Reports

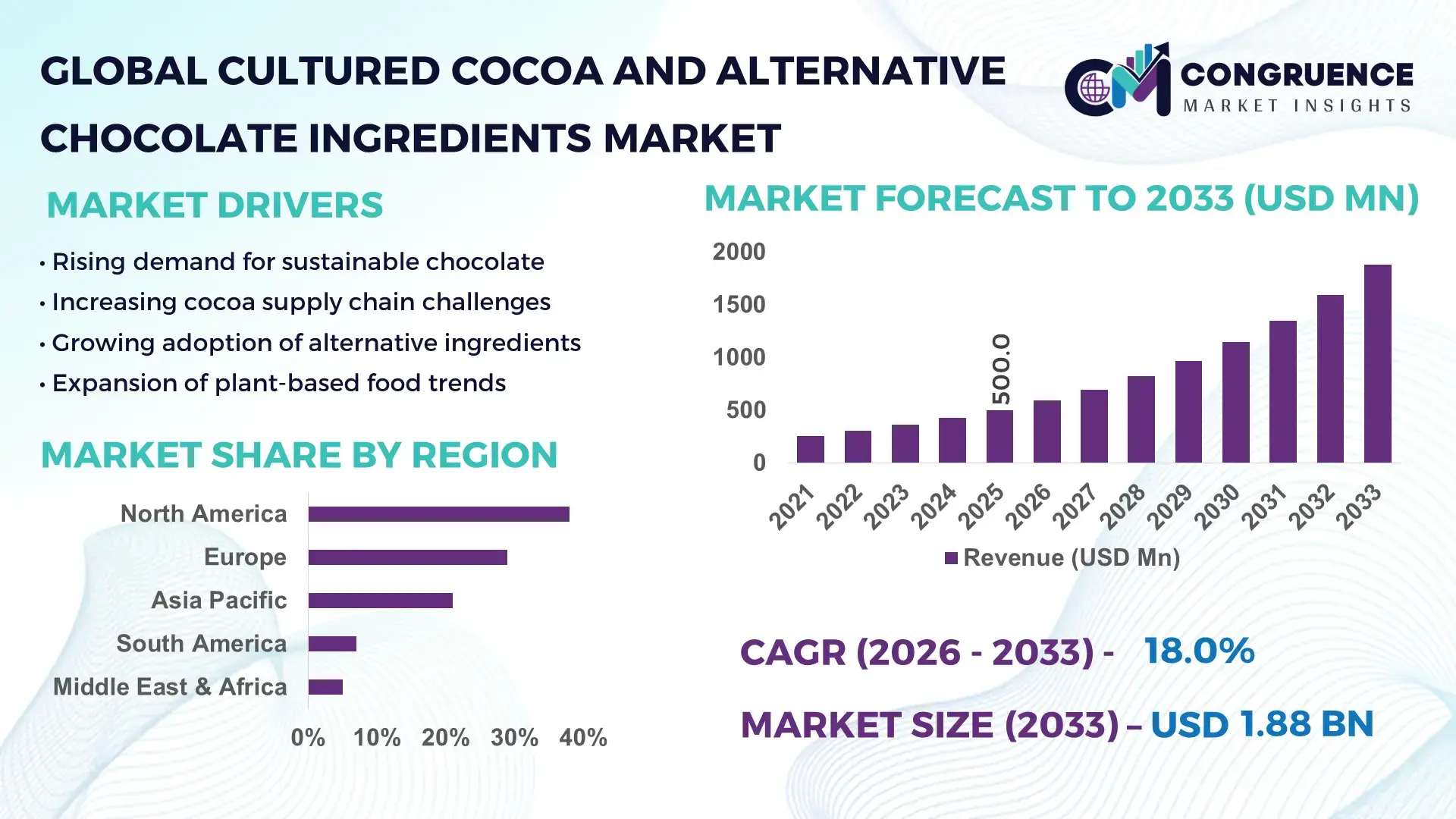

The Global Cultured Cocoa and Alternative Chocolate Ingredients Market was valued at USD 500.0 Million in 2025 and is anticipated to reach a value of USD 1,879.4 Million by 2033 expanding at a CAGR of 18% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by increasing demand for sustainable cocoa substitutes amid supply volatility and rising raw material costs.

The United States dominates the Cultured Cocoa and Alternative Chocolate Ingredients Market with strong investment in food biotechnology and precision fermentation. In 2025, over 65% of alternative chocolate startups were headquartered in the U.S., with fermentation-based ingredient production capacity exceeding 120,000 metric tons annually. The country has witnessed over USD 1.2 billion in venture funding for cocoa alternatives since 2020, supporting commercialization across confectionery, bakery, and beverage sectors. Consumer adoption rates for sustainable chocolate alternatives exceeded 28% among urban populations, while major food manufacturers have integrated alternative cocoa ingredients into over 15% of new product launches. Advanced R&D in cellular agriculture and flavor replication technologies continues to enhance scalability and product quality across industrial applications.

Market Size & Growth: USD 500.0 Million (2025) to USD 1,879.4 Million (2033), CAGR 18%, driven by supply-chain disruptions and sustainability mandates.

Top Growth Drivers: Sustainable sourcing adoption (42%), cost volatility mitigation (35%), alternative protein integration (28%).

Short-Term Forecast: By 2028, production costs expected to decline by 22% through process optimization.

Emerging Technologies: Precision fermentation, cellular agriculture, AI-based flavor synthesis.

Regional Leaders: North America (USD 720M by 2033, strong biotech adoption), Europe (USD 510M, regulatory-driven innovation), Asia-Pacific (USD 430M, rising consumption demand).

Consumer Trends: 38% of Gen Z consumers prefer sustainable chocolate alternatives; plant-based product demand rising.

Pilot Example: In 2024, a fermentation-based cocoa pilot improved yield efficiency by 31%.

Competitive Landscape: Leader holds ~18% share; key players include Voyage Foods, Planet A Foods, Endless Food Co., Nukoko.

Regulatory & ESG Impact: 45% of manufacturers adopting deforestation-free sourcing mandates.

Investment Patterns: Over USD 1.5 billion invested globally in alternative cocoa innovation since 2020.

Innovation Outlook: Integration of AI and biotech expected to enhance flavor replication accuracy by 40%.

The market encompasses confectionery (52%), bakery (23%), and beverage (15%) sectors, with innovations such as cocoa-free formulations and fermentation-derived cocoa compounds improving sustainability metrics by over 30%. Regulatory push for deforestation-free supply chains and rising consumer demand in Europe (41% sustainable preference) and North America (38%) are shaping adoption trends, while Asia-Pacific shows strong future consumption growth.

The Cultured Cocoa and Alternative Chocolate Ingredients Market holds strategic importance as global cocoa supply chains face increasing disruption due to climate variability and regulatory pressure. Precision fermentation delivers 35% higher yield efficiency compared to traditional cocoa farming methods, significantly reducing land dependency and environmental impact. The integration of AI-driven flavor engineering has improved taste replication accuracy by nearly 40%, enabling manufacturers to maintain product quality while reducing reliance on conventional cocoa sources.

Regionally, Africa dominates in volume due to traditional cocoa production, while North America leads in adoption with over 48% of enterprises investing in alternative cocoa technologies. By 2028, advanced fermentation systems are expected to reduce production costs by 25%, improving scalability for mass-market applications. Firms are committing to ESG metrics such as 50% reduction in deforestation-linked sourcing by 2030, aligning with global sustainability frameworks.

In 2025, a U.S.-based food-tech company achieved a 32% reduction in carbon emissions through precision fermentation-based cocoa production, demonstrating measurable sustainability benefits. These advancements are enabling food manufacturers to diversify sourcing strategies while enhancing supply chain resilience.

Looking ahead, the Cultured Cocoa and Alternative Chocolate Ingredients Market is positioned as a critical pillar of sustainable food innovation, ensuring resilience against supply shocks, compliance with environmental regulations, and long-term scalability across global confectionery industries.

The Cultured Cocoa and Alternative Chocolate Ingredients Market is evolving rapidly due to shifting supply-demand dynamics in the global cocoa industry. Increasing climate-related disruptions in cocoa-producing regions have led to production inconsistencies, impacting raw material availability for chocolate manufacturers. This has accelerated interest in alternative solutions such as fermentation-derived cocoa and cocoa-free formulations.

Technological advancements in food biotechnology, particularly in precision fermentation and cellular agriculture, are enabling the development of scalable, cost-efficient alternatives with improved flavor profiles. At the same time, regulatory frameworks emphasizing sustainable sourcing and deforestation-free supply chains are influencing procurement strategies among global food manufacturers. Consumer awareness around ethical sourcing and environmental impact is also contributing to increased adoption of alternative chocolate ingredients.

Additionally, investments in research and development, coupled with strategic partnerships between startups and established food companies, are strengthening the innovation ecosystem. However, challenges related to scalability, cost competitiveness, and consumer perception remain critical factors shaping market dynamics.

The demand for sustainable food ingredients has intensified as consumers and regulators push for environmentally responsible sourcing practices. Over 60% of global consumers now consider sustainability when purchasing food products, directly influencing manufacturers to adopt alternative cocoa ingredients. Traditional cocoa farming contributes to deforestation and carbon emissions, with approximately 70% of global cocoa production linked to regions experiencing environmental degradation. Alternative chocolate ingredients, particularly those derived from fermentation processes, offer up to 90% reduction in land usage and 80% lower water consumption compared to conventional cocoa farming. This significant environmental advantage is encouraging major confectionery companies to integrate these ingredients into their product portfolios. Additionally, sustainability certifications and eco-labeling initiatives are further accelerating adoption, making environmentally friendly products more appealing to consumers and retailers alike.

Despite strong growth potential, high production costs remain a major barrier to widespread adoption of cultured cocoa and alternative ingredients. Precision fermentation and cellular agriculture require advanced infrastructure, specialized bioreactors, and skilled labor, resulting in production costs that are currently 30–50% higher than traditional cocoa processing methods. Limited scalability also poses challenges, as many alternative cocoa producers operate at pilot or small commercial scales. Industrial-scale production facilities are still under development, restricting supply availability for large manufacturers. Additionally, inconsistencies in flavor replication and texture compared to traditional cocoa can impact consumer acceptance, particularly in premium chocolate segments. These factors collectively slow market penetration, especially in price-sensitive regions where cost competitiveness is critical for adoption.

Technological innovation presents significant opportunities for expanding the Cultured Cocoa and Alternative Chocolate Ingredients Market. Advances in synthetic biology and fermentation technologies are improving production efficiency by over 35%, enabling manufacturers to scale operations more effectively. AI-driven flavor engineering is also enhancing product quality, allowing companies to closely mimic the taste and texture of traditional cocoa. Emerging markets in Asia-Pacific and Latin America offer untapped growth potential, with rising urbanization and increasing demand for premium confectionery products. Additionally, partnerships between food-tech startups and global confectionery brands are accelerating commercialization efforts, enabling faster market entry and wider distribution. The development of hybrid chocolate products, combining traditional cocoa with alternative ingredients, is further expanding product offerings and consumer acceptance.

Regulatory complexity remains a significant challenge in the Cultured Cocoa and Alternative Chocolate Ingredients Market, as novel food products must comply with stringent safety and labeling standards across different regions. Approval processes for fermentation-derived ingredients can take several years, delaying product commercialization. Consumer perception also poses challenges, as some consumers remain skeptical about lab-grown or synthetic food products. Surveys indicate that nearly 35% of consumers are hesitant to adopt alternative chocolate ingredients due to concerns about taste and naturalness. Additionally, labeling requirements and transparency expectations add complexity for manufacturers, requiring clear communication of product benefits and production processes. Addressing these challenges is essential for achieving widespread market acceptance and growth.

Precision fermentation adoption rising by 45% across food-tech companies: The use of fermentation-based cocoa alternatives has increased significantly, with over 45% of new food-tech startups focusing on microbial or yeast-based production systems. These technologies have improved yield efficiency by nearly 30% while reducing reliance on traditional agricultural inputs, supporting scalable production models.

Cocoa-free chocolate product launches increasing by 38% annually: Major confectionery brands are expanding their portfolios with cocoa-free alternatives, with product launches growing by 38% year-on-year. These products are gaining traction among environmentally conscious consumers, with adoption rates exceeding 32% in urban markets across Europe and North America.

Investment in alternative ingredient R&D exceeding 50% growth: Research and development spending in alternative chocolate ingredients has surged, with over 50% growth in funding allocations toward synthetic biology and flavor engineering technologies. This has enabled improvements in taste accuracy by nearly 40% and enhanced product consistency.

Sustainable sourcing commitments reaching 60% among manufacturers: Approximately 60% of global food manufacturers have committed to deforestation-free sourcing policies, driving demand for alternative cocoa ingredients. These initiatives are supported by regulatory frameworks and consumer demand for ethically sourced products, accelerating market adoption.

The Cultured Cocoa and Alternative Chocolate Ingredients Market is segmented based on type, application, and end-user, each contributing uniquely to overall market development. Product types include fermentation-based cocoa, cocoa-free chocolate compounds, and plant-based chocolate alternatives, each offering distinct advantages in sustainability and cost optimization. Fermentation-based cocoa dominates due to its ability to replicate traditional cocoa flavor while reducing environmental impact.

Applications span confectionery, bakery, beverages, and dairy alternatives, with confectionery accounting for the largest adoption due to high consumption volumes. End-users include food manufacturers, specialty chocolate producers, and foodservice providers, each leveraging alternative ingredients to meet sustainability goals and evolving consumer preferences. Increasing innovation and diversification across these segments are enhancing product offerings and expanding market reach globally.

Fermentation-based cocoa currently leads the Cultured Cocoa and Alternative Chocolate Ingredients Market, accounting for approximately 46% of total adoption due to its ability to closely replicate traditional cocoa flavor profiles while offering significant sustainability benefits. Cocoa-free chocolate compounds hold around 32% share, driven by cost efficiency and reduced dependency on volatile cocoa supply chains. However, plant-based chocolate alternatives are emerging as the fastest-growing segment, expected to expand at a CAGR of 21% through 2033, supported by rising consumer demand for vegan and allergen-free products. Other niche types, including hybrid cocoa blends and lab-cultured cocoa derivatives, collectively contribute nearly 22% of the market, catering to specialized applications in premium and functional chocolate products. These segments are gaining traction due to their ability to combine traditional taste with innovative ingredient profiles.

• In 2025, a leading food-tech institute demonstrated fermentation-derived cocoa achieving 95% flavor similarity to conventional cocoa in controlled sensory evaluations, supporting its commercial viability.

Confectionery remains the leading application segment, accounting for approximately 52% of market adoption, as chocolate products represent the primary use case for alternative cocoa ingredients. Bakery applications hold around 24%, driven by demand for sustainable and cost-effective ingredients in cakes, pastries, and snacks. Beverage applications account for 14%, with increasing use in cocoa-based drinks and nutritional formulations. Dairy alternatives and functional foods are the fastest-growing applications, expected to expand at a CAGR of 20% through 2033, supported by rising health-conscious consumer trends and demand for plant-based products. Collectively, other niche applications contribute nearly 10% of the market. In 2025, more than 41% of global food manufacturers reported integrating alternative cocoa ingredients into at least one product line. Additionally, over 36% of consumers indicated willingness to try cocoa-free chocolate products.

• In 2024, a global food research organization reported deployment of alternative cocoa ingredients in over 200 commercial product formulations, improving sustainability metrics across multiple categories.

Food manufacturers dominate the end-user segment, accounting for approximately 58% of market adoption, as they integrate alternative cocoa ingredients into large-scale production lines. Specialty chocolate producers hold around 26% share, focusing on premium and niche product offerings that emphasize sustainability and innovation. Foodservice providers contribute approximately 16%, driven by increasing demand for sustainable menu options. Foodservice is the fastest-growing end-user segment, expected to expand at a CAGR of 19% through 2033, supported by rising consumer demand for sustainable dining experiences. Over 44% of global restaurants are exploring alternative ingredients to reduce environmental impact. Additionally, nearly 39% of consumers prefer brands that offer sustainable chocolate options.

• In 2025, an international food innovation body reported that over 500 foodservice outlets adopted alternative cocoa ingredients to enhance sustainability and reduce supply chain risks.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20% between 2026 and 2033.

North America leads due to strong investment in food technology, with over 55% of global alternative cocoa startups based in the region. Europe follows with a 29% share, driven by stringent sustainability regulations and high consumer awareness, while Asia-Pacific accounts for 21%, supported by rising demand in countries such as China, India, and Japan. South America and Middle East & Africa collectively contribute 12%, with growing interest in sustainable ingredient sourcing. Increasing regional investments, regulatory frameworks, and consumer demand are shaping the global market landscape.

North America holds approximately 38% of the global market, driven by strong demand from the confectionery and food manufacturing industries. The region benefits from advanced R&D infrastructure and significant investment in food biotechnology, with over 60% of startups focusing on fermentation-based cocoa solutions. Regulatory support for sustainable food production and increasing adoption of ESG practices are further boosting market growth. Technological advancements, including AI-driven flavor engineering and precision fermentation, are enabling improved product quality and scalability. For example, a U.S.-based startup has developed cocoa-free chocolate formulations with over 90% flavor similarity to traditional products. Consumer behavior in the region shows high adoption of sustainable products, with over 40% of consumers prioritizing eco-friendly chocolate alternatives.

Europe accounts for approximately 29% of the global market, with key countries including Germany, the UK, and France leading adoption. Strict regulatory frameworks promoting deforestation-free supply chains and sustainable sourcing are driving demand for alternative cocoa ingredients. Over 50% of European consumers prefer sustainably sourced chocolate products, influencing manufacturers to adopt innovative solutions. The region is also witnessing increased adoption of precision fermentation and plant-based technologies, supported by government incentives and research funding. A European food-tech company recently introduced cocoa-free chocolate products with improved sustainability metrics, reducing environmental impact significantly. Consumer behavior reflects strong preference for transparency and eco-labeling, further accelerating market adoption.

Asia-Pacific represents approximately 21% of the global market, with China, India, and Japan being the प्रमुख consuming countries. Rapid urbanization and increasing disposable income are driving demand for premium and sustainable chocolate products. The region is emerging as a key manufacturing hub, with growing investments in food processing infrastructure and alternative ingredient production. Technological innovation is also accelerating, with several startups focusing on fermentation-based cocoa solutions. Consumer behavior indicates strong growth potential, with rising adoption of plant-based and sustainable food products. E-commerce platforms are playing a crucial role in expanding product availability and consumer reach across the region.

South America accounts for approximately 7% of the global market, with Brazil and Argentina leading regional adoption. The region’s strong agricultural base provides opportunities for integrating alternative cocoa production with existing supply chains. Government initiatives promoting sustainable agriculture and trade policies supporting innovation are driving market development. Local companies are exploring hybrid cocoa solutions to enhance production efficiency and reduce environmental impact. Consumer behavior shows increasing interest in sustainable products, particularly among urban populations. The region’s growing focus on value-added food products is further supporting market expansion.

The Middle East & Africa region contributes approximately 5% to the global market, with countries such as the UAE and South Africa leading adoption. Increasing demand from foodservice and hospitality sectors is driving the use of alternative chocolate ingredients. Technological modernization and investments in food processing infrastructure are supporting market growth. Trade partnerships and regulatory frameworks promoting sustainable sourcing are encouraging adoption of alternative ingredients. Consumer behavior varies across the region, with growing interest in premium and sustainable products in urban markets. Local companies are exploring innovative solutions to meet evolving consumer preferences and industry requirements.

United States – 38% Market share: High investment in food-tech innovation and large-scale production capacity

Germany – 14% Market share: Strong regulatory push and advanced food processing industry

The Cultured Cocoa and Alternative Chocolate Ingredients Market is moderately fragmented, with over 40 active players competing across various segments, including fermentation-based cocoa, cocoa-free chocolate, and plant-based alternatives. The top five companies collectively account for approximately 45% of the market, indicating a competitive yet evolving landscape.

Key players are focusing on strategic initiatives such as partnerships with global confectionery brands, product innovation, and expansion of production capacities. For instance, collaborations between food-tech startups and established chocolate manufacturers are enabling faster commercialization and wider distribution of alternative products. Additionally, mergers and acquisitions are becoming increasingly common as companies seek to strengthen their market position and technological capabilities.

Innovation remains a critical competitive factor, with companies investing heavily in R&D to improve flavor replication, production efficiency, and scalability. The adoption of advanced technologies such as AI-driven flavor engineering and precision fermentation is further intensifying competition, as players strive to differentiate their offerings and capture market share.

Planet A Foods

Nukoko

Endless Food Co.

Celleste Bio

California Cultured

Win-Win

Fooditive

Cargill

Barry Callebaut

Nestlé

Mars Incorporated

Olam Food Ingredients

Givaudan

Technological innovation is a cornerstone of the Cultured Cocoa and Alternative Chocolate Ingredients Market, with precision fermentation emerging as a dominant production method. This technology enables the cultivation of cocoa-like compounds using microorganisms, achieving up to 90% reduction in land usage and 80% lower water consumption compared to traditional cocoa farming.

AI-driven flavor engineering is another critical advancement, allowing manufacturers to replicate the complex flavor profile of cocoa with over 95% accuracy. Machine learning algorithms analyze chemical compositions and optimize ingredient formulations, improving product consistency and consumer acceptance. Cellular agriculture is also gaining traction, enabling the production of cocoa cells in controlled environments, reducing dependency on climate-sensitive agricultural practices.

Automation and digitalization are further enhancing production efficiency, with smart bioreactors improving yield rates by nearly 30%. Blockchain technology is being integrated into supply chains to ensure transparency and traceability, addressing consumer concerns about sourcing and sustainability. These technological advancements are not only improving scalability but also reducing production costs, making alternative cocoa ingredients more competitive in the global market.

• In April 2024, Cargill announced a commercial partnership with Voyage Foodsto scale cocoa-free chocolate alternatives globally. Cargill became the exclusive B2B distributor, enabling integration of sustainable, allergen-free ingredients across bakery, ice cream, and confectionery applications. Source: www.cargill.com

• In November 2025, Barry Callebaut and Planet A Foodsentered a long-term partnership to commercialize cocoa-free chocolate solutions. The collaboration focuses on scaling ChoViva, a sunflower-based chocolate alternative, to reduce supply chain dependency and improve sustainability outcomes.

• In October 2024, Voyage Foods initiated development of a 284,000-square-foot manufacturing facility in Ohio to scale production of cocoa-free chocolate and related products, significantly expanding industrial capacity and supporting large-scale commercialization of alternative chocolate ingredients.

• In December 2024, Planet A Foods secured $30 million in Series B funding to industrialize its fermentation-based platform and expand production of cocoa-free ingredients, reinforcing its position as a leading innovator in sustainable chocolate alternatives.

The Cultured Cocoa and Alternative Chocolate Ingredients Market Report provides a comprehensive analysis of emerging technologies, product innovations, and industry trends shaping the global market landscape. The report covers key segments, including fermentation-based cocoa, cocoa-free chocolate compounds, and plant-based alternatives, offering detailed insights into their applications across confectionery, bakery, beverages, and dairy alternatives.

Geographically, the report examines market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional variations in adoption, regulatory frameworks, and consumer preferences. It also explores the role of advanced technologies such as precision fermentation, AI-driven flavor engineering, and cellular agriculture in transforming production processes and enhancing scalability.

The report further analyzes end-user segments, including food manufacturers, specialty chocolate producers, and foodservice providers, providing insights into adoption patterns and industry-specific requirements. Additionally, it evaluates competitive strategies, innovation trends, and investment patterns, offering a holistic view of the market.

By integrating qualitative and quantitative insights, the report serves as a valuable resource for decision-makers, enabling them to identify growth opportunities, assess market risks, and develop effective strategies in the rapidly evolving Cultured Cocoa and Alternative Chocolate Ingredients Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 500.0 Million |

| Market Revenue (2033) | USD 1,879.4 Million |

| CAGR (2026–2033) | 18% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Voyage Foods; Planet A Foods; Nukoko; Endless Food Co.; Celleste Bio; California Cultured; Win-Win; Fooditive; Cargill; Barry Callebaut; Nestlé; Mars Incorporated; Olam Food Ingredients; Givaudan |

| Customization & Pricing | Available on Request (10% Customization Free) |