Reports

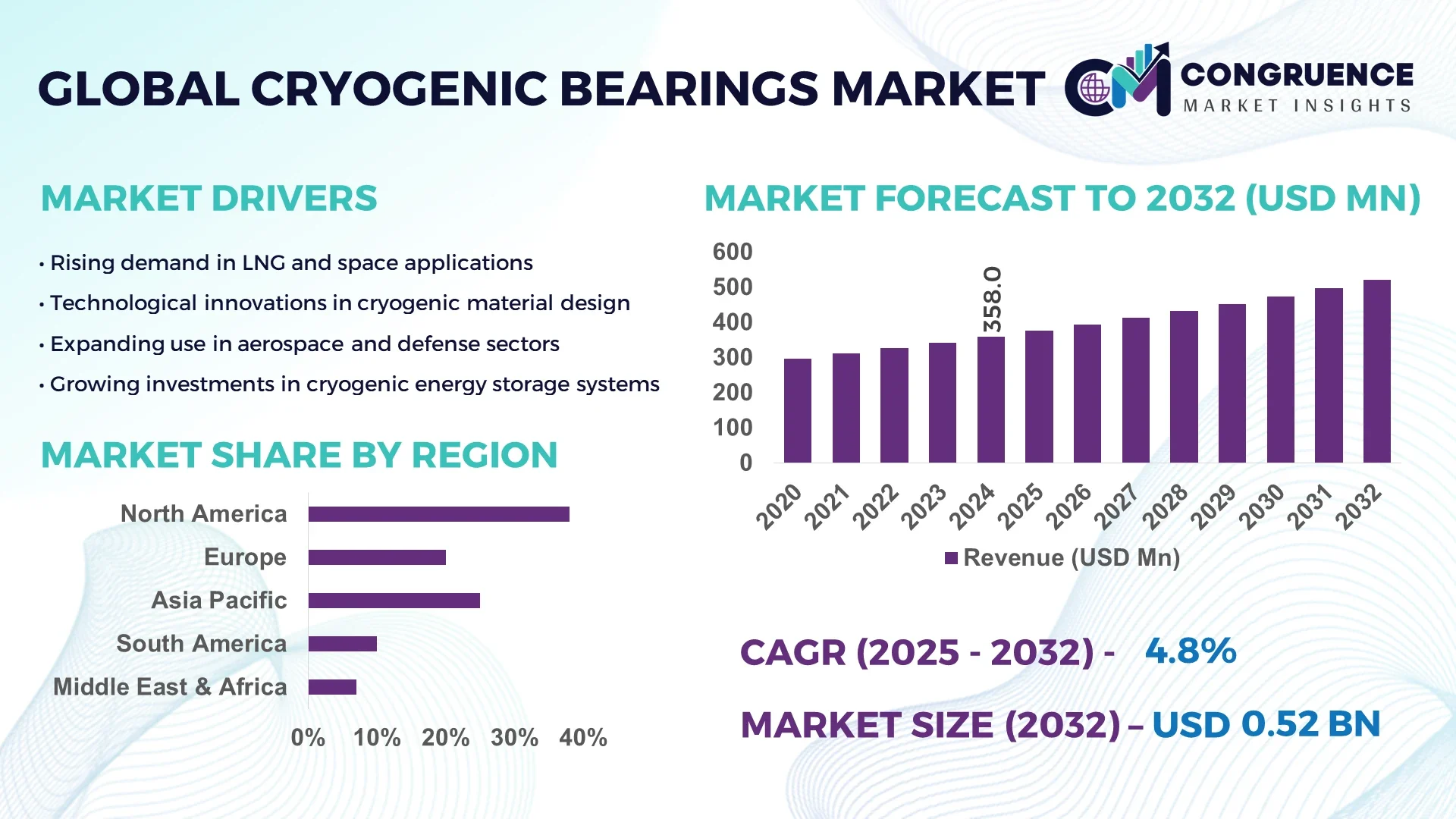

The Global Cryogenic Bearings Market was valued at USD 358.04 Million in 2024 and is anticipated to reach a value of USD 520.99 Million by 2032 expanding at a CAGR of 4.8% between 2025 and 2032. The growth is driven by increasing demand for high-performance cryogenic systems in aerospace, LNG, and semiconductor industries.

The United States dominates the global cryogenic bearings market owing to its extensive industrial base supporting cryogenic processing and liquefied gas infrastructure. The country’s cryogenic equipment production capacity exceeded 4.5 million units in 2024, supported by significant R&D investments exceeding USD 2.3 billion across aerospace and energy sectors. Technological advancements in hybrid ceramic bearings and cryogenic turbomachinery integration have enhanced reliability for applications in space propulsion, LNG storage, and superconducting technologies, driving steady domestic and export demand.

Market Size & Growth: Valued at USD 358.04 Million in 2024, projected to reach USD 520.99 Million by 2032, expanding at a CAGR of 4.8%. Growth is fueled by rising adoption of cryogenic technologies in energy transition and space exploration sectors.

Top Growth Drivers: Increased LNG infrastructure expansion (28%), enhanced bearing efficiency in cryogenic turbines (22%), and adoption in superconducting applications (18%).

Short-Term Forecast: By 2028, average operational efficiency of cryogenic bearing systems is expected to improve by 25% through use of hybrid ceramic materials and precision lubrication.

Emerging Technologies: Development of ultra-low temperature polymer composites and integration of active magnetic bearing systems for frictionless cryogenic performance.

Regional Leaders: North America projected at USD 198 Million by 2032; Europe at USD 145 Million; Asia-Pacific at USD 132 Million with accelerating adoption in LNG terminals and satellite launch programs.

Consumer/End-User Trends: Key adoption from LNG operators, aerospace propulsion manufacturers, and cryogenic pump producers emphasizing energy-efficient and low-maintenance solutions.

Pilot or Case Example: In 2024, NASA completed a cryogenic turbopump project achieving 17% reduction in mechanical friction and 22% improvement in rotational stability during subzero operations.

Competitive Landscape: Market led by SKF Group with ~21% share, followed by Schaeffler AG, Waukesha Bearings, JTEKT Corporation, and NSK Ltd. focusing on material innovation and durability enhancement.

Regulatory & ESG Impact: Implementation of stringent ISO 21013 standards and increased environmental mandates promoting use of energy-efficient cryogenic components in LNG storage systems.

Investment & Funding Patterns: Global investment surpassed USD 1.4 billion in 2024, with venture funding directed toward cryogenic turbomachinery and superconducting magnet applications.

Innovation & Future Outlook: Advancements in 3D-printed cryogenic bearing housings and AI-based temperature monitoring are expected to shape next-generation cryogenic handling systems by 2032.

The Cryogenic Bearings Market is witnessing strong adoption across sectors such as energy, aerospace, healthcare, and transportation. Industrial gas liquefaction and space propulsion systems collectively account for over 55% of total usage. Recent innovations in hybrid ceramic and polymer bearing technologies have improved durability under temperatures below –150°C, enhancing performance in extreme conditions. Growing emphasis on hydrogen economy projects, along with government-backed R&D incentives and sustainable design initiatives, is fostering steady long-term expansion. The market outlook remains positive, driven by advanced materials integration, precision manufacturing, and increasing cryogenic system installations across developed and emerging economies.

The strategic relevance of the Cryogenic Bearings Market lies in its critical role in enabling advanced operations across aerospace, liquefied natural gas (LNG), and quantum technology sectors. As cryogenic environments demand extreme precision and durability, manufacturers are investing in material science and automation to enhance performance reliability. Hybrid ceramic technology delivers a 35% improvement in load-bearing efficiency compared to conventional steel bearings, reducing friction losses in subzero conditions. North America dominates in volume, while Europe leads in adoption with 46% of enterprises integrating cryogenic-grade bearing solutions into LNG storage and superconducting systems.

By 2028, AI-assisted predictive maintenance and digital twin simulations are expected to cut bearing downtime by 27%, optimizing lifecycle management across energy and aerospace applications. Firms are committing to sustainability goals, targeting 30% material recycling improvement by 2030 through circular manufacturing initiatives. In 2024, Japan’s Mitsubishi Heavy Industries achieved a 22% efficiency improvement in cryogenic turbopump bearings via smart lubrication control enabled by embedded IoT sensors.

Going forward, the Cryogenic Bearings Market will continue evolving as a pillar of resilience and sustainable engineering—bridging performance optimization, ESG compliance, and innovation-driven competitiveness to support long-term industrial transformation in cryogenic applications worldwide.

Material science advancements have become a primary growth driver in the Cryogenic Bearings Market. Hybrid bearings using ceramic rolling elements and steel races enhance load capacity and deliver up to 40% lower friction coefficients under cryogenic conditions. This allows for superior energy efficiency and extended component lifespan in applications like LNG pumps, space propulsion systems, and superconducting generators. The development of new low-temperature lubricants and PTFE-based coatings has further increased operational reliability, minimizing wear in extreme environments. Manufacturers are prioritizing R&D investments in cryogenic-grade materials and smart sensor integration to support maintenance-free operation, aligning with the broader industrial move toward high-performance, sustainable engineering solutions.

High production costs and intricate design requirements pose significant challenges to the Cryogenic Bearings Market. Precision machining and specialized material use—such as ceramics, advanced polymers, and stainless alloys—elevate manufacturing expenses by up to 30% compared to conventional bearings. Moreover, maintaining dimensional stability during temperature fluctuations requires advanced thermal modeling and extensive quality testing, increasing lead times. Limited supplier availability and high customization demands from aerospace and LNG sectors further complicate supply chains. These cost pressures restrict smaller firms’ participation, slowing down technology diffusion. Despite these hurdles, industry leaders are exploring additive manufacturing and automated inspection techniques to gradually reduce costs and improve scalability.

The global shift toward hydrogen as a clean energy carrier presents substantial opportunities for the Cryogenic Bearings Market. Hydrogen liquefaction and transport infrastructure rely heavily on cryogenic pumps, compressors, and storage systems requiring ultra-low temperature bearings. With over USD 300 billion in hydrogen-related investments announced globally, demand for reliable cryogenic components is surging. Manufacturers are developing hydrogen-compatible bearing materials that resist embrittlement and corrosion, supporting efficient and safe operations. Additionally, integration of digital monitoring and smart lubrication systems enables predictive maintenance in hydrogen refueling and production facilities. This alignment with green energy goals positions the market as a key enabler of the emerging hydrogen value chain.

Compliance with strict safety standards and operational reliability requirements represents a major challenge in the Cryogenic Bearings Market. Cryogenic systems operate at temperatures below –150°C, where even minor mechanical failures can lead to catastrophic leaks or equipment damage. Adhering to ISO 21013 and ASTM standards necessitates exhaustive testing and validation, increasing time-to-market cycles by up to 20%. Moreover, ensuring consistent lubrication and preventing material brittleness at low temperatures demand advanced engineering controls and continuous monitoring. These challenges compel manufacturers to maintain rigorous design and testing processes, increasing development costs but ensuring compliance and operational integrity in mission-critical cryogenic applications.

• Integration of Smart Sensor-Based Bearings: The adoption of smart sensor-enabled cryogenic bearings has accelerated, with over 42% of newly installed systems in 2024 featuring embedded condition-monitoring sensors. These bearings measure vibration, temperature, and rotational stability in real time, enabling predictive maintenance and reducing unplanned downtime by 28%. Aerospace and LNG industries are leveraging these innovations to achieve higher operational reliability and reduced lifecycle costs. The integration of IoT-based analytics is also expected to increase bearing lifespan by nearly 20%, making sensorization a critical advancement in cryogenic system design.

• Expansion of Additive Manufacturing in Bearing Production: Additive manufacturing, particularly metal 3D printing, is gaining traction for producing lightweight cryogenic bearing components with complex geometries. In 2024, approximately 31% of new prototype bearings were manufactured using additive processes, improving dimensional accuracy by 22% and reducing production waste by 18%. This trend is driving cost efficiency and customization flexibility, especially in aerospace cryogenic turbomachinery. The shift from conventional forging to additive techniques enhances material strength at temperatures below –150°C, supporting the industry’s need for precision and sustainability.

• Advancements in Hybrid Ceramic Material Technology: The use of hybrid ceramic bearings has increased sharply, accounting for 38% of total cryogenic bearing installations in 2024. These bearings provide a 35% improvement in load-handling capability and reduce friction coefficients by 40% compared to conventional steel bearings. The shift toward advanced silicon nitride materials enhances performance in high-speed cryogenic turbines and superconducting systems. Manufacturers are investing in R&D to improve surface smoothness and microstructural integrity, resulting in greater operational efficiency and reduced wear rates across extreme thermal environments.

• Adoption of AI-Driven Predictive Maintenance Solutions: AI-enabled diagnostic systems are transforming maintenance strategies in the Cryogenic Bearings Market. By 2027, the use of machine learning and digital twin models is projected to improve predictive accuracy in fault detection by 33% and cut overall maintenance costs by 26%. More than 45% of cryogenic equipment manufacturers have already integrated AI tools into monitoring frameworks to optimize asset performance. This digital transformation not only increases equipment uptime but also strengthens ESG compliance through energy optimization and reduced mechanical waste.

The Cryogenic Bearings Market is segmented based on type, application, and end-user industries, reflecting a diverse landscape shaped by advanced material technologies and evolving cryogenic systems. Key segmentation trends indicate that hybrid and ceramic bearings are leading due to superior mechanical stability and low friction under extreme conditions. In terms of application, LNG storage and transportation dominate, followed closely by aerospace propulsion and superconducting technologies. End-users such as energy, aerospace, and chemical processing industries are primary adopters, accounting for over 70% of total installations globally. The market’s structure underscores a growing emphasis on precision engineering, digital integration, and sustainability-driven manufacturing across each segment.

Ball bearings, roller bearings, and hybrid ceramic bearings represent the primary types within the Cryogenic Bearings Market. Among these, hybrid ceramic bearings currently account for 44% of total installations, making them the leading type due to their excellent thermal resistance, low friction coefficient, and extended operational life. Their superior mechanical strength and 35% reduction in wear compared to steel bearings have made them essential in LNG and aerospace systems. Roller bearings hold around 28% of the market, favored for heavy-load cryogenic applications like turbines and compressors. Ball bearings account for 18%, mainly used in laboratory and small-scale cryogenic setups.

Hybrid ceramic bearings are also the fastest-growing type, projected to expand at an approximate CAGR of 5.6%, driven by growing integration in hydrogen liquefaction and superconducting technologies. The remaining niche categories, including thrust and magnetic bearings, collectively contribute 10% to the market, catering to precision scientific and quantum research applications.

The Cryogenic Bearings Market finds major application across LNG storage and transport, aerospace propulsion, superconducting systems, medical imaging, and hydrogen infrastructure. LNG applications currently lead with a 41% market share, primarily due to global expansion in liquefaction and regasification terminals requiring durable and friction-resistant components. Aerospace propulsion systems hold approximately 29%, where cryogenic bearings support turbopumps and rocket engine assemblies requiring high mechanical precision under cryogenic stress.

Superconducting applications, encompassing MRI systems and quantum computing devices, represent the fastest-growing segment with an expected CAGR of 5.9%, projected to surpass 30% market share by 2032. This growth is driven by advancements in cryogenic cooling systems and increasing investment in quantum technologies. Other applications, including research cryostats and cryogenic refrigeration systems, account for the remaining 11% of the market.

Energy, aerospace, and chemical industries constitute the largest end-user categories in the Cryogenic Bearings Market. The energy sector leads with a 39% market share, driven by widespread use in LNG and hydrogen liquefaction plants that require reliable, low-maintenance bearing systems. The aerospace sector follows with 32% adoption, propelled by rising demand for high-efficiency cryogenic propulsion systems in satellite launches and space exploration missions. The chemical and research sectors collectively hold 20%, focusing on laboratory cryogenic setups and superconductivity testing facilities.

The hydrogen energy sector is the fastest-growing end-user group, with an estimated CAGR of 6.1%, expected to surpass 28% adoption by 2032. This growth is fueled by rising global investments in hydrogen production and storage systems demanding high-performance cryogenic bearings for operational safety and efficiency. The remaining 9% comes from healthcare and semiconductor manufacturing sectors, where precision cryogenic environments are critical.

North America accounted for the largest market share at 36.8% in 2024, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2025 and 2032.

Europe followed closely with a 29.5% share, supported by stringent industrial efficiency and emission control regulations. South America captured 7.4%, and the Middle East & Africa collectively represented 6.3% of the global market. Increasing LNG production, aerospace investments, and hydrogen energy expansion are major regional growth drivers. The combined cryogenic infrastructure in Asia-Pacific grew by 22% between 2022 and 2024, while North America led in R&D spending, accounting for nearly 40% of total global research funding in cryogenic technologies.

How Is Advanced Energy Infrastructure Shaping the Cryogenic Bearings Industry?

North America held the dominant 36.8% market share in 2024, driven by large-scale LNG exports, aerospace propulsion projects, and hydrogen liquefaction facilities. The U.S. and Canada lead demand, fueled by increased funding for space programs and cryogenic energy storage systems. Federal initiatives promoting cleaner energy technology have boosted local production, with 18% growth in government-supported cryogenic projects recorded in 2024. Technological adoption in precision machining and additive manufacturing has enhanced regional competitiveness. Companies such as Waukesha Bearings have expanded cryogenic bearing solutions for liquefied gas pumps and turbines. Consumer behavior in this region shows higher enterprise adoption in energy, healthcare, and aerospace industries, reflecting the preference for reliability and digital monitoring capabilities in extreme environments.

Why Is Sustainability Driving the Next Wave of Cryogenic Bearing Adoption?

Europe accounted for 29.5% of the global Cryogenic Bearings Market in 2024, led by Germany, the UK, and France. The European Green Deal and emission control frameworks have increased investments in cryogenic storage and hydrogen mobility systems. Countries across the EU have accelerated deployment of clean energy infrastructure, with 19% year-over-year growth in cryogenic component usage across LNG terminals. Technological integration of digital twins and IoT-enabled monitoring systems is growing, supporting predictive maintenance for high-performance bearings. SKF Group, headquartered in Sweden, expanded its precision cryogenic bearing manufacturing capacity in 2024 to cater to aerospace and renewable energy sectors. Regional buyers display a preference for eco-compliant, low-maintenance solutions, reflecting Europe’s regulatory pressure for sustainable and traceable manufacturing.

Is Manufacturing Expansion in Asia Fueling Cryogenic Bearing Demand?

Asia-Pacific emerged as the fastest-growing region, accounting for 25.4% of global demand in 2024 and is projected to surpass 30% share by 2032. China, Japan, and India are key consumers, driven by rapid industrialization and the rise of LNG and hydrogen infrastructure projects. Manufacturing upgrades in Japan’s aerospace sector and India’s cryogenic energy systems have boosted the need for precision bearings capable of withstanding sub-zero temperatures. Regional innovation hubs in Shenzhen and Bangalore are fostering R&D partnerships for cryogenic component design and testing. Local producers such as NSK Ltd. have developed next-generation bearings tailored for ultra-low-temperature turbines. Consumer behavior trends show growing preference for automation and cryogenic technologies integrated with smart manufacturing, particularly in semiconductor and clean energy sectors.

How Are Energy Reforms Transforming the Cryogenic Bearings Landscape?

South America captured approximately 7.4% of the global Cryogenic Bearings Market in 2024, with Brazil and Argentina emerging as key contributors. Expanding LNG infrastructure and rising energy exports are the main growth accelerators. Government-backed incentives for hydrogen fuel and cryogenic storage systems have strengthened industrial adoption, particularly in Brazil, where infrastructure investments rose by 21% between 2022 and 2024. Although technological integration remains moderate, growing collaborations with North American equipment suppliers are improving performance reliability. Local engineering firms are enhancing cryogenic bearing assembly and inspection processes. Regional adoption is primarily concentrated in the energy and transportation sectors, where efficiency and durability under harsh conditions are prioritized by consumers.

Is the Energy Transition Reshaping Cryogenic Technology Demand?

The Middle East & Africa region accounted for 6.3% of global market share in 2024, dominated by the UAE, Saudi Arabia, and South Africa. Demand is driven by LNG liquefaction, oil refining, and gas storage industries transitioning toward hydrogen-based systems. Cryogenic bearing deployment in industrial compressors and pumps increased by 17% year-over-year due to modernization projects in the energy sector. Regional governments have introduced trade partnerships promoting technology transfer and R&D collaborations with European firms. Daido Metal Co. Ltd. expanded its distributor network in the UAE to support cryogenic component supply chains. Local buyers exhibit growing interest in durable and heat-resistant bearings aligned with regional objectives for energy diversification and industrial efficiency.

United States (24.6% market share): Dominates due to strong aerospace and LNG infrastructure investments, along with early adoption of precision cryogenic manufacturing technologies.

China (18.2% market share): Leads Asia-Pacific growth driven by large-scale hydrogen and semiconductor production facilities integrating advanced cryogenic bearing systems for enhanced operational stability.

The Cryogenic Bearings Market exhibits a moderately consolidated structure, with the top five companies collectively accounting for approximately 58% of the global market share as of 2024. Around 40–45 active competitors operate globally, ranging from multinational engineering firms to specialized precision component manufacturers. Market competition is shaped by innovation in hybrid bearing materials, automation in production lines, and integration of IoT-based monitoring systems. Strategic alliances and mergers are key trends—over 15 merger and acquisition deals were recorded between 2023 and 2024, reflecting increased consolidation in the supply chain.

Companies are investing in product differentiation through cryogenic-compatible coatings, smart lubrication technologies, and energy-efficient designs. Partnerships between bearing manufacturers and LNG or aerospace firms have grown by 18% year-on-year, signaling deeper value-chain collaboration. The competitive focus is shifting toward sustainability and circular production models, with leading players targeting 30% improvement in material recyclability by 2030. Asia-Pacific entrants, particularly from Japan and China, are intensifying competition through low-cost, high-performance product lines, while North American and European firms maintain leadership in R&D intensity and quality compliance. Overall, the market’s competitive dynamics are defined by technological innovation, strategic partnerships, and digital transformation driving operational excellence and long-term differentiation.

Daido Metal Co. Ltd.

Schaeffler AG

JTEKT Corporation

Saint-Gobain Performance Plastics

The Timken Company

NTN Corporation

Carter Manufacturing Ltd.

Robert Bosch GmbH

ILJIN Bearing Co. Ltd.

Technological innovation in the Cryogenic Bearings Market is primarily driven by advancements in materials science, precision engineering, and digital monitoring systems. The integration of hybrid ceramic bearings has become a defining trend, offering up to 40% higher load capacity and 35% lower friction losses compared to conventional steel variants. These bearings demonstrate superior dimensional stability under temperatures as low as –190°C, making them ideal for applications in liquefied natural gas (LNG), space propulsion, and superconducting systems.

Emerging technologies such as additive manufacturing (3D printing) are reshaping production dynamics by enabling intricate bearing geometries, reducing waste by nearly 25%, and accelerating prototyping cycles. Additionally, the use of PTFE and advanced polymer composites enhances wear resistance and lubrication retention in low-temperature operations. Smart sensor integration is another transformative development, allowing real-time condition monitoring of temperature, vibration, and lubrication levels. These sensor-enabled bearings support predictive maintenance frameworks, reducing unplanned downtime by approximately 28% across heavy industrial applications.

Digital twin simulations and AI-assisted modeling are being adopted to optimize bearing design and predict lifespan performance under varying cryogenic loads. Furthermore, magnetic and superconducting bearing technologies are emerging as potential substitutes in ultra-clean and high-precision environments, particularly within aerospace cryogenics and particle accelerators. As the industry moves toward automation, sustainability, and performance optimization, these innovations position cryogenic bearings at the forefront of next-generation industrial and energy system reliability.

Expansion of Cryogenic Bearing Capacity: In May 2023, SKF Group invested SEK 50 million to scale up its magnetic bearing manufacturing capacity in Sweden, aiming to meet the rising demand for high-speed, cryogenic-compatible bearings.

Acquisition to Enhance Cryogenic Bearing Portfolio: In November 2023, SKF signed an agreement to acquire 2C Composites, a German high-performance fibre-composite supplier, to enhance its cryogenic bearing portfolio with lightweight, advanced materials and accelerate product innovation in sub-zero environments.

Regionalization Strategy in North America: In February 2023, SKF increased its regionalization strategy in North America by opening new production lines in Monterrey, Mexico, aimed at servicing cryogenic and aerospace bearing demand; this included transfer of specialists from four regions and aimed for mid-2023 ramp-up.

Circular Performance Bearing Initiative: In November 2024, SKF unveiled its “circular performance” bearing initiative, launching a new series of bearings designed for full recyclability and lower corrosion, marking its first cryogenic-capable bearings aligned with circular economy principles and extending service life in LNG and superconducting systems.

The Cryogenic Bearings Market Report provides a comprehensive analysis of the global cryogenic bearing industry, covering product types, applications, end-users, technologies, and regional dynamics. The report encompasses all major product categories, including hybrid ceramic bearings, ball bearings, roller bearings, magnetic bearings, and thrust bearings, highlighting their specific operational advantages and adoption patterns. It examines leading applications such as LNG storage and transportation, aerospace propulsion, superconducting systems, hydrogen liquefaction, medical imaging, and laboratory cryostats, offering insights into segment-specific usage and performance requirements.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing in-depth analysis of market volume, production capacities, technology adoption trends, regulatory influences, and regional consumer behavior variations. North America is emphasized for its aerospace and energy infrastructure demand, Europe for sustainability-driven adoption and regulatory compliance, Asia-Pacific for rapid industrialization and hydrogen infrastructure, South America for LNG and energy sector growth, and the Middle East & Africa for oil, gas, and energy transition projects.

The report also focuses on emerging technologies shaping the market, including additive manufacturing, AI-enabled predictive maintenance, smart sensor integration, hybrid ceramic materials, and magnetic bearings. Key industry segments, such as energy, aerospace, chemical processing, healthcare, and research institutions, are analyzed for adoption trends, operational requirements, and sector-specific performance metrics. Additionally, niche markets like quantum computing, high-speed cryogenic turbines, and superconducting devices are highlighted, providing strategic insights into innovation, investment opportunities, and future growth pathways across the global cryogenic bearings landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sandvik, FLSmidth, Joy Global, Weir Group, ABB, Caterpillar, Murray & Roberts, China Coal Technology & Engineering Group, Howden Group, Metso Outotec |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |