Reports

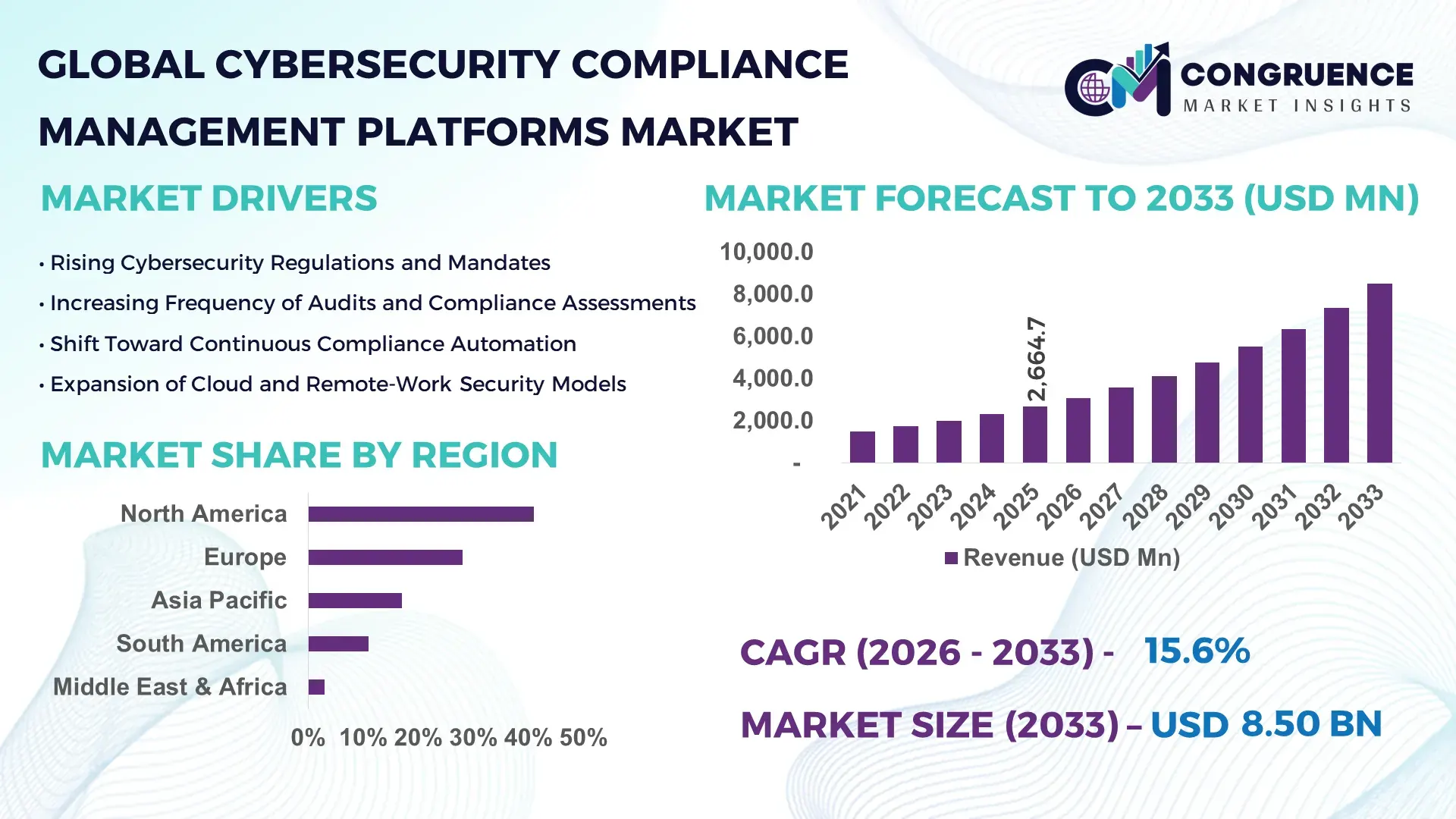

The Global Cybersecurity Compliance Management Platforms Market was valued at USD 2,664.7 Million in 2025 and is anticipated to reach a value of USD 8,497.9 Million by 2033 expanding at a CAGR of 15.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by the rapid expansion of regulatory mandates and enterprise-wide cyber risk governance requirements.

The United States represents the most mature ecosystem for Cybersecurity Compliance Management Platforms deployment. In 2025, over 68% of large U.S. enterprises operated centralized compliance platforms covering frameworks such as SOC 2, ISO 27001, HIPAA, PCI DSS, and FedRAMP. Annual enterprise spending on governance, risk, and compliance software exceeded USD 9.2 billion, with compliance automation platforms supporting sectors including BFSI, healthcare, cloud service providers, and federal contractors. More than 1,300 cybersecurity software vendors in the U.S. offered compliance-aligned modules, while AI-enabled continuous controls monitoring tools were integrated into 47% of Fortune 1000 security operations, reflecting strong technological advancement and platform maturity.

Market Size & Growth: Valued at USD 2,664.7 Million in 2025, projected to reach USD 8,497.9 Million by 2033, expanding at a CAGR of 15.6%, driven by regulatory complexity and audit automation demand.

Top Growth Drivers: Regulatory compliance automation adoption 49%, cloud security governance expansion 36%, third-party risk monitoring 28%.

Short-Term Forecast: By 2028, automated compliance workflows are expected to reduce audit preparation time by 41%.

Emerging Technologies: AI-driven continuous compliance monitoring, policy-as-code engines, automated evidence collection.

Regional Leaders: North America projected at USD 3,620 Million by 2033 with enterprise GRC platforms; Europe USD 2,480 Million driven by data protection mandates; Asia Pacific USD 1,720 Million via cloud compliance adoption.

Consumer/End-User Trends: Large enterprises account for over 52% of platform deployments, followed by regulated SMEs.

Pilot or Case Example: In 2025, a financial services pilot reduced compliance reporting effort by 38% using automated controls mapping.

Competitive Landscape: Market leader with approximately 16% share, followed by ServiceNow, OneTrust, RSA, and LogicGate.

Regulatory & ESG Impact: Expanding data protection laws and ESG disclosure requirements accelerating compliance platform uptake.

Investment & Funding Patterns: Over USD 4.6 billion invested globally since 2022 in compliance automation and cyber GRC platforms.

Innovation & Future Outlook: Growth of real-time compliance dashboards and AI-assisted regulatory interpretation engines.

Cybersecurity Compliance Management Platforms primarily serve BFSI (34%), technology and cloud services (27%), healthcare and life sciences (19%), and government-linked enterprises (20%). Platform innovation focuses on continuous controls monitoring, regulatory mapping automation, and cloud-native integrations. Regional consumption is highest among organizations with multi-jurisdictional operations, while future growth is expected from AI-assisted compliance intelligence and embedded governance within DevSecOps pipelines.

The Cybersecurity Compliance Management Platforms Market is strategically redefining how organizations manage regulatory obligations, cyber risk exposure, and audit readiness in increasingly complex digital environments. These platforms centralize compliance frameworks, automate evidence collection, and provide continuous visibility into control effectiveness across hybrid IT infrastructures. AI-driven continuous compliance monitoring delivers up to 43% improvement compared to manual audit preparation processes, enabling faster response to regulatory changes. North America dominates in deployment volume, while Europe leads in adoption with 55% of large enterprises actively using automated compliance platforms aligned with data protection and operational resilience mandates. By 2028, policy-as-code and automated control validation are expected to reduce compliance remediation cycles by 35%, particularly in cloud-native environments. ESG considerations are also shaping strategy, with firms committing to 30% reduction in compliance documentation redundancy by 2030 through centralized governance platforms. In 2025, a global cloud service provider achieved a 39% reduction in compliance audit costs by deploying AI-enabled evidence mapping across multiple regulatory standards. The market’s forward trajectory positions the Cybersecurity Compliance Management Platforms Market as a foundational pillar for operational resilience, regulatory assurance, and sustainable digital trust.

The Cybersecurity Compliance Management Platforms market dynamics are influenced by rising regulatory scrutiny, expanding cloud adoption, and increasing cyber risk accountability at board levels. Organizations face overlapping compliance requirements across data privacy, financial reporting, and cybersecurity controls, driving demand for centralized compliance orchestration. In 2025, more than 62% of enterprises reported managing five or more regulatory frameworks simultaneously. Cloud migration and remote work models have further expanded the attack surface, requiring continuous compliance validation rather than periodic audits. Technological advances such as AI-based control testing, automated risk scoring, and real-time dashboards are transforming compliance from static reporting to proactive risk management. However, platform integration complexity and skills gaps continue to shape adoption strategies.

Rising regulatory complexity is a primary driver of the Cybersecurity Compliance Management Platforms market. In 2025, enterprises operating across regions managed an average of 7.4 active compliance frameworks, increasing operational burden. Automated compliance platforms streamline control mapping and evidence collection, reducing manual workload by 45%. Financial institutions and healthcare providers increasingly rely on these platforms to maintain continuous compliance and reduce regulatory exposure. Demand is further amplified by regulatory penalties, with organizations prioritizing compliance automation to minimize audit risk and operational disruptions.

Despite strong demand, integration challenges and cybersecurity skill gaps restrain the Cybersecurity Compliance Management Platforms market. In 2025, nearly 33% of organizations cited difficulties integrating compliance platforms with legacy systems and cloud environments. Limited availability of trained compliance engineers and security analysts slows deployment and optimization. Additionally, organizations with fragmented IT architectures face higher implementation complexity, delaying full platform utilization and measurable benefits.

Cloud-native compliance presents significant growth opportunities for the Cybersecurity Compliance Management Platforms market. In 2025, 48% of enterprises adopted cloud-hosted compliance platforms to support scalable operations and remote audits. Native integrations with DevSecOps pipelines enable real-time compliance validation during software development, reducing post-deployment risks. Opportunities are expanding in managed compliance services for SMEs, where outsourced governance platforms lower entry barriers and improve regulatory adherence.

Cost optimization and regulatory interpretation remain key challenges for the Cybersecurity Compliance Management Platforms market. While automation reduces long-term costs, initial platform deployment requires upfront investment and process reengineering. Additionally, translating evolving regulatory language into technical controls demands specialized expertise. In 2025, 29% of enterprises reported delays in compliance updates due to ambiguity in regulatory guidance, impacting timely platform configuration.

Expansion of Continuous Compliance Monitoring: In 2025, over 58% of new deployments featured real-time controls monitoring, reducing audit preparation cycles by 41%.

Integration with DevSecOps Pipelines: Approximately 46% of technology enterprises embedded compliance checks into CI/CD workflows, improving release governance by 33%.

AI-Assisted Regulatory Mapping: AI-based regulation-to-control mapping improved compliance accuracy by 29% compared to manual methods.

Growth of Third-Party Risk Compliance Modules: Third-party compliance tracking adoption increased by 37%, driven by supply chain cyber risk exposure.

The Cybersecurity Compliance Management Platforms market is segmented by type, application, and end-user, reflecting diverse organizational needs. By type, platforms range from standalone compliance tools to integrated governance, risk, and compliance suites. Application segmentation highlights strong demand for audit management, risk assessment, and regulatory reporting. End-user insights reveal adoption differences between large enterprises, regulated SMEs, and public sector organizations. Across all segments, scalability, regulatory coverage, and automation depth influence purchasing decisions.

Integrated GRC platforms lead with 44% adoption, offering unified risk, compliance, and audit management. Standalone compliance automation tools account for 26%, preferred by SMEs seeking focused functionality. Cloud-native compliance platforms represent the fastest-growing type, expanding at a 17.9% CAGR, driven by scalability and remote audit support. Other niche solutions, including industry-specific compliance modules, contribute a combined 30% share.

In 2025, a national infrastructure provider deployed a cloud-native compliance platform to automate over 120 regulatory controls across distributed environments.

Audit management and reporting applications dominate with 39% share, supported by demand for continuous evidence collection. Risk assessment applications account for 28%, while regulatory intelligence and policy management contribute 33% combined share. Regulatory intelligence applications are the fastest-growing, expanding at a 16.8% CAGR, driven by frequent regulatory updates. In 2025, more than 38% of enterprises piloted automated compliance reporting platforms, improving audit readiness across multi-cloud environments.

In 2025, a global public sector initiative deployed automated compliance tools across 150 agencies, improving audit efficiency for over 2 million digital assets.

Large enterprises represent the leading end-user segment with 52% adoption, driven by complex regulatory exposure. Regulated SMEs account for 31%, while government and public sector entities contribute 17%. SMEs are the fastest-growing end-user group, expanding at a 18.4% CAGR, supported by managed compliance services. In 2025, 38% of enterprises piloted centralized compliance platforms, and 42% of regulated organizations integrated compliance monitoring into cloud security operations.

In 2025, adoption of automated compliance tools among mid-sized enterprises increased by 22%, enabling over 500 organizations to streamline audit and reporting processes.

North America accounted for the largest market share at 41% in 2025 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 14% between 2026 and 2033.

In 2025, North America recorded more than USD 1,095 Million in annual procurement of cybersecurity compliance management platforms, with over 78% of Fortune 500 companies deploying centralized compliance orchestration tools across multi-cloud environments. Europe followed with approximately USD 712 Million in compliance spending, while Asia Pacific exceeded USD 654 Million in enterprise licensing and SaaS adoption. Regional segmentation indicates that over 62% of North American financial services, 54% of healthcare networks, and 47% of federal contractors integrated advanced audit automation and controls mapping into enterprise risk programs in 2025. Adoption of automated evidence collection and continuous monitoring dashboards increased by 39% year-on-year across regulated industries, and the number of enterprises implementing third-party risk compliance modules expanded by 33% in 2025. Digital transformation initiatives in North America also resulted in 52% higher deployment rates of integrated platform suites versus standalone point solutions. In addition, enterprise security teams in North America reported a 42% improvement in remediation turnaround times using compliance platforms that integrate policy-as-code engines and AI-assisted controls.

North America’s cybersecurity compliance management platforms market holds a dominant 41% share, driven by demand from heavily regulated industries such as financial services, healthcare, and federal contracting. Key industries driving demand include banking, insurance, and cloud service providers, where compliance with PCI DSS, HIPAA, and FedRAMP is mandated. Regulatory changes such as expanded data privacy laws and enhanced federal cybersecurity requirements have prompted increased enterprise investment in automated compliance solutions. Technological advancements in this region include integrated AI engines for continuous controls monitoring and automated evidence collection workflows, improving audit readiness and reducing manual effort by over 40% in 2025. Local players and major systems integrators are expanding platform interoperability with identity management and SIEM systems to provide a unified compliance and risk management ecosystem. Regional consumer behavior variations show higher enterprise adoption in healthcare and finance sectors where regulatory penalties and reputation risk drive broader platform rollout, while mid-size enterprises are increasingly adopting SaaS compliance tools to manage external audit requirements efficiently.

Europe’s cybersecurity compliance management platforms market represents approximately 28% of total enterprise deployments, led by key markets including Germany, the UK, and France where strong data protection frameworks require demonstrable audit trails and explainable controls. EU GDPR enforcement and national security mandates have driven growth in automated compliance reporting and documentation tracking. Adoption of emerging technologies like real-time continuous monitoring, regulatory change intelligence feeds, and automated policy mapping are increasing across European enterprises. Local players in this region have developed multilingual compliance orchestration modules and region-specific control libraries to support pan-EU regulatory alignment. European regulatory bodies also encourage sustainability reporting and cyber governance transparency, which influences platform configurations to include extended documentation and audit logging functionalities. Consumer behavior variations highlight that regulatory pressure leads to demand for explainable cybersecurity compliance management platforms with integrated risk assessment matrices and traceable audit artifacts, particularly in sectors such as manufacturing, automotive, and energy.

The Asia-Pacific cybersecurity compliance management platforms market ranks strongly in volume with enterprise licensing and SaaS uptake exceeding USD 654 Million in 2025, supported by robust growth in China, India, and Japan. Infrastructure and digital transformation trends in this region emphasize rapid cloud adoption across financial services, telecommunications, and retail sectors, driving demand for compliance platforms that integrate cloud security posture management and regulatory reporting. Regional tech innovation hubs in Bengaluru, Shanghai, and Tokyo are advancing AI-enabled compliance analytics and automated policy enforcement capabilities. Local players and regional integrators are tailoring solutions to support diverse regulatory environments and multi-jurisdictional compliance requirements, with 48% of enterprises in Asia Pacific deploying automated evidence collection and controls dashboards. Consumer behavior variations indicate growth driven by e-commerce and mobile AI apps, where organizations emphasize real-time compliance visibility and integration with DevSecOps pipelines to support continuous delivery and audit readiness.

In South America, the cybersecurity compliance management platforms market is supported by key countries like Brazil and Argentina, where enterprises face evolving regulatory expectations and data protection mandates. The regional market share is estimated at 11% of total global deployments, with infrastructure trends showing increased investment in compliance workflows and automated audit reporting frameworks. Government incentives aimed at strengthening national cybersecurity postures and trade policies encouraging technology import facilitation have helped expand local distribution of compliance platforms. Local system integrators are developing localized compliance content libraries to support Spanish and Portuguese requirements, increasing enterprise confidence in platform applicability. Consumer behavior variations show demand tied to media and language localization, with 42% of South American enterprises prioritizing compliance platforms that incorporate region-specific regulatory mappings and bilingual interfaces.

The Middle East & Africa cybersecurity compliance management platforms market reflects growing enterprise prioritization of digital governance, particularly in major growth countries such as the UAE and South Africa. Regional demand trends include alignment with national cybersecurity strategies and smart government initiatives, driving platform deployment across banking, oil & gas, and large infrastructure sectors. Technological modernization includes cloud-based compliance automation and integration with advanced threat intelligence feeds for real-time risk assessment. Local regulations and trade partnerships have facilitated platform procurement and localized implementation support. Regional players are enhancing compliance modules to support multi-sector frameworks and cross-border audit artifacts. Consumer behavior variations indicate an increased focus on premium compliance platforms with strong reporting and traceability features, reflecting enterprise emphasis on regulatory adherence and cyber resilience.

United States – 36% Market Share: The United States leads the cybersecurity compliance management platforms market with extensive enterprise adoption and advanced regulatory frameworks.

China – 18% Market Share: China’s prominence is supported by rapid digital transformation, large technology enterprise presence, and broad compliance system deployment across public and private sectors.

The Cybersecurity Compliance Management Platforms market is characterized by a mix of large established technology vendors, specialized governance risk and compliance (GRC) platform providers, and emerging SaaS innovators that deliver automated compliance orchestration across industries. As of 2025, more than 85 active competitors operate globally, offering solutions ranging from standalone compliance automation tools to integrated risk and audit management suites. The top five companies collectively command approximately 41% of platform deployments, reflecting a moderately fragmented competitive environment with opportunities for niche specialists. Market leaders emphasize strategic initiatives such as partnerships with cloud service providers, integration with SIEM and identity governance systems, and the introduction of AI-assisted regulatory mapping engines. Recent product launches focus on enhancing continuous compliance dashboards, real-time controls scanning, and automated evidence gathering to support complex regulatory landscapes. Mergers and acquisitions have played a significant role in expanding platform capabilities, with larger vendors acquiring analytics and risk orchestration startups to bolster their compliance automation portfolios. Innovation trends influencing competition include the adoption of policy-as-code engines, automated third-party compliance modules, and machine learning models that predict regulatory change impacts. Demand for cross-framework compliance support, such as simultaneous coverage of ISO, SOC, PCI, and data privacy mandates, has intensified platform feature competition. Additionally, regional players in Asia Pacific and Europe are customizing offerings to meet localized regulatory requirements and multilingual enterprise environments. As organizations prioritize cyber risk governance and audit readiness, competitive positioning increasingly hinges on comprehensive controls coverage, ease of integration, and measurable reductions in audit cycle times.

LogicGate

MetricStream

IBM Security

SAP GRC

Microsoft Compliance Manager

Archer by RSA

NAVEX Global

SAI Global

RiskVision

Galvanize (Diligent GRC)

Secureframe

Technology advancements in the Cybersecurity Compliance Management Platforms market are accelerating the transition from manual compliance workflows to automated, intelligent governance models. Key technological innovations include AI-driven continuous compliance monitoring, which scans control environments in real time and alerts security and compliance teams to deviations, significantly reducing manual audit preparation efforts. Automated evidence collection engines integrate with enterprise systems — including cloud infrastructure, identity management, and endpoint security — to gather artifacts necessary for multi-framework reporting, responding to the complexity of concurrent compliance requirements such as ISO 27001, SOC 2, HIPAA, and GDPR. Policy-as-code frameworks allow compliance policies to be embedded directly into software development lifecycles, enabling DevSecOps teams to validate regulatory adherence early in the development process, bridging traditional gaps between security and development functions. Machine learning and natural language processing (NLP) models are increasingly used to map evolving regulatory text to corresponding technical controls, enhancing regulatory change management and reducing interpretation overhead for compliance teams. Cloud-native platform architectures support scalable deployments, with containerized compliance functions that can be distributed across multi-cloud environments. Real-time dashboards and analytics provide decision makers with consolidated views of control effectiveness, audit readiness, and risk exposure, supporting faster remediation prioritization. Integration with orchestration tools enables automated workflow generation for compliance tasks, reducing cycle times from weeks to days. Advanced threat intelligence integrations inform compliance risk scoring, correlating external threat vectors with internal control status to guide risk-based decision making. Enhanced API connectivity with SIEM, SOAR, IAM, and vulnerability management platforms ensures that compliance data is synchronized across the security operations ecosystem, improving contextual visibility and operational alignment. Emerging technologies such as blockchain-enhanced audit trails and secure multiparty computation are being explored to strengthen tamper-proof evidence and cross-organization compliance reporting. These technological developments empower enterprises to manage complex regulatory landscapes more effectively and provide measurable improvements in audit efficiency, control transparency, and overall cyber governance effectiveness.

• In March 2025, OneTrust expanded its compliance automation suite with integrated third-party risk assessment tools that streamline vendor compliance evaluations across multiple frameworks, enhancing enterprise risk visibility. Source:www.onetrust.com

• In July 2025, ServiceNow launched an AI-enhanced continuous compliance monitoring module that improves automated control validation and reporting workflows for large regulated enterprises. Source:www.servicenow.com

• In September 2024, RSA Security introduced a specialized compliance engine tailored to financial services standards, enabling real-time audit evidence collection and automated documentation workflows. Source:www.rsa.com

• In November 2025, MetricStream unveiled extended policy-as-code capabilities within its governance platform, allowing automated integration of regulatory changes into operational controls for cloud and hybrid environments. Source:www.metricstream.com

The Cybersecurity Compliance Management Platforms Market Report provides a detailed evaluation of global trends, platform types, application domains, and end-user segments critical to enterprise risk governance and regulatory adherence planning. It examines compliance solutions ranging from standalone audit automation and evidence collection modules to fully integrated governance, risk, and compliance (GRC) suites that incorporate continuous monitoring, policy mapping, and risk assessment engines. The report covers how platforms address diverse compliance regimes including SOC, ISO, HIPAA, PCI, and data privacy mandates across geographies, reflecting regional regulatory nuances and enterprise maturity levels. Technology analysis focuses on AI and machine learning applications for regulatory intelligence, real-time control validation, API-driven integrations with security operations tools, policy-as-code frameworks, and cloud-native delivery models that support scalable enterprise deployments. End-user insights explore adoption dynamics among large enterprises, regulated SMEs, and public sector organizations, profiling industry-specific use cases such as financial services compliance orchestration, healthcare data protection workflows, and energy sector audit readiness. Geographic segmentation provides insights into market growth patterns, regulatory pressures, and digital transformation priorities across North America, Europe, Asia Pacific, South America, and Middle East & Africa. The report also identifies emerging niche opportunities in managed compliance services, third-party risk compliance modules, and compliance support for hybrid and multi-cloud environments. Strategic themes include competitive positioning of major vendors, partnership ecosystems with cloud service providers and security solution integrators, and innovations influencing platform differentiation. Quantitative analysis spans deployment volumes, technology adoption rates, and feature utilization patterns that inform decision makers on investment priorities and technology roadmaps. The scope further encompasses future outlooks for compliance automation, integration with DevSecOps practices, and the role of continuous monitoring in enhancing organizational resilience and audit efficiency.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2,664.7 Million |

|

Market Revenue in 2033 |

USD 8,497.9 Million |

|

CAGR (2026 - 2033) |

15.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ServiceNow, OneTrust, RSA Security, LogicGate, MetricStream, IBM Security, SAP GRC, Microsoft Compliance Manager, Archer by RSA, NAVEX Global, SAI Global, RiskVision, Galvanize (Diligent GRC), Secureframe |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |