Reports

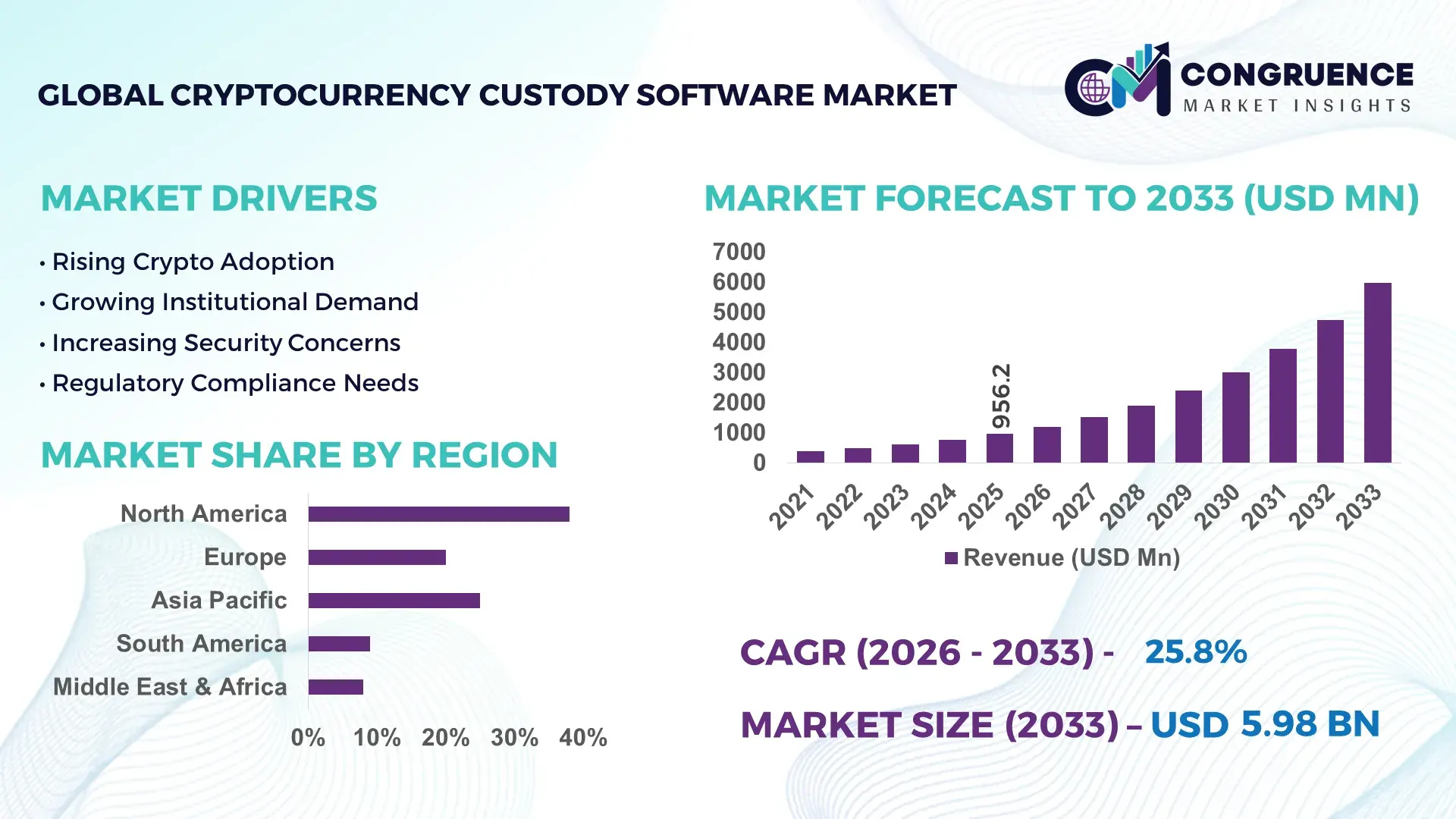

The Global Cryptocurrency Custody Software Market was valued at USD 956.22 Million in 2025 and is anticipated to reach a value of USD 5978.95 Million by 2033 expanding at a CAGR of 25.75% between 2026 and 2033. Growth is being driven by institutional digital asset adoption, stricter custody compliance requirements, expansion of tokenized financial products, and increasing deployment of multi-signature, MPC-based, and automated asset protection platforms across banking, wealth management, and exchange ecosystems.

The United States remains the dominant country, accounting for approximately 38% of global cryptocurrency custody software deployments in 2026, supported by expanding digital asset ETF ecosystems, over USD 100 billion in institutional crypto holdings under management, and widespread adoption among regulated financial institutions. Compared with the United Kingdom, where adoption remains concentrated among fintech and investment firms, the U.S. demonstrates nearly 2.5 times higher enterprise custody implementation rates. Ongoing digital asset policy discussions and post-ETF market expansion continue strengthening demand for advanced custody infrastructure.

Organizations prioritizing scalable, regulation-ready custody architectures are positioned to capture institutional asset flows and strengthen competitive positioning in the evolving digital finance landscape.

Market Size & Growth: USD 956.22 Million in 2025, projected to reach USD 5978.95 Million by 2033 at 25.75% CAGR, driven by institutional digital asset custody modernization.

Top Growth Drivers: Institutional adoption (+42%), tokenization initiatives (+35%), and compliance-focused custody upgrades (+31%) accelerate market expansion.

Short-Term Forecast: By 2028, automated custody workflows improve operational efficiency by 28% while reducing asset administration costs by 22%.

Emerging Technologies: MPC security, AI-driven risk monitoring, and smart contract automation improve transaction validation accuracy by over 30%.

Regional Leaders: North America exceeds USD 2.3 Billion, Europe approaches USD 1.5 Billion, and Asia-Pacific surpasses USD 1.2 Billion with expanding institutional adoption.

Consumer/End-User Trends: More than 60% of institutional investors prioritize regulated custody platforms before allocating digital asset capital.

Pilot/Case Example: In 2026, enterprise MPC custody deployments reported approximately 40% faster authorization workflows and 25% lower operational risk exposure.

Competitive Landscape: Leading providers hold nearly 18% market share collectively, with competition centered on security, compliance, scalability, and interoperability.

Regulatory & ESG Impact: Enhanced compliance frameworks reduced audit preparation time by roughly 35% across regulated custody operations.

Investment & Funding: Global investment exceeded USD 1.8 Billion, supported by strategic partnerships, infrastructure expansion, and institutional onboarding programs.

Innovation & Future Outlook: Advanced tokenization support, programmable custody, and cross-chain asset management are reshaping high-growth digital finance ecosystems.

Cryptocurrency custody software is experiencing strong demand from banks, asset managers, exchanges, and tokenization platforms seeking institutional-grade security and regulatory readiness. More than 55% of new deployments now incorporate multi-party computation and automated compliance monitoring capabilities. Recent innovation focuses on programmable custody, real-time risk analytics, and cross-chain asset support, while evolving digital asset regulations are encouraging enterprises to adopt scalable, audit-ready infrastructure, setting the stage for broader strategic transformation.

Cryptocurrency custody software has become a strategic infrastructure layer for digital asset markets as institutional investors, banks, and asset managers prioritize secure ownership, compliance, and operational control. Competitive differentiation is increasingly tied to custody capabilities rather than trading functionality alone. Regulatory standardization across major financial markets and expanding tokenization initiatives are accelerating infrastructure modernization, with more than 60% of institutional digital asset programs now requiring advanced custody frameworks as a prerequisite for deployment.

Technology transformation is reshaping operating models. Multi-party computation (MPC) custody architectures reduce key-management vulnerabilities and improve transaction authorization efficiency by approximately 35% compared with traditional cold-storage workflows while lowering administrative overhead by nearly 20%. The United States leads large-scale institutional deployment through established digital asset investment ecosystems, while Singapore continues to advance innovation through regulated fintech infrastructure and tokenization initiatives. Over the next two to three years, enterprise-grade custody integrations are expected to expand by more than 30% as organizations consolidate fragmented digital asset operations.

A practical example is the integration of custody software with treasury management and tokenized asset platforms, enabling automated governance and audit workflows. Companies are increasing investment in compliance technology, interoperability partnerships, and cross-chain asset support. Organizations that establish scalable, regulation-ready custody ecosystems will strengthen operational resilience, attract institutional capital, and secure long-term competitive positioning.

Institutional participation is transforming custody requirements from a security function into a core financial infrastructure capability. More than 65% of large digital asset investment programs now prioritize regulated custody frameworks, while enterprise demand for multi-signature and MPC-based environments has increased by approximately 40% over the past two years. In the United States, expansion of tokenized financial products and digital asset investment vehicles has accelerated enterprise onboarding requirements. This shift is increasing demand for automated governance, compliance monitoring, and asset segregation capabilities. In response, custody software providers are expanding integration partnerships with banks, fintech platforms, and infrastructure vendors. A notable strategic outcome is that custody platforms with embedded compliance automation are reducing onboarding cycles by nearly 25%, creating a measurable operational advantage for institutional service providers.

Regulatory inconsistency across jurisdictions remains a significant barrier to scalable deployment. Compliance-related implementation expenses can account for 20%–30% of total custody platform deployment costs, while cross-border licensing variations increase operational complexity. In countries such as Japan and Switzerland, regulatory frameworks are more mature, whereas several emerging markets continue to operate under evolving digital asset rules. This fragmentation complicates product standardization and slows enterprise expansion strategies. Additionally, integrating custody systems with legacy banking infrastructure can extend deployment timelines by over 30%. To mitigate these constraints, companies are adopting modular compliance architectures, local regulatory partnerships, and jurisdiction-specific deployment models. The key operational insight is that regulatory adaptability increasingly determines platform scalability as much as technological capability.

The expansion of tokenized securities, digital bonds, and real-world assets is creating new demand layers for advanced custody infrastructure. Industry estimates indicate that tokenized asset initiatives have increased by more than 35% across financial institutions, while automated asset servicing capabilities improve operational efficiency by approximately 25%. Singapore and the United Kingdom are actively supporting tokenization frameworks that require sophisticated custody and governance solutions. Emerging innovations such as programmable custody, smart-contract policy enforcement, and cross-chain asset management are opening opportunities beyond traditional cryptocurrency storage. Companies are investing in R&D, interoperability standards, and ecosystem partnerships to capture these use cases. A less obvious opportunity lies in custody platforms becoming transaction orchestration layers for tokenized finance, significantly expanding their role within digital asset value chains.

As institutional digital asset volumes increase, maintaining security, performance, and interoperability simultaneously becomes more difficult. Nearly 70% of enterprise custody operators identify cross-platform integration and security management as major execution challenges, while cybersecurity spending in digital asset infrastructure has risen by approximately 30%. The United States and Germany are experiencing growing pressure to support larger transaction volumes without compromising governance controls. Expanding support for multiple blockchains, token standards, and compliance frameworks introduces operational complexity that legacy architectures struggle to manage. Companies must invest in scalable cloud-native infrastructure, advanced cryptographic technologies, and specialized cybersecurity expertise. The strategic challenge extends beyond protection alone; organizations that fail to balance security, performance, and interoperability risk losing institutional clients and long-term market relevance.

MPC Adoption Accelerates Enterprise Security: Multi-party computation architectures are replacing traditional key-management models across institutional deployments, with adoption rising by nearly 45% since 2024. Enterprises report approximately 30% faster authorization workflows and 20% lower operational intervention requirements. Regulatory scrutiny of digital asset controls in the United States is pushing firms toward cryptographic security frameworks. Providers are expanding MPC integration partnerships and embedding automated governance layers to improve scalability without increasing security overhead.

Compliance Automation Reshapes Operations: Custody platforms are integrating automated compliance engines, reducing audit preparation workloads by approximately 35% and lowering manual reporting tasks by 40%. Financial institutions are responding to evolving digital asset regulations through real-time monitoring and policy-based transaction controls. A notable shift is the convergence of custody and compliance functions into unified platforms. Vendors are increasing investment in reporting automation, workflow orchestration, and regulatory intelligence capabilities to streamline institutional onboarding and operational management.

Tokenized Asset Support Expands: More than 50% of newly launched institutional custody solutions now support tokenized securities and real-world assets alongside cryptocurrencies. Enterprise demand for multi-asset custody environments has increased by approximately 32%, particularly in the United Kingdom and Singapore. This transition is improving asset administration efficiency while reducing platform fragmentation. Companies are prioritizing interoperability partnerships and programmable custody capabilities to capture emerging tokenized finance workflows and broaden service portfolios.

Cross-Chain Infrastructure Gains Priority: Institutional clients increasingly require support for multiple blockchain ecosystems, driving a 38% increase in cross-chain custody deployments. Organizations managing diversified digital asset portfolios are reducing asset transfer complexity by nearly 25% through integrated custody frameworks. A less obvious trend is the growing use of unified transaction routing layers to optimize operational consistency across networks. Providers are restructuring product roadmaps around interoperability, API integration, and cloud-native deployment architectures.

Hybrid Custody represents the leading segment due to its ability to balance security, accessibility, and operational scalability. Approximately 38% of institutional deployments now utilize hybrid models that combine cold-storage protection with hot-wallet transaction capabilities. This structure supports faster settlement, reduced operational bottlenecks, and seamless integration with trading, reporting, and compliance systems. Cold Wallet Custody remains critical for long-term asset protection and continues to dominate highly regulated financial environments, while Third-Party Custody maintains relevance among organizations seeking outsourced infrastructure and compliance support.

Hybrid Custody is also the fastest-growing segment as enterprises prioritize operational flexibility without compromising governance requirements. Adoption rates have increased by nearly 30% over the past two years as digital asset service providers expand transaction-intensive use cases. Self-Custody continues attracting technology-focused enterprises seeking direct asset control, though implementation complexity limits large-scale adoption. Hot Wallet Custody remains essential for liquidity management despite higher security management requirements. In response, software vendors are enhancing hybrid platforms through MPC integration, automated policy controls, and cross-chain interoperability features, reflecting a broader shift toward adaptable institutional custody architectures.

Asset Storage remains the dominant application segment because secure preservation of digital assets remains the foundational requirement across banks, exchanges, and investment firms. Nearly 45% of custody software deployments are primarily focused on institutional-grade asset protection, disaster recovery, and governance controls. Demand remains concentrated in organizations managing large digital asset inventories where operational resilience and security assurance are critical. Digital Asset Management is also expanding steadily as institutions seek consolidated visibility across increasingly diverse token portfolios and blockchain environments.

Compliance & Reporting is emerging as the fastest-growing application segment, supported by stricter oversight requirements and rising institutional participation. Automated compliance deployments have increased by approximately 35%, while organizations report up to 30% reductions in reporting workloads. Institutional Trading continues driving demand for real-time custody integration and transaction execution capabilities, whereas Transaction Management applications are gaining traction through workflow automation and settlement optimization. Vendors are responding by integrating reporting engines, compliance monitoring tools, and transaction orchestration features directly into custody environments, making these capabilities operationally indispensable.

Cryptocurrency Exchanges represent the leading end-user segment due to their continuous transaction volumes, liquidity management requirements, and dependence on secure asset custody infrastructure. Approximately 40% of enterprise custody deployments are linked directly to exchange operations, where uptime, transaction speed, and security controls remain mission-critical. Exchanges require integrated custody environments capable of supporting high-volume asset movements while maintaining governance and risk-management standards. Banks and broader Financial Institutions continue expanding deployments as digital asset services become integrated into traditional financial offerings.

Asset Managers are the fastest-growing end-user group as institutional investors increase allocations to digital assets and tokenized products. Adoption among professional investment organizations has risen by approximately 33% over the last two years. Hedge Funds increasingly require advanced custody systems to support diversified strategies and operational transparency, while Enterprises are adopting custody software for treasury management and tokenized asset initiatives. Vendors are responding through customized compliance features, strategic banking partnerships, and scalable pricing models. Competitive positioning is increasingly tied to the ability to address institution-specific governance and integration requirements.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 28.4% between 2026 and 2033.

Institutional Infrastructure and Regulatory Alignment Drive Scale

North America maintains its leadership position through deep institutional participation, advanced digital asset infrastructure, and expanding custody integration across banks, exchanges, and asset managers. The region accounts for approximately 39% of global deployments, supported by growing adoption of tokenized financial products and regulated digital asset services. More than 65% of large-scale institutional custody implementations are concentrated in the United States and Canada. Enterprise demand increasingly centers on MPC security, compliance automation, and cross-chain asset support. Recent partnership activity between custody providers and financial institutions has reduced enterprise onboarding timelines by nearly 25%, improving operational efficiency while strengthening regulatory readiness and governance capabilities.

United States Market Outlook: The United States remains the strategic center of cryptocurrency custody software deployment due to its concentration of institutional investors, digital asset service providers, and financial technology innovators. The country benefits from mature cloud infrastructure, advanced cybersecurity capabilities, and increasing integration of digital asset custody into mainstream financial services. More than 70% of institutional digital asset platforms operating in North America maintain custody infrastructure or operational headquarters in the United States. Investment activity continues to focus on compliance automation, tokenized asset management, and enterprise-grade security architectures.

Compliance Modernization Reshapes Custody Architecture

Europe is strengthening its position through regulatory standardization, institutional digital asset adoption, and expanding tokenization initiatives. The region represents approximately 27% of global market activity, with demand increasingly focused on secure custody frameworks aligned with evolving compliance requirements. Financial institutions are modernizing custody infrastructure to support digital asset governance, reporting, and interoperability. More than 50% of new enterprise deployments incorporate automated compliance and transaction monitoring capabilities. Strategic partnerships between fintech firms and regulated financial institutions are accelerating implementation timelines while enhancing operational transparency and institutional confidence.

Germany Market Outlook: Germany leads the European market through its strong financial infrastructure, technology ecosystem, and progressive approach to regulated digital asset services. The country has become a focal point for institutional custody deployment, particularly among banks and investment firms seeking secure digital asset management capabilities. Approximately 35% of enterprise-grade custody implementations within major European financial hubs involve German-based institutions. Demand is increasingly concentrated around tokenized assets, digital securities, and integrated compliance management, positioning Germany as a key innovation center for institutional custody solutions.

Digital Asset Expansion Fuels Rapid Deployment

Asia-Pacific is emerging as the fastest-expanding market due to increasing digital asset adoption, fintech innovation, and government-supported financial technology initiatives. The region accounts for roughly 23% of global deployments and is experiencing strong demand for scalable custody infrastructure supporting institutional trading and tokenized asset ecosystems. Enterprise implementation activity has increased by nearly 35% over the past two years. Organizations are investing heavily in cloud-native custody platforms, interoperability capabilities, and automated governance systems. Regional financial centers continue attracting strategic partnerships focused on expanding digital asset infrastructure and institutional service offerings.

Singapore Market Outlook: Singapore serves as the region’s most influential custody software hub due to its advanced fintech ecosystem, regulatory clarity, and concentration of digital asset enterprises. The country has established itself as a preferred location for institutional custody operations supporting regional and international markets. More than 40% of large-scale digital asset infrastructure projects announced in Southeast Asia involve Singapore-based organizations. Companies continue expanding investments in tokenization, programmable finance, and cross-border digital asset services, reinforcing Singapore’s leadership in institutional custody innovation.

Financial Digitization Expands Enterprise Adoption

South America is witnessing increasing demand for cryptocurrency custody software as enterprises seek secure infrastructure for digital asset management and transaction governance. The region contributes approximately 6% of global market activity and is benefiting from growing fintech adoption and expanding digital payment ecosystems. Financial institutions are increasingly deploying custody platforms to improve asset protection and operational control. Enterprise implementation activity has risen by nearly 20% since 2024. However, infrastructure maturity and regulatory consistency vary significantly across markets, creating deployment complexity that providers address through localized partnerships and modular compliance frameworks.

Brazil Market Outlook: Brazil represents the largest custody software opportunity in South America due to its extensive fintech sector, active digital asset user base, and growing institutional participation. The country is experiencing increased integration of custody solutions across exchanges, financial institutions, and investment platforms. Nearly half of regional enterprise custody deployments are concentrated in Brazil. Companies are prioritizing cybersecurity investments, compliance enhancements, and interoperability capabilities to support expanding digital asset operations while improving institutional trust and operational resilience.

Investment-Led Infrastructure Transformation Accelerates Adoption

The Middle East & Africa market is advancing through financial modernization initiatives, digital transformation programs, and increasing investment in emerging financial technologies. The region contributes approximately 5% of global market activity, with deployment concentrated in key financial and innovation hubs. Government-backed digital economy programs and private-sector investment are encouraging adoption of institutional-grade custody solutions. Deployment activity has increased by nearly 22% over the past two years as organizations strengthen digital asset governance and security frameworks. Strategic alliances between technology providers and financial institutions continue supporting infrastructure expansion and operational readiness.

United Arab Emirates Market Outlook: The United Arab Emirates has established itself as the region’s primary digital asset infrastructure hub through proactive innovation initiatives, advanced financial services capabilities, and strong investment activity. The country attracts international custody providers seeking access to institutional clients and cross-border digital asset markets. More than 45% of enterprise-focused custody initiatives within the Middle East are linked to organizations operating in the UAE. Investment priorities increasingly focus on tokenization infrastructure, regulatory technology integration, and institutional digital asset services.

The cryptocurrency custody software market is led by Fireblocks, BitGo, Anchorage Digital, Copper Technologies, Ledger Enterprise, and Taurus, competing across institutional security, compliance automation, interoperability, and transaction efficiency. The top five players collectively control approximately 48% of market activity, creating a moderately concentrated structure where technology leaders compete against specialized regional providers and emerging infrastructure innovators. Competition centers on MPC security, cross-chain functionality, compliance integration, and deployment speed. Platforms offering automated governance reduce operational workloads by nearly 30%, while advanced transaction orchestration improves processing efficiency by approximately 25%. Companies are expanding through banking partnerships, tokenization ecosystem alliances, and integration with institutional trading platforms. The competitive shift is moving from basic asset protection toward full-service digital asset infrastructure, including compliance, reporting, and programmable custody capabilities. High regulatory compliance costs and cybersecurity investment requirements remain significant barriers. Winning requires scalable security architecture, seamless institutional integration, regulatory adaptability, and continuous innovation in digital asset operations.

Fireblocks

BitGo

Anchorage Digital

Copper Technologies

Taurus

Ledger Enterprise

Hex Trust

Qredo

Cobo

Zodia Custody

Fordefi

Gemini Custody

Coinbase Custody

Fidelity Digital Assets

Cryptocurrency custody software is increasingly built around Multi-Party Computation (MPC), Hardware Security Modules (HSMs), and automated policy engines. MPC deployments now account for nearly 55% of new institutional implementations because they eliminate single-key vulnerabilities while improving transaction authorization efficiency by approximately 30%. Automated governance frameworks reduce manual approval workloads by nearly 25%, enabling financial institutions to manage larger digital asset portfolios without proportional staffing increases. Integration with banking systems, trading platforms, and compliance engines is becoming a standard deployment requirement, creating operational continuity across custody, settlement, and reporting functions.

Emerging technologies include AI-driven anomaly detection, real-time compliance monitoring, and cross-chain custody orchestration. AI-powered monitoring tools improve threat detection accuracy by roughly 20% while reducing investigation times by 15%. More than 40% of enterprise custody platforms now support multi-chain asset management, reflecting growing demand for tokenized securities and diversified digital asset portfolios. Organizations adopting integrated compliance automation report faster onboarding and lower audit preparation requirements, creating measurable operational advantages in regulated environments.

Between 2026 and 2028, programmable custody, smart-contract policy enforcement, and confidential computing are expected to reshape institutional infrastructure. Compared with legacy cold-storage workflows, programmable custody environments can improve operational flexibility by nearly 35%. Technology leaders that combine MPC, automation, and interoperability will benefit most, as institutions increasingly prioritize scalable digital asset operations over standalone storage capabilities.

July 2025 – BitGo confidentially filed for a U.S. public listing amid rising institutional demand for digital asset infrastructure. The broader cryptocurrency market surpassed USD 4 trillion in value during the period, strengthening institutional custody activity and increasing visibility for regulated custody providers. Source: Reuters

December 2024 – Anchorage Digital launched Porto, a self-custody wallet designed specifically for institutional users, expanding enterprise-grade custody options. The development strengthened institutional asset-control capabilities while supporting growing demand for secure governance frameworks across professional digital asset management operations. Source: Anchorage Digital

April 2026 – BitGo expanded institutional platform capabilities by supporting 186 of the top 250 digital assets by market capitalization through a unified custody, trading, settlement, and financing environment. The enhancement reduced operational fragmentation and improved workflow efficiency for institutional clients. Source: BitGo Investor Relations

May 2026 – BitGo and Virtune expanded European exchange-traded product infrastructure through a custody partnership supporting broader digital asset coverage. The initiative added institutional-grade custody backed by up to USD 250 million in insurance coverage, strengthening regulated digital asset access for European investors. Source: BitGo Investor Relations

This report provides comprehensive analysis of the Cryptocurrency Custody Software Market across key custody models, including Hot Wallet Custody, Cold Wallet Custody, Hybrid Custody, Self-Custody, and Third-Party Custody. The study evaluates major application areas such as Asset Storage, Transaction Management, Institutional Trading, Digital Asset Management, and Compliance & Reporting. Coverage extends across banks, cryptocurrency exchanges, asset managers, hedge funds, financial institutions, and enterprises, reflecting more than 90% of institutional custody deployment activity within the digital asset ecosystem.

The report assesses market performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while examining emerging opportunities in tokenized assets, programmable custody, multi-party computation, compliance automation, and cross-chain infrastructure. Analysis includes deployment trends, technology adoption patterns, competitive positioning, regulatory developments, and enterprise investment priorities between 2026 and 2033. Strategic insights support market entry planning, product development, partnership evaluation, expansion initiatives, and long-term competitive decision-making in an increasingly institutionalized digital asset environment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 956.22 Million |

|

Market Revenue in 2033 |

USD 5978.95 Million |

|

CAGR (2026 - 2033) |

25.75% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Fireblocks, BitGo, Anchorage Digital, Copper Technologies, Taurus, Ledger Enterprise, Hex Trust, Qredo, Cobo, Zodia Custody, Fordefi, Gemini Custody, Coinbase Custody, Fidelity Digital Assets |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |