Reports

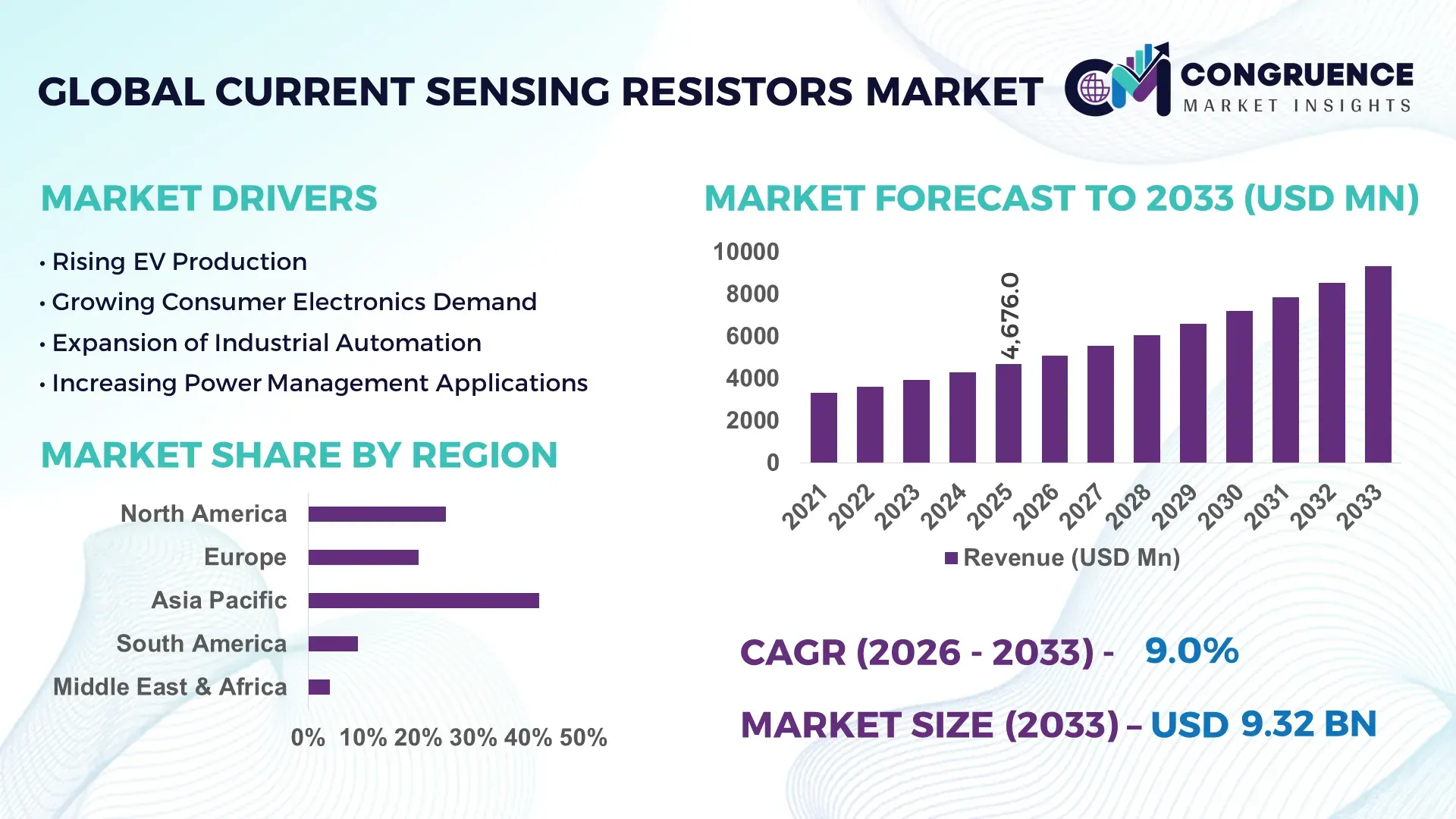

The Global Current Sensing Resistors Market was valued at USD 4676 Million in 2025 and is anticipated to reach a value of USD 9317.22 Million by 2033 expanding at a CAGR of 9% between 2026 and 2033. Electrification across automotive, industrial automation, and renewable power systems is accelerating demand for precision current sensing components, with low-resistance metal strip technologies improving thermal stability by over 28% compared to conventional thick-film designs in high-load applications.

China remains the dominant production and consumption hub, accounting for nearly 38% of global current sensing resistor output in 2026, supported by aggressive EV battery investments, industrial robotics expansion, and large-scale power electronics manufacturing. Japan and South Korea collectively contribute over 24% of advanced precision resistor capacity, driven by high-reliability automotive electronics and AI server infrastructure. Compared with standard shunt resistors, next-generation alloy-based sensing resistors deliver nearly 22% lower power loss in EV inverter systems, strengthening adoption across fast-charging and smart-grid deployments. Rising investments in silicon carbide power modules are also increasing integration rates of compact high-accuracy sensing resistors by over 31% across premium electric vehicle platforms.

Manufacturers focusing on high-efficiency designs, localized supply resilience, and automotive-grade reliability standards are securing stronger long-term positioning in the high-growth global current sensing resistors market.

Market Size & Growth: USD 4676 million in 2025 rising toward USD 9317.22 million by 2033, driven by EV power electronics and advanced battery management integration at 9% CAGR.

Top Growth Drivers: EV electronics adoption up 34%, industrial automation deployment up 27%, and renewable energy inverter demand rising 29%.

Short-Term Forecast: By 2028, advanced low-ohmic resistor designs reduce thermal loss by 21% and improve sensing accuracy by 18% in high-load systems.

Emerging Technologies: AI-enabled power monitoring, metal alloy shunt resistors, and ultra-compact SMD architectures are accelerating high-efficiency system optimization.

Regional Leaders: Asia-Pacific exceeds USD 4.1 billion with EV dominance, Europe surpasses USD 1.9 billion through energy regulations, while North America crosses USD 1.6 billion via AI data-center expansion.

Consumer/End-User Trends: Over 46% of automotive OEMs increased adoption of precision current sensing components in next-generation battery platforms during 2025–2026.

Pilot/Case Example: In 2025, a smart-grid modernization project improved power conversion efficiency by 17% using high-precision current sensing resistor modules.

Competitive Landscape: Top manufacturers control nearly 41% market share, with automotive-grade specialization strengthening competitive differentiation among global suppliers.

Regulatory & ESG Impact: Energy-efficiency mandates reduced system power waste by nearly 14%, accelerating deployment of low-resistance sensing technologies.

Investment & Funding: More than USD 1.8 billion flowed into power electronics expansion, localized manufacturing, and resistor material innovation initiatives since 2024.

Innovation & Future Outlook: Thin-film precision architectures and silicon carbide-compatible sensing systems are transforming high-density EV and industrial power management strategies.

Automotive electronics contribute nearly 42% of total demand, followed by industrial automation at 26% and renewable energy systems at 18%, reflecting strong integration across high-efficiency power applications. Precision alloy resistor adoption increased by 31% in EV inverter platforms due to improved thermal endurance and lower energy dissipation. Asia-Pacific maintains over 48% consumption share as regional manufacturing expansion and localized semiconductor sourcing continue accelerating. Simultaneously, tighter energy-efficiency standards across Europe are pushing adoption of ultra-low resistance sensing technologies in smart-grid infrastructure. Increasing integration with silicon carbide power modules is redefining next-generation system optimization and setting the stage for intensified strategic competition.

Current sensing resistors are rapidly transforming into mission-critical components for electric mobility, AI-driven power systems, industrial robotics, and renewable infrastructure, making the market increasingly strategic for technology investors and advanced electronics manufacturers. High-power battery systems now require sensing accuracy improvements exceeding 20% to optimize thermal management and charging performance, while compact resistor architectures are enabling nearly 18% higher power density across modern EV platforms. Supply-chain localization pressures and stricter energy-efficiency standards are simultaneously forcing procurement and design restructuring across the global electronics ecosystem.

Advanced metal alloy current sensing technology improves efficiency by 24% while reducing operational heat loss by 19% compared to legacy thick-film resistor systems. Asia-Pacific leads in production volume, while Europe leads in adoption innovation with nearly 33% faster integration of energy-efficient automotive electronics. Over the next three years, high-precision resistor deployment in industrial automation systems is projected to improve power monitoring efficiency by 21%, supported by accelerating smart-factory investments. ESG-focused manufacturers are also reducing energy waste by nearly 14% through low-resistance architectures, strengthening compliance positioning and lowering operational costs.

In 2025, a leading EV battery manufacturer improved inverter reliability by 16% after integrating ultra-low-ohmic sensing resistors into high-voltage control modules. Major component suppliers are shifting capital allocation toward localized fabrication, automotive-grade reliability testing, and silicon carbide-compatible resistor development to secure long-term supply resilience. Companies optimizing precision, thermal efficiency, and regional manufacturing alignment are establishing stronger competitive control in the next phase of the global current sensing resistors market.

Electric vehicle production growth and industrial electrification are forcing rapid expansion of precision current sensing resistor deployment across battery management systems, inverters, and fast-charging infrastructure. Demand for low-resistance metal strip resistors increased by 32% during 2025 as automakers prioritized higher thermal stability and accurate current monitoring in high-voltage architectures. Simultaneously, industrial automation investments expanded over 26%, accelerating integration into robotics and smart manufacturing equipment. Ongoing U.S.-China electronics supply-chain restructuring is also shifting sourcing toward regional manufacturing ecosystems, increasing localized component procurement. In response, major manufacturers are accelerating capacity expansion, securing alloy material contracts, and forming strategic partnerships with EV power module suppliers to strengthen production scalability and long-term delivery reliability globally.

Rising dependence on nickel, manganese, and specialty alloy materials is constraining production economics across the current sensing resistors market. Precision resistor manufacturing costs increased nearly 18% between 2024 and 2026 due to raw material inflation and higher automotive-grade compliance requirements. Asia controls more than 61% of specialty resistor alloy processing capacity, creating supply concentration risks during geopolitical trade disruptions and logistics bottlenecks. These pressures directly increase lead times, restrict margin flexibility, and slow scalable deployment across mid-tier electronics manufacturers. To reduce exposure, companies are diversifying supplier networks, locking long-term procurement agreements, and accelerating investment into alternative conductive materials and localized manufacturing facilities designed to stabilize pricing, improve sourcing resilience, and maintain production continuity globally.

AI server infrastructure, renewable energy storage, and advanced industrial power systems are creating high-value growth opportunities for precision current sensing technologies. Data-center power monitoring demand increased by 29% in 2025 as hyperscale facilities intensified energy optimization initiatives. Simultaneously, renewable inverter installations expanded over 24%, accelerating adoption of ultra-low resistance sensing architectures for high-efficiency current management. Integration with silicon carbide power modules is emerging as a major innovation shift, improving thermal performance by nearly 21% compared to traditional configurations. Manufacturers are aggressively increasing R&D investment, expanding automotive-grade product portfolios, and building ecosystem partnerships with power electronics firms to secure future dominance across fast-growing electrification, energy storage, and intelligent infrastructure markets globally through scalable integration capabilities.

Thermal management complexity, miniaturization requirements, and reliability expectations are redefining execution risks across the current sensing resistors market. Failure rates in compact high-current environments rise nearly 17% when resistor heat dissipation is not optimized for next-generation EV and industrial systems. At the same time, advanced electronics manufacturers are demanding over 25% smaller component footprints without sacrificing sensing accuracy or operational durability. Grid modernization delays and semiconductor packaging constraints are also slowing synchronized deployment across power electronics ecosystems. To remain competitive, companies must accelerate investment into advanced alloy engineering, automated precision manufacturing, and collaborative design partnerships with EV and industrial OEMs. Solving scalability, thermal endurance, and integration precision will determine long-term market leadership and supply-chain resilience globally.

31% increase in ultra-low resistance component deployment is reshaping EV power architectures. Automotive OEMs are replacing conventional thick-film designs with metal alloy and surface-mount current sensing resistors to reduce thermal drift and improve inverter stability. Precision resistor integration in fast-charging systems increased by 27% during 2025, while compact module adoption reduced board space requirements by 18%. Manufacturers are expanding automated production lines and restructuring supplier agreements to secure high-purity alloy materials amid ongoing semiconductor localization pressure.

24% rise in AI server power monitoring integration is redefining industrial resistor specifications. Data-center operators are deploying high-accuracy thin-film and metal plate resistors to optimize real-time current balancing across high-density power systems. Average sensing accuracy improved by 16%, while operational heat loss declined by 14% in advanced server racks. Electronics suppliers are responding through co-development partnerships with power module manufacturers and accelerating precision calibration technologies to manage increasing energy-efficiency compliance requirements across hyperscale infrastructure.

19% faster adoption of surface-mount architectures is optimizing electronics manufacturing efficiency. Consumer electronics and industrial automation companies are shifting toward compact SMD resistor configurations that improve assembly throughput by 22% and reduce manual calibration dependency. This transition is forcing legacy resistor suppliers to modernize fabrication capabilities and expand laser-trimming processes for tighter tolerance control. A non-obvious shift is emerging as smaller resistor footprints increase thermal engineering complexity, raising demand for integrated cooling-compatible component designs.

28% expansion in regionalized sourcing agreements is reshaping procurement and pricing models. North American and European manufacturers are reducing dependency on concentrated Asian supply chains following logistics disruptions and regulatory scrutiny tied to strategic electronics components. Dual-sourcing contracts increased by 21%, while localized inventory strategies shortened delivery cycles by 17%. Companies are responding through regional warehousing expansion, long-term alloy procurement contracts, and selective manufacturing partnerships designed to stabilize pricing and improve operational continuity under volatile trade conditions.

The Current Sensing Resistors Market is segmented by type, application, and end-user, with demand increasingly concentrated in high-efficiency electronics and electrified power systems. Shunt resistors and surface mount resistors collectively account for over 52% of component adoption due to compact integration advantages in EVs and industrial automation. Battery management systems and automotive electronics contribute nearly 46% of application demand as precision current monitoring becomes critical for thermal control and energy optimization. Automotive and electronics manufacturing together represent more than 58% of end-user consumption, while telecommunications and energy infrastructure are rapidly increasing deployment rates. Demand is shifting toward miniaturized, low-resistance architectures, forcing manufacturers to prioritize precision engineering, localized production, and advanced thermal performance capabilities.

Shunt Resistors dominate the Current Sensing Resistors Market with nearly 34% share due to their low-cost structure, high-current handling capability, and widespread integration across battery systems, industrial equipment, and automotive electronics. Their scalability and reliability in high-load environments continue strengthening deployment across electric mobility and power conversion platforms. However, Thin Film Resistors are emerging as the fastest-growing category, with adoption increasing by over 26% during 2025–2026 as manufacturers prioritize ultra-high precision, lower temperature coefficients, and compact electronics integration. Compared with Thick Film Resistors, thin-film technologies deliver nearly 19% higher measurement accuracy and improved stability in AI power systems and telecommunications hardware.

Metal Plate Resistors and Surface Mount Resistors collectively account for approximately 41% of market demand, driven by strong adoption in compact EV inverters, industrial robotics, and next-generation power modules. Thick Film Resistors retain niche relevance in cost-sensitive consumer electronics applications despite growing pressure from precision-focused alternatives. Companies are aggressively expanding automated SMD production, investing in alloy engineering, and repositioning product portfolios toward automotive-grade and high-efficiency resistor technologies. Investment focus is shifting toward compact, thermally optimized architectures, while legacy low-precision resistor categories are gradually losing strategic importance in advanced electronics manufacturing.

Automotive Electronics remains the leading application segment, accounting for nearly 31% of total demand due to accelerating integration of current sensing resistors across EV inverters, onboard chargers, battery protection systems, and power steering electronics. Usage concentration is driven by rising power density requirements and stricter energy-efficiency standards across global vehicle platforms. Battery Management Systems are the fastest-growing application area, with deployment increasing by over 29% as automakers intensify focus on thermal monitoring, charging optimization, and battery lifespan management. Compared with traditional Power Supplies applications, battery systems require significantly tighter resistance tolerances and faster response stability under high-current conditions.

Motor Control, Consumer Electronics, and Industrial Automation collectively contribute approximately 49% of application demand, supported by robotics deployment, smart manufacturing upgrades, and compact electronics miniaturization. Industrial automation systems are increasingly adopting precision sensing architectures to improve operational efficiency and predictive maintenance performance. In response, manufacturers are scaling low-ohmic resistor production, strengthening partnerships with automotive OEMs, and optimizing high-accuracy product lines for power-intensive applications. Demand is decisively shifting toward high-reliability sensing solutions capable of supporting intelligent electrification systems, making precision integration a critical competitive differentiator across advanced electronics markets.

Automotive leads the Current Sensing Resistors Market with approximately 36% share, driven by intensive resistor deployment across EV battery packs, motor drives, charging systems, and advanced vehicle electronics. Demand concentration remains high because electric vehicles require continuous high-accuracy current monitoring for thermal stability and power optimization. Energy and Utilities is emerging as the fastest-growing end-user category, with adoption increasing by nearly 25% as renewable energy storage systems and smart-grid infrastructure accelerate deployment of advanced power monitoring architectures. Compared with Electronics Manufacturing, which prioritizes scale and assembly efficiency, energy infrastructure buyers focus more heavily on durability, thermal endurance, and long-cycle operational reliability.

Industrial Equipment, Telecommunications, Healthcare Devices, and Electronics Manufacturing collectively account for nearly 48% of total demand, supported by industrial automation expansion, AI server infrastructure, and precision medical electronics integration. Telecommunications companies are increasingly demanding thin-film and surface-mount resistor solutions optimized for compact, high-frequency power environments. In response, manufacturers are introducing customized resistor platforms, expanding automotive-grade certifications, and strengthening long-term supply agreements with infrastructure operators. Future demand is shifting toward high-performance applications requiring tighter tolerance control, faster thermal response, and reliability-focused engineering, forcing suppliers to compete through precision manufacturing, vertical integration, and application-specific customization strategies.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

Asia-Pacific dominates global production and consumption due to large-scale electronics manufacturing, EV battery expansion, and integrated semiconductor supply chains across China, Japan, and South Korea. Europe contributes nearly 24% of demand, driven by strict energy-efficiency regulations and accelerated deployment of automotive power electronics. North America holds approximately 21% share but is rapidly increasing localized sourcing and AI power infrastructure investments, reshaping procurement and manufacturing strategies. Supply-chain diversification policies implemented after semiconductor disruptions continue forcing OEMs to regionalize critical electronic component sourcing. While Asia-Pacific leads in manufacturing scale, Europe advances precision innovation, and North America accelerates high-performance adoption. Global manufacturers are increasingly prioritizing regional production hubs, automotive-grade expansion, and strategic partnerships to secure resilience and long-term market positioning.

North America represents nearly 21% of the global Current Sensing Resistors Market, supported by strong demand across EV manufacturing, AI data centers, industrial automation, and aerospace electronics. Automotive-grade resistor deployment increased by 27% during 2025 as U.S.-based manufacturers accelerated battery management and fast-charging infrastructure investments. Semiconductor localization policies and supply-chain security initiatives are forcing companies to reduce overseas dependency and expand regional sourcing networks. Precision thin-film resistor adoption improved operational power efficiency by 16% in advanced server infrastructure, accelerating technology upgrades across enterprise power systems. Major suppliers are increasing localized manufacturing capacity and long-term OEM partnerships to strengthen delivery resilience. Enterprises increasingly prioritize reliability, thermal stability, and compliance-focused sourcing, making North America a critical region for high-performance electronics expansion and strategic investment.

Europe accounts for approximately 24% of global Current Sensing Resistors Market demand, led by Germany, France, and the Netherlands through advanced automotive electronics and industrial electrification programs. Strict carbon reduction and energy-efficiency mandates are accelerating deployment of ultra-low resistance sensing technologies across EV platforms and smart-grid infrastructure. Industrial power monitoring integration increased by 22% during 2025 as manufacturers optimized energy consumption and regulatory compliance performance. Automotive OEMs are increasingly shifting toward thin-film and metal plate resistor technologies to improve thermal accuracy and reduce operational power loss by nearly 15%. Enterprises across the region prioritize long-life reliability, precision engineering, and sustainability-aligned procurement standards. Europe continues forcing technology adaptation through compliance-driven innovation, making the region strategically critical for advanced resistor design and high-efficiency manufacturing investment.

Asia-Pacific remains the largest and fastest-scaling regional market, contributing nearly 48% of global Current Sensing Resistors Market demand and production volume. China, Japan, South Korea, and Taiwan dominate through vertically integrated electronics manufacturing, EV battery expansion, and semiconductor ecosystem concentration. Precision resistor deployment across automotive and industrial power systems increased by 31% during 2025, while localized manufacturing capacity expansion exceeded 24% across key electronics clusters. Companies are rapidly scaling automated surface-mount resistor production to support high-volume exports and cost-efficient electronics integration. Regional enterprises prioritize speed, scale, and procurement flexibility, creating strong demand for compact low-resistance architectures optimized for mass deployment. Asia-Pacific remains strategically essential for global supply continuity, production scalability, and accelerated commercialization of advanced power electronics technologies.

South America contributes approximately 5% of global Current Sensing Resistors Market demand, with Brazil and Argentina leading regional adoption across industrial automation, energy infrastructure, and automotive electronics assembly. Renewable energy expansion and industrial modernization projects increased precision resistor deployment by nearly 18% during 2025, particularly within motor control and power monitoring systems. However, import dependency and currency volatility continue constraining large-scale manufacturing expansion and increasing component procurement costs by over 12% across regional supply chains. Enterprises are responding through localized sourcing agreements and selective integration of lower-cost surface-mount resistor technologies. Buyers remain highly price-sensitive while prioritizing operational durability and maintenance efficiency. The region presents strong expansion potential for suppliers capable of balancing affordability, localized distribution, and resilient supply-chain execution under volatile economic conditions.

The Middle East & Africa region accounts for nearly 4% of global Current Sensing Resistors Market demand, driven by infrastructure modernization, industrial electrification, and smart energy investments across the UAE, Saudi Arabia, and South Africa. Deployment of precision current monitoring systems in utility-scale energy projects increased by 20% during 2025 as governments accelerated grid optimization and industrial automation programs. Oil and gas operators are increasingly adopting high-reliability sensing technologies to improve operational safety and reduce power instability across critical facilities. Strategic partnerships tied to renewable energy and smart-city development expanded localized electronics integration activity by approximately 14%. Enterprises prioritize long-life durability, environmental resistance, and energy-efficiency performance when selecting electronic components. The region is emerging as a strategic investment destination for suppliers targeting infrastructure-led power electronics expansion and industrial modernization demand.

China – 38% market share in the Current Sensing Resistors Market due to dominant electronics manufacturing capacity, EV battery production scale, and integrated semiconductor supply-chain infrastructure.

United States – 19% market share in the Current Sensing Resistors Market driven by strong demand from AI data centers, advanced automotive electronics, and localized power semiconductor investments.

The Current Sensing Resistors Market is defined by intense competition between global precision electronics leaders such as Vishay Intertechnology, Yageo Corporation, ROHM Semiconductor, KOA Speer Electronics, and Bourns, alongside regional cost-focused manufacturers competing aggressively in automotive and industrial supply chains. The top five players collectively control nearly 43% of market activity through advanced thin-film technologies, high-volume manufacturing scale, and long-term OEM partnerships. Competition is increasingly centered on thermal stability, miniaturization, and delivery resilience, with precision resistor accuracy improving over 18% in next-generation EV systems while automated production reduces manufacturing defects by nearly 14%. Companies are expanding localized production facilities, vertically integrating alloy sourcing, and accelerating surface-mount innovation to secure strategic positioning. Technology-driven consolidation and semiconductor ecosystem partnerships are redefining competitive advantage, while high capital requirements and automotive-grade certification standards create strong entry barriers. Winning requires precision engineering, scalable manufacturing, and resilient global supply execution.

Vishay Intertechnology

Yageo Corporation

ROHM Semiconductor

KOA Speer Electronics

Bourns Inc.

TT Electronics

Susumu Co., Ltd.

Panasonic Industry

Viking Tech Corporation

Stackpole Electronics

Ohmite Manufacturing Company

Cyntec Co., Ltd.

Walsin Technology Corporation

Advanced metal strip and thin-film resistor technologies are currently dominating high-performance applications across EVs, industrial automation, and AI power systems. Ultra-low-ohmic architectures reduced power dissipation by nearly 18% in high-current battery modules during 2025, while thin-film precision designs improved sensing accuracy by 21% compared to conventional thick-film resistors. More than 46% of automotive-grade current sensing deployments now use compact surface-mount configurations to optimize thermal stability and board density. Manufacturers are increasingly integrating laser-trimming and automated calibration systems to improve tolerance consistency, reduce production defects, and strengthen competitiveness in high-reliability electronics markets.

Emerging technologies are reshaping integration strategies across compact power electronics. Metal plate shunt resistors with ultra-low TCR values improved thermal performance by 16% in fast-switching silicon carbide power systems, while new wide-terminal structures enhanced heat dissipation efficiency by 14%. Compared with legacy shunt resistor platforms, next-generation alloy-based sensing technologies deliver nearly 24% higher current stability under high-load operating conditions. Electronics manufacturers are responding through localized fabrication expansion, advanced alloy engineering, and tighter partnerships with EV and renewable energy power module suppliers to accelerate deployment speed and improve supply resilience.

Disruptive developments between 2026 and 2028 are expected to redefine resistor miniaturization, thermal intelligence, and AI-enabled power monitoring. High-density 0201 resistor architectures are reducing component footprint requirements by over 20% in advanced telecommunications and automotive electronics systems. Simultaneously, integrated smart sensing platforms combining precision resistors with real-time analytics are optimizing predictive power management across industrial infrastructure. Companies investing aggressively in compact, low-loss, silicon carbide-compatible sensing technologies are securing operational advantages in next-generation electrification and intelligent energy systems.

October 2025 – Vishay Intertechnology introduced the WSLF1206 Power Metal Strip resistor with power ratings up to 5W and resistance values down to 0.3mΩ, delivering nearly 20x higher power capability within compact 1206 footprints. The launch strengthened board-space optimization and high-efficiency EV power system integration. [High-Density Scaling] Source: Vishay Intertechnology

June 2024 – ROHM Semiconductor expanded its PMR100 metal plate shunt resistor lineup with new 5W ultra-low resistance models supporting 0.5mΩ, 1mΩ, and 1.5mΩ configurations. The development improved miniaturization capability and thermal efficiency for automotive motor control and industrial power applications. [Miniaturization Push] Source: ROHM Semiconductor

March 2025 – Vishay Intertechnology launched WSBE Power Metal Strip shunt resistors featuring TCR values down to ±10 ppm/°C and power ratings up to 50W. The innovation reduced calibration complexity while improving current measurement precision across energy storage, automotive, and industrial infrastructure deployments. [Precision Optimization]

May 2025 – Vishay Intertechnology expanded its D2TO35 series automotive-grade thick-film power resistors with enhanced pulse absorption capability reaching 15J/0.1s, improving transient protection performance by 30%. The release strengthened reliability standards for EV power electronics and high-load industrial systems. [Pulse Protection Upgrade]

This report delivers a comprehensive analysis of the Current Sensing Resistors Market across core product types, applications, end-user industries, regional markets, and evolving power electronics technologies. Coverage includes shunt resistors, metal plate resistors, thick-film resistors, thin-film resistors, and surface-mount resistor architectures, alongside applications spanning battery management systems, automotive electronics, industrial automation, power supplies, and consumer electronics. The study evaluates demand trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while also examining strategic technology shifts linked to EV electrification, AI infrastructure, renewable energy systems, and high-density industrial electronics.

The report analyzes more than 10 leading global manufacturers and tracks key operational indicators including adoption concentration, sourcing patterns, deployment intensity, and component integration trends. Surface-mount resistor configurations account for over 35% of advanced electronics integration, while automotive and battery-related applications represent nearly 46% of precision sensing demand. The assessment also covers emerging technologies such as ultra-low TCR alloys, silicon carbide-compatible resistor systems, and compact 0201 architectures reshaping miniaturized electronics manufacturing.

Strategically, the report supports investment prioritization, product positioning, supply-chain planning, and regional expansion decisions through forward-looking analysis covering 2026–2033 technology adoption pathways, competitive restructuring, and evolving operational requirements across advanced power electronics ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4676 Million |

|

Market Revenue in 2033 |

USD 9317.22 Million |

|

CAGR (2026 - 2033) |

9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Vishay Intertechnology, Yageo Corporation, ROHM Semiconductor, KOA Speer Electronics, Bourns Inc., TT Electronics, Susumu Co., Ltd., Panasonic Industry, Viking Tech Corporation, Stackpole Electronics, Ohmite Manufacturing Company, Cyntec Co., Ltd., Walsin Technology Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |