Reports

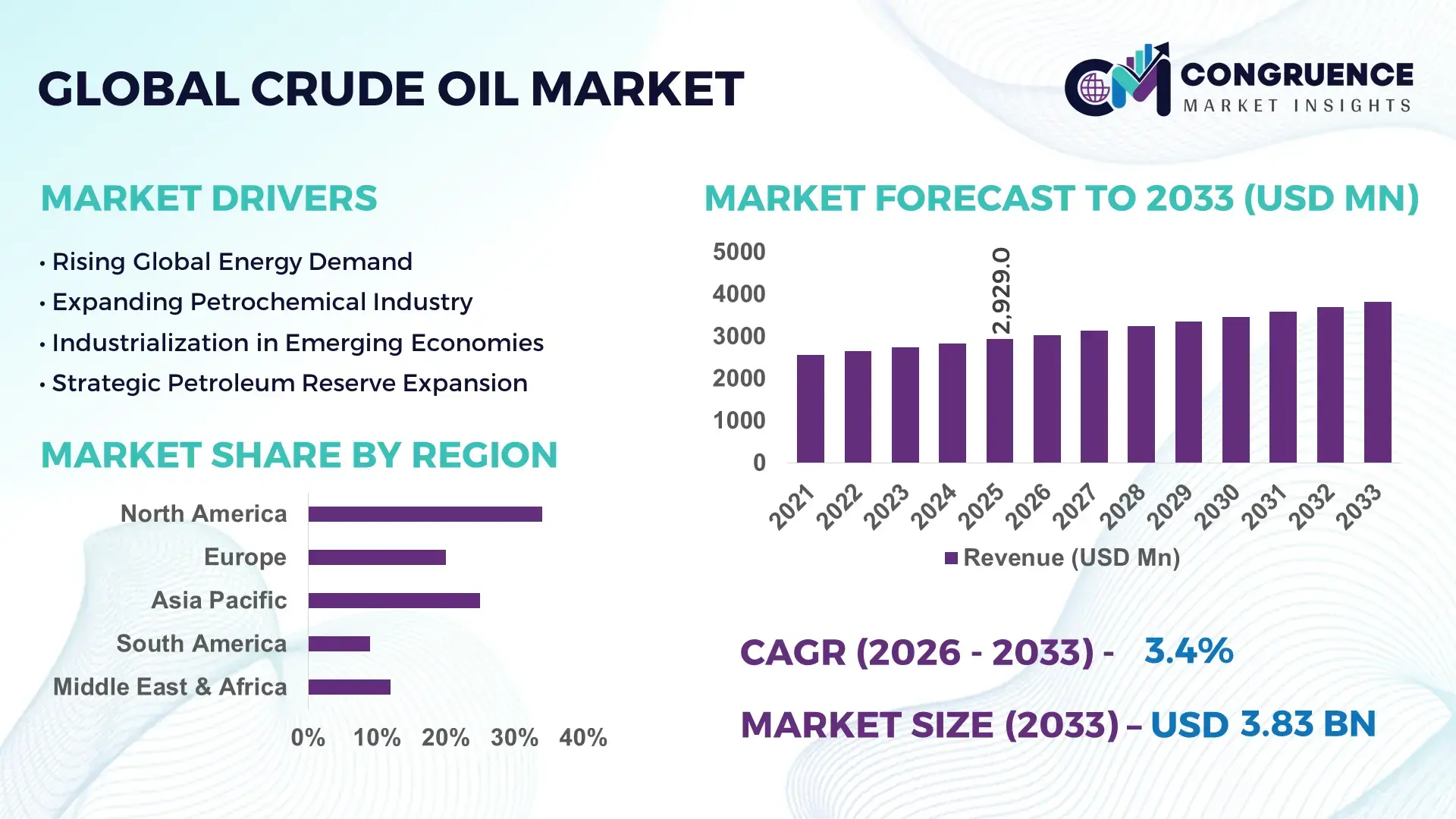

The Global Crude Oil Market was valued at USD 2929 Million in 2025 and is anticipated to reach a value of USD 3827.22 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033. Escalating geopolitical tensions and sudden war scenarios since yesterday have intensified supply uncertainty, triggering short-term price volatility and strategic stockpiling across major importing economies.

The United States remains the dominant country in the global crude oil market with production consistently exceeding 13 million barrels per day, supported by advanced shale extraction technologies and digital oilfield integration. Capital expenditure in upstream operations surpassed USD 120 billion in recent investment cycles, reflecting sustained drilling activity across the Permian Basin. Refining capacity stands above 18 million barrels per day, enabling high-value downstream applications in transportation fuels, petrochemicals, and aviation turbine fuel. Over 65% of domestic crude output is processed for transportation fuels, while petrochemical feedstock demand accounts for nearly 15%. Deployment of enhanced oil recovery and AI-enabled reservoir modeling has improved well productivity by over 20%, strengthening operational efficiency across mature and unconventional fields.

Market Size & Growth: Valued at USD 2929 Million in 2025, projected to reach USD 3827.22 Million by 2033 at 3.4% CAGR, driven by rising energy security investments and sustained industrial fuel demand.

Top Growth Drivers: Strategic petroleum reserve expansion (18%), petrochemical demand growth (12%), upstream digitalization efficiency gains (15%).

Short-Term Forecast: By 2028, predictive drilling analytics are expected to reduce operational downtime by 14%.

Emerging Technologies: AI-based reservoir simulation, carbon capture integration in upstream fields, and advanced hydraulic fracturing optimization.

Regional Leaders: North America projected above USD 1100 Million by 2033 with shale innovation focus; Middle East exceeding USD 950 Million driven by capacity expansion; Asia-Pacific surpassing USD 800 Million fueled by refining upgrades.

Consumer/End-User Trends: Transportation accounts for over 55% of crude utilization, while petrochemicals and aviation sectors show accelerated adoption.

Pilot Example: In 2024, a Gulf-based upstream project achieved 17% productivity improvement via AI-driven well monitoring.

Competitive Landscape: Saudi Aramco holds approximately 15% production share, followed by ExxonMobil, Shell, BP, and Chevron.

Regulatory & ESG Impact: Emission intensity reduction targets of 25% by 2030 influencing upstream modernization.

Investment Patterns: Global upstream investments exceeded USD 450 billion recently, with increasing allocation toward low-carbon extraction.

Innovation & Outlook: Integration of digital twins and automated drilling platforms shaping resilient and technology-driven crude oil operations.

The crude oil market serves critical sectors including transportation fuels (over 55% consumption), petrochemicals (approximately 18%), industrial manufacturing, and power generation in emerging economies. Recent advancements such as smart drilling rigs, real-time seismic imaging, and carbon capture utilization systems are transforming operational performance. Regulatory measures targeting methane emission reductions and carbon intensity benchmarks are accelerating modernization of aging infrastructure. Asia-Pacific consumption continues to rise due to expanding refining capacity exceeding 35 million barrels per day, while Middle Eastern producers are investing in downstream petrochemical integration. Future growth pathways emphasize supply chain diversification, energy security reinforcement, and hybrid integration with low-carbon technologies to ensure long-term market stability.

The crude oil market remains strategically indispensable to global energy security, industrial productivity, and defense logistics, particularly under heightened war-driven supply disruptions. Benchmark Brent crude prices have shown intraday volatility exceeding 8% during geopolitical escalations, prompting governments to enhance strategic petroleum reserves by over 10% in certain regions. Advanced digital oilfield technology delivers 22% efficiency improvement compared to conventional manual reservoir management systems, enabling producers to stabilize output despite operational constraints.

North America dominates in production volume, while Asia-Pacific leads in adoption with over 60% of refineries deploying advanced process optimization software. By 2027, AI-enabled predictive maintenance across upstream assets is expected to reduce equipment failure rates by 18%, strengthening operational continuity. Firms are committing to ESG metrics including 30% methane emission reductions by 2030, aligning with global decarbonization targets while maintaining output stability.

In 2024, Saudi Arabia achieved a 12% reduction in upstream carbon intensity through automated monitoring and carbon capture integration initiatives. Comparative benchmarks show automated drilling platforms deliver 15% faster well completion compared to traditional rotary systems. Over the next three years, integration of digital twins and carbon management analytics is anticipated to improve asset utilization rates by 16%. Positioned at the intersection of resilience, compliance, and energy transition strategy, the crude oil market continues to function as a foundational pillar supporting industrial continuity and macroeconomic stability.

Escalating geopolitical conflicts and war-related supply chain disruptions have compelled governments to expand strategic petroleum reserves and incentivize domestic drilling. Global oil demand remains above 100 million barrels per day, with emerging economies contributing over 60% of incremental consumption growth. Increased defense operations and aviation fuel requirements during conflict scenarios can raise regional fuel demand by 5–7% within short periods. National energy security policies have led to upstream investment commitments exceeding USD 450 billion globally, strengthening drilling programs and offshore exploration. Technological deployment such as horizontal drilling and enhanced oil recovery has boosted output efficiency by nearly 20%, enabling producers to offset potential export shortfalls. These strategic measures reinforce the resilience of the crude oil market amid evolving geopolitical uncertainties.

Stringent environmental regulations targeting methane emissions and carbon intensity are increasing compliance costs for upstream operators. Over 70 countries have announced net-zero commitments, driving gradual diversification toward renewable energy alternatives. Carbon pricing mechanisms in several developed economies have raised operational expenditures by up to 10% for carbon-intensive assets. Financial institutions are tightening lending conditions for new oil exploration projects, redirecting capital toward low-carbon investments. Electric vehicle adoption, growing at double-digit percentages annually in key markets, is moderating long-term gasoline demand projections. Additionally, public pressure and shareholder activism are influencing capital discipline strategies, limiting aggressive production expansion. These combined regulatory and structural shifts create constraints on sustained high-volume crude output growth.

Petrochemical demand continues to rise, accounting for nearly 18% of global crude utilization, driven by plastics, synthetic fibers, and specialty chemicals. Asia-Pacific refining and petrochemical capacity expansions exceeding 2 million barrels per day are creating new feedstock integration opportunities. Advanced refinery configurations such as residue upgrading and hydrocracking improve product yield efficiency by 15%, enhancing value extraction from each barrel. Emerging economies with urbanization rates above 55% are witnessing rapid infrastructure and packaging demand, stimulating naphtha and LPG consumption. Integration of carbon capture in refining units offers dual benefits of emission reduction and regulatory compliance, unlocking sustainable production pathways. These factors collectively position downstream diversification as a significant growth lever within the global crude oil market.

Crude oil prices can fluctuate by more than 10% within days during armed conflicts or sanctions announcements, complicating procurement and hedging strategies for refiners. Shipping insurance premiums in high-risk maritime corridors have surged by up to 30% during war scenarios, increasing landed crude costs. Infrastructure vulnerabilities, including pipeline sabotage or port blockades, disrupt supply chains and delay exports. Currency depreciation in importing nations further amplifies procurement expenses. Additionally, balancing production quotas among major exporting alliances becomes increasingly complex during unstable geopolitical conditions. Such volatility undermines long-term investment planning and elevates risk exposure across upstream, midstream, and downstream operations, reinforcing the need for diversified sourcing and digital risk management systems within the crude oil market.

Strategic Petroleum Reserve Expansion Surges by 12% Amid Geopolitical Tensions: Heightened war scenarios and supply chain disruptions have prompted major importing nations to expand strategic petroleum reserves by over 12% within a 12-month window. The United States maintains reserves exceeding 350 million barrels, while China’s commercial and state reserves collectively surpass 400 million barrels. This accumulation trend has tightened spot availability by nearly 4%, influencing short-term pricing benchmarks and strengthening long-term procurement contracts. Refiners are increasingly adopting diversified sourcing strategies, with over 35% of crude procurement now structured under multi-origin agreements to mitigate geopolitical risk exposure.

Digital Oilfield Adoption Improves Upstream Efficiency by 20%: Advanced digital oilfield technologies, including AI-based reservoir modeling and predictive maintenance platforms, are improving drilling accuracy and production optimization by approximately 20%. Over 60% of large-scale upstream operators in North America have integrated real-time well monitoring systems, reducing non-productive time by 15%. Automated drilling rigs now account for nearly 30% of new installations globally, shortening well completion cycles by 10–18%. These measurable operational gains are reshaping capital allocation toward data-driven asset management and performance analytics.

Refining and Petrochemical Integration Expands by 8% Annually: Integrated refinery-petrochemical complexes are increasing output efficiency, with petrochemical feedstock utilization rising by 8% annually in Asia-Pacific. More than 40% of new refinery projects incorporate residue upgrading and hydrocracking units, improving product yield efficiency by 12–15%. This structural shift reflects rising demand for plastics, synthetic fibers, and specialty chemicals, which collectively account for nearly 18% of total crude consumption. Enhanced integration supports higher-value derivative production and reduces reliance on fuel-only output models.

Carbon Intensity Reduction Initiatives Achieve 25% Emission Cuts in Pilot Fields: Upstream operators are deploying carbon capture and methane detection systems, achieving up to 25% emission reductions in pilot fields. Approximately 45% of major oil companies have announced methane intensity targets aligned with a 30% reduction by 2030. Deployment of satellite-based monitoring and automated leak detection has reduced fugitive emissions by 18% in monitored assets. These quantifiable ESG-focused advancements are influencing investment decisions and strengthening regulatory compliance frameworks across global crude oil operations.

The crude oil market segmentation reflects distinct variations across types, applications, and end-user categories, each influenced by refining complexity, consumption patterns, and industrial demand. By type, light crude holds a dominant position due to its higher yield of gasoline and middle distillates, while heavy crude remains critical for complex refineries equipped with advanced upgrading units. Applications are primarily concentrated in transportation fuels, petrochemical feedstocks, and industrial energy use, with transportation accounting for more than half of global crude utilization. End-user segmentation highlights refiners as the leading category, followed by petrochemical manufacturers and power generation utilities in developing economies. Regional demand dynamics further shape segmentation, with Asia-Pacific representing over 35% of global consumption, driven by industrial expansion and urbanization. These segmentation insights enable decision-makers to align investment, procurement, and operational strategies with high-demand, high-efficiency market segments.

Light crude oil currently accounts for approximately 48% of global crude processing due to its lower sulfur content and higher gasoline yield efficiency. Medium crude represents nearly 32%, while heavy crude contributes around 20% of total production streams. Light crude remains the leading segment because it requires less complex refining and generates up to 15% higher output of high-value transportation fuels compared to heavier grades. In contrast, heavy crude processing is the fastest-growing type, expanding at an estimated 4.2% CAGR, driven by refinery modernization projects that integrate cokers and hydrocrackers to enhance conversion efficiency by 18%. Medium crude continues to play a strategic balancing role, particularly in regions with moderate refining complexity. Collectively, medium and heavy grades account for 52% of total supply diversity, supporting energy security objectives.

Transportation fuels dominate crude oil applications, representing approximately 55% of total consumption, including gasoline, diesel, and aviation turbine fuel. Petrochemical feedstock accounts for nearly 18%, while industrial energy and power generation collectively contribute around 15%. Transportation remains the leading application due to sustained global vehicle fleets exceeding 1.4 billion units and aviation recovery trends that raised jet fuel demand by over 12% year-on-year. Petrochemical application is the fastest-growing segment, expanding at an estimated 5.1% CAGR, supported by rising demand for plastics, packaging materials, and synthetic textiles. Asia-Pacific petrochemical capacity additions surpassed 2 million barrels per day equivalent in recent project cycles, strengthening feedstock integration. Industrial and marine fuel applications, though smaller, collectively account for 12% and provide stability in emerging markets.

Refineries represent the leading end-user segment, accounting for approximately 62% of crude oil utilization globally. Petrochemical manufacturers hold around 20%, while power generation utilities and industrial consumers collectively contribute nearly 18%. Refining remains dominant due to integrated downstream infrastructure exceeding 100 million barrels per day in global capacity. In comparison, petrochemical manufacturers are the fastest-growing end-user group, expanding at an estimated 5.4% CAGR, fueled by increasing demand for polymers and specialty chemicals in construction and consumer goods sectors. Power generation utilities maintain a niche presence in developing economies where oil-fired plants still supply up to 8% of electricity output. Industrial end-users, including shipping and heavy manufacturing, show adoption rates above 10% in energy-intensive sectors.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

North America’s dominance is supported by crude production exceeding 19 million barrels per day, with refining capacity above 20 million barrels per day and strategic reserves surpassing 350 million barrels. Europe represents approximately 18% of global crude oil consumption, with refinery throughput averaging 13 million barrels per day. Asia-Pacific holds nearly 30% of total demand, driven by combined consumption in China and India exceeding 20 million barrels per day. The Middle East & Africa contribute around 12% to global downstream demand while accounting for over 30% of export supply volumes. South America maintains close to 6% share, led by offshore production exceeding 3 million barrels per day in Brazil alone. Infrastructure modernization, refinery upgrades exceeding 5 million barrels per day in cumulative additions since 2022, and strategic pipeline expansions of over 8,000 kilometers globally are reinforcing regional performance differentials in the crude oil market.

How Are Advanced Shale Technologies Reshaping Production Efficiency and Downstream Integration?

North America holds approximately 34% share of the global crude oil market, with production surpassing 19 million barrels per day. Key demand drivers include transportation fuels accounting for nearly 57% of refined output and petrochemicals contributing around 16%. Regulatory frameworks such as methane emission reduction mandates target 30% cuts by 2030, influencing upstream investment decisions. Over 65% of operators deploy AI-based drilling analytics, improving well productivity by nearly 20%. ExxonMobil has expanded Permian Basin output beyond 600,000 barrels per day through digital reservoir optimization initiatives. Regional consumer behavior reflects higher enterprise adoption of automated risk management platforms, with over 70% of refiners integrating predictive maintenance systems to reduce downtime by 15%, strengthening operational resilience.

How Are Sustainability Mandates and Refinery Upgrades Driving Competitive Transformation?

Europe accounts for nearly 18% of global crude oil demand, with Germany, the UK, and France representing over 55% of regional refining capacity. Refinery throughput averages 13 million barrels per day, with utilization rates close to 82%. Regulatory bodies enforce carbon intensity benchmarks targeting 55% emission reductions by 2030, accelerating modernization of refining infrastructure. Approximately 40% of refineries have integrated advanced hydrocracking units to improve yield efficiency by 12%. BP is investing in digital twin technology across selected European refineries, achieving 10% process optimization improvements. Consumer behavior trends indicate strong preference for lower-sulfur fuels, with ultra-low sulfur diesel accounting for more than 75% of road fuel consumption, reflecting regulatory-driven demand shifts.

What Is Fueling Rapid Capacity Expansion and Industrial Consumption Growth?

Asia-Pacific represents nearly 30% of global crude oil consumption, with China, India, and Japan collectively exceeding 20 million barrels per day in demand. China alone processes over 14 million barrels per day, while India’s refining capacity has crossed 5 million barrels per day. Infrastructure investments include refinery expansions totaling more than 2 million barrels per day since 2023. Regional technology hubs are implementing automated blending systems and AI-based supply chain optimization, improving logistics efficiency by 18%. Sinopec has advanced integrated refinery-petrochemical complexes capable of converting 70% of crude into high-value chemicals. Consumer demand is influenced by industrial manufacturing growth exceeding 6% annually and expanding aviation markets, reinforcing robust crude oil utilization patterns.

How Are Offshore Discoveries and Trade Partnerships Strengthening Export Potential?

South America contributes approximately 6% to global crude oil market share, led by Brazil and Argentina. Brazil’s offshore pre-salt production exceeds 3 million barrels per day, accounting for nearly 75% of national output. Regional infrastructure upgrades include floating production storage units adding 500,000 barrels per day capacity. Government policies encourage foreign direct investment through royalty adjustments and export incentives. Petrobras has implemented subsea digital monitoring systems, reducing maintenance costs by 14%. Consumer demand is closely linked to transportation and industrial sectors, with diesel representing over 40% of refined fuel consumption. Trade agreements with Asia have increased crude exports by nearly 9% year-on-year, enhancing regional market integration.

How Are Capacity Expansions and Technological Modernization Enhancing Global Supply Influence?

The Middle East & Africa account for over 30% of global crude export supply while representing around 12% of downstream consumption. Major growth countries include the UAE and South Africa, with refining capacity expansions exceeding 1 million barrels per day in combined projects. Oil & gas and construction sectors drive nearly 60% of regional crude utilization. Technological modernization includes carbon capture deployment targeting 25% emission reductions in pilot assets. Saudi Aramco has implemented automated drilling platforms, shortening well completion time by 15%. Trade partnerships across Asia and Europe have expanded export routes, while regional consumer behavior reflects strong dependence on transportation fuels exceeding 65% of refined product demand.

United States – 20% share in the Crude Oil market: Dominance driven by production exceeding 13 million barrels per day and advanced shale extraction technologies enhancing operational efficiency.

Saudi Arabia – 17% share in the Crude Oil market: Leadership supported by sustainable output capacity above 10 million barrels per day and large-scale export infrastructure across global markets.

The crude oil market exhibits a moderately consolidated structure, with the top five producers collectively controlling approximately 55% of global output capacity. Over 100 national and international oil companies operate across upstream, midstream, and downstream segments, intensifying competitive positioning. Strategic initiatives include mergers, joint ventures, and digital transformation programs aimed at improving extraction efficiency by 15–20%. Capital expenditure commitments in upstream projects exceed USD 450 billion globally, with 30% allocated toward offshore and deepwater exploration. Partnerships between national oil companies and international majors are expanding cross-border production capacity by nearly 8% annually. Innovation trends include AI-driven seismic imaging, automated drilling systems, and carbon capture projects capable of reducing upstream emissions by up to 25%. Competitive differentiation increasingly depends on cost optimization, reserve replacement ratios above 100%, and integration of refining-petrochemical complexes that enhance margin stability across volatile pricing cycles.

Saudi Aramco

ExxonMobil

Shell

BP

Chevron

TotalEnergies

ConocoPhillips

Petrobras

Sinopec

Kuwait Petroleum Corporation

Technological transformation across the crude oil market is increasingly centered on automation, artificial intelligence, and carbon management solutions designed to enhance productivity and regulatory compliance. Advanced seismic imaging using 4D reservoir monitoring now improves hydrocarbon recovery rates by up to 10–15% compared to traditional 3D seismic methods, enabling more accurate well placement and reducing dry-well risks. Horizontal drilling combined with multi-stage hydraulic fracturing has boosted unconventional well output by nearly 20%, particularly in shale basins where lateral lengths frequently exceed 10,000 feet.

Digital oilfield platforms are now deployed across more than 60% of large upstream operations globally, integrating IoT sensors that generate real-time data streams exceeding 1 terabyte per well annually. Predictive maintenance systems leveraging machine learning algorithms have reduced equipment failure rates by approximately 18%, lowering non-productive time by 12–15%. Automated drilling rigs equipped with closed-loop control systems shorten well completion cycles by up to 14%, while robotic inspection technologies cut offshore platform inspection time by nearly 30%.

Carbon capture, utilization, and storage (CCUS) integration is becoming a strategic priority, with pilot facilities capable of capturing over 1 million metric tons of CO₂ annually. Methane detection satellites and drone-based infrared monitoring have reduced fugitive emissions by around 20% in digitally managed fields. Additionally, blockchain-enabled crude trading platforms are streamlining transaction settlements, decreasing documentation processing time by nearly 40%. These technology-driven efficiencies are reshaping asset optimization strategies, cost structures, and sustainability performance across the global crude oil market.

• In March 2025, Saudi Aramco completed the expansion of its Jafurah unconventional gas development, integrating advanced hydraulic fracturing and digital reservoir monitoring systems to enhance liquids recovery. The project supports increased condensate output and strengthens upstream capacity resilience. Source: www.aramco.com

• In February 2025, ExxonMobil announced the start-up of a new offshore production platform in Guyana, adding approximately 250,000 barrels per day of gross capacity through advanced subsea systems and high-efficiency floating production storage technology. Source: corporate.exxonmobil.com

• In April 2024, Shell commenced operations at its Whale deepwater platform in the U.S. Gulf of Mexico, designed to produce up to 100,000 barrels of oil equivalent per day using energy-efficient host technology to reduce greenhouse gas intensity. Source: www.shell.com

• In January 2024, Petrobras initiated production from the Sepetiba FPSO in Brazil’s Mero field, with processing capacity of 180,000 barrels of oil per day and 12 million cubic meters of gas daily, strengthening offshore crude supply from pre-salt reserves.

The Crude Oil Market Report provides a comprehensive evaluation of upstream, midstream, and downstream segments, covering conventional and unconventional crude types including light, medium, and heavy grades. The study analyzes production volumes exceeding 100 million barrels per day globally and assesses refining capacities surpassing 100 million barrels per day across key industrial economies. Market segmentation includes detailed insights by type, application, and end-user industries such as transportation fuels, petrochemicals, aviation, marine, and power generation.

Geographically, the report examines five primary regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—accounting collectively for over 95% of global crude production and consumption. It evaluates infrastructure assets including more than 2 million kilometers of pipelines worldwide, offshore platforms exceeding 7,000 units, and floating production storage facilities with cumulative capacity above 15 million barrels per day.

The report further investigates technological integration such as AI-driven drilling optimization, carbon capture systems capable of mitigating millions of metric tons of CO₂ annually, and digital oilfield solutions adopted by over 60% of major operators. Regulatory frameworks, emission reduction targets approaching 30% by 2030 in several regions, and strategic petroleum reserve policies are also analyzed. Emerging focus areas include refinery-petrochemical integration, offshore deepwater expansion, and energy security initiatives influencing capital allocation decisions across the crude oil market value chain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Saudi Aramco, ExxonMobil, Shell, BP, Chevron, TotalEnergies, ConocoPhillips, Petrobras, Sinopec, Kuwait Petroleum Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |