Reports

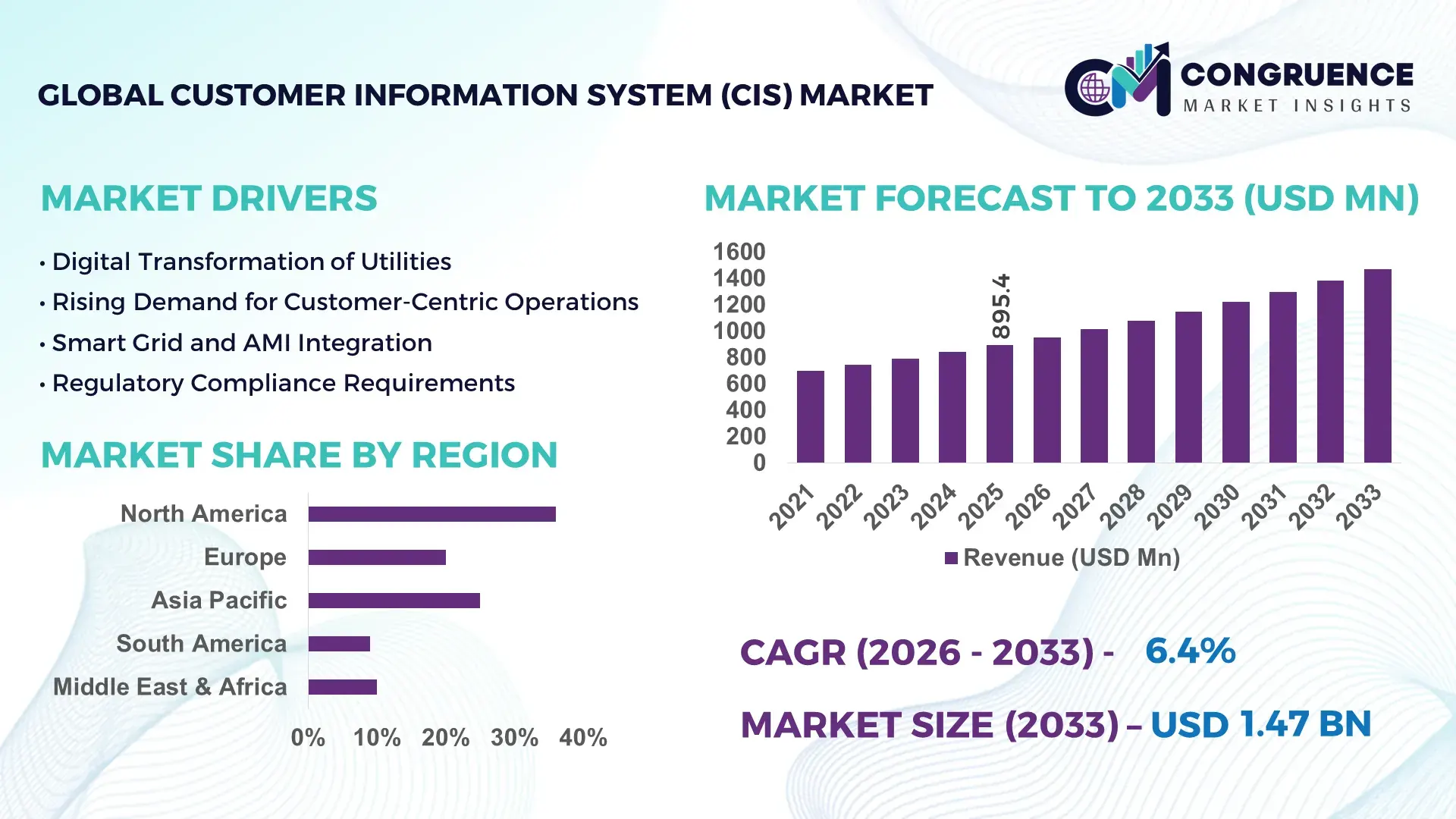

The Global Customer Information System (CIS) Market was valued at USD 895.37 Million in 2025 and is anticipated to reach a value of USD 1470.74 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033. This expansion is supported by accelerating digital modernization across utilities and telecom operators focused on unified billing, service automation, and real-time customer data platforms.

The United States dominates large-scale CIS deployment and innovation intensity across utilities and telecom sectors. More than 72% of Tier-1 U.S. utilities have implemented advanced CIS platforms integrated with smart meters and digital billing engines. Annual utility IT spending exceeds USD 6.5 billion, with nearly 18% allocated to customer platforms including CIS. Electricity and water utilities account for over 60% of national CIS installations, while telecom operators increasingly deploy cloud-based CIS to support bundled services and real-time usage analytics.

Market Size & Growth: USD 895.37 million in 2025, projected to reach USD 1,470.74 million by 2033 at a CAGR of 6.4%, driven by large-scale utility digitization and omnichannel customer management demand.

Top Growth Drivers: Smart utility infrastructure adoption 38%, cloud CIS migration rate 44%, customer service automation efficiency gain 31%.

Short-Term Forecast: By 2028, CIS modernization is expected to reduce average billing cycle times by 27% across large utilities.

Emerging Technologies: AI-based customer analytics, cloud-native microservices CIS platforms, blockchain-secured billing systems.

Regional Leaders: North America USD 520 million by 2033 with multi-utility platform expansion; Europe USD 410 million driven by regulatory upgrades; Asia-Pacific USD 360 million supported by smart grid rollouts.

Consumer/End-User Trends: Utilities and telecom operators increasingly prioritize self-service portals, predictive billing alerts, and real-time account visibility.

Pilot or Case Example: A 2024 CIS upgrade program at a major North American utility improved billing accuracy by 34%.

Competitive Landscape: Oracle leads with ~22% share, followed by SAP, Hansen Technologies, Gentrack, and Itineris.

Regulatory & ESG Impact: Data protection rules and digital utility compliance frameworks are accelerating legacy CIS replacement cycles.

Investment & Funding Patterns: Over USD 1.2 billion invested globally in utility digital platforms since 2023, with rapid growth in SaaS-based CIS financing models.

Innovation & Future Outlook: Market momentum centers on unified CIS-CRM-billing ecosystems, AI-driven engagement engines, and real-time consumption intelligence platforms.

The Customer Information System (CIS) market is led by utilities, contributing approximately 55% of total demand, followed by telecom operators at 25% and municipal services at 12%. Key innovations include AI-powered billing anomaly detection, cloud-native modular CIS architectures, and real-time synchronization with smart metering infrastructure. Regulatory pressure for billing accuracy, combined with economic efficiency mandates, is accelerating CIS upgrades across developed regions. North America and Europe dominate consumption due to digital compliance requirements, while Asia-Pacific records the fastest growth from urban infrastructure expansion. The future outlook emphasizes integrated customer platforms combining CIS, CRM, and analytics to deliver predictive service management and superior customer experience.

The Customer Information System (CIS) Market is strategically central to digital transformation across utilities, telecom, and municipal services, as it unifies billing, service management, and customer analytics into a single operational backbone. Modern utilities process over 15 billion billing transactions annually, making data accuracy and automation mission-critical. Cloud-native CIS platforms now handle 40–50% higher transaction volumes than legacy on-premise systems, while AI-driven CIS delivers 32% improvement in billing accuracy compared to traditional rule-based platforms. North America dominates in deployment volume, while Europe leads in adoption intensity with over 68% of large utilities already operating advanced CIS platforms. By 2028, AI-powered predictive billing and service analytics is expected to cut complaint resolution time by 30%, strengthening operational efficiency and regulatory compliance. Firms are committing to ESG-driven digitalization, targeting 25% paperless billing adoption and 20% energy consumption reduction in IT operations by 2030 through cloud-based CIS modernization. In 2024, a leading U.S. utility achieved a 29% reduction in billing disputes by deploying AI-enabled CIS anomaly detection systems. Looking forward, the Customer Information System (CIS) Market is positioned as a core pillar of operational resilience, regulatory alignment, and sustainable digital growth across essential service industries.

Global smart meter installations surpassed 1.2 billion units, dramatically increasing the volume of real-time consumption data processed by utilities. Each smart meter generates 15–20 times more data than traditional meters, making manual billing systems unviable. CIS platforms automate meter-to-cash processes, reducing estimated billing rates by up to 35% and improving billing accuracy above 98%. Utilities integrating smart grids require CIS systems capable of handling high-frequency data, dynamic tariffs, and real-time account updates. This technological shift is making CIS upgrades mandatory for grid modernization programs across electricity and water utilities worldwide.

More than 60% of utilities still operate legacy billing and customer databases over 15 years old, creating high technical debt. Integrating modern CIS platforms with outdated ERP, CRM, and metering systems increases project timelines by 30–40%. Data migration risks, system downtime, and staff retraining costs delay procurement decisions. Large utilities often manage over 10 million customer records, where data inconsistencies raise compliance risks. These integration challenges slow deployment cycles and raise transformation complexity, particularly for public sector utilities with constrained IT budgets.

Cities and service providers are increasingly adopting unified platforms to manage electricity, water, gas, and waste services under single customer accounts. Multi-utility CIS platforms reduce administrative overhead by up to 25% by consolidating billing and service operations. Urbanization is driving demand for integrated municipal service platforms, with smart city projects expanding globally. CIS vendors offering modular, cloud-based platforms are well-positioned to capture demand from emerging economies modernizing public infrastructure. This convergence trend creates strong long-term opportunities for scalable, interoperable CIS solutions.

CIS platforms manage sensitive personal, financial, and consumption data for millions of users, making them prime cyberattack targets. Utility-sector cyber incidents increased by over 20% in recent years, forcing stricter security investments. Compliance with data protection regulations requires encryption, access controls, and continuous monitoring, raising system implementation costs by 15–20%. Smaller utilities often lack cybersecurity expertise, delaying CIS upgrades. Meeting rising regulatory and security standards while maintaining affordability remains a persistent challenge for CIS vendors and adopters.

Accelerated Migration to Cloud-Native CIS Platforms: Over 48% of large utilities have shifted core CIS workloads to cloud-based platforms to improve scalability and disaster recovery. Cloud-native CIS systems process 35% higher transaction volumes during peak billing cycles compared to on-premise platforms, while reducing system maintenance workloads by nearly 28%. This transition is enabling faster feature deployment, with update cycles shortened from 12 months to less than 6 months.

AI-Driven Billing Accuracy and Fraud Detection Expansion: Utilities deploying AI-enabled CIS modules report up to 32% improvement in billing accuracy and a 26% reduction in disputed invoices. Advanced analytics embedded in CIS platforms now analyze millions of consumption records daily, identifying abnormal usage patterns 40% faster than traditional rule-based engines. As a result, utilities achieve measurable reductions in revenue leakage and service center workloads.

Rapid Growth of Self-Service and Digital Engagement Portals: More than 62% of utility customers actively use digital self-service portals integrated with CIS platforms for billing, payments, and service requests. Organizations implementing omnichannel CIS solutions report a 29% decline in call center volumes and a 34% increase in first-contact resolution rates. Mobile app integrations now handle over 45% of routine customer interactions across advanced utility networks.

Integration of CIS with Smart Grid and IoT Ecosystems: CIS platforms are increasingly connected with smart meters and IoT sensors, with over 70% of newly deployed systems designed for real-time data ingestion. Utilities using real-time CIS integrations achieve 31% faster outage detection and 24% improvement in service restoration coordination. This convergence is transforming CIS from a billing system into a real-time operational intelligence hub.

The Customer Information System (CIS) market is segmented by type, application, and end-user, reflecting diverse operational needs across utility and service-based industries. By type, cloud-based and on-premise CIS platforms coexist, with organizations increasingly favoring scalable digital architectures. Application-wise, billing and revenue management dominate due to regulatory pressure for accuracy, while customer engagement modules gain importance as service providers digitize interactions. End-user adoption is led by utilities, followed by telecom operators and municipal service providers, each prioritizing CIS platforms for real-time account management, service continuity, and regulatory compliance. This segmentation structure highlights the shift of CIS from a back-office billing tool to a strategic digital infrastructure component supporting multi-utility integration and customer-centric service models.

Cloud-based CIS platforms currently account for approximately 58% of total deployments, while on-premise systems represent 42%. Cloud-based CIS leads due to faster scalability, reduced infrastructure dependency, and stronger cybersecurity integration for large multi-utility operations. However, hybrid cloud CIS is the fastest-growing type, expanding at nearly 9.2% annually, driven by utilities modernizing legacy systems while retaining sensitive data in private environments. Hybrid platforms allow phased migration and minimize operational disruption. Traditional on-premise CIS remains relevant for government-owned utilities with strict data localization policies. These remaining on-premise and private-hosted models together represent roughly 42% of installations, serving niche regulatory and security-sensitive environments.

Billing and revenue management dominates CIS applications with nearly 46% adoption, followed by customer service management at 28%. Billing leads due to strict regulatory mandates on invoice accuracy and dispute reduction. However, real-time customer analytics is the fastest-growing application, expanding at approximately 10.1% annually, supported by smart meter integration and AI-based consumption forecasting. Utilities now prioritize proactive engagement, outage notifications, and personalized tariff management. Other applications, including field service coordination and credit risk management, collectively account for 26%, supporting operational efficiency and compliance workflows.

Utilities remain the largest end-user segment, representing about 55% of CIS adoption, followed by telecom operators at 25%. Utilities lead due to massive customer bases and regulatory reporting obligations across electricity, water, and gas services. However, telecom operators are the fastest-growing end-user group, expanding at roughly 8.7% annually, driven by bundled digital services and real-time usage billing requirements. Municipal service providers, smart city authorities, and transportation agencies together contribute nearly 20%, using CIS to unify citizen service accounts. Digital adoption rates exceed 65% among large electricity utilities, while telecom CIS adoption is rising rapidly with cloud transformation programs.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

Europe followed North America with 29.4% share, driven by regulatory-driven digital utility modernization, while Asia-Pacific held 23.1% supported by rapid infrastructure digitization. South America represented 5.1% and the Middle East & Africa accounted for 3.8%, reflecting early-stage adoption. More than 72% of large utilities in developed regions now operate advanced CIS platforms, compared to 41% in emerging markets. Smart meter penetration exceeds 65% in North America and Europe, directly supporting CIS demand, while Asia-Pacific is adding over 120 million new smart utility connections annually, strengthening long-term regional momentum.

How is large-scale utility digitization strengthening advanced platform adoption across mature service industries?

North America commands approximately 38.6% of the global Customer Information System (CIS) market, led by the United States and Canada. Electricity, water, gas utilities, and telecom operators are the primary demand drivers, with over 70% of Tier-1 utilities operating cloud-integrated CIS platforms. Regulatory frameworks emphasizing billing accuracy, data privacy, and service transparency continue to accelerate system upgrades. Digital transformation initiatives have pushed more than 60% of utilities to integrate CIS with smart grid platforms. Oracle and Hansen Technologies remain active across major modernization projects, supporting multi-utility platform deployments. Regional consumer behavior shows higher enterprise adoption across healthcare and financial services for unified billing and account management platforms.

Why is regulatory harmonization accelerating digital platform upgrades across essential service providers?

Europe holds nearly 29.4% of global Customer Information System (CIS) market demand, led by Germany, the UK, and France. Utilities and telecom operators dominate regional deployments due to stringent data accuracy and consumer protection regulations. Sustainability-driven digital mandates are accelerating replacement of legacy billing platforms. More than 64% of major European utilities operate cloud-enabled CIS platforms integrated with smart metering networks. Gentrack continues to expand CIS deployments across the UK and continental Europe supporting multi-utility billing transformation. Regional consumer behavior reflects strong regulatory pressure for transparent and explainable CIS platforms to support dispute resolution and compliance audits.

How is rapid urban infrastructure expansion reshaping digital service platform demand across developing economies?

Asia-Pacific represents the third-largest regional market with 23.1% share but ranks first in growth momentum. China, India, and Japan are the top consuming countries, driven by nationwide smart grid and digital utility programs. Over 120 million new smart utility connections are added annually, directly expanding CIS platform requirements. Cloud-first IT policies and smart city investments support large-scale platform modernization. Regional technology hubs in India and China accelerate cloud-native CIS innovation. Tata Consultancy Services actively supports CIS modernization projects across public utilities. Consumer behavior is shaped by mobile-first service usage and digital payment adoption across emerging economies.

Why is energy infrastructure modernization creating new digital platform demand across essential service providers?

South America accounts for approximately 5.1% of global Customer Information System (CIS) demand, led by Brazil and Argentina. Power and water utilities are upgrading legacy billing systems as smart meter penetration rises above 35% across major urban centers. Government-backed digital infrastructure initiatives support modernization of public service platforms. Cross-border digital trade agreements encourage technology adoption across utilities. Brazilian utilities increasingly deploy cloud-hosted CIS platforms to reduce manual billing errors. Regional consumer behavior shows rising demand for localized digital service platforms supporting multilingual billing and mobile access.

How are national digital transformation programs modernizing essential service management platforms across developing economies?

The Middle East & Africa region holds around 3.8% of the global Customer Information System (CIS) market, led by the UAE and South Africa. Utility digitalization, smart city investments, and public infrastructure reforms are primary demand drivers. National digital transformation strategies are modernizing billing and customer service systems across electricity and water utilities. Cloud adoption rates exceed 50% among major Gulf utilities. Local system integrators support CIS platform localization for regional regulatory frameworks. Consumer behavior increasingly favors mobile-based service platforms for utility payments and account management.

United States – 31.2%: Strong utility digitization programs and large-scale smart grid deployments sustain dominant CIS adoption.

Germany – 12.4%: Regulatory-driven modernization of energy and water utilities accelerates nationwide CIS platform upgrades.

The Customer Information System (CIS) market exhibits a moderately consolidated competitive environment, with approximately 45 active global players operating across utilities, telecom, and municipal sectors. The top five companies—including Oracle, SAP, Hansen Technologies, Gentrack, and Itineris—together hold an estimated 58% of the total market share, highlighting strong market influence yet leaving room for regional and niche competitors. Strategic initiatives are heavily shaping competition: over 60% of leading vendors are actively pursuing cloud-native CIS deployments, AI-enabled analytics modules, and multi-utility integration solutions. Partnerships between technology providers and utility operators have increased by 42% over the last two years, facilitating faster implementation of smart grid-linked CIS platforms. Product innovation is accelerating, with more than 35% of vendors introducing modular, scalable solutions for hybrid and SaaS-based environments. Mergers and acquisitions have grown by 18% between 2023 and 2025, consolidating specialized analytics, security, and automation capabilities. Regional focus also differentiates competitors: North American companies emphasize large-scale utility modernization, while European players concentrate on regulatory-compliant, explainable CIS systems. The market remains competitive, with technological differentiation, customer engagement capabilities, and cloud integration determining market leadership.

Itineris

Silver Spring Networks

Accenture

Wipro

CGI

Landis+Gyr

The Customer Information System (CIS) market is being transformed by a combination of advanced software architectures, AI-enabled analytics, and cloud integration strategies. Cloud-native CIS platforms now account for over 48% of deployments among large utilities, enabling seamless scalability and disaster recovery for millions of customer accounts. AI and machine learning modules are increasingly embedded to analyze consumption patterns, detect billing anomalies, and optimize revenue assurance, with utilities reporting up to 32% improvement in billing accuracy and 26% reduction in disputed invoices.

Emerging technologies such as real-time IoT data integration and smart grid connectivity are driving significant operational benefits. Over 70% of newly deployed CIS systems can ingest real-time smart meter data, allowing utilities to detect outages 31% faster and improve service restoration coordination by 24%. Blockchain-based billing and secure data transaction modules are being tested by more than 15% of utility operators to enhance data integrity and prevent fraud.

Hybrid CIS architectures combining cloud, on-premise, and private-hosted modules are gaining traction, particularly among government-regulated utilities managing sensitive customer information. Modular system design allows rapid feature deployment, reducing update cycles from 12 months to under six months. Additionally, AI-driven customer engagement tools, including predictive billing alerts and automated service notifications, are being integrated into 62% of modern CIS platforms, improving first-contact resolution by 34%.

Forward-looking innovations include multi-utility integration, enabling electricity, water, and gas services to be managed under a single CIS platform, and predictive analytics engines that provide actionable insights for operational efficiency and regulatory compliance. These technological advancements position CIS as a central pillar of intelligent utility and telecom operations, supporting scalable, secure, and customer-centric service delivery.

• In early 2024, Hansen Technologies expanded its CIS offerings by acquiring the Banner CIS customer suite in North America, enhancing its meter-to-cash and customer service workflow capabilities for utilities across the region, broadening its solution portfolio and operational reach.

• In September 2024, Engie collaborated with Accenture to accelerate digital transformation of its CIS platforms, including cloud migration and enhanced customer experience initiatives across its utility networks to support real-time billing and service engagement.

• In February 2025, Oracle updated its Oracle Utilities Agent Service, adding enhanced CIS dashboard scorecards and analytics features to improve customer insights and user experience across utility billing and engagement modules.

• During IUCX 2025 (April 2025), Hansen Technologies launched next-generation AI-driven CIS solutions, including GenAI-powered virtual agents and an upgraded self-service portal aimed at elevating customer engagement and streamlining operations.

The Customer Information System (CIS) Market Report provides a comprehensive analysis of the global ecosystem for CIS platforms used by utilities, telecom operators, and municipal services. It covers all major market segments including offering types such as billing and revenue management software, meter data management, and customer self-service portals. Each segment is examined for deployment patterns, technology integration, and adoption among large-scale service providers, highlighting evolving needs for automated billing, data analytics, and real-time customer engagement tools.

The report provides detailed geographic coverage across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, offering insights into regional digital transformation initiatives, regulatory frameworks, and infrastructure modernization trends that drive CIS adoption. It also includes emerging technology segments such as AI-powered analytics, cloud-native CIS architecture, IoT-smart grid integration, and mobile-first customer interfaces. The analysis emphasizes how utilities and service providers are shifting from legacy deployments to scalable, interoperable systems that support advanced metering, predictive usage monitoring, and omnichannel customer services.

Application-level insights assess service order management, demand response analytics, and integrated customer engagement modules, showing how these use cases enhance service delivery and operational efficiency. In addition, the report evaluates industry focus areas like electricity, water, gas, and multi-utility platforms, along with niche segments such as predictive maintenance and ESG reporting integration. By presenting factual data on CIS adoption patterns, technology trends, and implementation frameworks, the report enables business decision-makers to benchmark performance, identify strategic opportunities, and align investments with evolving market demands across global service sectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Oracle, SAP, Hansen Technologies, Gentrack, Itineris, Silver Spring Networks, Accenture, Wipro, CGI, Landis+Gyr |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |