Reports

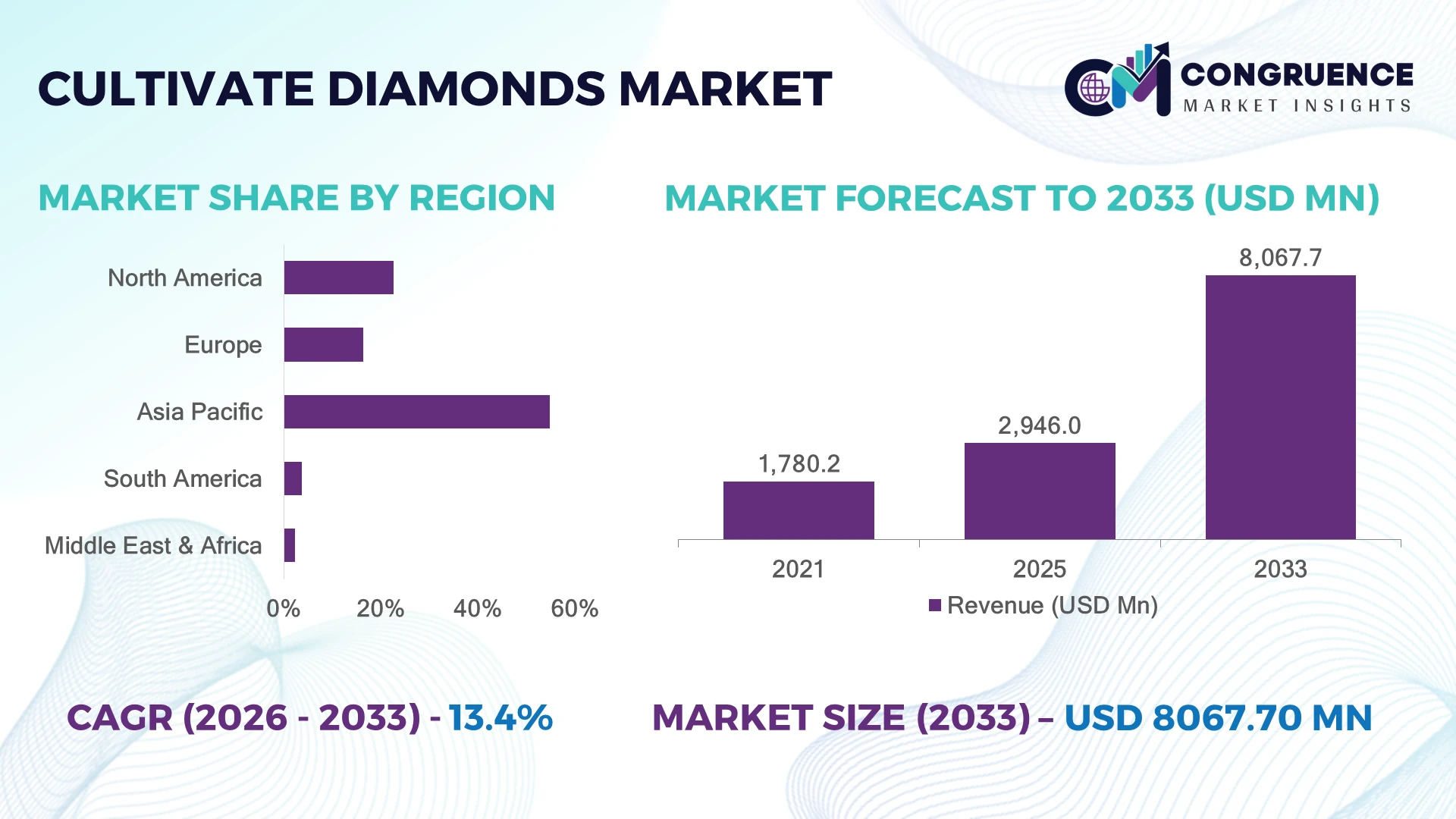

The Global Cultivate Diamonds Market was valued at USD 2,946.0 Million in 2025 and is anticipated to reach a value of USD 8067.7 Million by 2033 expanding at a CAGR of 13.42% between 2026 and 2033. Rising adoption of chemical vapor deposition (CVD) technology, expanding sustainable luxury jewelry demand, and increasing industrial use in precision electronics and semiconductor manufacturing are accelerating market expansion.

China dominates the global cultivated diamonds ecosystem with over 45% of global production capacity, supported by large-scale HPHT manufacturing facilities and continuous investments in advanced synthetic crystal technologies. India follows as the fastest-growing polishing and jewelry manufacturing hub, processing more than 90% of the world's polished diamonds while rapidly expanding lab-grown diamond exports. Strong manufacturing ecosystems, export incentives, and advanced production infrastructure reinforce leadership across the value chain.

Companies strengthening production efficiency, certified traceability, and regional manufacturing partnerships are securing stronger competitive positioning across premium jewelry and industrial applications.

Market Size & Growth: USD 2,946.0 Million in 2025, projected to reach USD 8,067.7 Million by 2033 at 13.42% growth, driven by advanced CVD manufacturing and sustainable luxury adoption.

Top Growth Drivers: CVD production expansion (+30%), sustainable jewelry preference (+55%), and industrial semiconductor applications (+20%) continue strengthening global demand.

Short-Term Forecast: By 2028, production efficiency is expected to improve by nearly 25% while manufacturing costs decline by approximately 18% through automation.

Emerging Technologies: AI-enabled crystal monitoring, automated reactor controls, and advanced plasma-enhanced CVD systems improve quality consistency and operational precision.

Regional Leaders: Asia Pacific exceeds USD 3.9 Billion through manufacturing expansion, North America approaches USD 2.1 Billion with premium jewelry adoption, while Europe surpasses USD 1.4 Billion through sustainability-focused demand.

Consumer/End-User Trends: More than 60% of younger luxury buyers actively consider lab-grown diamonds because of ethical sourcing and environmental transparency.

Pilot/Case Example: In 2024, automated CVD production facilities achieved nearly 22% higher crystal yield while reducing production defects by around 15%.

Competitive Landscape: Leading manufacturers collectively account for approximately 40% market presence, including Diamond Foundry, WD Lab Grown Diamonds, Greenlab Diamonds, Lusix, and New Diamond Technology.

Regulatory & ESG Impact: Carbon footprint reductions exceeding 70% compared with conventional mining strengthen compliance with evolving sustainability standards across major export markets.

Investment & Funding: More than USD 1 Billion in manufacturing expansion, technology partnerships, and production capacity investments supports global supply-chain diversification.

Innovation & Future Outlook: Next-generation reactor optimization, digital certification platforms, and high-purity industrial diamond production are redefining long-term competitive strategies.

Cultivate Diamonds Market demand continues expanding across luxury jewelry, semiconductor components, thermal management systems, and precision cutting applications. Manufacturers are introducing AI-assisted crystal optimization, higher-efficiency CVD reactors, and blockchain-enabled certification platforms to improve quality assurance. More than 60% of premium jewelry retailers now include lab-grown collections, while evolving sustainability regulations and diversified global supply chains continue reshaping sourcing and manufacturing strategies, setting the foundation for broader strategic transformation.

The cultivated diamonds market has become strategically important as manufacturers, jewelry brands, and industrial technology companies prioritize resilient supply chains, ethical sourcing, and advanced materials. Expansion of regional manufacturing clusters across Asia and North America, together with increasing traceability requirements and sustainability-focused procurement, is reshaping competitive dynamics. Companies are strengthening localized production networks to improve supply security and reduce dependence on mined diamond availability.

Modern chemical vapor deposition technology delivers approximately 25% higher crystal consistency while reducing production costs by nearly 18% compared with conventional manufacturing processes. Asia Pacific continues to lead large-scale production through manufacturing capacity, whereas North America emphasizes premium branded jewelry, advanced industrial applications, and certified product innovation. Over the next two to three years, automated production systems are expected to increase manufacturing throughput by nearly 20%, supporting faster commercialization and improved product quality.

Leading producers are expanding strategic partnerships with jewelry retailers, electronics manufacturers, and certification organizations while investing in automated production infrastructure and digital verification platforms. Sustainability-focused manufacturing practices, efficient resource utilization, and transparent product authentication are strengthening competitive differentiation, enabling companies to secure long-term operational advantages and reinforce their position across both luxury and industrial end-use markets.

Chemical Vapor Deposition (CVD) technology is reshaping cultivated diamond production by improving crystal consistency, reducing processing time, and enabling scalable manufacturing. More than 65% of newly commissioned production facilities now prioritize CVD systems, while automated process controls improve usable crystal yield by approximately 20% and reduce quality variation by nearly 18%. India continues expanding polishing capacity alongside growing domestic lab-grown diamond manufacturing, supported by export-focused industrial policies, while the United States strengthens premium branded production through technology investments. This combination of manufacturing efficiency and ethical sourcing is driving broader commercial adoption. Producers are expanding reactor capacity, investing in AI-enabled quality monitoring, and forming technology partnerships to secure higher throughput, lower defect rates, and stronger global competitiveness.

Despite technological advances, inconsistent certification frameworks and energy-intensive manufacturing remain structural constraints for cultivated diamond producers. Electricity represents nearly 30% of total production expenditure in several manufacturing facilities, while certification differences across export destinations increase compliance costs by approximately 15%. China continues to dominate production capacity, creating supply concentration that exposes manufacturers to trade policy adjustments and logistics disruptions. These conditions affect pricing consistency, inventory planning, and international market acceptance. Companies are responding by diversifying manufacturing locations, securing long-term renewable energy agreements, adopting internationally recognized grading standards, and expanding localized processing operations to improve operational resilience and strengthen customer confidence across premium jewelry markets.

Expanding industrial demand presents opportunities beyond jewelry as cultivated diamonds gain wider acceptance in semiconductor components, quantum technologies, and thermal management solutions. More than 40% of ongoing product development initiatives now target industrial-grade applications, while digital certification platforms reduce product verification time by approximately 35%. India is strengthening its digital diamond ecosystem through traceability initiatives, and the United States continues investing in advanced materials research for next-generation electronics. Companies are increasing research collaborations, integrating blockchain-enabled authentication, and developing high-purity synthetic crystals for precision manufacturing. This strategic diversification enables higher-value applications while reducing dependence on traditional luxury jewelry demand and expanding long-term commercial potential.

Maintaining consistent premium-quality production across expanding manufacturing facilities remains one of the industry's most significant execution challenges. Approximately 12% of cultivated diamonds still require additional post-production processing because of crystal inconsistencies, while scaling automated manufacturing without compromising quality demands continuous capital investment and skilled technical expertise. Rapid production expansion in China and India has intensified competition for experienced materials engineers and reactor specialists, creating workforce constraints for advanced manufacturing operations. Companies must strengthen process standardization, expand technical workforce development, and deploy AI-assisted production monitoring to maintain product consistency. Long-term competitiveness will increasingly depend on manufacturing precision, reliable certification, and resilient production infrastructure rather than production volume alone.

Advanced CVD Process Automation – Diamond producers are integrating AI-enabled reactor controls and automated crystal monitoring to improve manufacturing precision. More than 65% of newly commissioned production lines now incorporate digital process control, while crystal yield has improved by nearly 20% and defect rates have declined by approximately 15%. Rising electricity costs and increasing quality certification requirements are encouraging companies in India and the United States to modernize production facilities through automation partnerships and smart manufacturing platforms that improve consistency and reduce production cycles.

Digital Traceability Gains Momentum – Blockchain-based certification and digital product passports are becoming standard across premium cultivated diamond supply chains. Around 55% of leading jewelry brands have expanded digital traceability programs, reducing authentication time by nearly 35% while improving customer transparency. Tightening sustainability expectations and evolving export compliance are prompting manufacturers to collaborate with certification providers and technology firms to strengthen product verification and enhance international market acceptance.

Industrial Demand Diversification – Demand is expanding beyond luxury jewelry as cultivated diamonds gain wider adoption in semiconductor manufacturing, thermal management, and precision optics. Industrial applications now represent nearly 30% of advanced synthetic diamond utilization, while demand for electronic-grade materials has increased by approximately 18%. Manufacturers are restructuring production portfolios, developing application-specific crystal grades, and strengthening partnerships with electronics companies to secure higher-value commercial opportunities.

Localized Manufacturing Expansion – Countries are strengthening domestic production ecosystems to reduce supply concentration and improve operational resilience. India has expanded integrated polishing and manufacturing capacity, while the United States continues investing in premium production facilities and advanced materials research. Local sourcing initiatives have shortened delivery timelines by nearly 22% and reduced logistics dependence by approximately 15%. Companies are scaling regional facilities, establishing strategic supplier networks, and increasing investment in localized processing to improve responsiveness and long-term supply-chain stability.

Chemical Vapor Deposition (CVD) Diamonds represent the leading segment, accounting for approximately 68% of cultivated diamond production because of superior scalability, high crystal purity, and greater flexibility for both jewelry and industrial applications. Automated reactor technologies and AI-assisted quality monitoring have improved production efficiency by nearly 20%, enabling manufacturers to deliver consistent gem-quality crystals while lowering rejection rates. Companies continue expanding CVD reactor capacity and investing in advanced plasma technologies to strengthen operational performance and support growing global demand. High Pressure High Temperature (HPHT) Diamonds remain strategically important, particularly for industrial applications requiring exceptional hardness and durability. HPHT is also the fastest-growing segment for specialized industrial-grade production, supported by rising demand from electronics and advanced manufacturing. Nearly 35% of new industrial diamond investments target upgraded HPHT facilities to improve crystal quality and production reliability. Manufacturers are balancing investments between mature CVD production and specialized HPHT innovation, creating a diversified portfolio capable of serving both premium jewelry and high-performance industrial markets.

Jewelry remains the dominant application, contributing approximately 70% of cultivated diamond demand as consumers increasingly prioritize certified, ethically sourced, and design-focused products. More than 60% of premium jewelry retailers now offer dedicated lab-grown collections, while customized engagement jewelry continues expanding across India, the United States, and the United Kingdom. Manufacturers are strengthening branded collections, enhancing digital certification, and expanding retail partnerships to improve customer confidence and accelerate premium product adoption. Electronics & Semiconductors represent the fastest-growing application as cultivated diamonds gain recognition for superior thermal conductivity and material stability. Industrial Tools, Thermal Management, Quantum Technologies, Optical Components, Healthcare & Medical Devices, and Research & Development continue expanding through application-specific innovation and precision engineering. Around 25% of industrial research programs now evaluate synthetic diamond materials for next-generation electronic systems and quantum devices. Companies are increasing production of application-specific crystal grades while collaborating with technology developers to broaden commercial deployment across advanced manufacturing sectors.

Jewelry Manufacturers remain the largest end-user group, representing approximately 65% of cultivated diamond consumption because of strong demand for sustainable luxury products, customized designs, and certified gemstones. Retailers continue expanding premium collections supported by digital authentication and transparent sourcing practices. Nearly 58% of new branded jewelry launches now include cultivated diamond offerings, encouraging producers to strengthen long-term supply agreements, manufacturing capacity, and design collaborations to maintain competitive differentiation. Electronics & Semiconductor Companies constitute the fastest-growing end-user segment as demand rises for high-performance thermal management materials and advanced electronic components. Industrial Manufacturing Companies maintain stable procurement for cutting and machining applications, while Healthcare & Medical Device Manufacturers, Research Institutes & Universities, Aerospace & Defense Organizations, Automotive Manufacturers, and Energy & Power Companies continue exploring specialized synthetic diamond solutions. Around 22% of advanced materials research programs now incorporate cultivated diamonds for emerging industrial technologies. Companies are responding through customized product development, strategic partnerships, and application-focused innovation to address increasingly specialized operational requirements.

Asia-Pacific accounted for the largest market share at 54.8% in 2025 however, North America is expected to register the fastest growth, expanding at a 14.6% CAGRbetween 2026 and 2033.

North America accounted for approximately 22.6% of the global cultivated diamonds market in 2025, supported by premium jewelry demand, advanced CVD manufacturing, and strong investment in certified sustainable products. The United States continues expanding domestic production capacity through automated manufacturing, AI-assisted quality inspection, and digital traceability platforms. More than 60% of premium jewelry retailers across the region now offer cultivated diamond collections, while enterprise partnerships between manufacturers and luxury brands continue strengthening supply reliability. Growing semiconductor research also supports industrial-grade diamond production for thermal management applications. Companies are increasing automation investments, expanding domestic manufacturing facilities, and integrating blockchain-based authentication to improve operational efficiency, strengthen consumer confidence, and reduce dependence on imported finished products.

United States Market Outlook: The United States remains the region's technology and branding leader through vertically integrated manufacturing, advanced CVD research, and premium retail distribution. Domestic producers continue investing in automated reactor technologies and digital certification infrastructure, while demand for ethically sourced luxury products supports consistent production expansion. Nearly 65% of cultivated diamond sales in North America originate from the United States, reinforcing its leadership across manufacturing, innovation, branded retail partnerships, and advanced industrial material development.

Europe represented approximately 16.4% of global market demand in 2025, driven by sustainability regulations, responsible sourcing requirements, and expanding premium jewelry consumption. Manufacturers and retailers increasingly prioritize certified low-carbon products to comply with evolving environmental expectations and strengthen consumer trust. More than 55% of luxury jewelry collections introduced by leading European brands now include cultivated diamond options. Investments in digital product passports and transparent supply-chain management continue improving traceability and operational efficiency. Companies are strengthening supplier qualification programs, expanding partnerships with certified producers, and modernizing retail authentication systems to maintain premium positioning while supporting sustainable procurement objectives.

Germany Market Outlook: Germany serves as Europe's leading technology and manufacturing hub for advanced materials and precision engineering. Industrial research organizations continue evaluating cultivated diamonds for electronics, optics, and thermal management applications alongside premium jewelry manufacturing. Approximately 30% of regional industrial diamond innovation projects involve German enterprises, supported by advanced manufacturing capabilities, engineering expertise, and strong collaboration between industrial companies, research institutions, and technology developers.

Asia-Pacific held the largest share of the cultivated diamonds market at approximately 54.8% in 2025 due to its extensive manufacturing ecosystem, integrated polishing infrastructure, and strong export capabilities. China leads synthetic diamond production through large-scale HPHT and CVD manufacturing, while India dominates polishing, jewelry manufacturing, and international exports. More than 70% of global cultivated diamond processing capacity is concentrated across these two countries. Continuous investment in automated production lines, quality control technologies, and manufacturing expansion supports high-volume production while improving operational efficiency. Companies continue scaling facilities, strengthening export partnerships, and investing in advanced crystal growth technologies to reinforce competitive leadership across global markets.

India Market Outlook: India has emerged as the region's most strategically significant cultivated diamond hub by combining world-leading polishing expertise with rapidly expanding domestic production. The country processes more than 90% of the world's polished diamonds while increasing investments in CVD manufacturing and export-oriented facilities. Government support, skilled technical labor, and integrated jewelry manufacturing continue strengthening India's position as a preferred destination for global cultivated diamond production and value-added processing.

South America accounted for approximately 3.8% of the global cultivated diamonds market in 2025, supported by growing premium jewelry demand, expanding retail modernization, and increasing awareness of sustainable gemstones. Brazil continues leading regional market activity through established jewelry manufacturing and improving distribution networks. Retailers are expanding certified cultivated diamond collections while strengthening digital sales channels and customer education initiatives. Nearly 28% of premium jewelry retailers in major metropolitan markets now include cultivated diamond product lines. Companies are improving regional logistics partnerships, strengthening sourcing agreements, and investing in retail expansion to improve product accessibility despite relatively limited domestic manufacturing capacity.

Brazil Market Outlook: Brazil remains the region's largest jewelry production and retail market, supported by a well-established gemstone industry and expanding luxury consumer base. Domestic manufacturers are integrating cultivated diamonds into premium collections while strengthening partnerships with international suppliers to improve product availability. Continued investment in branded retail networks and digital commerce platforms supports broader market penetration and enhances long-term operational competitiveness.

The Middle East & Africa represented approximately 2.4% of global cultivated diamond demand in 2025, driven by expanding luxury retail infrastructure, premium consumer spending, and increasing investment in branded jewelry distribution. The United Arab Emirates has become a regional trading and distribution hub supported by modern logistics infrastructure and international jewelry exhibitions. More than 40% of regional premium jewelry imports are distributed through the UAE, strengthening its strategic role in cultivated diamond trade. Companies continue expanding retail partnerships, enhancing certified product portfolios, and improving regional distribution capabilities to serve growing demand for sustainable luxury products.

United Arab Emirates Market Outlook: The United Arab Emirates continues strengthening its position as the region's primary luxury jewelry trading and distribution center through advanced logistics infrastructure, international trade connectivity, and supportive commercial policies. Dubai's global diamond ecosystem attracts leading jewelry brands and international suppliers, while expanding premium retail networks and digital certification adoption improve customer confidence. Continued investment in high-value retail infrastructure reinforces the country's importance within the regional cultivated diamond value chain.

The competitive landscape is led by Diamond Foundry, Greenlab Diamonds, New Diamond Technology, Lusix, and WD Lab Grown Diamonds, competing against regional manufacturers in India and China on technology, quality, and production efficiency rather than price alone. The top five participants collectively control approximately 42% of the global market, while specialized producers compete through premium positioning and industrial-grade applications. Competition centers on automated CVD technology, crystal quality, certification, and vertically integrated supply chains, with advanced manufacturers achieving nearly 20% higher production efficiency and reducing defect rates by approximately 15% through AI-assisted process optimization. Companies are expanding manufacturing capacity, strengthening retailer partnerships, investing in proprietary reactor technologies, and integrating polishing and certification to improve speed and traceability. Competitive momentum is shifting toward technology leadership and supply-chain control as digital authentication and industrial applications gain importance. High capital requirements, technical expertise, and certification credibility remain major entry barriers. Winning requires scalable manufacturing, consistent crystal quality, trusted certification, and differentiated application-focused innovation.

Greenlab Diamonds

New Diamond Technology

Lusix

WD Lab Grown Diamonds

IIa Technologies

Pure Grown Diamonds

Adamas One Corp.

Ethereal Green Diamond LLP

Fenix Diamonds

Limelight Diamonds

Swarovski Created Diamonds

Advanced Chemical Vapor Deposition (CVD) technology remains the foundation of cultivated diamond manufacturing, enabling higher crystal purity, improved scalability, and greater production consistency. More than 65% of newly commissioned manufacturing facilities now utilize automated CVD platforms integrated with AI-based process monitoring. These systems improve usable crystal yield by nearly 20%, reduce quality variation, and enable faster production cycles. Digital production analytics and predictive maintenance are becoming standard across high-capacity manufacturing facilities.

Emerging technologies are transforming manufacturing and product authentication. AI-enabled reactor optimization, blockchain-based traceability, and digital certification platforms are now deployed across approximately 55% of premium cultivated diamond supply chains. Compared with conventional manual process control, automated manufacturing improves operational efficiency by nearly 25% while reducing production defects by around 15%. Companies investing in vertically integrated digital manufacturing benefit from stronger quality consistency, faster customer verification, and improved export compliance.

Between 2026 and 2028, adoption of advanced plasma reactors, digital twins, and automated crystal inspection is expected to accelerate across premium jewelry and industrial applications. Technology leaders developing semiconductor-grade and quantum-grade synthetic diamonds will strengthen competitive positioning. Companies that combine manufacturing automation, traceability, and advanced materials engineering will secure higher-value contracts while improving operational resilience and long-term market differentiation.

May 2025 – De Beers Group announced the planned closure of its Lightbox lab-grown diamond jewelry business, refocusing Element Six exclusively on industrial synthetic diamond applications after wholesale lab-grown diamond prices declined by about 90%. This reinforces industry specialization. Source: www.debeersgroup.com

June 2025 – Gemological Institute of America (GIA) introduced a new descriptive quality assessment system for laboratory-grown diamonds, replacing traditional color and clarity grading with two quality categories. The move is reshaping certification standards and improving market differentiation. Source: www.gia.edu

July 2025 – International Gemological Institute (IGI) reaffirmed its commitment to maintaining the 4Cs grading methodology for laboratory-grown diamonds, strengthening grading consistency and retailer confidence while supporting transparent global trade practices. Source: www.igi.org

December 2025 – Limelight Diamonds announced vertical integration into in-house diamond growing and manufacturing alongside a INR 250 crore expansion initiative targeting 200 stores by 2027, improving supply-chain control and accelerating product launches.

This report provides comprehensive analysis of the cultivated diamonds market across Chemical Vapor Deposition (CVD) and High Pressure High Temperature (HPHT) technologies, covering applications including jewelry, industrial tools, electronics & semiconductors, thermal management, quantum technologies, optical components, healthcare & medical devices, and research & development. It further evaluates demand across jewelry manufacturers, industrial companies, semiconductor enterprises, healthcare organizations, research institutes, aerospace, automotive, and energy sectors while assessing market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report combines technology assessment, competitive benchmarking, supply-chain analysis, regional deployment trends, and strategic company profiling. It highlights segment leadership, adoption patterns, manufacturing developments, and enterprise investment priorities, supported by operational indicators such as production concentration, technology penetration, and application expansion. The analysis enables stakeholders to evaluate investment opportunities, expansion strategies, competitive positioning, technology adoption pathways, and evolving business priorities expected to shape the cultivated diamonds market between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,946.0 Million |

| Market Revenue (2033) | USD 8,067.7 Million |

| CAGR (2026–2033) | 13.42% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Diamond Foundry; Greenlab Diamonds; New Diamond Technology; Lusix; WD Lab Grown Diamonds; IIa Technologies; Pure Grown Diamonds; Adamas One Corp.; Ethereal Green Diamond LLP; Fenix Diamonds; Limelight Diamonds; Swarovski Created Diamonds |

| Customization & Pricing | Available on Request (10% Customization Free) |