Reports

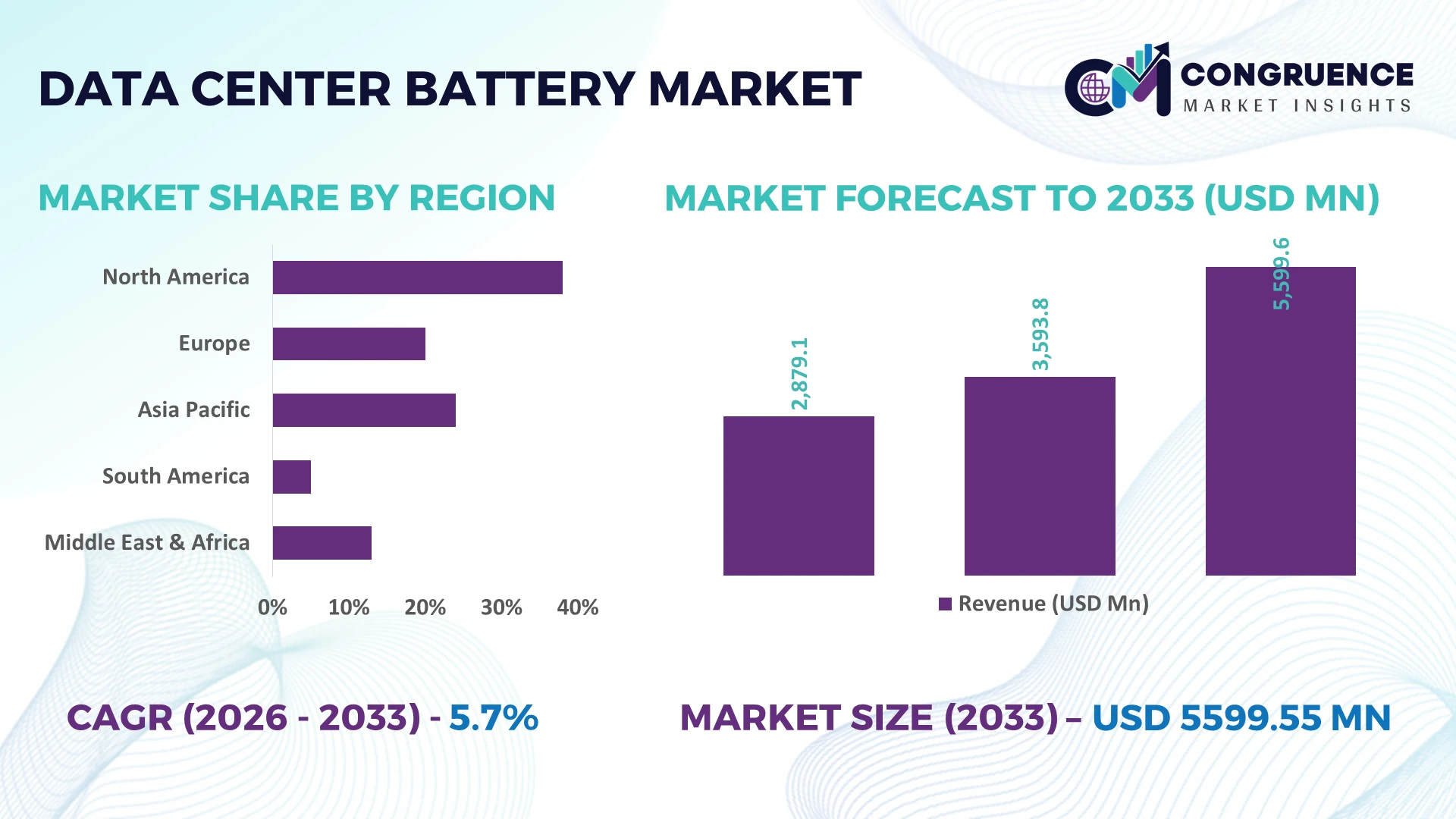

The Global Data Center Battery Market was valued at USD 3593.8 Million in 2025 and is anticipated to reach a value of USD 5599.55 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. Rapid AI data center deployment, hyperscale capacity expansion, stricter uptime standards, and accelerated adoption of high-performance lithium-ion and intelligent battery monitoring systems are driving sustained investment across global backup power infrastructure.

The United States leads the global Data Center Battery Market with approximately 34% of installed battery backup capacity, supported by hyperscale cloud operators, AI computing facilities, and utility-scale grid modernization investments exceeding USD 70 billion. Compared with Germany's advanced colocation expansion, the U.S. deploys significantly higher rack density and battery monitoring technologies, while energy resilience initiatives strengthened following ongoing global semiconductor and energy supply chain realignments during 2026.

Organizations prioritizing scalable battery technologies, predictive maintenance, and resilient energy infrastructure are strengthening operational continuity while improving long-term infrastructure investment efficiency.

Market Size & Growth: USD 3593.8 Million in 2025, reaching USD 5599.55 Million by 2033 at 5.7% CAGR, driven by AI-ready hyperscale infrastructure and resilient backup power investments.

Top Growth Drivers: AI workload expansion (+38%), hyperscale capacity additions (+31%), and lithium-ion battery adoption (+27%) accelerate global deployment.

Short-Term Forecast: By 2028, intelligent battery monitoring reduces maintenance costs by 20% while improving backup system availability by 18%.

Emerging Technologies: AI-powered battery analytics, digital battery management systems, and advanced lithium iron phosphate solutions improve lifecycle performance by over 25%.

Regional Leaders: North America exceeds USD 2.1 billion, Asia-Pacific reaches USD 1.7 billion, and Europe surpasses USD 1.2 billion, supported by hyperscale expansion and energy resilience programs.

Consumer/End-User Trends: More than 62% of new hyperscale facilities prioritize lithium-ion battery systems over conventional alternatives for higher energy density.

Pilot/Case Example: 2026 AI-focused data center deployment achieved 24% lower backup power maintenance time through predictive battery monitoring integration.

Competitive Landscape: Top manufacturers collectively account for nearly 48% market share, with competition focused on battery efficiency, lifecycle performance, and integrated power solutions.

Regulatory & ESG Impact: Sustainable energy initiatives improve battery recycling participation by 30% while strengthening operational compliance across advanced facilities.

Investment & Funding: More than USD 9 billion supports manufacturing expansion, strategic partnerships, and localized supply chains amid regional infrastructure growth.

Innovation & Future Outlook: Next-generation solid-state concepts, intelligent energy management, and modular battery architectures strengthen high-density data center resilience.

Growing AI computing clusters, edge facilities, and hyperscale campuses continue to reshape the Data Center Battery Market, increasing demand for high-cycle lithium-ion systems and intelligent battery management platforms. More than 60% of new enterprise deployments integrate predictive battery analytics to improve uptime, while localized manufacturing and evolving sustainability requirements strengthen supply-chain resilience, setting the foundation for the strategic discussion that follows.

The Data Center Battery Market has become a strategic pillar of digital infrastructure as AI computing, cloud expansion, and enterprise continuity requirements redefine investment priorities. Operators increasingly view advanced battery systems as critical assets rather than passive backup equipment, driving infrastructure modernization alongside grid resilience initiatives. Supply-chain restructuring since 2026 has accelerated localized battery manufacturing and diversified sourcing strategies, reducing procurement risks while supporting faster deployment across hyperscale and colocation facilities.

Modern lithium-ion battery platforms deliver up to 35% lower maintenance requirements and nearly 25% higher energy density than conventional VRLA systems, enabling greater rack utilization and reduced operational downtime. The United States leads large-scale hyperscale deployments with widespread predictive battery management integration, while Japan emphasizes compact, high-efficiency energy storage for space-constrained facilities. Over the next two to three years, intelligent battery monitoring adoption is expected to exceed 65% of newly commissioned enterprise data centers, improving operational visibility and lifecycle management.

Large operators are deploying modular battery architectures integrated with AI-driven power management while expanding partnerships with battery manufacturers and energy technology providers. These investments improve resilience, shorten maintenance cycles, and strengthen procurement flexibility, positioning companies with superior power continuity capabilities to secure long-term competitive advantage in an increasingly performance-driven digital infrastructure landscape.

Rapid AI infrastructure deployment and increasing rack power density are accelerating demand for high-performance battery systems capable of supporting uninterrupted operations. More than 68% of newly announced hyperscale facilities specify lithium-ion battery technology, while predictive battery management reduces unexpected failures by approximately 30%. The United States continues expanding AI data center capacity, supported by infrastructure modernization and domestic battery manufacturing initiatives that strengthen supply resilience. In response, leading companies are expanding production capacity, investing in intelligent battery analytics, and forming technology partnerships to integrate energy management platforms. A notable strategic shift is the convergence of battery monitoring with digital facility management, enabling operators to optimize replacement cycles, reduce lifecycle costs, and improve infrastructure reliability under continuously increasing computational workloads.

Battery manufacturing remains exposed to fluctuations in lithium, nickel, and critical mineral supply, creating cost uncertainty across procurement and deployment cycles. Battery material prices experienced swings exceeding 20% during recent global supply adjustments, while import dependency remains above 55% for several manufacturing economies. China continues to dominate critical battery processing, increasing sourcing concentration for global suppliers. These structural pressures affect project budgeting, inventory planning, and long-term procurement strategies for data center operators. Companies are reducing exposure by diversifying supplier networks, expanding localized assembly operations, and securing multi-year procurement contracts. Another operational response includes adopting alternative battery chemistries that reduce dependence on scarce raw materials while improving long-term procurement stability.

Next-generation battery ecosystems create opportunities beyond backup power by enabling predictive maintenance, grid interaction, and intelligent energy optimization. AI-enabled battery management systems improve asset utilization by nearly 28%, while modular battery platforms shorten installation time by approximately 22%. India is emerging as a strategic manufacturing and hyperscale infrastructure hub through supportive digital infrastructure policies and expanding domestic production capabilities. Companies are increasing R&D investments in lithium iron phosphate technologies, digital twin platforms, and integrated energy orchestration software. An emerging opportunity lies in batteries participating in facility-wide energy optimization strategies, allowing operators to reduce operational costs while improving resilience through real-time power balancing and automated performance analytics.

Increasing rack densities and AI computing workloads require battery systems that integrate seamlessly with sophisticated power architectures without compromising operational continuity. More than 45% of operators report integration complexity between legacy infrastructure and intelligent battery platforms, while skilled energy management professionals remain in limited supply across several advanced markets. Germany and other industrial economies face growing pressure to modernize existing facilities without disrupting mission-critical operations. Companies must strengthen workforce capabilities, standardize battery communication protocols, and invest in advanced digital monitoring infrastructure. Successfully addressing interoperability, predictive maintenance integration, and lifecycle optimization will determine long-term operational consistency and competitive differentiation as high-density computing environments continue expanding.

AI-Driven Battery Intelligence: More than 60% of newly commissioned hyperscale facilities are integrating AI-enabled battery management systems, reducing unplanned battery failures by nearly 30% and shortening inspection cycles by 25%. As rack densities continue increasing, operators are automating battery diagnostics and predictive maintenance workflows instead of relying on scheduled servicing. Technology vendors are expanding software partnerships and embedded analytics capabilities to improve uptime while lowering lifecycle maintenance costs across mission-critical environments.

Localized Manufacturing Expansion: Battery manufacturers are restructuring supply chains by increasing regional production, with localized assembly capacity expanding by over 22% and average procurement lead times declining nearly 18%. Continued geopolitical trade adjustments and critical mineral diversification strategies are encouraging enterprises in the United States and India to establish long-term sourcing agreements. Companies are balancing inventory, investing in domestic production, and strengthening supplier collaboration to improve deployment consistency and procurement resilience.

Lithium Iron Phosphate Adoption: Lithium iron phosphate battery deployments now represent approximately 45% of new enterprise installations because of improved thermal stability, longer operating life, and lower maintenance requirements. Operators report maintenance interventions declining by nearly 20% compared with conventional battery technologies. Manufacturers are accelerating product development, certification programs, and system integration partnerships as enterprise buyers prioritize operational reliability over short-term procurement costs.

Modular Energy Storage Integration: Modular battery architectures are reducing installation time by approximately 28% while increasing deployment flexibility across edge and colocation facilities. More than 50% of large-scale expansion projects now specify scalable battery modules that simplify future capacity upgrades without extensive infrastructure redesign. Companies are standardizing modular platforms, automating commissioning processes, and aligning battery deployments with evolving sustainability objectives to improve long-term operational efficiency.

Lithium-Ion remains the leading battery type because of its superior energy density, longer lifecycle, lower maintenance requirements, and compatibility with intelligent battery management systems. Nearly 65% of new hyperscale deployments specify lithium-ion solutions as operators prioritize reduced footprint and higher operational efficiency. Lead-Acid batteries continue serving cost-sensitive legacy facilities where existing infrastructure supports established maintenance practices, while Nickel-Based batteries maintain relevance in specialized environments requiring high-temperature tolerance. Companies are expanding lithium-ion manufacturing capacity, improving battery monitoring software, and strengthening integration with digital power infrastructure.

Solid-State Batteries represent the fastest-growing segment as enterprise operators seek improved safety, faster charging capability, and higher energy density for next-generation AI facilities. Flow Batteries remain strategically important for extended-duration backup applications where discharge time outweighs footprint considerations. Around 18% of pilot deployments now evaluate advanced battery chemistries for future scalability, prompting manufacturers to increase R&D partnerships and commercial validation programs. Investment priorities continue shifting toward intelligent, high-efficiency battery technologies capable of supporting increasingly dense computing environments.

Hyperscale Data Centers represent the largest application segment as AI infrastructure, cloud expansion, and high-density computing require resilient backup power architectures. Approximately 58% of advanced battery deployments are directed toward hyperscale facilities where uninterrupted operations remain operationally essential. UPS Systems continue serving as the foundation of enterprise power protection, while Backup Power applications remain critical for conventional facilities upgrading resilience capabilities. Companies are expanding modular battery integration and intelligent power management to support larger computing clusters with improved operational continuity.

Edge Data Centers are the fastest-growing application because distributed computing and low-latency services require localized power resilience closer to users. Deployment activity has increased by approximately 24% across enterprise edge networks, encouraging battery suppliers to develop compact, scalable solutions with simplified maintenance. Colocation Data Centers continue expanding battery investments to satisfy tenant uptime commitments and differentiated service agreements. Technology providers are strengthening automation capabilities, remote monitoring, and deployment partnerships to support increasingly distributed digital infrastructure requirements.

Cloud Providers remain the dominant end-user segment because they operate the world's largest hyperscale infrastructure portfolios and require continuous investment in resilient power systems. Nearly 60% of advanced battery deployments support cloud computing facilities, where AI processing and digital services significantly increase power continuity requirements. IT & Telecom organizations continue modernizing legacy infrastructure to improve network availability, while Colocation Providers expand battery capacity to strengthen customer service-level commitments. Manufacturers are developing customized battery configurations and integrated monitoring platforms to address varying operational requirements across enterprise environments.

Healthcare represents the fastest-growing end-user segment as digital diagnostics, electronic health records, and connected medical infrastructure increase dependence on uninterrupted computing environments. Battery deployment activity within healthcare facilities has expanded by approximately 21%, supported by modernization initiatives and resilient infrastructure planning. BFSI institutions continue investing in advanced backup systems to support high-availability transaction processing, while Government organizations upgrade critical digital infrastructure through modernization programs. Companies are strengthening ecosystem partnerships, tailored service offerings, and lifecycle management capabilities to compete across increasingly specialized customer segments.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 6.8% CAGR between 2026 and 2033.

AI Infrastructure Accelerates High-Density Power Modernization

North America maintains the largest position in the Data Center Battery Market due to extensive hyperscale deployments, mature cloud infrastructure, and rapid AI data center expansion. The region contributes nearly 38.4% of global demand, supported by advanced battery management integration and strong enterprise investment in resilient backup power systems. More than 65% of newly commissioned hyperscale facilities specify lithium-ion battery platforms with intelligent monitoring capabilities. Operators continue modernizing critical power architecture through modular energy storage deployments and long-term technology partnerships, improving maintenance efficiency and operational continuity while supporting increasing rack power densities across digital infrastructure.

United States Market Outlook: The United States remains the region's operational center, driven by large hyperscale campuses, AI computing investments, and advanced battery manufacturing initiatives. More than 70% of North America's hyperscale capacity is concentrated in the country, encouraging suppliers to expand domestic production and strengthen strategic partnerships with cloud operators. Enterprise investment continues prioritizing predictive battery management, modular deployment, and resilient energy infrastructure to support continuously increasing computational workloads.

Sustainability Standards Reshape Critical Power Infrastructure

Europe continues strengthening its position through energy efficiency regulations, sustainable infrastructure investments, and modernization of enterprise and colocation facilities. Approximately 24% of global battery deployments are associated with European data center projects emphasizing operational resilience and lower environmental impact. Adoption of lithium iron phosphate systems has increased by nearly 22% across newly developed facilities as operators align infrastructure with evolving sustainability objectives. Companies are investing in battery recycling partnerships, digital energy management platforms, and advanced monitoring technologies that improve operational reliability while supporting long-term infrastructure modernization.

Germany Market Outlook: Germany leads the European market through strong industrial capabilities, advanced engineering expertise, and expanding colocation investments. Large enterprise operators continue upgrading legacy facilities with intelligent battery management and modular backup systems. More than 40% of new high-capacity data center projects incorporate advanced lithium-ion infrastructure, reflecting the country's focus on energy efficiency, digital transformation, and resilient industrial computing operations.

Manufacturing Scale Fuels Infrastructure Expansion

Asia-Pacific is emerging as the fastest-growing market, supported by large-scale battery manufacturing, expanding hyperscale investments, and accelerating digital infrastructure development. The region accounts for approximately 31% of global deployment activity, while battery production capacity continues increasing through domestic manufacturing expansion. More than 25% of recently announced enterprise facilities incorporate modular battery architectures to improve deployment flexibility and lifecycle efficiency. Companies continue strengthening localized production, technology partnerships, and supply-chain integration to support growing enterprise demand while improving procurement resilience.

China Market Outlook: China dominates regional manufacturing through extensive battery production capacity, integrated supply chains, and large-scale cloud infrastructure expansion. The country produces a substantial share of global lithium-ion battery components while supporting continuous hyperscale construction activity. Domestic manufacturers are investing in automated production, advanced battery chemistries, and intelligent monitoring technologies, enabling faster deployment and stronger cost competitiveness across enterprise infrastructure projects.

Cloud Expansion Strengthens Infrastructure Demand

South America is experiencing increasing battery deployment as cloud investment, enterprise digitalization, and colocation expansion improve regional infrastructure capabilities. Brazil represents the largest deployment concentration, while enterprise modernization programs continue increasing demand for resilient backup power systems. Approximately 18% of recently commissioned facilities integrate intelligent battery monitoring platforms to improve maintenance planning and operational reliability. Infrastructure limitations remain in selected markets, prompting operators to prioritize modular deployment strategies and phased expansion supported by technology partnerships and localized service networks.

Brazil Market Outlook: Brazil serves as the primary operational hub for regional data center development through expanding cloud investments and enterprise digital transformation. Major colocation providers continue increasing backup power capacity to support financial services, telecommunications, and government workloads. Ongoing investment in resilient electrical infrastructure and battery modernization enables operators to strengthen service continuity while supporting growing enterprise demand for high-availability computing environments.

Digital Infrastructure Investment Accelerates Modernization

The Middle East & Africa market is advancing through government-backed digital transformation initiatives, hyperscale investments, and expanding enterprise infrastructure projects. Regional operators increasingly deploy advanced battery technologies to improve resilience in high-temperature operating conditions and support mission-critical facilities. Nearly 20% of recently announced large-scale projects include intelligent battery monitoring and modular backup systems as part of integrated power infrastructure planning. Companies continue forming strategic technology partnerships while investing in localized engineering capabilities to improve operational reliability and deployment efficiency.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through significant investments in hyperscale facilities, smart city initiatives, and digital economy development. Enterprise operators continue deploying advanced lithium-ion battery systems integrated with intelligent power management platforms. Strong government support for digital infrastructure and international technology partnerships has accelerated construction of resilient data center ecosystems capable of supporting rapidly expanding AI and cloud computing workloads.

The Data Center Battery Market is led by Eaton, Schneider Electric, Vertiv, EnerSys, and East Penn Manufacturing, competing against regional battery manufacturers, specialized lithium-ion providers, and integrated power infrastructure vendors. Global technology leaders compete through intelligent energy management and turnkey solutions, while regional manufacturers emphasize cost efficiency and localized supply. The top five companies collectively control approximately 47% of the market, reflecting moderate consolidation with strong competition across enterprise and hyperscale projects. Technology performance, lifecycle cost, and deployment speed remain primary differentiators, with lithium-ion systems reducing maintenance by nearly 30% and modular architectures shortening installation time by about 25%. Leading vendors are expanding manufacturing, forming battery technology partnerships, integrating digital monitoring platforms, and strengthening vertical supply chains to secure critical components. Competition is shifting toward software-enabled battery intelligence and localized production rather than hardware alone. High certification requirements, product reliability expectations, and long qualification cycles create significant entry barriers. Winning requires integrated power ecosystems, resilient supply chains, predictive battery analytics, and scalable deployment capabilities.

Eaton

Schneider Electric

Vertiv

EnerSys

East Penn Manufacturing

Exide Technologies

GS Yuasa Corporation

Leoch International Technology Limited

Saft

Toshiba Corporation

Hitachi Energy

Huawei Digital Power Technologies

Delta Electronics

Contemporary Amperex Technology Co., Limited (CATL)

Advanced lithium-ion batteries, intelligent battery management systems, and AI-driven predictive analytics define current technology leadership across the Data Center Battery Market. More than 60% of newly deployed hyperscale facilities integrate digital battery monitoring, reducing unexpected failures by nearly 30% while improving maintenance planning. Cloud operators and colocation providers benefit most because real-time diagnostics extend asset life and improve operational resilience across high-density computing environments.

Emerging technologies include lithium iron phosphate batteries, digital twins for power infrastructure, and modular battery architectures designed for scalable expansion. Compared with conventional VRLA batteries, modern lithium-ion platforms provide approximately 25% higher energy density and reduce maintenance requirements by nearly 35%. Around 45% of new enterprise installations now favor lithium iron phosphate chemistry because of enhanced thermal stability, longer lifecycle, and simplified integration with automated facility management platforms.

Between 2026 and 2028, solid-state battery development, AI-powered energy orchestration, and advanced battery recycling technologies are expected to reshape competitive positioning. Manufacturers investing in intelligent software integration and modular energy ecosystems will strengthen deployment flexibility while reducing operational costs by approximately 20%. Companies acting now through strategic R&D, manufacturing expansion, and technology partnerships will secure stronger differentiation as enterprise buyers increasingly prioritize lifecycle performance, predictive intelligence, and resilient digital infrastructure over conventional backup power solutions.

December 2025: Vertiv launched the EnergyCore Grid battery energy storage system featuring integrated lithium iron phosphate technology for data center applications, supporting modular deployments from 1 MW to over 200 MW. The platform strengthens grid resilience and accelerates power availability for AI infrastructure. Source: vertiv.com

April 2026: Vertiv partnered with CPower to integrate battery energy storage with virtual power plant capabilities, successfully deploying a 1 MW microgrid at its Ohio Customer Experience Center. The collaboration improves interconnection speed, enables demand-response participation, and enhances energy asset utilization for data centers. Source: datacenterdynamics.com

May 2026: Schneider Electric introduced its next-generation integrated Battery Energy Storage System with battery-agnostic architecture and advanced digital intelligence, enabling scalable energy storage while improving deployment flexibility. The solution supports 100% integrated cell-to-grid architecture, strengthening resilient infrastructure strategies. Source: pv-magazine-india.com

February 2026: Calibrant Energy announced a 23 MWh battery energy storage project at Iron Mountain's New Jersey data center, integrated with an existing 7.2 MW rooftop solar installation. The project enhances grid flexibility, strengthens operational resilience, and supports continuous low-carbon data center operations.

The report delivers comprehensive analysis of the global Data Center Battery Market across five battery types, five core applications, and six major end-user categories, supported by detailed assessment of North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates deployment trends, technology adoption, competitive positioning, and infrastructure modernization, with more than 60% of recent enterprise projects emphasizing intelligent battery management and advanced lithium-based systems.

The study examines operational strategies, supply-chain developments, battery innovations, and evolving power resilience requirements between 2026 and 2033. It provides strategic insights into hyperscale expansion, edge infrastructure, AI-driven power requirements, modular battery deployment, and emerging storage technologies while assessing investment priorities, partnership activity, enterprise adoption patterns, and competitive differentiation. The report supports expansion planning, portfolio optimization, market entry evaluation, procurement strategy, and long-term business positioning across mature and emerging data center ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3593.8 Million |

Market Revenue in 2033 | USD 5599.55 Million |

CAGR (2026 - 2033) | 5.7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Eaton, Schneider Electric, Vertiv, EnerSys, East Penn Manufacturing, Exide Technologies, GS Yuasa Corporation, Leoch International Technology Limited, Saft, Toshiba Corporation, Hitachi Energy, Huawei Digital Power Technologies, Delta Electronics, Contemporary Amperex Technology Co., Limited (CATL) |

Customization & Pricing | Available on Request (10% Customization is Free) |