Reports

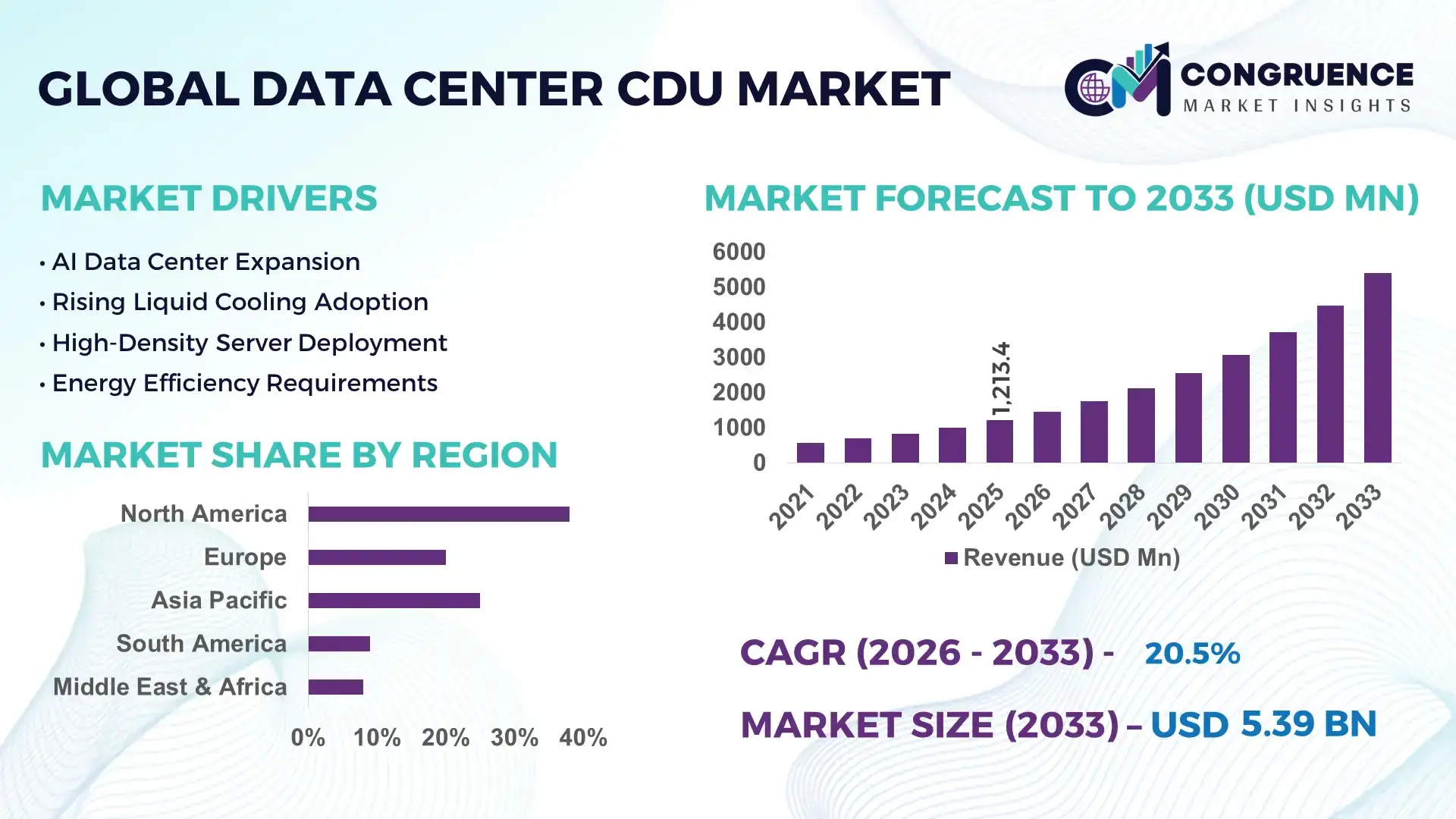

The Global Data Center CDU Market was valued at USD 1213.43 Million in 2025 and is anticipated to reach a value of USD 5394.02 Million by 2033 expanding at a CAGR of 20.5% between 2026 and 2033.

Rapid deployment of AI accelerators, high-density GPU clusters, and liquid-cooled hyperscale facilities is accelerating CDU adoption globally, with advanced liquid-cooling systems improving thermal transfer efficiency by nearly 35% while reducing facility-level cooling energy consumption by over 20% compared to conventional air-cooling infrastructure. Between 2024 and 2026, tightening European energy-efficiency regulations and ongoing U.S.-China semiconductor trade restrictions accelerated regional investments in localized AI-ready data center ecosystems. Average rack density in AI-focused facilities exceeded 40 kW during 2025 versus 12–15 kW in traditional enterprise environments, forcing operators to shift toward direct-to-chip and immersion cooling architectures.

The United States dominated the global Data Center CDU market in 2025 with nearly 38% share of installed liquid-cooling capacity supported by more than USD 45 billion in hyperscale and AI infrastructure investments across Virginia, Texas, and Arizona. More than 55% of newly commissioned hyperscale facilities integrated intelligent CDU systems with automated thermal monitoring capabilities, while deployment of immersion cooling and rear-door heat exchanger technologies increased by approximately 28% year-over-year. Compared with several European markets constrained by power availability and stricter sustainability thresholds, U.S. operators achieved faster scaling through stronger utility infrastructure and higher AI infrastructure spending intensity.

The market is transitioning from conventional cooling optimization toward integrated liquid thermal management ecosystems, making CDU efficiency, scalability, and automation core competitive factors for hyperscale operators and infrastructure technology providers.

Market Size & Growth: USD 1213.43 Million in 2025 reaching USD 5394.02 Million by 2033 at 20.5% CAGR driven by AI-ready liquid cooling expansion.

Top Growth Driver 1: AI infrastructure deployment increased CDU demand by 42% across hyperscale facilities in 2025.

Top Growth Driver 2: Direct-to-chip cooling adoption rose 31% as rack density exceeded 40 kW globally.

Top Growth Driver 3: Edge data center expansion accelerated advanced CDU installations by 28% during 2024–2026.

Short-Term Forecast: By 2027, advanced CDU systems are projected to reduce cooling energy usage by 25%.

Emerging Technologies: AI thermal analytics, immersion cooling, and modular liquid-cooling systems improved operational efficiency by 30%.

Regional Leaders: North America exceeded USD 2.1 billion, Europe crossed USD 1.3 billion, while Asia-Pacific recorded 29% deployment growth.

Consumer/End-User Trends: More than 55% of new hyperscale facilities integrated liquid-cooled CDU systems for GPU-intensive workloads.

Pilot/Case Example: A 2025 Texas AI data center project reduced cooling downtime by 18% using intelligent CDU monitoring.

Competitive Landscape: Top manufacturers controlled nearly 48% share led by Vertiv, Schneider Electric, STULZ, Rittal, and CoolIT Systems.

Regulatory, Investment & Future Outlook: Over USD 12 billion in AI infrastructure investments accelerated smart CDU innovation amid stricter global energy-efficiency regulations.

Hyperscale cloud providers contributed nearly 46% of total CDU demand in 2025, followed by AI research infrastructure and semiconductor manufacturing facilities with combined contribution exceeding 32%. Intelligent coolant monitoring platforms, modular liquid distribution architectures, and immersion-ready CDU systems emerged as major product innovations improving thermal efficiency by approximately 30%. North America maintained dominant deployment activity, while Asia-Pacific recorded nearly 29% growth supported by semiconductor expansion and regional cloud investments. Increasing localization of semiconductor and server supply chains, combined with stricter sustainability regulations, is accelerating adoption of advanced liquid-cooling ecosystems. The market is steadily evolving toward fully automated, AI-optimized thermal management infrastructure across next-generation data centers.

The Data Center CDU market is rapidly transforming into a strategic infrastructure segment as hyperscale operators, AI cloud providers, and semiconductor companies prioritize liquid cooling to manage escalating thermal loads from GPU-intensive computing environments. Rack density in AI-focused facilities surpassed 40 kW during 2025, forcing operators to redesign cooling architectures for performance optimization and energy efficiency. Increasing deployment of generative AI infrastructure, combined with rising power utilization costs, is accelerating capital allocation toward intelligent CDU systems capable of real-time thermal management and predictive monitoring.

Global supply chain restructuring and stricter sustainability mandates are reshaping procurement and deployment strategies across the industry. Advanced direct-to-chip liquid cooling improves thermal efficiency by nearly 35% while reducing operational cooling costs by approximately 22% compared to legacy air-cooling systems. North America leads in deployment volume due to hyperscale expansion, while Asia-Pacific leads in innovation adoption with nearly 29% annual growth in immersion-ready CDU integration. By 2028, intelligent CDU platforms are expected to reduce data center cooling downtime by over 20% through AI-driven thermal analytics and automated flow optimization. ESG-focused cooling systems are also becoming competitive differentiators by lowering water consumption and supporting compliance with stricter carbon-efficiency benchmarks.

A 2025 AI infrastructure deployment in Texas improved thermal stability by 18% after integrating modular CDU systems with automated coolant balancing technology. Major infrastructure providers are shifting investments toward scalable liquid-cooling ecosystems, advanced monitoring software, and regional manufacturing expansion to secure long-term competitive positioning. Companies capable of optimizing cooling efficiency, deployment scalability, and energy compliance simultaneously are establishing decisive advantages in the next generation of AI-driven data center infrastructure.

AI training clusters, hyperscale cloud expansion, and high-density GPU workloads are forcing rapid adoption of advanced CDU systems globally. Average rack density exceeded 40 kW in 2025 compared to 12–15 kW in conventional facilities, making liquid cooling essential for operational stability. Advanced CDU integration improved thermal efficiency by nearly 35% while reducing cooling-related energy usage by over 20%. Between 2024 and 2026, semiconductor supply chain restructuring and hyperscale AI investments accelerated liquid-ready infrastructure deployment across North America and Asia-Pacific. More than 55% of newly commissioned hyperscale facilities integrated intelligent CDU platforms with automated monitoring capabilities. In response, manufacturers are expanding regional production, increasing R&D investment, and forming strategic cooling technology partnerships to secure long-term AI infrastructure contracts.

High infrastructure conversion costs and limited supplier concentration are constraining large-scale CDU deployment across enterprise and colocation environments. Retrofitting legacy air-cooled facilities with liquid cooling systems increases initial infrastructure costs by nearly 30%, while procurement lead times for precision pumps and heat exchangers increased approximately 20% during 2025. Power infrastructure limitations and stricter sustainability regulations across Europe and parts of Asia are further delaying deployment scalability. These pressures directly impact expansion timelines, operational budgets, and cooling standardization efforts. To reduce risk exposure, major operators are diversifying supplier networks, securing long-term procurement agreements, and investing in modular CDU architectures that simplify deployment across mixed cooling environments.

AI-enabled thermal management systems, immersion-ready cooling infrastructure, and predictive analytics platforms are creating major growth opportunities across the Data Center CDU market. Intelligent CDU integration improved cooling efficiency by nearly 30% while reducing maintenance-related downtime by approximately 18% during 2025 hyperscale deployments. Asia-Pacific and Middle Eastern markets are witnessing accelerated investment in sovereign AI infrastructure and semiconductor manufacturing ecosystems, increasing immersion-compatible CDU deployment by nearly 27%. A key non-obvious opportunity is the integration of CDU systems with AI-based facility optimization software capable of automating coolant flow, thermal balancing, and predictive servicing. Leading companies are positioning for long-term dominance through smart cooling software development, regional manufacturing expansion, and strategic partnerships with hyperscale cloud and AI infrastructure providers.

Scaling advanced CDU infrastructure across hyperscale and enterprise environments presents major operational and infrastructure challenges. A significant percentage of existing facilities remain optimized for less than 15 kW rack density, while AI-focused facilities now exceed 40 kW, creating complex retrofit and compatibility barriers. Cooling integration failures can increase operational downtime risk by nearly 15%, directly impacting hyperscale service continuity and infrastructure reliability. Grid constraints across North America and Europe are also slowing expansion of power-intensive AI facilities, while advanced liquid-cooling deployments increase implementation costs by approximately 20% compared to conventional systems. To remain competitive, companies must accelerate investment in modular CDU platforms, predictive monitoring technologies, and interoperable cooling ecosystems capable of supporting scalable AI-ready infrastructure under increasingly strict energy-efficiency requirements.

Liquid cooling deployment up 55% across hyperscale facilities as AI server density exceeded 40 kW per rack during 2025. Operators are replacing legacy air-cooling systems with direct-to-chip architectures improving thermal efficiency by nearly 35% while reducing cooling-related energy usage by over 20%. This operational shift is forcing CDU manufacturers to expand modular production capacity, restructure supply agreements, and strengthen integration partnerships with GPU infrastructure providers to support faster deployment cycles and higher thermal loads.

Intelligent monitoring adoption increased 31% as operators integrated AI-based thermal analytics and predictive maintenance platforms into CDU systems. Automated coolant management reduced cooling downtime by approximately 18% and improved operational efficiency by nearly 22% across high-density facilities. Labor shortages in specialized infrastructure management are accelerating deployment of autonomous cooling optimization platforms capable of reducing manual intervention while improving operational continuity across multi-site data center networks.

Immersion-compatible CDU installations grew 29% across Asia-Pacific due to semiconductor expansion, sovereign AI infrastructure programs, and localized supply chain investments. North America continues leading deployment volume, while Asia-Pacific leads faster adoption of advanced liquid-cooling ecosystems through aggressive hyperscale construction and regional manufacturing integration. This shift is redefining competitive positioning for global CDU suppliers expanding local assembly, service operations, and immersion-ready product portfolios.

Modular CDU adoption crossed 48% as operators prioritized scalable and retrofit-friendly cooling infrastructure for mixed deployment environments. Standardized CDU platforms reduced installation timelines by nearly 26% while improving maintenance flexibility and deployment speed across colocation and enterprise facilities. Stricter energy-efficiency regulations and rising operational power costs are forcing companies to optimize long-term thermal performance through scalable CDU ecosystems and service-based cooling management models.

The Data Center CDU market is segmented by type, application, and end-user, with demand increasingly concentrated around liquid-ready hyperscale infrastructure and AI-intensive computing environments. Liquid-Cooled CDU systems account for a dominant share of advanced deployments due to their ability to support rack densities exceeding 40 kW while reducing cooling-related energy consumption by more than 20%. Hyperscale Data Centers represent the largest application segment with nearly 45% demand share driven by accelerated AI infrastructure expansion and GPU cluster deployment. Cloud Providers and IT & Telecom companies collectively contribute over 60% of market demand as operators prioritize scalable thermal management infrastructure capable of supporting high-density workloads. Demand is steadily shifting toward modular, intelligent, and immersion-compatible CDU systems as operators optimize efficiency, reduce downtime risks, and strengthen long-term infrastructure scalability across rapidly expanding AI ecosystems.

Liquid-Cooled CDU dominates the market with nearly 46% share due to higher thermal efficiency, scalability for AI workloads, and compatibility with direct-to-chip cooling systems. These platforms improve cooling efficiency by nearly 35% while reducing operational energy usage by over 20% compared to Air-Cooled CDU systems. Rack-Mounted CDU is the fastest-growing segment with deployment growth exceeding 30% during 2025 as operators prioritize modular and space-efficient cooling infrastructure for hyperscale facilities. Standalone CDU and Air-Cooled CDU collectively account for nearly 38% share, maintaining demand across retrofit projects and enterprise facilities requiring deployment flexibility. Manufacturers are accelerating investment in intelligent liquid-cooling platforms and modular CDU expansion to capture growing AI-ready infrastructure demand.

“According to a 2025 report by the Uptime Institute, liquid-cooled CDU systems were adopted by over 52% of hyperscale data center operators, resulting in nearly 30% improvement in thermal efficiency and significant reduction in cooling-related operational strain, reinforcing their growing strategic importance.”

Hyperscale Data Centers lead the market with approximately 45% demand share driven by AI infrastructure expansion and GPU-intensive computing workloads. High-Performance Computing is the fastest-growing application segment with deployment growth exceeding 33% during 2025 as semiconductor firms and AI research facilities accelerated adoption of advanced liquid-cooling systems. Compared with mature hyperscale deployments focused on operational scale, Edge Data Centers are increasing demand for modular and low-latency cooling infrastructure. Colocation Facilities and Edge Data Centers together contribute nearly 37% market share due to rising distributed computing and cloud migration activity. Companies are repositioning product portfolios toward immersion-compatible and intelligent CDU platforms to support evolving high-density infrastructure requirements.

“According to a 2025 report by the International Data Corporation, advanced CDU systems were deployed across more than 3,500 hyperscale and high-performance computing facilities globally, improving processing efficiency by nearly 28% and reducing thermal instability risks significantly, highlighting rapid operational adoption.”

Cloud Providers dominate the market with nearly 38% share due to large-scale hyperscale expansion, AI model training demand, and continuous deployment of high-density GPU infrastructure. Government is the fastest-growing end-user segment with adoption growth exceeding 27% during 2025, supported by sovereign AI investments and national digital infrastructure programs. Compared with Cloud Providers prioritizing infrastructure scale and automation, BFSI organizations increasingly focus on secure and energy-efficient cooling systems for mission-critical operations. IT and Telecom along with BFSI collectively account for nearly 42% market demand driven by cloud migration and rising edge computing workloads. Vendors are strengthening partnerships and customized liquid-cooling offerings to capture demand from AI-ready enterprise and government infrastructure projects.

“According to a 2025 report by the International Energy Agency, adoption among cloud providers increased by 34%, with over 2,000 operators implementing advanced liquid-cooling CDU solutions, leading to nearly 24% improvement in cooling energy optimization, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23.1% between 2026 and 2033.

North America leads in deployment scale due to hyperscale AI infrastructure expansion and high-density liquid-cooling adoption across cloud facilities. Europe contributed nearly 27% share driven by strict energy-efficiency compliance and sustainable cooling modernization. Asia-Pacific accounted for approximately 29% of deployment activity during 2025 as semiconductor manufacturing and sovereign AI investments accelerated advanced CDU integration. While North America dominates operational scale, Asia-Pacific leads infrastructure expansion speed and immersion-cooling adoption. Europe remains strongest in sustainability-driven thermal optimization. Semiconductor supply chain restructuring and regional AI infrastructure investments are shifting competitive priorities toward localized liquid-cooling ecosystems. Companies are increasingly prioritizing North American hyperscale projects and Asia-Pacific manufacturing expansion to secure long-term deployment advantages.

North America holds nearly 38% share of the global Data Center CDU market due to rapid hyperscale AI infrastructure deployment and increasing GPU-intensive workloads across cloud environments. The United States dominates regional demand as operators deploy liquid-cooling systems supporting rack densities above 40 kW. More than 55% of newly commissioned hyperscale facilities integrated intelligent CDU platforms during 2025, reducing cooling-related energy usage by over 20%. Semiconductor supply chain localization and large-scale AI infrastructure funding are accelerating regional deployment activity. Enterprises increasingly prioritize scalable and automated cooling ecosystems with predictive monitoring capabilities, driving strong investment in modular CDU expansion and advanced thermal management infrastructure across hyperscale facilities.

Europe accounted for nearly 27% of the global Data Center CDU market during 2025, led by Germany, the Netherlands, and the Nordic countries. Strict carbon-efficiency regulations and rising electricity costs are forcing operators to optimize thermal management infrastructure through liquid-cooling adoption. Advanced CDU deployment improved facility-level cooling efficiency by approximately 28% while supporting compliance with aggressive sustainability targets. More than 48% of new hyperscale projects integrated intelligent cooling systems with automated monitoring capabilities during 2025. Enterprises increasingly prioritize energy-efficient and low-water-consumption cooling platforms to meet ESG and operational performance requirements. The region is pushing manufacturers toward innovation-focused cooling technologies optimized for long-term efficiency, compliance, and infrastructure resilience.

Asia-Pacific accounted for approximately 29% of global Data Center CDU deployment activity during 2025 driven by semiconductor manufacturing expansion, sovereign AI initiatives, and hyperscale cloud infrastructure growth across China, Japan, South Korea, and India. Immersion-compatible CDU installations increased nearly 29% as operators accelerated deployment of high-density AI facilities. Regional manufacturers are strengthening localized production and supply chain integration to reduce deployment lead times by approximately 22%. Enterprises increasingly prioritize scalable and cost-efficient cooling ecosystems capable of supporting rapid infrastructure expansion. Aggressive hyperscale construction activity and localized semiconductor ecosystems are positioning Asia-Pacific as the critical growth and manufacturing hub for advanced CDU deployment strategies.

South America contributed nearly 7% share of the global Data Center CDU market during 2025, with Brazil and Chile leading regional deployment activity due to increasing cloud adoption and colocation infrastructure expansion. Rising digital transformation projects and enterprise data processing requirements are accelerating demand for modular liquid-cooling systems across urban data center clusters. However, infrastructure funding limitations and power availability constraints continue restricting large-scale hyperscale deployment. CDU adoption across advanced facilities increased approximately 18% during 2025 as operators focused on improving cooling efficiency and operational stability. Enterprises remain highly price-sensitive, prioritizing scalable and retrofit-friendly cooling platforms. The region presents strong long-term opportunity but requires infrastructure modernization and localized service expansion to support sustainable deployment growth.

Middle East & Africa accounted for approximately 6% of global Data Center CDU demand during 2025, driven by digital infrastructure modernization and sovereign technology investments across the UAE, Saudi Arabia, and South Africa. Large-scale AI infrastructure projects and smart city development programs are accelerating deployment of advanced liquid-cooling ecosystems. CDU integration across high-density facilities increased nearly 21% during 2025 as operators prioritized thermal optimization and energy-efficiency improvement. Strategic partnerships between hyperscale operators and regional infrastructure developers are expanding localized deployment capabilities. Enterprises increasingly favor scalable and climate-optimized cooling platforms capable of supporting high-temperature operating environments. The region is emerging as a strategic infrastructure expansion zone for advanced CDU manufacturers targeting long-term digital transformation projects.

United States – 38% market share: The U.S. Data Center CDU market dominates due to aggressive hyperscale AI infrastructure expansion, high-density GPU deployment, and strong cloud computing investments.

China – 21% market share: China leads large-scale CDU deployment through rapid semiconductor manufacturing growth, sovereign AI initiatives, and accelerated hyperscale data center construction.

The Data Center CDU market is characterized by intense competition between global thermal management leaders, hyperscale-focused cooling innovators, and regional infrastructure specialists. Vertiv, Schneider Electric, STULZ, Rittal, and CoolIT Systems collectively control nearly 48% market share, competing aggressively across hyperscale AI infrastructure and liquid-cooling deployments. Global leaders focus on intelligent CDU platforms, predictive monitoring software, and integrated thermal ecosystems, while regional manufacturers compete through lower-cost modular deployment and localized service capabilities.

Competition is increasingly centered on cooling efficiency, deployment scalability, customization speed, and supply chain control. Advanced liquid-cooling systems improve thermal efficiency by nearly 35% while reducing operational cooling energy usage by over 20%, forcing vendors to accelerate innovation and infrastructure partnerships. Companies are expanding regional manufacturing, strengthening GPU server integration partnerships, and investing in immersion-ready CDU technologies to capture rising AI infrastructure demand. Growing transition toward modular liquid-cooling ecosystems is accelerating competitive consolidation and increasing pressure on conventional air-cooling suppliers. Winning in this market requires scalable liquid-cooling innovation, rapid deployment capability, and strong hyperscale infrastructure partnerships.

Vertiv

Schneider Electric

STULZ

Rittal

CoolIT Systems

Boyd Corporation

Motivair Corporation

Delta Electronics

Nortek Air Solutions

Asetek

nVent

Chilldyne

Submer

Fujitsu

Advanced direct-to-chip liquid cooling systems are becoming the core technology standard across AI-ready data centers as rack density exceeds 40 kW in hyperscale environments. Compared with legacy air-cooling infrastructure, liquid-cooled CDU systems improve thermal efficiency by nearly 35% while reducing cooling-related energy consumption by over 20%. More than 55% of newly commissioned hyperscale facilities integrated liquid-ready CDU platforms during 2025, accelerating demand for modular and high-capacity thermal management ecosystems. This transition is optimizing operational stability for GPU-intensive workloads while enabling faster AI infrastructure scaling.

AI-based thermal analytics and predictive cooling management platforms are reshaping operational execution across large-scale facilities. Intelligent CDU monitoring systems reduced cooling downtime by approximately 18% while improving coolant flow optimization efficiency by nearly 22% during advanced deployments. Operators are increasingly integrating automated monitoring software with immersion-ready CDU platforms to reduce labor dependency and improve multi-site operational continuity. Hyperscale cloud providers and semiconductor firms are benefiting most from these technologies due to rising compute density and continuous infrastructure utilization requirements.

Immersion cooling and hybrid liquid-air cooling architectures are emerging as disruptive technologies between 2026 and 2028 as AI workloads push rack density beyond 100 kW. Advanced hybrid cooling systems reduced annual cooling energy usage by nearly 70% compared to traditional cooling configurations while improving deployment flexibility across retrofit environments. Manufacturers are accelerating investment in intelligent modular CDU ecosystems, GPU-integrated thermal platforms, and localized production expansion to secure competitive advantage as AI infrastructure deployment rapidly intensifies.

June 2025 – Vertiv launched the CoolChip CDU 600 supporting up to 600 kW liquid-cooling capacity for AI and HPC deployments, improving scalable thermal management for high-density GPU clusters. The launch strengthened Vertiv’s hyperscale liquid-cooling portfolio expansion strategy. [AI Cooling Scale]

March 2025 – Vertiv introduced the CoolLoop Trim Cooler with up to 3 MW cooling capacity, reducing annual cooling energy consumption by nearly 70% in hybrid liquid-air deployments. The system accelerated energy-efficient cooling adoption across AI-ready data centers. [Energy Optimization Push]

October 2024 – Schneider Electric acquired a 75% stake in Motivair to expand advanced liquid-cooling capabilities for AI-focused data center infrastructure. The acquisition strengthened Schneider Electric’s position in direct-to-chip cooling and high-density CDU deployment markets. [Cooling Portfolio Expansion]

March 2024 – Schneider Electric inaugurated a new Bengaluru cooling facility with nearly 85% export-focused production capacity targeting advanced liquid-cooling systems. The expansion improved regional manufacturing scale and accelerated Asia-Pacific cooling equipment deployment. [Regional Manufacturing Shift]

The Data Center CDU Market report provides detailed coverage across product types including Air-Cooled CDU, Liquid-Cooled CDU, Rack-Mounted CDU, and Standalone CDU, along with key applications such as Hyperscale Data Centers, Colocation Facilities, Edge Data Centers, and High-Performance Computing environments. The report further evaluates demand trends across major end-users including IT and Telecom, Cloud Providers, BFSI, and Government sectors. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa with focused assessment of regional deployment patterns, cooling infrastructure adoption, and AI-driven thermal management transformation.

The report analyzes more than 10 major market participants and evaluates strategic shifts across intelligent cooling systems, immersion-compatible CDU platforms, and AI-based thermal monitoring technologies. Liquid-cooled CDU systems accounted for nearly 46% of deployment demand during 2025, while hyperscale facilities contributed approximately 45% of application concentration. The study also tracks operational indicators including cooling efficiency improvement exceeding 30%, adoption of modular CDU infrastructure above 48%, and increasing deployment of AI-integrated thermal optimization platforms.

The report supports investment planning, infrastructure expansion, supplier benchmarking, and competitive positioning by identifying high-growth deployment environments, emerging cooling technologies, regional infrastructure shifts, and execution-level adoption trends shaping the global Data Center CDU market between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1213.43 Million |

|

Market Revenue in 2033 |

USD 5394.02 Million |

|

CAGR (2026 - 2033) |

20.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Vertiv, Schneider Electric, STULZ, Rittal, CoolIT Systems, Boyd Corporation, Motivair Corporation, Delta Electronics, Nortek Air Solutions, Asetek, nVent, Chilldyne, Submer, Fujitsu |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |