Reports

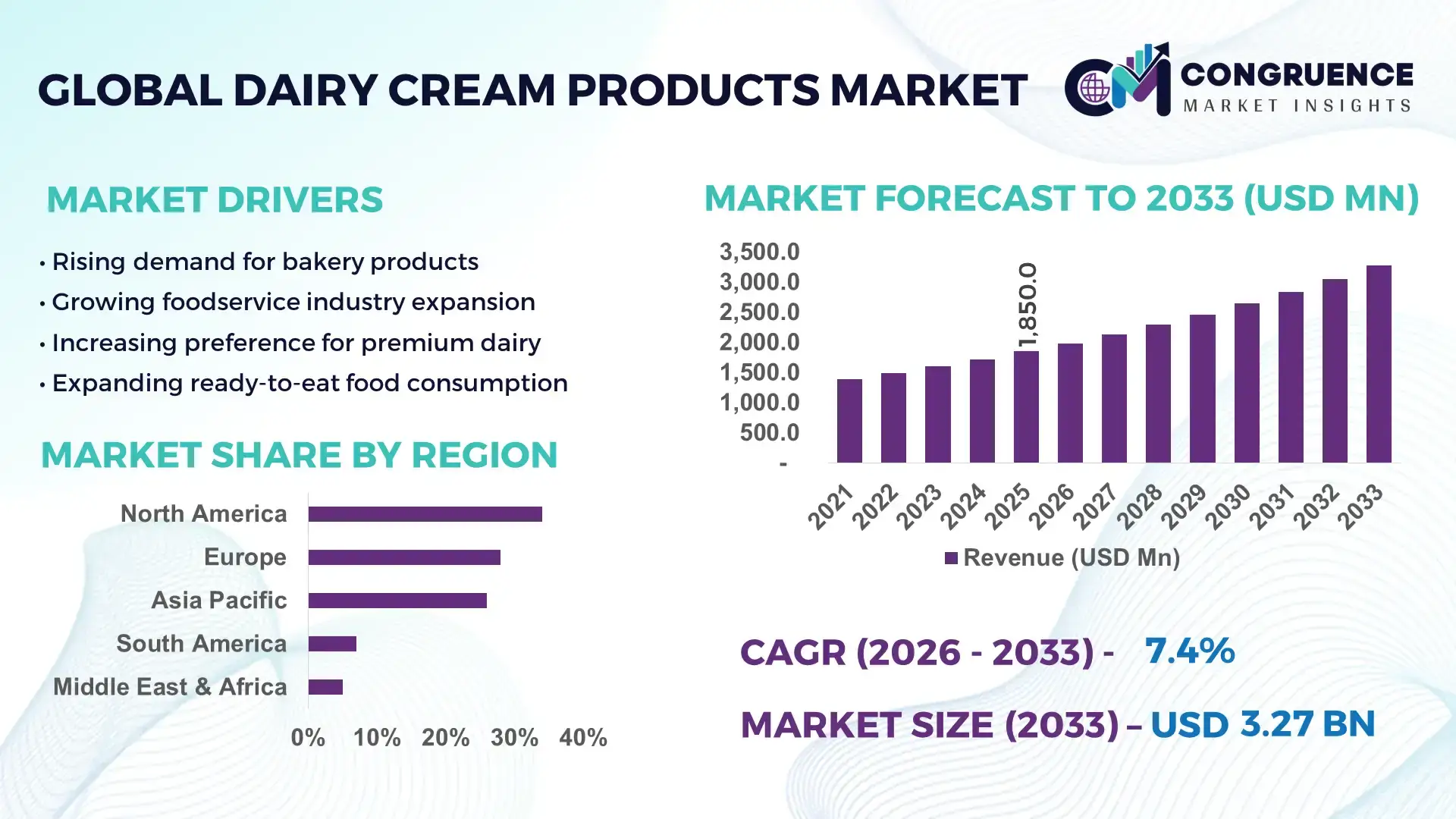

The Global Dairy Cream Products Market was valued at USD 1,850.0 Million in 2025 and is anticipated to reach a value of USD 3,275.0 Million by 2033 expanding at a CAGR of 7.4% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing demand for premium dairy-based desserts, bakery applications, and rising consumption of high-fat dairy products across urban populations.

The United States remains a key production hub in the Dairy Cream Products Market, supported by an annual milk production exceeding 100 billion kilograms, of which nearly 28% is processed into cream-based derivatives. Large-scale investments in automated dairy processing facilities have exceeded USD 2.5 billion annually, enabling high-efficiency cream separation and packaging systems. The foodservice sector accounts for over 35% of total cream consumption, driven by bakery chains and quick-service restaurants. Technological advancements such as ultra-high temperature (UHT) processing and extended shelf-life packaging have improved product stability by 40%, supporting long-distance distribution. Additionally, over 62% of consumers in the country regularly purchase cream-based products, highlighting strong domestic adoption supported by evolving dietary preferences and premiumization trends.

Market Size & Growth: USD 1,850.0 Million in 2025, projected to reach USD 3,275.0 Million by 2033, growing at 7.4% CAGR, driven by rising premium dairy consumption.

Top Growth Drivers: 65% increase in bakery demand, 48% rise in ready-to-eat desserts, 52% growth in foodservice cream usage.

Short-Term Forecast: By 2028, processing efficiency is expected to improve by 30% through automation and cold-chain optimization.

Emerging Technologies: UHT processing, aseptic packaging, and AI-based dairy quality monitoring systems.

Regional Leaders: North America (USD 1,020M by 2033, high QSR adoption), Europe (USD 890M, premium dairy focus), Asia-Pacific (USD 1,150M, rapid urban consumption growth).

Consumer/End-User Trends: Over 58% of urban consumers prefer high-fat dairy for taste enhancement in desserts and beverages.

Pilot or Case Example: In 2024, a European dairy processor achieved 22% waste reduction through AI-based cream separation systems.

Competitive Landscape: Market leader holds ~18% share; key players include Nestlé, Danone, Fonterra, Lactalis, and Arla Foods.

Regulatory & ESG Impact: Over 45% of producers adopting sustainable packaging aligned with carbon reduction mandates.

Investment & Funding Patterns: Over USD 3.2 billion invested globally in dairy processing modernization and cold-chain expansion.

Innovation & Future Outlook: Growth in plant-dairy hybrid creams and lactose-free innovations is reshaping product portfolios.

Dairy cream products are increasingly integrated across bakery (38%), confectionery (26%), and foodservice sectors (21%), with innovations such as lactose-free creams and plant-dairy blends gaining traction. Regulatory focus on clean labeling and sustainable sourcing is influencing production practices, while Asia-Pacific consumption is rising by over 40% in urban centers. Future growth is supported by premiumization and functional dairy product development.

The Dairy Cream Products Market holds strong strategic relevance as a critical component of the global dairy value chain, supporting high-margin applications across bakery, confectionery, and foodservice industries. Increasing demand for premium dairy formulations and functional food ingredients is reshaping production strategies, with manufacturers focusing on value-added cream variants such as lactose-free and fortified products. Advanced homogenization technology delivers 35% better texture consistency compared to conventional mechanical separation methods, enhancing product quality and shelf stability.

From a regional perspective, North America dominates in production volume, while Asia-Pacific leads in consumption adoption with over 54% of urban consumers regularly purchasing cream-based products. This contrast reflects strong industrial infrastructure in developed markets and rapidly expanding consumer bases in emerging economies. By 2028, AI-based dairy processing systems are expected to improve production efficiency by 28%, reducing operational waste and enhancing supply chain responsiveness.

Sustainability has become a key strategic pillar, with firms committing to reduce carbon emissions by 30% by 2030 through renewable energy adoption and recyclable packaging solutions. In 2025, a leading European dairy cooperative achieved a 25% reduction in water usage through advanced filtration technologies, demonstrating measurable ESG progress.

Looking ahead, the Dairy Cream Products Market is expected to evolve through digitalization, supply chain integration, and product innovation, positioning itself as a resilient and sustainable pillar within the global food industry.

The Dairy Cream Products Market is shaped by evolving consumer dietary preferences, expansion of processed food industries, and technological advancements in dairy processing. Increasing demand for high-fat dairy ingredients in bakery, confectionery, and ready-to-eat food segments is significantly influencing production volumes. Approximately 60% of cream demand is driven by industrial food processing applications, reflecting strong B2B consumption patterns. Additionally, improvements in cold-chain logistics have enhanced product shelf life by up to 35%, enabling wider geographic distribution. Emerging markets are witnessing increased dairy consumption due to urbanization and rising disposable incomes, with per capita dairy intake growing by over 20% in select regions. Meanwhile, regulatory frameworks focused on food safety, labeling, and sustainability are shaping operational practices. Innovations in packaging, including aseptic and recyclable formats, are further influencing market competitiveness, making the Dairy Cream Products Market highly dynamic and innovation-driven.

The rapid expansion of the bakery and confectionery industry is a major driver of the Dairy Cream Products Market, as cream is a critical ingredient in cakes, pastries, desserts, and fillings. Over 65% of bakery manufacturers globally rely on cream-based formulations to enhance texture and taste. The global bakery consumption index has risen by nearly 30% over the past five years, directly increasing demand for whipping and heavy creams. Additionally, the growth of café culture and quick-service restaurants has led to a 50% surge in demand for cream-based beverages and desserts. Premiumization trends are further boosting consumption, with more than 55% of consumers willing to pay higher prices for high-quality dairy ingredients. This rising preference for indulgent and premium food products continues to drive large-scale adoption of dairy cream products across both commercial and retail sectors.

Fluctuations in raw milk production present a significant challenge to the Dairy Cream Products Market, as cream is directly derived from milk fat. Seasonal variations, climate changes, and feed costs impact milk yield, causing supply inconsistencies. In many regions, milk production can fluctuate by up to 15% annually, affecting cream availability. Additionally, rising costs of cattle feed, which have increased by over 25% in recent years, place pressure on dairy farmers, leading to reduced output. Supply chain disruptions further exacerbate these challenges, especially in regions lacking robust cold-chain infrastructure. These factors result in inconsistent raw material availability and price volatility, limiting production planning and operational stability for dairy processors.

The increasing demand for lactose-free and hybrid dairy products offers significant opportunities for the Dairy Cream Products Market. Approximately 65% of the global population experiences some level of lactose intolerance, creating a large consumer base for alternative cream products. Manufacturers are introducing lactose-free creams and plant-dairy blends that maintain taste while improving digestibility. The adoption of these products has grown by over 40% in urban markets, particularly among health-conscious consumers. Additionally, innovations in enzymatic processing technologies have improved lactose breakdown efficiency by nearly 35%, enabling large-scale production. These advancements open new revenue streams and expand market reach across diverse consumer segments.

Stringent regulations related to food safety, labeling, and environmental sustainability present ongoing challenges for the Dairy Cream Products Market. Compliance with international standards requires significant investment in quality control systems and traceability technologies. Over 50% of dairy producers have had to upgrade processing facilities to meet new hygiene and safety requirements. Additionally, sustainability mandates, such as reducing carbon emissions and adopting eco-friendly packaging, have increased operational costs by up to 20%. The need to balance regulatory compliance with cost efficiency remains a critical challenge, particularly for small and medium-sized dairy processors operating in competitive markets.

• Surge in Premium and Artisanal Cream Consumption: Over 48% of urban consumers now prefer premium cream variants with higher fat content exceeding 35%, driven by demand for gourmet desserts and specialty beverages. Artisanal dairy products have seen a 32% increase in retail shelf presence, particularly in North America and Europe, reflecting evolving consumer taste preferences.

• Expansion of Lactose-Free and Functional Cream Products: Lactose-free cream adoption has grown by over 42% globally, with functional variants enriched with vitamins and probiotics gaining traction. Approximately 37% of health-conscious consumers actively seek dairy products with added nutritional benefits, supporting innovation in this segment.

• Growth in Foodservice and QSR Integration: The foodservice industry accounts for nearly 36% of total cream usage, with quick-service restaurants increasing cream-based menu offerings by 28%. Beverage chains report a 25% rise in demand for cream-based coffee and dessert drinks, indicating strong commercial utilization trends.

• Adoption of Advanced Processing and Packaging Technologies: More than 55% of dairy manufacturers are integrating automated cream separation and aseptic packaging systems, improving efficiency by 30% and extending shelf life by 40%. Smart packaging solutions with traceability features have also increased by 20%, enhancing supply chain transparency.

The Dairy Cream Products Market is segmented based on type, application, and end-user, reflecting diverse consumption patterns across industries. Heavy cream and whipping cream dominate due to their extensive use in bakery and foodservice applications, collectively accounting for over 60% of total consumption. Application-wise, bakery and confectionery segments lead, supported by increasing demand for premium desserts and ready-to-eat products. Foodservice remains a critical distribution channel, contributing significantly to overall demand, while retail consumption continues to grow with the availability of packaged cream products. End-user segmentation highlights strong demand from commercial establishments such as hotels, restaurants, and cafés, alongside rising household consumption. Emerging trends such as lactose-free products and plant-dairy blends are influencing segmentation dynamics, expanding the market into health-conscious and specialty product categories.

Heavy cream leads the Dairy Cream Products Market, accounting for approximately 38% of total consumption due to its high fat content and versatility in culinary applications. Whipping cream follows with around 27% share, widely used in desserts and beverages. However, lactose-free cream is the fastest-growing segment, expanding at an estimated 8.6% CAGR, driven by increasing lactose intolerance awareness and health-focused consumption. Light cream and double cream collectively contribute nearly 35% share, catering to niche culinary and regional applications. Innovations in processing technologies are enhancing product consistency and shelf life, supporting broader adoption across both commercial and retail sectors.

• In 2025, a major dairy processor introduced advanced UHT-treated heavy cream with 40% extended shelf life, enabling distribution across over 20 international markets.

Bakery and confectionery applications dominate the Dairy Cream Products Market, accounting for nearly 42% of total usage due to high demand for cakes, pastries, and desserts. Foodservice applications hold around 30%, supported by increasing café culture and QSR expansion. The beverages segment is the fastest-growing, with an estimated 8.9% CAGR, driven by rising consumption of specialty coffee and cream-based drinks. Other applications, including ready-to-eat meals and packaged foods, collectively contribute approximately 28% share. In 2025, over 45% of global consumers reported increased consumption of cream-based desserts, while 38% of foodservice operators expanded cream-based menu offerings to meet demand.

• In 2024, a global coffee chain expanded its cream-based beverage portfolio across 1,500 outlets, increasing sales of specialty drinks by 18%.

The foodservice sector leads the Dairy Cream Products Market with approximately 44% share, driven by high demand from restaurants, cafés, and hotels. Household consumption accounts for around 34%, supported by rising retail availability and home baking trends. The industrial food processing sector is the fastest-growing, expanding at an estimated 8.2% CAGR due to increased use in packaged foods and desserts. Other end-users, including catering and institutional buyers, contribute roughly 22% share. In 2025, more than 40% of households reported regular use of cream in cooking and baking, while 36% of foodservice businesses increased cream procurement to meet rising demand.

• In 2025, a large bakery chain adopted automated cream dispensing systems across 300 outlets, improving operational efficiency by 20%.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2026 and 2033.

North America’s dominance is supported by high dairy consumption levels exceeding 85 kg per capita annually and strong foodservice penetration. Europe follows with approximately 28% share, driven by premium dairy product demand and established processing infrastructure. Asia-Pacific holds around 26% share, with rapid urbanization and increasing dairy intake boosting demand. South America and Middle East & Africa collectively contribute nearly 12%, supported by growing dairy industries and expanding retail networks. Consumption growth in Asia-Pacific has exceeded 35% in urban regions, while Europe has seen a 20% rise in premium cream product adoption.

North America holds approximately 34% share of the Dairy Cream Products Market, driven by strong demand from bakery, confectionery, and quick-service restaurant industries. The region benefits from advanced dairy processing infrastructure, with over 70% of facilities adopting automated systems. Government support for dairy farmers and strict food safety regulations ensure high-quality production standards. Technological advancements such as UHT processing and smart packaging have improved product shelf life by over 40%. A leading regional player has invested heavily in sustainable packaging, reducing plastic usage by 25%. Consumer behavior indicates higher preference for premium and organic dairy products, with over 60% of consumers willing to pay a premium for quality.

Europe accounts for around 28% of the Dairy Cream Products Market, with key markets including Germany, France, and the UK. Regulatory frameworks emphasizing sustainability and clean labeling are driving product innovation. Over 50% of dairy producers have adopted eco-friendly packaging solutions to meet EU standards. Advanced processing technologies are widely implemented, improving efficiency by 30%. A major European dairy cooperative has introduced carbon-neutral cream production processes, reducing emissions by 20%. Consumers in this region prioritize organic and sustainably sourced products, with nearly 45% preferring eco-labeled dairy items.

Asia-Pacific represents approximately 26% of the Dairy Cream Products Market, with strong growth in China, India, and Japan. Rising disposable incomes and urbanization are key drivers, with dairy consumption increasing by over 35% in metropolitan areas. The region is witnessing significant investment in dairy processing infrastructure, with over 40% of facilities upgrading to modern technologies. A leading regional company has expanded production capacity by 30% to meet growing demand. Consumer behavior is influenced by convenience and affordability, with increasing preference for packaged and ready-to-use cream products.

South America holds nearly 7% share of the Dairy Cream Products Market, led by Brazil and Argentina. The region benefits from strong dairy farming capabilities, with milk production increasing by over 18% in recent years. Government incentives supporting dairy exports have boosted production levels. Infrastructure improvements and cold-chain development have enhanced distribution efficiency by 25%. A regional dairy company has introduced new cream-based products targeting urban consumers, increasing sales by 15%. Consumer demand is driven by affordability and growing interest in processed dairy foods.

Middle East & Africa accounts for approximately 5% of the Dairy Cream Products Market, with growth driven by rising urbanization and expanding retail sectors. Countries such as UAE and South Africa are key contributors, with dairy consumption increasing by over 20% in urban areas. Investments in cold-chain infrastructure have improved product availability by 30%. A local dairy producer has expanded its distribution network across multiple countries, enhancing market reach. Consumer behavior reflects increasing demand for packaged and long shelf-life dairy products, supported by changing dietary patterns.

United States – 28% Market share: Driven by large-scale dairy production and strong foodservice demand

Germany – 16% Market share: Supported by advanced processing technologies and premium dairy consumption

The Dairy Cream Products Market is moderately fragmented, with over 120 active global and regional competitors operating across different value chain segments. The top five companies collectively account for approximately 42% of the total market share, indicating a competitive yet consolidated structure among leading players. Key market participants focus on product innovation, particularly in lactose-free and premium cream variants, to differentiate their offerings. Strategic initiatives such as mergers, acquisitions, and partnerships are increasingly common, with over 25 major deals recorded in the past three years.

Companies are also investing heavily in automation and digital transformation, with nearly 55% of large-scale producers adopting advanced processing technologies. Sustainability initiatives, including eco-friendly packaging and carbon reduction strategies, are becoming critical competitive factors. Additionally, regional players are expanding their presence through localized production and distribution networks, intensifying competition across emerging markets.

Danone

Fonterra

Lactalis

Arla Foods

Dean Foods

Saputo Inc.

Dairy Farmers of America

FrieslandCampina

Amul

Britannia Industries

Yili Group

Mengniu Dairy

Parmalat

Technological advancements are playing a crucial role in transforming the Dairy Cream Products Market, particularly in processing, packaging, and supply chain optimization. Automated cream separation systems have improved efficiency by up to 35%, enabling consistent product quality and reducing manual intervention. Ultra-high temperature (UHT) processing technology is widely adopted, extending product shelf life by over 40% without compromising nutritional value. Homogenization techniques have also advanced, delivering up to 30% improvement in texture consistency and stability.

Digital transformation is gaining momentum, with approximately 50% of large dairy processors integrating AI and IoT-based monitoring systems to enhance quality control and traceability. Smart sensors are used to monitor temperature and storage conditions, reducing spoilage rates by nearly 25%. Packaging innovations, including aseptic and biodegradable materials, are helping companies meet sustainability targets, with over 45% of manufacturers adopting eco-friendly solutions. Blockchain technology is also being explored to improve supply chain transparency and ensure product authenticity.

Emerging technologies such as enzymatic processing are enabling the development of lactose-free cream products with improved digestibility. Additionally, advancements in cold-chain logistics have enhanced distribution efficiency by 30%, ensuring product freshness across long distances. These technological developments are reshaping the Dairy Cream Products Market, driving efficiency, sustainability, and product innovation.

• In February 2025, Nestlé confirmed a CHF 2.5 billion cost-saving and reinvestment program aimed at strengthening product innovation and expanding dairy portfolios, including cream-based and premium dairy categories. The company also secured over CHF 300 million in savings to support product development and operational efficiency improvements. Source: www.nestle.com

• In August 2025, Fonterra announced the sale of its global consumer dairy business, including cream and related product lines, to Lactalis for approximately USD 2.24 billion. The deal includes well-known dairy brands and strengthens Lactalis’ global dairy product portfolio across Asia-Pacific and other regions.

• In October 2025, Fonterra received approval from over 88% of its farmer shareholders for the divestment of its consumer dairy segment to Lactalis, covering foodservice and ingredient operations. The move enables strategic focus on high-value dairy ingredients and streamlined cream product supply chains.

• In 2024, Arla Foods announced restructuring of its dairy production network, including closure of the Tistrup facility and consolidation of operations into more advanced processing plants to meet evolving safety, quality, and efficiency standards in dairy product manufacturing.

The Dairy Cream Products Market Report provides a comprehensive analysis of the global industry, covering a wide range of segments, applications, and geographic regions. The report includes detailed insights into product types such as heavy cream, whipping cream, lactose-free cream, and specialty variants, highlighting their industrial and retail applications. Application areas analyzed include bakery and confectionery, foodservice, beverages, and packaged foods, reflecting diverse usage patterns across sectors.

Geographically, the report examines key regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering detailed insights into regional consumption patterns, production capacities, and technological adoption levels. The report also evaluates end-user segments such as households, foodservice providers, and industrial processors, providing a holistic view of demand dynamics.

Additionally, the scope includes analysis of technological advancements, including UHT processing, automated separation systems, and sustainable packaging solutions. The report explores regulatory frameworks, environmental considerations, and evolving consumer preferences shaping the market landscape. Emerging segments such as plant-dairy hybrids and functional cream products are also covered, offering forward-looking insights into future growth opportunities. Overall, the report serves as a strategic tool for decision-makers, providing actionable insights into market trends, competitive dynamics, and innovation pathways.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,850.0 Million |

| Market Revenue (2033) | USD 3,275.0 Million |

| CAGR (2026–2033) | 7.4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Nestlé; Danone; Fonterra; Lactalis; Arla Foods; Dean Foods; Saputo Inc.; Dairy Farmers of America; FrieslandCampina; Amul; Britannia Industries; Yili Group; Mengniu Dairy; Parmalat |

| Customization & Pricing | Available on Request (10% Customization Free) |