Reports

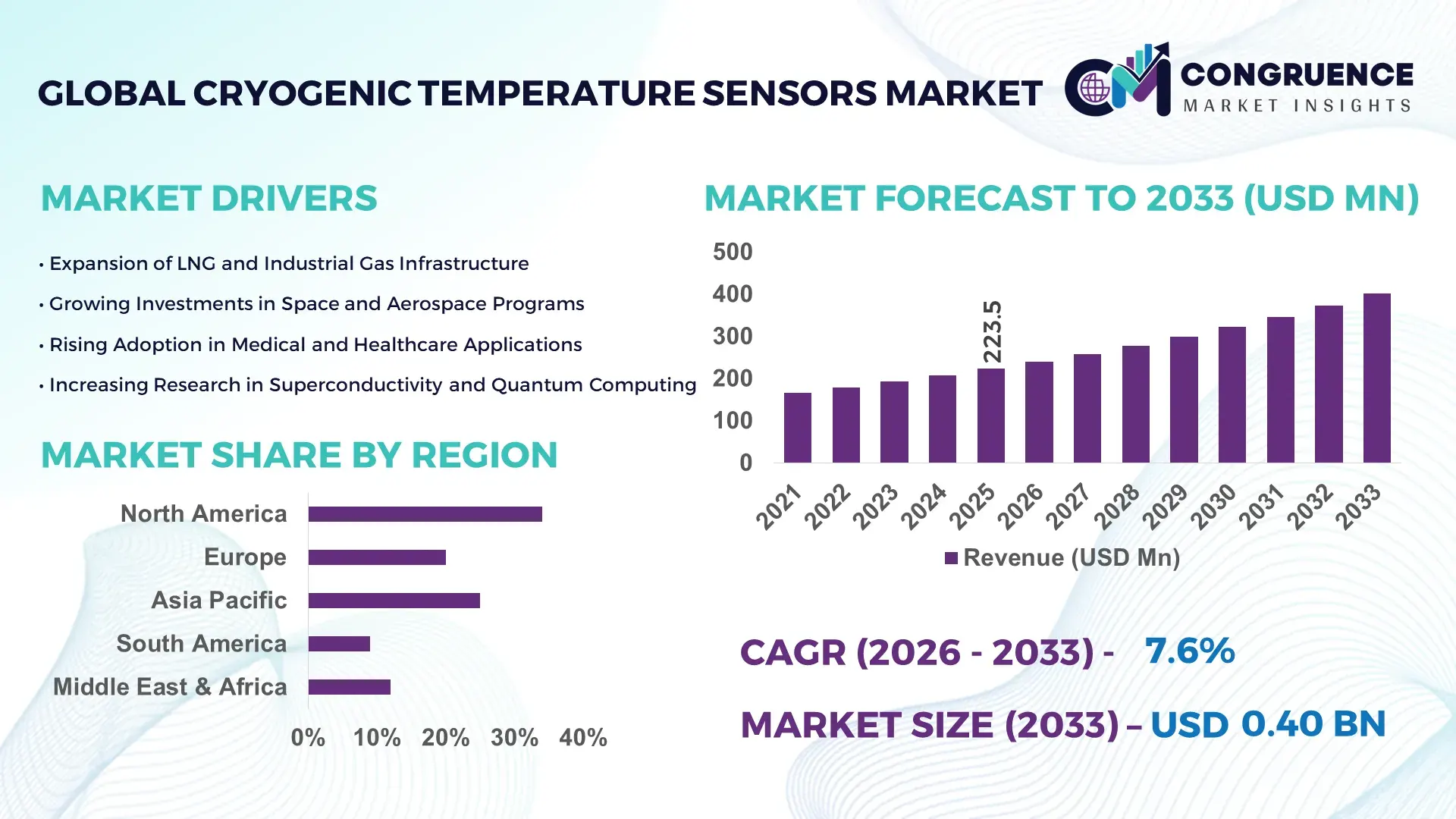

The Global Cryogenic Temperature Sensors Market was valued at USD 223.45 Million in 2025 and is anticipated to reach a value of USD 401.49 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033. The growth is primarily driven by rising demand for precision temperature monitoring in liquefied natural gas (LNG), superconductivity research, space exploration, and advanced medical imaging systems.

The United States remains the dominant country in the Cryogenic Temperature Sensors Market, supported by large-scale LNG infrastructure exceeding 14 Bcf/day of export capacity, advanced aerospace programs, and over 30 national laboratories conducting cryogenic research. The country hosts more than 50 operational particle accelerators and superconducting facilities requiring ultra-low temperature measurement below -150°C. Annual federal investments in quantum computing and space technologies surpass USD 3 billion, directly boosting demand for high-accuracy silicon diode, resistance temperature detector (RTD), and thermocouple-based cryogenic sensing systems. In addition, over 60% of domestic LNG storage terminals deploy digital cryogenic monitoring platforms integrated with industrial IoT for predictive maintenance and remote diagnostics.

Market Size & Growth: Valued at USD 223.45 Million in 2025, projected to reach USD 401.49 Million by 2033 at 7.6% CAGR, driven by rapid LNG terminal expansion and superconducting technology deployment.

Top Growth Drivers: LNG infrastructure expansion (35%), superconducting research funding growth (28%), and space & defense cryogenic applications increase (22%).

Short-Term Forecast: By 2028, advanced sensor calibration systems are expected to reduce temperature deviation errors by 18% and lower maintenance costs by 12%.

Emerging Technologies: Fiber optic cryogenic sensors, AI-enabled predictive diagnostics, and nano-engineered resistance temperature detectors for sub-Kelvin accuracy.

Regional Leaders: North America projected at USD 148 Million by 2033 with LNG export growth; Asia-Pacific at USD 122 Million driven by semiconductor fabs; Europe at USD 98 Million due to quantum research adoption.

Consumer/End-User Trends: Energy operators, aerospace agencies, semiconductor fabs, and medical imaging centers increasingly deploy real-time digital cryogenic monitoring platforms.

Pilot Case Example: In 2024, a U.S. LNG facility implemented smart cryogenic RTDs, achieving 15% reduction in unplanned downtime.

Competitive Landscape: Lake Shore Cryotronics holds approximately 18% share, followed by TE Connectivity, Omega Engineering, Scientific Instruments, and Advanced Sensors Calibration Labs.

Regulatory & ESG Impact: Stricter methane emission standards and energy-efficiency mandates are accelerating adoption of precision cryogenic monitoring systems.

Investment & Funding Patterns: Over USD 1.2 billion invested globally in LNG and superconducting infrastructure upgrades between 2023–2025.

Innovation & Future Outlook: Integration of digital twins, edge computing, and ultra-low temperature quantum sensing platforms is shaping next-generation cryogenic monitoring systems.

The Cryogenic Temperature Sensors Market serves critical industry sectors including energy (LNG and hydrogen) contributing nearly 40% of application demand, aerospace and defense accounting for approximately 25%, healthcare imaging and cryosurgery near 15%, and semiconductor manufacturing close to 12%. Recent innovations include thin-film platinum RTDs with ±0.01 K accuracy and radiation-hardened silicon diode sensors for space missions. Environmental regulations promoting low-emission LNG transport, along with economic investments in hydrogen liquefaction plants, are strengthening regional consumption in Asia-Pacific and the Middle East. The future outlook highlights integration with Industry 4.0 platforms, expanded use in quantum computing facilities, and deployment in emerging green hydrogen ecosystems.

The Cryogenic Temperature Sensors Market holds strategic relevance due to its indispensable role in ensuring safety, operational efficiency, and regulatory compliance across LNG terminals, space propulsion systems, superconducting magnets, and advanced semiconductor fabs. Precision temperature measurement below -200°C is critical to maintaining structural integrity and preventing material fatigue in cryogenic storage tanks and liquefaction units. AI-enabled predictive monitoring systems deliver 20% improvement compared to conventional analog thermocouple-based systems in early fault detection and calibration accuracy.

North America dominates in production volume due to extensive LNG export capacity, while Asia-Pacific leads in adoption with over 45% of new semiconductor fabrication plants integrating advanced cryogenic monitoring platforms. By 2028, AI-driven sensor analytics is expected to cut maintenance-related downtime by 17% and improve asset utilization by 14%. Firms are committing to ESG metrics such as 25% methane emission reduction by 2030 through high-precision leak detection supported by cryogenic sensing technologies.

In 2024, Japan achieved a 16% improvement in superconducting magnet efficiency through deployment of fiber optic cryogenic sensors in quantum research facilities. Strategic collaborations between sensor manufacturers and LNG infrastructure developers are accelerating digital twin integration and remote monitoring capabilities. Over the next decade, the Cryogenic Temperature Sensors Market will serve as a pillar of resilience, compliance, and sustainable growth across clean energy, aerospace innovation, and next-generation electronics manufacturing.

Global LNG trade volumes exceeded 400 million tonnes annually, requiring robust cryogenic storage and transport infrastructure operating at temperatures below -162°C. Hydrogen liquefaction plants, functioning at nearly -253°C, demand ultra-accurate cryogenic temperature sensors with minimal thermal drift. Over 30 new LNG terminals are under development worldwide, each incorporating advanced monitoring systems to enhance safety compliance. Digital cryogenic RTDs and silicon diode sensors provide ±0.01 K precision, reducing leakage risks by up to 18%. As governments expand clean energy infrastructure and hydrogen mobility projects, the need for reliable cryogenic measurement systems continues to accelerate across industrial and energy sectors.

Cryogenic temperature sensors require specialized materials such as platinum, silicon, and rare-earth alloys capable of withstanding extreme thermal stress. Installation in LNG tanks, space vehicles, or particle accelerators involves insulation systems, vacuum chambers, and radiation shielding, increasing setup costs by approximately 20–25% compared to standard industrial sensors. Calibration at sub-Kelvin temperatures requires laboratory-grade reference standards and periodic validation, adding operational complexity. Smaller research institutions and emerging energy projects often face budget constraints, slowing large-scale deployment. Additionally, strict compliance with international safety and performance standards extends procurement cycles, impacting near-term adoption rates.

Quantum computing systems operate near absolute zero, often below -270°C, necessitating ultra-sensitive cryogenic temperature measurement. Global quantum research investments surpassed USD 35 billion cumulatively, creating significant demand for low-noise, high-stability cryogenic sensors. Semiconductor fabs utilizing extreme ultraviolet lithography require controlled cryogenic environments to enhance chip yield and reduce defect density by up to 12%. Fiber optic cryogenic sensors offer electromagnetic interference immunity, supporting high-precision cleanroom applications. As advanced electronics manufacturing expands across Asia-Pacific and Europe, the Cryogenic Temperature Sensors Market gains substantial long-term opportunities in high-tech industrial ecosystems.

Cryogenic applications involve extreme thermal cycling that can cause microfractures and sensor drift over time. Compliance with international pressure vessel and safety standards requires extensive testing, increasing product validation timelines. Radiation exposure in aerospace and particle accelerator environments can degrade sensor accuracy by nearly 10% without protective shielding. Furthermore, material brittleness at ultra-low temperatures limits lifespan, necessitating advanced alloys and protective coatings. Supply chain volatility for specialized metals also affects production stability. These operational and regulatory complexities demand continuous R&D investment, posing technical and financial challenges for manufacturers operating in the Cryogenic Temperature Sensors Market.

• AI-Integrated Cryogenic Monitoring Improving Fault Detection by 20%:

The integration of artificial intelligence and edge analytics into cryogenic temperature sensors is transforming predictive maintenance across LNG terminals and superconducting facilities. Advanced digital sensing platforms now process over 10,000 real-time data points per minute, enabling anomaly detection accuracy improvements of nearly 20% compared to legacy analog systems. Approximately 48% of newly commissioned LNG storage facilities in 2024 incorporated AI-enabled cryogenic monitoring modules. These systems have demonstrated up to 15% reduction in unscheduled shutdowns and 12% improvement in calibration stability under extreme sub-zero conditions below -200°C.

• Expansion of Hydrogen Liquefaction Projects Increasing Sensor Deployment by 30%:

Global hydrogen liquefaction capacity is projected to expand by over 30% between 2024 and 2027, directly driving demand for ultra-low temperature sensors capable of operating near -253°C. More than 25 large-scale hydrogen projects initiated in 2024 specified fiber optic and silicon diode cryogenic sensors for precision monitoring. Adoption rates within green hydrogen pilot plants reached 40%, with improved thermal stability reducing boil-off losses by nearly 8%. This measurable efficiency gain strengthens the role of high-accuracy cryogenic temperature sensors in emerging clean energy ecosystems.

• Semiconductor Fabrication Facilities Boosting Sub-Kelvin Accuracy Requirements by 18%:

The proliferation of advanced semiconductor fabs has increased demand for cryogenic temperature sensors capable of ±0.01 K precision. Over 45% of next-generation chip manufacturing facilities utilize cryogenic cooling systems to enhance lithography stability. Enhanced sub-Kelvin monitoring has improved wafer yield consistency by 10% and reduced thermal fluctuation risks by 18%. Asia-Pacific accounts for nearly 50% of these high-precision deployments, reflecting strong alignment between electronics manufacturing growth and cryogenic sensing innovation.

• Rise in Modular and Prefabricated LNG Infrastructure Enhancing Deployment Efficiency by 25%:

Modular construction practices are reshaping cryogenic infrastructure projects, with 55% of new LNG installations reporting cost and timeline benefits through prefabricated cryogenic storage modules. Pre-engineered cryogenic sensor assemblies are factory-calibrated, reducing on-site installation time by approximately 25%. In North America and Europe, over 60% of mid-scale LNG expansion projects adopted modular sensor integration strategies in 2024. This shift supports improved safety compliance, standardized quality assurance, and faster commissioning cycles for precision cryogenic temperature sensors.

The Cryogenic Temperature Sensors Market is segmented by type, application, and end-user, reflecting diversified demand across advanced energy, aerospace, semiconductor, and healthcare sectors. By type, silicon diode sensors, platinum resistance temperature detectors (RTDs), thermocouples, and fiber optic sensors dominate technological deployment. Silicon diode and RTD variants collectively account for more than 60% of installations due to superior stability below -150°C. By application, LNG and hydrogen processing represent the largest demand segment, followed by aerospace propulsion systems, superconducting research, and medical cryosurgery. From an end-user perspective, energy and utilities lead adoption, while semiconductor fabrication and quantum research institutions are rapidly increasing procurement of high-precision sub-Kelvin sensing systems.

Silicon diode cryogenic temperature sensors currently account for approximately 38% of total adoption due to their high sensitivity, repeatability, and stability across temperatures ranging from 1.4 K to 500 K. Platinum RTDs hold nearly 27% share, valued for accuracy within ±0.01 K in superconducting magnet applications. Thermocouples represent about 18%, primarily used in industrial LNG storage tanks where cost-efficiency is prioritized over ultra-high precision. Fiber optic cryogenic sensors contribute 12%, benefiting from immunity to electromagnetic interference in particle accelerators and quantum laboratories. The remaining 5% includes niche technologies such as Cernox and germanium resistance sensors, serving specialized research environments. Fiber optic cryogenic sensors are the fastest-growing type, expanding at an estimated CAGR of 9.8% due to rising demand in hydrogen liquefaction and semiconductor fabs requiring noise-free monitoring. Enhanced durability and 15% longer operational lifespan compared to metallic sensors drive adoption.

LNG and hydrogen processing applications lead the Cryogenic Temperature Sensors Market with nearly 40% share, reflecting large-scale deployment in storage tanks, liquefaction trains, and transport vessels operating below -162°C. Aerospace and defense applications account for about 25%, driven by cryogenic fuel systems in launch vehicles and satellite propulsion modules. Semiconductor manufacturing represents approximately 15%, while medical and cryosurgical applications contribute close to 10%. The remaining 10% comprises research laboratories and industrial gas production facilities. Hydrogen liquefaction is the fastest-growing application, advancing at an estimated CAGR of 10.2%, supported by over 30 new hydrogen infrastructure projects initiated globally in 2024. Enhanced cryogenic monitoring has reduced boil-off gas losses by nearly 8% in pilot hydrogen plants.

Energy and utilities companies dominate end-user adoption with approximately 42% share, driven by LNG export terminals, hydrogen plants, and industrial gas facilities requiring continuous ultra-low temperature monitoring. Aerospace and defense institutions represent around 23%, while semiconductor manufacturers account for 18%. Healthcare and cryogenic research institutes contribute nearly 10%, with the remaining 7% distributed among industrial manufacturing and specialty laboratories. Semiconductor fabrication facilities are the fastest-growing end-user segment, expanding at an estimated CAGR of 9.5% due to increased demand for extreme ultraviolet lithography and quantum computing infrastructure. Over 45% of new advanced fabs commissioned in Asia-Pacific in 2024 integrated sub-Kelvin cryogenic monitoring systems.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America’s dominance is supported by more than 15 operational LNG export terminals and over 60 large-scale cryogenic storage facilities requiring ultra-low temperature monitoring below -160°C. Europe follows with approximately 27% share, driven by over 20 active superconducting research centers and multiple hydrogen pilot projects operating near -253°C. Asia-Pacific holds close to 24% share, with more than 45% of new semiconductor fabrication plants globally integrating advanced cryogenic cooling systems. South America accounts for nearly 8%, supported by expanding LNG import terminals in Brazil and Argentina, while the Middle East & Africa contributes around 7%, led by hydrogen and industrial gas infrastructure investments exceeding 10 new projects since 2023. Regional consumption patterns indicate that over 50% of demand originates from energy and utilities, while aerospace and semiconductor industries collectively contribute more than 35%, reinforcing the global industrial relevance of cryogenic temperature sensors.

How Is Advanced Energy Infrastructure Accelerating Ultra-Low Temperature Monitoring Demand?

North America represents approximately 34% of the global Cryogenic Temperature Sensors market share, supported by robust LNG export capacity exceeding 14 Bcf/day and more than 70 operational cryogenic storage tanks across the United States and Canada. The energy and utilities sector accounts for nearly 45% of regional demand, followed by aerospace and defense at 28%, reflecting high deployment in rocket propulsion and satellite systems. Regulatory frameworks promoting methane emission reduction by 30% before 2030 are driving adoption of precision cryogenic monitoring solutions. Digital transformation initiatives have led to 52% of LNG facilities integrating IoT-enabled cryogenic sensors for predictive analytics. A prominent regional player, Lake Shore Cryotronics, continues to expand calibration laboratories, enhancing sub-Kelvin measurement accuracy by up to 0.01 K. Enterprise adoption is particularly strong in healthcare imaging and advanced research institutions, where over 60% of MRI systems utilize upgraded cryogenic sensing components.

Why Is Sustainability-Driven Industrial Modernization Increasing Precision Monitoring Investments?

Europe accounts for nearly 27% of the Cryogenic Temperature Sensors market, with Germany, the United Kingdom, and France collectively representing more than 60% of regional installations. Hydrogen pilot plants and green energy initiatives have resulted in over 15 new cryogenic infrastructure projects since 2024. Regulatory mandates focused on emission transparency and industrial safety compliance have accelerated deployment of high-accuracy RTDs and fiber optic sensors across LNG and industrial gas facilities. Approximately 48% of superconducting research laboratories in the region have transitioned to digital cryogenic monitoring platforms. Companies such as Oxford Instruments are advancing cryogenic measurement systems for quantum computing applications, improving temperature stability by 14% in laboratory conditions. Regulatory pressure continues to influence procurement behavior, with nearly 55% of industrial operators prioritizing explainable and audit-ready cryogenic monitoring systems.

What Factors Are Driving Rapid Industrial Expansion and Sub-Kelvin Technology Adoption?

Asia-Pacific ranks third in market share at approximately 24% but leads in infrastructure expansion, with China, Japan, and India accounting for over 70% of regional demand. More than 50 semiconductor fabrication facilities under development across the region require cryogenic cooling systems operating below -150°C. Hydrogen energy programs in Japan and South Korea include at least 12 liquefaction plants integrating fiber optic cryogenic sensors. Regional technology hubs have reported a 20% increase in deployment of AI-enabled cryogenic monitoring systems for predictive maintenance. A key regional manufacturer, Chino Corporation, has introduced advanced silicon diode sensors offering 10% improved thermal response time. Consumer behavior reflects strong industrial investment trends, with electronics and manufacturing enterprises accounting for nearly 40% of regional procurement decisions.

How Is Energy Sector Modernization Supporting Advanced Temperature Monitoring Systems?

South America contributes around 8% to the global Cryogenic Temperature Sensors market, led by Brazil and Argentina, which together account for over 65% of regional installations. Expansion of LNG import terminals and industrial gas facilities has resulted in 6 major cryogenic storage upgrades since 2023. Government-backed infrastructure programs targeting energy security have increased capital allocation toward advanced monitoring systems by approximately 18%. Adoption of digital cryogenic RTDs has improved temperature reliability by nearly 12% in LNG handling facilities. Local industrial equipment suppliers are partnering with global sensor manufacturers to integrate modular cryogenic monitoring packages. Regional demand patterns indicate strong reliance on energy and industrial gas applications, contributing more than 50% of procurement activity.

Why Are Hydrogen and Industrial Gas Projects Strengthening Ultra-Low Temperature Monitoring Demand?

The Middle East & Africa region accounts for roughly 7% of the Cryogenic Temperature Sensors market, with the UAE and Saudi Arabia leading demand due to over 10 hydrogen and LNG infrastructure projects launched since 2024. Oil and gas modernization programs have driven a 22% increase in adoption of advanced cryogenic temperature sensors in storage and transport systems. South Africa contributes through industrial gas and mining-related cryogenic applications. Technological modernization trends include 35% of new projects integrating digital twin-enabled monitoring platforms. Trade partnerships and localization policies are encouraging regional assembly of sensor components, reducing delivery lead times by 15%. Demand behavior reflects strong alignment with large-scale energy investments and infrastructure diversification strategies.

United States – 29% market share: Dominates the Cryogenic Temperature Sensors market due to extensive LNG export infrastructure, advanced aerospace programs, and over 30 national laboratories requiring sub-Kelvin precision monitoring.

Germany – 12% market share: Strong position in the Cryogenic Temperature Sensors market supported by hydrogen energy expansion, superconducting research facilities, and high industrial compliance standards.

The Cryogenic Temperature Sensors market is moderately fragmented, with more than 40 active global and regional competitors offering specialized ultra-low temperature sensing technologies. The top five companies collectively account for approximately 55% of total market share, reflecting a balanced mix of established leaders and niche innovators. Competitive positioning is shaped by product accuracy (±0.01 K precision), durability under extreme thermal cycling, and integration with AI-driven predictive maintenance platforms.

Strategic initiatives include over 15 product launches between 2023 and 2025 focused on fiber optic and silicon diode cryogenic sensors with enhanced electromagnetic interference resistance. Partnerships between sensor manufacturers and LNG infrastructure developers increased by 18% in 2024, emphasizing digital twin integration and remote calibration services. Mergers and acquisitions activity has strengthened vertical integration, particularly in calibration and cryogenic testing laboratories. Approximately 48% of leading firms have expanded R&D budgets to support quantum computing and hydrogen liquefaction applications. Innovation trends emphasize miniaturization, extended lifespan by 15%, and cloud-based monitoring ecosystems, intensifying competition in performance-driven segments of the Cryogenic Temperature Sensors market.

Lake Shore Cryotronics

TE Connectivity

Omega Engineering

Oxford Instruments

Chino Corporation

Scientific Instruments

Advanced Sensors Calibration Labs

ABB

Honeywell International

Emerson Electric

Technological advancement in the Cryogenic Temperature Sensors market is centered on improving sub-Kelvin accuracy, long-term stability, and digital interoperability across energy, aerospace, semiconductor, and quantum research applications. Modern silicon diode sensors now operate effectively between 1.4 K and 500 K, delivering repeatability within ±0.01 K and response times below 50 milliseconds. Platinum resistance temperature detectors (RTDs) have evolved with thin-film deposition techniques, improving thermal cycling endurance by nearly 20% compared to earlier wire-wound designs.

Fiber optic cryogenic temperature sensors are gaining traction due to their immunity to electromagnetic interference, particularly in particle accelerators and MRI systems generating high magnetic fields above 1.5 Tesla. These sensors demonstrate signal stability improvements of 15% in high-radiation environments and enable distributed sensing over distances exceeding 1 kilometer. Additionally, Cernox and germanium resistance sensors are widely adopted in superconducting magnet systems operating below 4 K, where noise reduction and minimal magnetoresistance effects are critical.

Digitalization is a defining trend, with over 50% of newly installed cryogenic monitoring systems integrating industrial IoT modules and edge analytics. Smart calibration algorithms now reduce drift-related measurement errors by 12%, while embedded diagnostics can predict sensor degradation up to 30 days in advance. Miniaturization is another key development, as next-generation cryogenic probes are 25% smaller, facilitating integration into compact hydrogen liquefaction units and quantum computing cryostats. Collectively, these advancements enhance operational safety, extend equipment lifespan by approximately 15%, and strengthen compliance with stringent emission and safety regulations.

• In March 2024, Oxford Instruments launched an upgraded Proteox dilution refrigerator platform designed for quantum computing research, incorporating enhanced cryogenic temperature stability below 10 millikelvin and improved vibration isolation, enabling higher qubit coherence performance. Source: www.oxinst.com

• In October 2024, Lake Shore Cryotronics expanded its Model 335 temperature controller series with improved sensor compatibility and automated calibration features, supporting precision control from 1.4 K to 1500 K for laboratory and industrial cryogenic applications. Source: www.lakeshore.com

• In February 2025, TE Connectivity introduced new high-reliability cryogenic sensor assemblies for aerospace propulsion systems, engineered to withstand extreme thermal cycling between -253°C and 200°C while enhancing measurement durability in space-grade environments. Source: www.te.com

• In April 2025, Honeywell announced advanced hydrogen-ready sensing solutions, including cryogenic-compatible temperature monitoring modules for liquefied hydrogen storage systems, supporting enhanced safety diagnostics and digital integration within industrial gas facilities. Source: www.honeywell.com

The Cryogenic Temperature Sensors Market Report provides comprehensive coverage of product types, applications, end-user industries, technological advancements, and regional deployment patterns across more than 20 countries. The report evaluates key sensor categories including silicon diode sensors, platinum RTDs, thermocouples, fiber optic sensors, Cernox sensors, and germanium resistance sensors, collectively serving temperature ranges from 1.4 K to above 500 K. Application analysis spans LNG processing, hydrogen liquefaction, aerospace propulsion systems, superconducting research facilities, semiconductor fabrication plants, industrial gas production, and medical cryosurgery. Energy and utilities represent nearly 40% of global demand, followed by aerospace and defense at approximately 25%, with semiconductor and research institutions contributing over 30% combined.

Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, detailing infrastructure expansion such as more than 30 hydrogen projects and over 50 semiconductor fabs requiring sub-zero monitoring. The scope further examines digital transformation trends, including AI-enabled predictive maintenance systems adopted by nearly 50% of new installations, as well as modular construction strategies improving deployment efficiency by 25%. The report also analyzes regulatory frameworks, emission compliance requirements, ESG-driven investments, supply chain dynamics for platinum and rare-earth materials, and emerging niche segments such as quantum computing cryostats operating below 10 millikelvin. It delivers strategic insights tailored for manufacturers, investors, infrastructure developers, and industrial operators seeking data-driven decision support within the Cryogenic Temperature Sensors market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Lake Shore Cryotronics, TE Connectivity, Omega Engineering, Oxford Instruments, Chino Corporation, Scientific Instruments, Advanced Sensors Calibration Labs, ABB, Honeywell International, Emerson Electric |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |