorporate structured energy management and operational certification frameworks. The country's engineering expertise and regulatory consistency support high-quality implementation while encouraging long-term investment in resilient digital infrastructure.

Digital Infrastructure Expansion Accelerates Adoption

Asia-Pacific represents the fastest-expanding market as governments and private enterprises rapidly scale cloud infrastructure, AI computing, and digital transformation initiatives. The region accounts for approximately 24% of global certification demand, supported by large hyperscale developments and expanding edge deployments. More than 35% of planned AI-ready facilities are integrating certification objectives during early infrastructure design. Companies are investing in automated compliance platforms, regional engineering partnerships, and standardized operational governance to support faster commissioning while maintaining internationally aligned infrastructure performance across increasingly complex deployments.

India Market Outlook: India is emerging as the region's most dynamic certification market due to sustained cloud investment, expanding colocation capacity, and nationwide digital infrastructure initiatives. Large technology companies and infrastructure developers increasingly require certification during design and operational phases. Nearly 40% of newly announced enterprise-scale facilities include structured sustainability and operational validation objectives. Domestic engineering expertise, favorable digital policies, and accelerating AI infrastructure deployment continue strengthening certification opportunities across both public and private sectors.

Enterprise Modernization Strengthens Compliance Demand

South America is experiencing steady certification adoption as enterprises modernize digital infrastructure and international cloud providers expand regional operations. The region contributes roughly 5% of global certification activity, with Brazil accounting for the largest deployment concentration. More than 30% of new colocation developments now include internationally recognized certification objectives to attract multinational customers. Infrastructure limitations remain in selected markets, yet operators continue investing in standardized operational governance, energy optimization, and automated compliance systems to improve competitiveness and strengthen service reliability.

Brazil Market Outlook: Brazil leads regional deployment through expanding cloud infrastructure, financial sector modernization, and increasing demand for certified colocation facilities. Enterprise operators continue upgrading existing infrastructure with integrated operational and energy certification programs. Approximately half of newly commissioned large-scale facilities incorporate advanced compliance planning before commercial operation. Strategic investment from international cloud providers and growing enterprise digitalization reinforce Brazil's position as the primary certification market within South America.

Strategic Infrastructure Investment Drives Transformation

The Middle East & Africa market is strengthening as governments prioritize digital infrastructure, smart city development, and sovereign cloud initiatives. The region represents approximately 4% of global certification activity while recording increasing deployment of certified hyperscale and enterprise facilities. More than 25% of recently announced digital infrastructure projects incorporate internationally recognized operational certification objectives. Operators are expanding partnerships with engineering specialists and compliance providers while integrating sustainability validation into large infrastructure programs to improve long-term operational resilience and investor confidence.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional certification adoption through extensive smart infrastructure investments, advanced connectivity, and strong enterprise digital transformation initiatives. Large hyperscale developments and government-backed digital programs continue expanding demand for internationally recognized certification frameworks. Around 45% of newly announced premium data center developments include integrated operational and sustainability certification planning. Strong regulatory support, strategic geographic positioning, and continued investment in AI-ready infrastructure reinforce the country's leadership in certified digital infrastructure deployment.

The market is led by Uptime Institute, TÜV SÜD, Bureau Veritas, SGS, and BICSI, competing directly against regional certification specialists and engineering consultancies expanding digital compliance services. The top five participants collectively account for approximately 54% of certification activity, while regional firms compete through localized expertise and faster project execution. Global leaders differentiate through technology-enabled assessments, international recognition, and multi-country delivery capabilities, whereas regional providers emphasize customization and regulatory familiarity. AI-enabled compliance platforms reduce audit preparation time by nearly 30%, while integrated certification workflows shorten project completion by approximately 22%, shifting competition toward digital efficiency rather than pricing alone. Companies are expanding through strategic partnerships with infrastructure consultants, cloud operators, and engineering firms while integrating continuous monitoring platforms into certification portfolios. Market consolidation is increasing as enterprise customers seek end-to-end compliance solutions instead of standalone assessments. Strong accreditation, technical credibility, and global operational consistency remain the primary entry barriers. Winning depends on scalable digital compliance, internationally trusted certification frameworks, and lifecycle service integration.

Uptime Institute

BICSI

TÜV SÜD

SGS

Bureau Veritas

DNV

DEKRA

Intertek Group

UL Solutions

NQA

BSI Group

LRQA

Current technology adoption is centered on AI-enabled compliance automation, digital audit platforms, and continuous infrastructure monitoring. Around 58% of newly certified enterprise facilities now utilize automated evidence collection, reducing documentation effort by approximately 35% while improving assessment accuracy by nearly 28%. Digital workflow integration enables faster collaboration between operators, engineering consultants, and certification bodies, minimizing operational disruption and improving certification consistency across geographically distributed facilities.

Emerging technologies include digital twins, predictive compliance analytics, and IoT-enabled infrastructure validation. Compared with conventional manual inspection methods, integrated digital assessment platforms reduce compliance verification time by nearly 40% while lowering recurring operational costs by approximately 20%. Hyperscale operators and cloud providers benefit most because these technologies support standardized governance across multiple facilities. Companies increasingly integrate cybersecurity monitoring, energy management, and operational reporting into unified certification ecosystems, strengthening infrastructure resilience while simplifying enterprise compliance management.

Between 2026 and 2028, autonomous compliance engines, AI-assisted risk modeling, and continuous digital certification are expected to become mainstream operational capabilities. Adoption across large enterprise and hyperscale environments is projected to exceed 65%, driven by expanding AI infrastructure and stricter operational governance. Organizations investing early in integrated compliance technologies will achieve faster deployment, stronger audit readiness, improved customer confidence, and a sustained competitive advantage over operators relying on legacy certification workflows.

November 2024 – Uptime Institute introduced an enhanced Management & Operations (M&O) Stamp of Approval, expanding the framework with 7 new operational assessment areas and advanced workforce evaluation tools. The update strengthens operational resilience, standardization, and continuous risk management across enterprise data center portfolios. Source: uptimeinstitute.com

June 2025 – UL Solutions launched a dedicated testing and certification service for immersion cooling fluids used in AI-driven data centers. The new program validates compliance under the UL 2417 outline, enabling safer deployment of high-density cooling technologies and accelerating enterprise adoption of liquid-cooled infrastructure. Source: securityinfowatch.com

September 2025 – Digi Power X announced its ARMS 200 modular AI platform achieved Tier 3 ANSI/TIA-942-C certification following an independent audit by EPI Certification. The certification strengthens procurement competitiveness for hyperscale and enterprise projects while validating high-availability infrastructure performance. Source: marketscreener.com

January 2026 – BSI launched its global Data Center Mark of Trust to address rapidly expanding AI infrastructure requirements, certifying its first implementation with BK Gulf. The modular framework supports 2 certification versions covering facilities and services, strengthening regulatory confidence and internationally standardized compliance. Source: bsigroup.com

This report provides comprehensive analysis of the Data Center Certification Market across Design Certification, Facility Certification, Operational Certification, Energy Certification, and Security Certification, covering deployment across colocation, enterprise, hyperscale, edge, and cloud facilities. It evaluates demand from data center operators, cloud providers, IT & telecom organizations, government agencies, and BFSI institutions, while assessing technology adoption, certification frameworks, operational governance, digital compliance platforms, and sustainability-focused infrastructure practices. More than 70% of new hyperscale developments now integrate certification objectives during planning, highlighting the strategic importance of standardized operational validation.

The study delivers detailed regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, examining deployment concentration, enterprise modernization, regulatory alignment, and infrastructure investment priorities. It supports investment planning, competitive benchmarking, market entry, partnership evaluation, and expansion strategy between 2026 and 2033. Coverage also includes emerging opportunities in AI-enabled compliance automation, continuous certification platforms, digital auditing, and integrated sustainability assessment, enabling informed decisions across rapidly evolving digital infrastructure ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 1150 Million |

Market Revenue in 2033 | USD 3517.87 Million |

CAGR (2026 - 2033) | 15% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Uptime Institute, BICSI, TÜV SÜD, SGS, Bureau Veritas, DNV, DEKRA, Intertek Group, UL Solutions, NQA, BSI Group, LRQA |

Customization & Pricing | Available on Request (10% Customization is Free) |