Reports

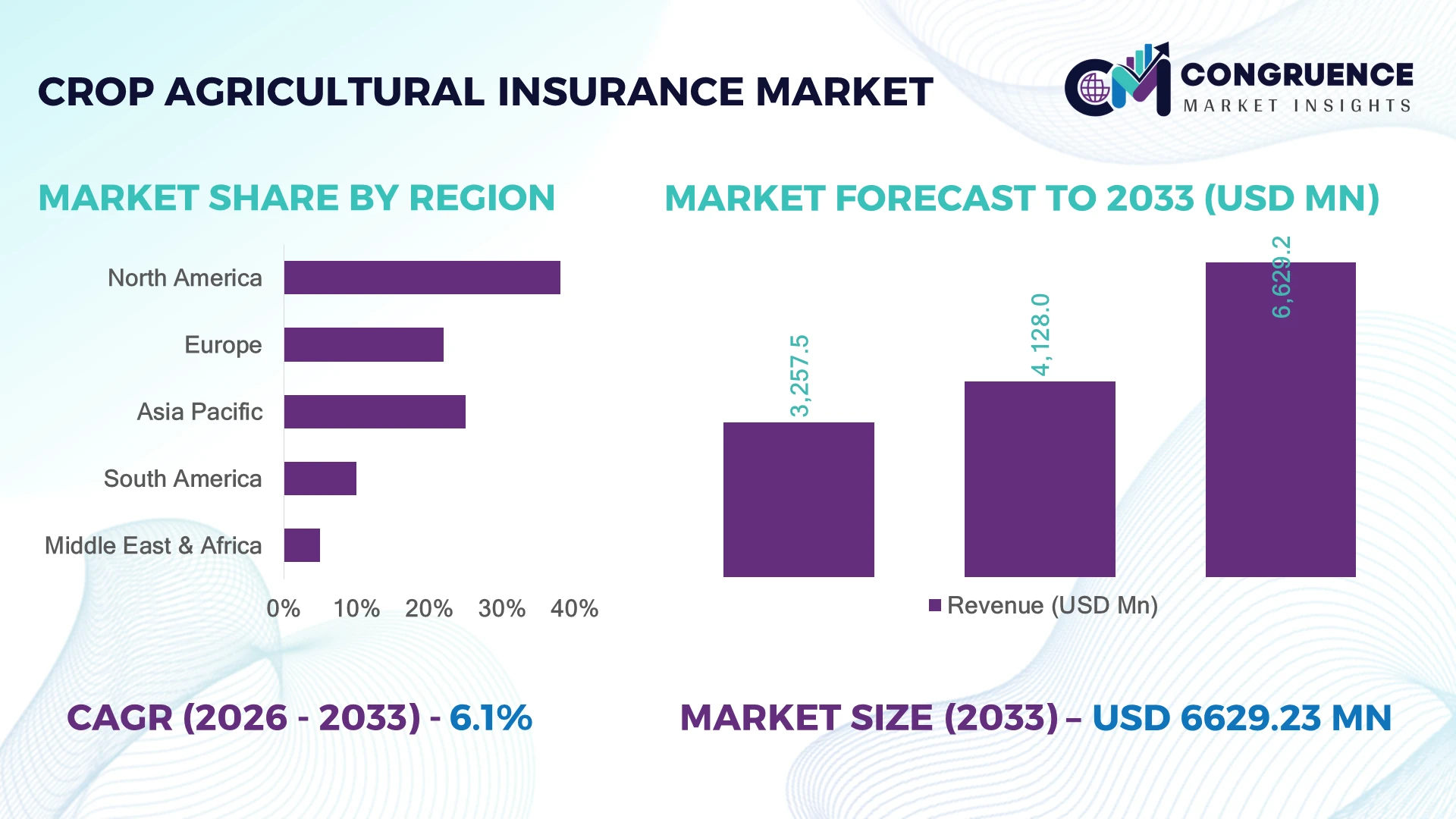

The Global Crop Agricultural Insurance Market was valued at USD 4,128.0 Million in 2025 and is anticipated to reach a value of USD 6,629.2 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Growth is driven by climate-risk management, expansion of parametric insurance models, satellite-based crop monitoring, and government-backed agricultural risk mitigation programs.

The United States dominates the market with nearly 35% share, supported by federal crop insurance programs covering over 120 million acres annually and advanced satellite-based risk assessment adoption. China follows with large-scale agricultural modernization and more than 1.3 billion tonnes of annual grain production capacity, while India is accelerating digital crop insurance enrollment after climate-related disruptions under government schemes. Compared with India’s fragmented farm landscape, the U.S. operates a highly structured insurance ecosystem with broader technology integration.

Strategic implication: insurers investing in digital risk analytics and climate-resilient solutions gain stronger competitive positioning.

Market Size & Growth: USD 4.13 Billion (2025) to USD 6.63 Billion (2033), 6.1% CAGR, driven by climate volatility and digital insurance platforms transforming agricultural risk management.

Top Growth Drivers: Climate-related crop losses 40%, government-supported insurance programs 35%, and precision agriculture adoption 25% are accelerating market expansion.

Short-Term Forecast: By 2028, digital claims processing reduces assessment time by 50% and improves settlement efficiency by 35%.

Emerging Technologies: AI-based risk scoring, satellite imaging, drone monitoring, and automated weather analytics are reshaping advanced crop insurance models.

Regional Leaders: North America reaches USD 2.3 Billion with high digital adoption; Asia-Pacific reaches USD 2.1 Billion through government programs; Europe reaches USD 1.2 Billion through sustainable farming policies.

Consumer/End-User Trends: Over 60% of commercial farmers prioritize technology-enabled insurance products offering faster claims and transparent risk evaluation.

Pilot/Case Example: 2023 satellite-based crop monitoring initiatives reduced field verification requirements by 45% and accelerated insurance assessments.

Competitive Landscape: North America leads with approximately 35% share; key players include Chubb Limited, Zurich Insurance Group, American International Group, Sompo Holdings, and AXA.

Regulatory & ESG Impact: Climate adaptation policies improve agricultural resilience, with insurance-supported sustainability programs reducing financial exposure from extreme weather events by 30%.

Investment & Funding: More than USD 5 Billion is directed toward agri-insurtech, partnerships, and digital claims infrastructure, strengthening global market capabilities.

Innovation & Future Outlook: Next-generation parametric insurance, AI forecasting, and blockchain-enabled claims verification are driving strategic shifts toward automated agricultural protection.

The Crop Agricultural Insurance Market is evolving beyond traditional indemnity coverage as insurers integrate satellite intelligence, predictive analytics, and automated underwriting systems. Adoption of digital insurance tools has increased by nearly 45% among technology-enabled agricultural operators, while regulatory reforms following extreme weather events such as droughts and floods are encouraging stronger risk-sharing frameworks. Emerging markets are increasingly adopting scalable insurance models supported by public-private partnerships, creating a transition toward more resilient agricultural ecosystems.

The Crop Agricultural Insurance Market is becoming strategically important as agriculture faces increasing climate uncertainty, supply-chain disruptions, and rising financial exposure from extreme weather events. Insurers, technology providers, and governments are restructuring risk-management approaches through digital platforms, satellite intelligence, and data-driven underwriting systems. Recent policy initiatives across major agricultural economies are accelerating modernization of insurance infrastructure and improving farmer accessibility.

Advanced AI-based crop assessment platforms now evaluate field conditions within hours compared with traditional manual inspections that require several days, reducing operational costs by nearly 30% and improving claim accuracy. North America maintains leadership through mature federal insurance systems, while Asia-Pacific demonstrates faster adoption momentum through government-supported digital agriculture programs and expanding rural connectivity.

Over the next 2–3 years, insurers are prioritizing automated claims processing, predictive weather analytics, and partnerships with agricultural technology firms. For example, satellite-enabled monitoring programs are helping insurers verify crop damage remotely, reducing inspection delays and improving farmer response times. Companies are increasing investments in insurtech collaborations, regional expansion, and climate-risk modeling capabilities. Strategic success will depend on building agile insurance ecosystems that combine technology, sustainability, and operational efficiency for long-term market leadership.

Increasing climate volatility is accelerating adoption of technology-enabled crop insurance solutions, with extreme weather events accounting for nearly 70% of agricultural insurance claims globally and digital monitoring platforms improving assessment efficiency by 40–50%. In the United States, satellite-based crop surveillance and predictive weather analytics are strengthening federal insurance programs by enabling faster risk evaluation. Companies are responding through investments in AI underwriting, remote sensing partnerships, and automated claims platforms. The strategic shift from traditional field inspections toward data-driven risk modeling is reducing operational delays while improving insurer profitability and farmer accessibility.

High premium costs, fragmented farm structures, and uneven digital infrastructure remain major constraints for crop agricultural insurance adoption. In countries such as India, smallholder farmers represent more than 80% of agricultural holdings, creating challenges for scalable insurance distribution and risk pricing. Administrative expenses can account for nearly 20–30% of policy servicing costs in developing markets due to manual verification processes. Insurers are addressing these limitations through localized partnerships, simplified policy structures, and digital enrollment channels. The key operational challenge is balancing affordable coverage with accurate risk assessment while maintaining sustainable underwriting models.

The integration of AI forecasting, satellite imagery, and parametric insurance models creates significant opportunities for market expansion, with automated risk assessment improving claim processing efficiency by approximately 50% and reducing manual verification requirements by 40%. Countries such as Brazil and India are increasing investment in digital agriculture ecosystems to improve farmer protection and climate resilience. Insurers are developing partnerships with agritech firms, weather data providers, and government agencies to expand coverage models. A major strategic opportunity lies in micro-insurance products that combine mobile platforms with real-time climate intelligence, enabling access to previously underserved agricultural segments.

Scaling advanced crop insurance systems requires overcoming fragmented agricultural data, cybersecurity concerns, and technology integration barriers. Approximately 35% of agricultural insurance providers still face limitations in accessing standardized farm-level datasets, affecting underwriting precision and portfolio management. In emerging markets, inconsistent connectivity and limited digital literacy restrict deployment of automated insurance platforms. Companies must strengthen cloud infrastructure, invest in secure data-sharing frameworks, and build partnerships with agricultural technology providers. The long-term competitive advantage will depend on creating interoperable insurance ecosystems capable of handling diverse farming conditions while maintaining reliable risk prediction and sustainable operations.

Parametric Insurance Adoption Growth Parametric crop insurance models are gaining traction as insurers move toward faster, event-based settlements triggered by weather indicators. Adoption of satellite and weather-index platforms has increased by nearly 40%, while automated claim verification can reduce assessment cycles by 50% compared with traditional inspections. In the United States and Australia, insurers are expanding partnerships with climate-data providers to improve policy accuracy. This shift is changing underwriting workflows by replacing manual field surveys with real-time risk measurement, improving operational efficiency and reducing administrative costs.

Satellite-Based Risk Monitoring Expansion Advanced remote sensing technologies are transforming crop insurance operations, with satellite imagery improving field-level visibility by approximately 45% and reducing physical verification requirements by 30–40%. Agricultural insurers are integrating geospatial analytics, drone monitoring, and AI-based crop health assessments into claims management processes. Rising climate variability and regulatory pressure for transparent risk evaluation are accelerating enterprise adoption. Companies are restructuring technology investments toward automated monitoring platforms that support faster decisions and stronger portfolio management.

Digital Farmer Access Platforms Rise Mobile-first insurance distribution is expanding as insurers address fragmented agricultural markets and improve farmer engagement. Digital enrollment channels have increased participation rates by nearly 35% in several developing agricultural economies, while electronic claim submission reduces processing delays by over 30%. In India, government-backed digital agriculture initiatives are encouraging insurers to develop integrated platforms combining farmer databases, weather information, and payment systems. The non-obvious shift is that customer accessibility, rather than only risk pricing, is becoming a major competitive differentiator.

AI Underwriting Modernization Accelerates Artificial intelligence is reshaping agricultural risk assessment through predictive analytics, automated pricing models, and portfolio optimization. AI-enabled underwriting tools improve forecasting accuracy by nearly 25–35% and help insurers identify regional risk variations more effectively. Extreme weather events, including drought and flooding pressures across major farming economies, are accelerating investments in intelligent insurance infrastructure. Companies are responding through technology partnerships, cloud deployment, and data-sharing ecosystems to create scalable insurance models with improved operational consistency.

Multi-peril crop insurance (MPCI) represents the leading type segment due to its broad coverage structure, protecting farmers against multiple risks including drought, flood, excessive rainfall, and yield losses. Its dominance is supported by government-backed programs in countries such as the United States, where MPCI covers more than 90% of insured farmland policies and remains the preferred solution among commercial growers. Traditional indemnity-based insurance continues to hold relevance in mature agricultural economies due to established distribution networks, while crop-hail insurance maintains importance for regions exposed to localized weather events. Parametric crop insurance is emerging as the fastest-growing type as insurers adopt weather-index triggers, satellite monitoring, and automated settlement mechanisms. Adoption of parametric models has increased by nearly 35–40% in climate-sensitive markets due to faster claims processing and lower administrative requirements. Companies are expanding digital underwriting capabilities, forming partnerships with climate-data providers, and developing hybrid insurance products that combine traditional coverage with real-time risk analytics.

Commercial farming is the leading application segment due to its high exposure to production risks, larger cultivated areas, and requirement for financial protection against unpredictable weather conditions. Large-scale agricultural enterprises in countries such as the United States, Brazil, and Australia rely heavily on crop insurance to protect operational investments and maintain supply-chain stability. Commercial farms account for approximately 60%+ of premium volumes in several developed agricultural markets because of higher acreage coverage and greater insurance penetration. Smallholder farming is the fastest-growing application segment as governments, insurers, and technology providers expand digital access models. Mobile-based enrollment, simplified policy structures, and government-supported insurance initiatives are increasing participation among smaller farmers, with digital distribution improving accessibility by nearly 30–40% in emerging markets. Plantation agriculture and specialty crop producers are also adopting customized insurance products for high-value crops requiring specialized risk protection.

Farmers represent the dominant end-user segment as crop insurance remains a critical financial protection tool against weather uncertainty, yield fluctuations, and production losses. Commercial farmers and agricultural enterprises drive demand through large-scale acreage coverage, risk management requirements, and integration with lending systems. In the United States, government-supported insurance programs protect over 100 million acres annually, demonstrating the importance of institutionalized crop protection frameworks for agricultural stakeholders. Insurance providers and government agencies represent the fastest-growing end-user category as public-private partnerships expand climate adaptation programs and digital insurance ecosystems. Governments are increasing investments in agricultural resilience initiatives, while insurers are developing AI-based underwriting, automated claims processing, and customized coverage solutions. Banks and agricultural lenders are also strengthening collaboration with insurers, as protected farm assets improve credit reliability and financing confidence.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

North America remains the leading market due to advanced crop insurance frameworks, large-scale commercial farming operations, and strong government participation. The region contributes nearly 38% of global crop agricultural insurance activity, supported by the United States federal insurance ecosystem covering more than 100 million acres annually. Insurers are increasingly deploying satellite imaging, AI-based underwriting, and automated claims platforms to improve operational efficiency. Partnerships between insurance providers and agricultural technology companies are expanding, with digital assessment tools reducing field verification requirements by nearly 40%. The region’s mature infrastructure enables insurers to focus on precision risk pricing and climate-resilient product innovation.

United States Market Outlook: The United States dominates North America through its structured crop insurance framework, extensive agricultural production base, and technology-driven risk management systems. The country supports large-scale coverage across corn, wheat, soybean, and specialty crop producers. More than 90% of insured crop policies utilize multi-peril insurance structures, while increasing adoption of remote sensing technologies is improving claim accuracy and operational speed. Insurers are strengthening partnerships with agritech firms to enhance predictive modeling and portfolio management.

Europe is advancing crop agricultural insurance adoption through climate adaptation initiatives, sustainable farming regulations, and improved digital monitoring capabilities. The region represents approximately 22% of global market activity, supported by agricultural modernization programs across countries such as France, Germany, and Italy. Increasing extreme weather events are encouraging insurers to develop flexible coverage models using weather analytics and satellite-based assessments. Digital platforms are improving policy administration efficiency by nearly 30%, enabling faster farmer engagement and claims processing. Companies are aligning product strategies with sustainability objectives, supporting resilient agricultural practices and reducing financial exposure from climate-related production losses.

France Market Outlook: France holds a strategic position in Europe due to its extensive agricultural sector, advanced farming infrastructure, and strong integration of insurance solutions into commercial agriculture. The country is among Europe’s largest agricultural producers, with more than 25 million hectares of agricultural land supporting diverse crop production. Insurers are expanding climate-risk products and digital monitoring solutions to support farmers facing increasing weather variability and regulatory sustainability requirements.

Asia-Pacific is becoming the fastest-transforming market as governments expand agricultural protection programs and digital farming infrastructure. The region accounts for nearly 25% of global crop insurance demand, driven by large farming populations in China and India. Digital enrollment platforms, mobile-based insurance access, and satellite monitoring are improving coverage reach, with technology-enabled insurance adoption increasing by more than 35% in emerging agricultural markets. Public-private partnerships are strengthening rural insurance ecosystems, while insurers are developing affordable products for fragmented farming communities. The region’s strategic advantage lies in combining large agricultural production capacity with rapidly expanding digital infrastructure.

China Market Outlook: China leads Asia-Pacific through large-scale agricultural modernization, government-supported insurance programs, and advanced digital agriculture deployment. The country produces more than 650 million tonnes of grain annually, creating significant demand for risk protection solutions. Insurers are integrating remote sensing, agricultural databases, and automated claims platforms to improve coverage efficiency. Investments in smart farming infrastructure are strengthening the connection between agricultural data and insurance decision-making.

South America is gaining importance due to its export-oriented agricultural sector, expanding commercial farming operations, and increasing climate-related risks. The region contributes approximately 10% of global crop agricultural insurance activity, with Brazil and Argentina representing major demand centers. Large-scale soybean, corn, and livestock-linked farming operations are driving adoption of customized insurance products. Satellite monitoring and digital claim solutions are improving operational efficiency, with remote assessment reducing inspection requirements by nearly 35%. However, uneven rural connectivity and fragmented insurance penetration remain challenges. Companies are responding through partnerships with agricultural cooperatives, digital platforms, and financial institutions to improve accessibility.

Brazil Market Outlook: Brazil represents the largest agricultural insurance opportunity in South America due to its global leadership in soybean, corn, and agricultural exports. The country cultivates more than 70 million hectares of major crops, creating significant demand for risk management solutions. Insurers are expanding partnerships with agritech companies and financial institutions to improve coverage penetration, particularly among large commercial producers and export-focused farming enterprises.

Middle East & Africa is emerging as a strategic market as governments and development organizations prioritize agricultural resilience, food security, and climate adaptation. The region currently contributes around 5% of global crop agricultural insurance activity, with adoption concentrated in South Africa, Egypt, and selected agricultural economies. Digital insurance platforms, weather-index products, and mobile-based distribution models are improving accessibility, particularly where traditional insurance infrastructure remains limited. Climate challenges such as drought and water scarcity are increasing demand for innovative risk-transfer solutions. Companies are investing in localized partnerships, technology-enabled underwriting, and scalable insurance models to address underserved agricultural markets.

South Africa Market Outlook: South Africa leads the regional market due to its developed agricultural sector, commercial farming base, and stronger financial infrastructure. The country supports more than 12 million hectares of cultivated agricultural land, creating demand for advanced crop protection solutions. Insurers are adopting satellite analytics and digital risk assessment tools to improve underwriting accuracy and expand coverage for commercial growers facing increasing climate variability.

The Crop Agricultural Insurance Market features competition between global insurers such as Chubb Limited, Zurich Insurance Group, and AXA versus regional specialists, government-backed insurers, and digital insurtech providers. The top five players collectively account for approximately 35–40% of market activity, creating a moderately consolidated structure. Competition is based on underwriting accuracy, technology integration, pricing flexibility, claims speed, and distribution networks. Digital platforms improve processing efficiency by 30–50%, while satellite-based assessments reduce manual verification costs by nearly 40%. Companies are expanding through agritech partnerships, AI underwriting investments, and customized climate-risk products. The competitive shift is moving from traditional indemnity coverage toward predictive, data-driven insurance ecosystems. High entry barriers include regulatory approvals, actuarial expertise, farmer networks, and access to agricultural datasets. Winning players will combine technology leadership, localized coverage models, and scalable risk analytics.

Zurich Insurance Group

AXA

American International Group

Sompo Holdings

Tokio Marine Holdings

Agriculture Insurance Company of India

QBE Insurance Group

Allianz

Kshema General Insurance

Great American Insurance Group

Everest Group

Artificial intelligence, satellite analytics, and remote sensing are becoming core technologies in crop insurance modernization. AI-based underwriting improves risk classification accuracy by 25–35%, while satellite monitoring reduces manual field assessment requirements by nearly 40%. Compared with traditional inspection methods requiring physical surveys, digital assessment platforms improve claim evaluation speed by more than 50%, giving technology-focused insurers a competitive advantage.

Parametric insurance platforms and blockchain-enabled claim verification are emerging as disruptive models. Weather-index solutions enable automated settlements using predefined climate triggers, reducing administrative processing time by approximately 30%. Adoption is expanding among insurers serving climate-sensitive agricultural markets, where faster payouts and transparent verification improve farmer participation. Companies integrating these systems benefit through lower operational costs and stronger customer retention.

Between 2026 and 2028, insurance providers are prioritizing AI forecasting, cloud-based risk platforms, and connected agricultural data ecosystems. Technology leaders and digital-first insurers will gain advantages through scalable underwriting models, while traditional providers are investing in partnerships with agritech companies to modernize legacy systems. The competitive focus is shifting from claim payment capacity toward predictive risk prevention and data-driven agricultural resilience.

March 2025 — Syngenta expanded its partnership with Planet Labs to integrate near-daily satellite imagery into Cropwise digital agriculture solutions. The platform uses 3-meter resolution imagery, improving crop monitoring and enabling faster risk assessment workflows. Source: www.syngenta.com

February 2026 — Ministry of Agriculture & Farmers Welfare expanded technology-based crop insurance initiatives by allowing additional coverage options under PMFBY and strengthening digital assessment mechanisms. The program continues supporting millions of farmers through technology-enabled risk protection. Source: www.pib.gov.in

January 2025 — Kshema General Insurance continued scaling its digital crop insurance model in India through app-based insurance access and automated claim services. The platform supports protection across 100+ crops, improving accessibility for farmers through digital distribution. Source: www.kshema.co

2025 — Pradhan Mantri Fasal Bima Yojana increased adoption of AI-enabled tools including YES-TECH and CROPIC for crop assessment modernization. Technology-based yield estimation received a minimum 30% weightage in selected assessments, improving transparency in insurance operations.

The Crop Agricultural Insurance Market Report provides comprehensive coverage of insurance types, including multi-peril crop insurance, parametric insurance, and specialized crop protection solutions. The analysis evaluates applications across commercial farming, smallholder agriculture, and specialty crop production while assessing demand from farmers, insurers, government agencies, and financial institutions. The report examines major markets across North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The study covers emerging technologies such as AI underwriting, satellite monitoring, remote sensing, digital claims platforms, and automated risk assessment systems. It analyzes adoption patterns, competitive strategies, partnership models, and operational transformation across key industry participants. The report supports investment planning, expansion decisions, product innovation, and competitive positioning by identifying technology shifts, regional opportunities, and strategic priorities shaping market direction through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,128.0 Million |

| Market Revenue (2033) | USD 6,629.2 Million |

| CAGR (2026–2033) | 6.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Chubb Limited; Zurich Insurance Group; AXA; American International Group; Sompo Holdings; Tokio Marine Holdings; Agriculture Insurance Company of India; QBE Insurance Group; Allianz; Kshema General Insurance; Great American Insurance Group; Everest Group |

| Customization & Pricing | Available on Request (10% Customization Free) |