Reports

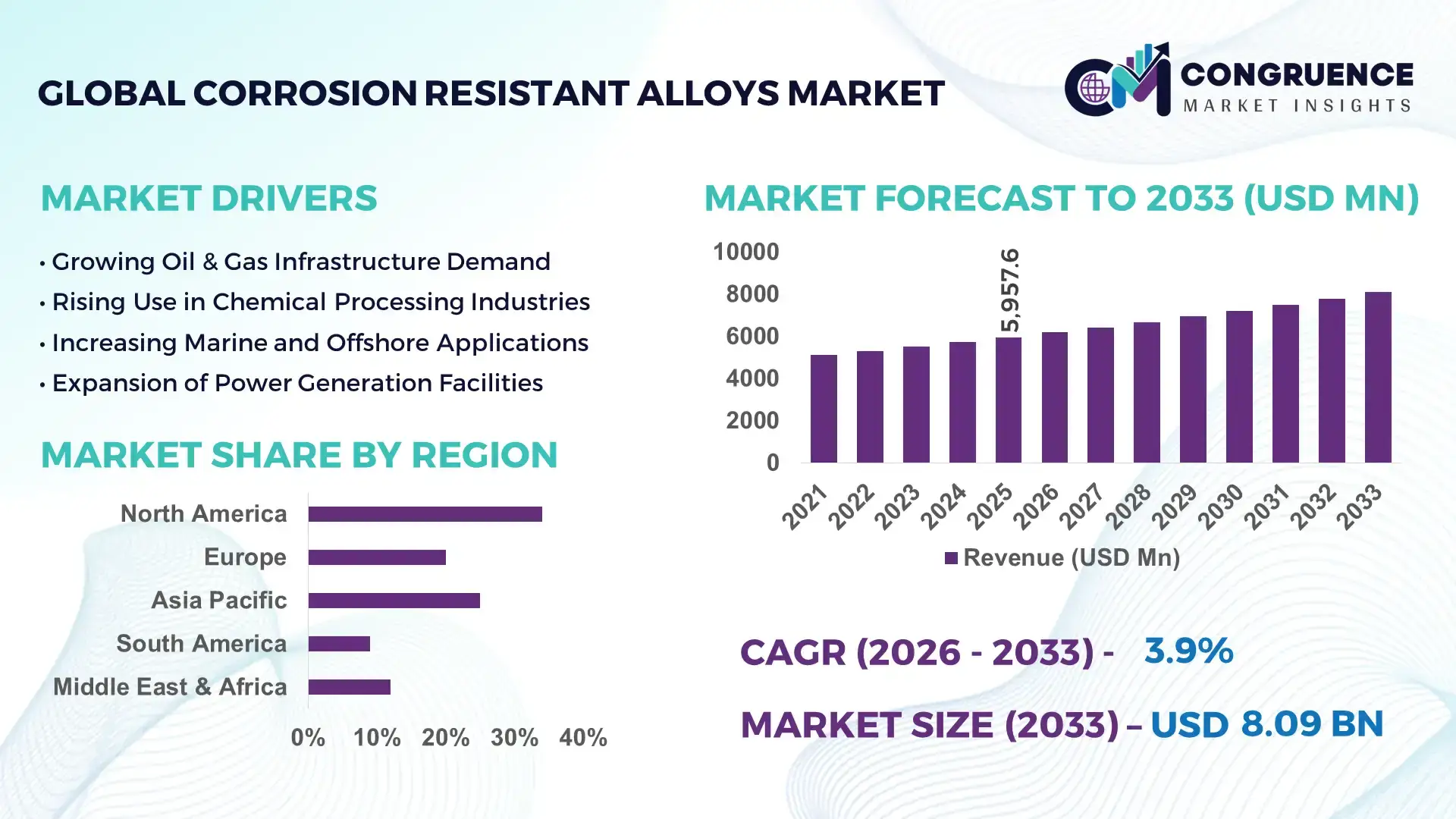

The Global Corrosion Resistant Alloys Market was valued at USD 5957.55 Million in 2025 and is anticipated to reach a value of USD 8090.81 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. The growth is primarily driven by rising demand for high-performance metallic materials capable of withstanding extreme chemical, marine, and high-temperature industrial environments.

The United States represents a dominant production hub in the Corrosion Resistant Alloys market, supported by advanced metallurgical infrastructure and large-scale industrial demand. The country operates more than 90 specialized alloy manufacturing facilities producing high-performance nickel, titanium, and stainless-based corrosion-resistant materials used across aerospace, energy, and petrochemical sectors. Annual domestic alloy steel production exceeds 80 million metric tons, with a significant portion engineered for corrosion protection applications. U.S. investments in advanced materials research surpassed USD 2.4 billion in 2024, enabling the development of next-generation alloys designed to withstand temperatures above 1000°C and aggressive chemical exposure. Adoption is particularly strong in offshore energy projects and chemical processing plants, where over 65% of critical components rely on corrosion-resistant alloys to maintain operational safety and extend equipment life cycles.

• Market Size & Growth: The Corrosion Resistant Alloys Market reached USD 5957.55 Million in 2025 and is projected to reach USD 8090.81 Million by 2033, growing at a CAGR of 3.9% due to increasing demand for durable metals in marine, oil & gas, and chemical processing infrastructure.

• Top Growth Drivers: Industrial corrosion control adoption increasing by 38%, offshore infrastructure expansion by 29%, and chemical processing equipment demand improving operational efficiency by 24%.

• Short-Term Forecast: By 2028, advanced corrosion-resistant alloy coatings are expected to reduce industrial maintenance costs by nearly 18% while improving equipment durability by 22%.

• Emerging Technologies: Additive manufacturing of nickel superalloys, nano-structured corrosion-resistant coatings, and AI-driven alloy composition modeling are transforming materials development.

• Regional Leaders: North America projected to reach USD 2450 Million by 2033 with strong aerospace demand; Asia-Pacific expected to approach USD 2950 Million driven by infrastructure expansion; Europe estimated near USD 1820 Million supported by advanced manufacturing.

• Consumer/End-User Trends: Oil and gas operators account for nearly 35% of total usage, followed by chemical processing plants and marine infrastructure with strong demand for long-life alloy components.

• Pilot or Case Example: In 2024, a large offshore energy operator implemented nickel-based corrosion resistant alloys in subsea pipelines, reducing maintenance downtime by 27%.

• Competitive Landscape: The market leader holds approximately 18% share, followed by several major global alloy manufacturers and specialty metals producers operating across aerospace and industrial segments.

• Regulatory & ESG Impact: Environmental regulations requiring corrosion-resistant materials in pipelines and chemical facilities are encouraging durable alloy adoption to reduce leakage risks and environmental contamination.

• Investment & Funding Patterns: Over USD 1.8 billion has been invested in advanced alloy manufacturing upgrades and materials research facilities since 2023.

• Innovation & Future Outlook: Hybrid alloys combining nickel, chromium, and molybdenum with advanced heat treatment processes are improving corrosion resistance by more than 30%, enabling longer service life for industrial infrastructure.

Corrosion resistant alloys play a critical role across multiple industries including oil and gas, aerospace, marine engineering, power generation, and chemical manufacturing. The oil and gas sector alone contributes nearly 35% of total material demand due to its requirement for pipelines, valves, and drilling equipment capable of resisting aggressive environments. Technological advances such as vacuum induction melting, powder metallurgy, and additive manufacturing are enabling the development of alloys with improved microstructural stability and higher resistance to oxidation and pitting corrosion. Governments worldwide are also introducing stricter infrastructure safety regulations, increasing the use of corrosion-resistant materials in energy and transportation systems. Rapid industrialization across Asia-Pacific and increasing offshore energy investments are expected to further accelerate demand for advanced corrosion resistant alloys in the coming decade.

The Corrosion Resistant Alloys Market holds strategic importance for industries requiring materials capable of operating in extreme chemical, thermal, and marine environments. These alloys are widely utilized in oil and gas pipelines, aerospace turbine systems, desalination plants, and chemical reactors where long-term structural integrity is critical. Global industrial corrosion costs are estimated to exceed USD 2.5 trillion annually, equivalent to nearly 3–4% of global GDP, highlighting the economic significance of corrosion-resistant materials. Businesses are increasingly investing in advanced alloy compositions to extend equipment life cycles and minimize maintenance disruptions. Modern alloy engineering technologies are transforming the industry’s performance benchmarks. For example, nano-structured corrosion resistant alloys deliver nearly 35% improvement in oxidation resistance compared to conventional stainless steel standards, enabling longer operational lifetimes in high-temperature environments. Advanced computational metallurgy and AI-assisted alloy design are also accelerating product innovation, reducing material development cycles by nearly 40%.

Regional dynamics illustrate distinct adoption patterns. Asia-Pacific dominates in production volume due to large-scale steel and specialty metal manufacturing facilities, while North America leads in technological adoption with nearly 48% of advanced alloy research facilities integrating AI-based materials engineering tools. Europe remains a key market for high-performance alloys used in energy transition technologies such as hydrogen processing and offshore wind infrastructure. In the short term, the market is expected to experience significant technological integration. By 2028, AI-driven metallurgical modeling is projected to reduce alloy development time by nearly 30%, enabling faster commercialization of high-performance corrosion-resistant materials. Companies are also incorporating ESG-focused strategies, committing to 25% recycled metal usage in alloy production by 2030 to reduce environmental impact.

A notable micro-scenario emerged in 2024 when a European aerospace manufacturer implemented advanced nickel-chromium alloys in turbine components, improving oxidation resistance by 32% and extending maintenance intervals by nearly 20%. These advancements demonstrate the role of corrosion resistant alloys in improving industrial reliability. As industries pursue durability, safety, and sustainability in infrastructure systems, the Corrosion Resistant Alloys Market is positioned as a foundational pillar supporting resilient industrial operations, regulatory compliance, and long-term sustainable growth.

Expansion of offshore oil and gas exploration activities is a significant driver for the Corrosion Resistant Alloys Market. Offshore drilling platforms, subsea pipelines, and marine processing facilities operate in highly corrosive saltwater environments where conventional steel materials degrade quickly. Corrosion resistant alloys such as nickel-based superalloys and duplex stainless steels provide superior resistance to chloride-induced corrosion, making them essential for offshore infrastructure. Global offshore energy production accounts for nearly 30% of total oil output, with more than 3,000 offshore platforms currently operating worldwide. Many of these facilities require specialized alloy components to ensure long operational life and structural reliability. Advanced corrosion resistant alloys used in subsea pipelines can extend service life by more than 25 years while reducing maintenance shutdowns by nearly 20%. Additionally, offshore wind energy installations are also driving demand for corrosion-resistant materials in turbine foundations and support structures, further expanding industrial applications for these alloys.

The manufacturing of corrosion resistant alloys involves complex metallurgical processes and expensive raw materials such as nickel, chromium, titanium, and molybdenum. These metals are often subject to supply fluctuations due to geopolitical factors and mining limitations, significantly increasing production costs. For instance, nickel prices experienced volatility exceeding 40% in recent years due to supply disruptions and rising demand from battery manufacturing sectors. Additionally, advanced alloy production requires specialized refining technologies including vacuum induction melting and electroslag remelting, which involve high energy consumption and specialized equipment. These manufacturing processes can increase production costs by nearly 25–35% compared to conventional carbon steel manufacturing. Small and mid-sized manufacturers often struggle to invest in these advanced facilities, limiting market participation. Furthermore, industries with tight capital budgets sometimes opt for lower-cost alternatives such as coated steel components, which can temporarily reduce demand for premium corrosion resistant alloys despite their long-term durability advantages.

The rapid expansion of hydrogen energy infrastructure presents significant opportunities for the Corrosion Resistant Alloys Market. Hydrogen production, storage, and transportation systems require materials capable of resisting hydrogen embrittlement and chemical corrosion. Advanced nickel-chromium and titanium alloys are increasingly used in electrolyzers, hydrogen pipelines, and high-pressure storage systems due to their exceptional resistance to chemical degradation. Global hydrogen production exceeded 95 million metric tons in 2024, with multiple countries investing in hydrogen fuel infrastructure to support energy transition goals. Hydrogen pipelines and storage tanks must withstand high-pressure environments, creating strong demand for corrosion-resistant materials capable of maintaining mechanical strength over long periods. New alloy compositions designed specifically for hydrogen applications have demonstrated resistance improvements of nearly 30% compared to traditional stainless steel grades. As more countries invest in hydrogen energy facilities, the demand for specialized corrosion resistant alloys is expected to increase significantly across energy and industrial sectors.

One of the major challenges facing the Corrosion Resistant Alloys Market is the stringent certification and quality requirements imposed by industries such as aerospace, nuclear energy, and petrochemical processing. These sectors require materials to meet strict mechanical performance and corrosion resistance standards before they can be used in critical applications. Certification processes often involve extensive laboratory testing, long approval timelines, and complex regulatory documentation. Testing procedures such as stress corrosion cracking evaluation, high-temperature oxidation testing, and chemical exposure analysis can extend product qualification timelines by 12–24 months. This slows down the introduction of new alloy compositions into commercial applications. Additionally, regulatory frameworks governing industrial safety and environmental compliance require manufacturers to maintain detailed traceability records for alloy materials used in critical infrastructure. Meeting these standards increases operational costs and slows the commercialization of innovative alloy technologies, creating barriers for smaller material developers attempting to enter the market.

• Rising adoption of advanced nickel-based superalloys in energy infrastructure: Industrial demand for nickel-chromium and nickel-molybdenum alloys has increased significantly due to their superior resistance to oxidation and high-temperature corrosion. In power generation and petrochemical processing facilities, nearly 42% of newly installed high-temperature components now utilize nickel-based corrosion resistant alloys. These alloys maintain structural stability at temperatures above 1000°C, extending equipment service life by nearly 30% compared with conventional stainless steel materials.

• Integration of additive manufacturing in alloy production: Additive manufacturing technologies are increasingly used to produce complex corrosion resistant alloy components with improved microstructural uniformity. More than 18% of advanced aerospace components now incorporate additively manufactured corrosion-resistant alloy parts, reducing production waste by 35% and improving manufacturing efficiency by 22%. The ability to design customized alloy structures is enabling new applications in turbine engines, chemical reactors, and offshore drilling equipment.

• Growing demand from offshore renewable energy infrastructure: Offshore wind and marine energy projects are accelerating the demand for corrosion resistant alloys used in turbine foundations, subsea cables, and structural support systems. Nearly 60% of offshore wind installations deployed after 2023 incorporate corrosion-resistant alloy coatings or structural components, reducing corrosion-related maintenance costs by 20% over long operational cycles.

• Increased use of nano-structured protective alloy coatings: Advanced nano-engineered coatings are improving corrosion protection across industrial equipment. Studies indicate that nano-coated alloy surfaces can improve corrosion resistance by 45% compared to conventional protective coatings. These technologies are gaining traction across marine shipping, chemical processing facilities, and desalination plants where prolonged exposure to aggressive chemical environments can rapidly degrade traditional metallic materials.

The Corrosion Resistant Alloys Market is segmented based on type, application, and end-user industries, reflecting the diverse industrial requirements for materials capable of withstanding aggressive environmental conditions. Different alloy compositions are engineered to address specific corrosion challenges such as high-temperature oxidation, chemical exposure, and marine corrosion. Type segmentation includes nickel-based alloys, stainless steel alloys, titanium alloys, and other specialty corrosion-resistant metals. Applications range across oil and gas infrastructure, marine engineering, aerospace components, power generation systems, and chemical processing equipment. End-user segmentation further highlights adoption patterns across energy companies, manufacturing industries, and infrastructure developers. Growing investments in offshore energy projects, advanced manufacturing, and sustainable infrastructure are strengthening demand across multiple segments, while technological improvements in metallurgy and alloy design are enabling enhanced performance characteristics tailored to specialized industrial environments.

Nickel-based corrosion resistant alloys represent the leading product type in the market, accounting for approximately 38% of global adoption due to their exceptional resistance to oxidation, high-temperature corrosion, and aggressive chemical exposure. These alloys are widely used in turbine engines, chemical processing equipment, and offshore oil and gas installations where material durability is essential. Stainless steel corrosion-resistant alloys follow with nearly 29% market adoption, supported by their cost-effectiveness and strong resistance to rust and pitting corrosion across industrial infrastructure. Titanium alloys are emerging as the fastest-growing type with an estimated CAGR of 6.2%, driven by increasing demand in aerospace, desalination plants, and biomedical applications. Titanium alloys offer a superior strength-to-weight ratio and can withstand highly corrosive chloride environments commonly encountered in marine operations. Other specialty alloys, including cobalt-based and aluminum-bronze alloys, collectively account for approximately 33% of the market, serving niche industrial applications requiring specific corrosion and wear resistance properties.

Oil and gas infrastructure represents the largest application segment, accounting for nearly 36% of market usage, due to the need for corrosion resistant alloys in pipelines, valves, drilling equipment, and offshore platforms exposed to corrosive environments. Marine engineering applications follow with approximately 22% adoption, supported by increasing shipbuilding activities and offshore renewable energy projects requiring durable metallic materials capable of withstanding saltwater exposure. Aerospace applications are the fastest-growing segment with an estimated CAGR of 6.5%, driven by rising aircraft production and increasing use of high-temperature corrosion resistant alloys in turbine engines and structural components. Aerospace manufacturers rely heavily on advanced nickel- and titanium-based alloys capable of maintaining strength under extreme heat and mechanical stress. Other applications including chemical processing equipment, desalination systems, and power generation infrastructure collectively contribute nearly 42% of overall demand, reflecting the widespread use of corrosion resistant alloys in industrial processing systems.

The energy sector represents the largest end-user segment, accounting for approximately 40% of total market demand, driven by the extensive use of corrosion resistant alloys in oil and gas extraction equipment, offshore drilling platforms, and power generation facilities. These materials are essential for maintaining structural integrity in high-pressure and chemically aggressive environments where conventional metals deteriorate rapidly. The aerospace and defense industry is the fastest-growing end-user segment with an estimated CAGR of 6.8%, fueled by increasing aircraft production and the need for high-performance materials capable of withstanding extreme operational conditions. Advanced corrosion resistant alloys are widely used in jet engines, turbine blades, and structural components where temperature resistance and durability are critical. Other key end-users include marine transportation, chemical manufacturing, and heavy industrial equipment producers, collectively accounting for nearly 60% of the remaining demand. Adoption rates are particularly high in the marine industry, where more than 70% of new offshore vessels incorporate corrosion resistant alloy components to improve operational longevity.

Region North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

North America maintains a strong position due to extensive industrial demand from aerospace manufacturing, petrochemical processing, and offshore oil production. The region operates more than 135 large refineries and over 900 chemical manufacturing facilities that require corrosion resistant alloys in reactors, pipelines, and heat exchangers to withstand aggressive chemical environments. Europe held nearly 27% of global demand in 2025, supported by strict industrial safety regulations and strong manufacturing bases in Germany, the United Kingdom, and France. Asia-Pacific represented close to 30% of global consumption with China producing more than 70 million metric tons of stainless and specialty alloy steel annually. Rapid infrastructure development across India and Southeast Asia is also increasing demand for corrosion resistant materials used in power plants, desalination systems, and industrial processing equipment. South America and the Middle East & Africa collectively accounted for approximately 9% of the market, driven by expansion in offshore oil projects, mining operations, and energy infrastructure modernization.

What industrial and technological factors are strengthening the demand for high-performance corrosion resistant alloys?

North America holds nearly 34% of the global Corrosion Resistant Alloys Market, driven primarily by large-scale adoption across aerospace, petrochemical processing, and offshore energy industries. The United States alone operates more than 135 oil refineries and a wide network of chemical production plants that require corrosion resistant alloys in pipelines, valves, reactors, and pressure vessels. Industrial regulations emphasizing safety and infrastructure durability have accelerated the adoption of high-performance alloys capable of resisting oxidation and chemical corrosion. Technological advancements such as additive manufacturing and advanced metallurgy simulation are increasingly used to develop stronger nickel-based and titanium alloys with improved durability in extreme environments. ATI Inc., a major regional alloy manufacturer, has expanded specialty alloy production to support aerospace turbine engine components designed to operate at temperatures exceeding 1000°C. Enterprise adoption patterns in this region indicate strong usage in aerospace, defense, and energy infrastructure where equipment reliability and long operational lifespans are critical requirements for industrial operators.

How are sustainability standards and industrial regulations influencing adoption of advanced corrosion resistant alloys?

Europe accounts for approximately 27% of the global Corrosion Resistant Alloys Market with major demand concentrated in Germany, the United Kingdom, France, and Italy. These countries collectively contribute more than 60% of the region’s industrial alloy processing capacity and rely heavily on corrosion resistant materials in automotive manufacturing, offshore energy systems, and chemical processing equipment. Strict environmental and safety regulations across the European Union require durable materials capable of preventing pipeline leaks and structural corrosion in industrial infrastructure. As a result, corrosion resistant alloys are widely used in offshore wind turbines, hydrogen processing plants, and chemical reactors operating in aggressive environments. Research institutions and advanced manufacturing facilities across Europe are also investing in nano-engineered alloy coatings capable of improving corrosion resistance by more than 40%. Outokumpu, a major European stainless steel manufacturer, has expanded corrosion resistant alloy production for chemical processing applications where high durability and environmental compliance are essential. Industrial users in this region prioritize materials that meet strict regulatory standards and support long-term sustainability goals.

What manufacturing and infrastructure trends are accelerating the adoption of corrosion resistant alloys in major industrial economies?

Asia-Pacific represents one of the largest production and consumption hubs for corrosion resistant alloys, accounting for nearly 30% of global demand. China, India, Japan, and South Korea are among the largest consuming markets due to rapid industrialization and large-scale infrastructure development. China produces more than 50 million metric tons of stainless and specialty alloy steel each year to support heavy manufacturing, energy infrastructure, and shipbuilding industries. Government investments in energy transmission pipelines, desalination plants, and offshore wind installations are significantly increasing the use of corrosion resistant materials across industrial sectors. Technological innovation centers in Japan and South Korea are also developing advanced titanium and nickel alloys designed for aerospace and marine engineering applications. Nippon Steel Corporation has introduced high-strength corrosion resistant steel used in offshore energy platforms capable of operating in harsh marine environments. Industrial demand patterns across this region are largely influenced by expanding manufacturing capacity, rapid urban infrastructure development, and increasing investment in large-scale energy and transportation projects.

How are natural resource industries influencing demand for corrosion resistant alloy materials in industrial infrastructure?

South America accounts for approximately 5% of the global Corrosion Resistant Alloys Market, with Brazil and Argentina representing the most significant national markets. Demand for corrosion resistant alloys in the region is primarily linked to offshore oil exploration, mining operations, and industrial infrastructure development. Brazil operates more than 15 offshore oil production hubs in deepwater environments where pipelines and drilling equipment require specialized alloys capable of resisting saltwater corrosion and high-pressure conditions. Mining operations across the region also rely on corrosion resistant materials to protect processing equipment exposed to abrasive and chemically aggressive environments. Government initiatives supporting domestic energy production and natural resource extraction are further driving industrial demand for durable alloy materials. Brazilian steel producer Gerdau has expanded specialty alloy production to support heavy industrial infrastructure projects and energy facilities. Industrial consumption patterns in the region are closely connected to oil production, mining development, and infrastructure modernization across major economies.

How are large-scale energy and industrial infrastructure projects increasing the use of corrosion resistant alloys?

The Middle East & Africa region represents nearly 4% of the global Corrosion Resistant Alloys Market, with demand largely driven by oil and gas production, petrochemical processing, and large-scale infrastructure development. Countries such as the United Arab Emirates, Saudi Arabia, and South Africa are major industrial markets due to their extensive energy production and refining sectors. The region operates more than 250 large oil and gas processing facilities that require corrosion resistant alloys in pipelines, storage systems, and high-pressure processing equipment to prevent structural degradation caused by chemical exposure and high temperatures. Industrial modernization programs are encouraging energy companies to adopt advanced corrosion monitoring technologies and high-performance alloy materials to extend infrastructure lifespans. ArcelorMittal South Africa produces specialized corrosion resistant steels used in mining and energy processing equipment operating under harsh environmental conditions. Industrial purchasing patterns in this region reflect strong demand from oil producers, petrochemical companies, and infrastructure developers seeking durable materials capable of operating in extreme environments.

• United States – 28% market share – The United States leads the Corrosion Resistant Alloys Market due to its advanced aerospace manufacturing sector, extensive petrochemical infrastructure, and strong investment in specialty alloy production technologies.

• China – 24% market share – China maintains a dominant position in the Corrosion Resistant Alloys Market through large-scale stainless steel and specialty alloy manufacturing capacity supporting energy, infrastructure, and heavy industrial sectors.

The Corrosion Resistant Alloys Market demonstrates a moderately consolidated competitive structure with a combination of large global alloy manufacturers and regional specialty metal producers. More than 80 active alloy manufacturing companies operate across global markets, supplying high-performance materials to industries including aerospace, energy, marine engineering, and chemical processing. The top five companies collectively account for approximately 42% of the global competitive landscape, supported by advanced metallurgical expertise and large production capacities.

Competition within the market is primarily driven by product innovation, expansion of advanced manufacturing facilities, and strategic partnerships with major industrial end-users. Manufacturers are investing heavily in technologies such as additive manufacturing, powder metallurgy, and nano-engineered alloy coatings to improve corrosion resistance and extend the durability of industrial equipment. Since 2023, more than 1.5 billion USD has been invested globally in specialty alloy production facility upgrades and materials research initiatives. Vertical integration strategies are also becoming increasingly important as companies seek to secure raw material supplies such as nickel, chromium, and molybdenum used in corrosion resistant alloy production. Strategic supply agreements with aerospace manufacturers and energy companies allow major producers to maintain long-term industrial contracts while supporting the development of next-generation corrosion resistant materials designed for high-temperature and chemically aggressive operating environments.

Allegheny Technologies Incorporated

Carpenter Technology Corporation

Haynes International Inc.

Nippon Steel Corporation

Outokumpu Oyj

Sandvik AB

ArcelorMittal

Aperam S.A.

Voestalpine AG

Thyssenkrupp AG

Sumitomo Metal Mining Co. Ltd.

Hitachi Metals Ltd.

Technological innovation in the Corrosion Resistant Alloys Market is being driven by advances in metallurgical engineering, computational materials science, and precision manufacturing. One of the most impactful developments is the increasing use of additive manufacturing technologies to produce complex alloy components with improved corrosion resistance and microstructural uniformity. Additive manufacturing enables manufacturers to reduce material waste by nearly 30% while producing intricate structures for aerospace turbines, chemical reactors, and offshore drilling components that are difficult to fabricate using traditional machining methods.

Another important technological advancement involves the development of nano-structured alloy coatings designed to improve corrosion resistance under extreme environmental conditions. These coatings incorporate nanoscale particles that create highly dense protective layers on alloy surfaces, improving resistance to pitting corrosion and oxidation by as much as 40% compared to conventional coatings. Such technologies are increasingly used in marine infrastructure, desalination plants, and petrochemical processing facilities where long-term exposure to aggressive chemicals is common.

Computational alloy design and artificial intelligence are also transforming the way corrosion resistant alloys are developed. Advanced simulation software allows researchers to model thousands of alloy compositions digitally before physical production, reducing development time by more than 35%. Machine learning algorithms can analyze complex microstructural data to optimize alloy compositions containing elements such as chromium, molybdenum, and nickel, enhancing resistance to chemical corrosion and high-temperature degradation.

High-performance processing technologies including vacuum induction melting and electroslag remelting are also improving alloy purity and structural integrity. These processes remove impurities from molten metals and refine grain structures, resulting in alloys capable of maintaining mechanical strength and corrosion resistance even in environments exceeding 900°C. As industries continue to demand durable materials for energy infrastructure, aerospace components, and chemical processing equipment, these technological advancements are expected to play a central role in improving alloy performance and operational reliability.

• In March 2025, Outokumpu announced the expansion of its corrosion-resistant stainless steel production capacity at its Tornio facility in Finland. The investment focuses on advanced duplex and super-duplex stainless steels designed for offshore wind energy and chemical processing equipment requiring enhanced corrosion resistance. Source: www.outokumpu.com

• In September 2024, Sandvik Materials Technology launched a new high-performance nickel alloy developed for hydrogen energy infrastructure. The alloy demonstrates improved resistance to hydrogen embrittlement and is designed for use in hydrogen pipelines, storage systems, and electrolyzer components.

• In November 2024, Carpenter Technology Corporation introduced an advanced corrosion-resistant alloy engineered for aerospace turbine components. The new material offers improved oxidation resistance at temperatures exceeding 1000°C and is optimized for next-generation aircraft engine applications. Source: www.carpentertechnology.com

• In February 2025, Allegheny Technologies Incorporated expanded its specialty alloy manufacturing capabilities at its advanced materials facility in Pennsylvania. The upgrade includes new vacuum induction melting equipment designed to produce high-purity corrosion-resistant alloys for aerospace and energy sector applications.

The Corrosion Resistant Alloys Market Report provides a comprehensive analysis of global industry dynamics, technological developments, and evolving demand across key industrial sectors. The report evaluates multiple alloy types including nickel-based alloys, stainless steel alloys, titanium alloys, and other specialty corrosion resistant materials designed for extreme environmental conditions. These materials are widely used in high-performance industrial applications requiring resistance to chemical corrosion, high-temperature oxidation, and marine degradation.

The report covers a broad range of application sectors including oil and gas extraction, offshore energy infrastructure, aerospace and defense manufacturing, marine engineering, chemical processing equipment, and power generation systems. These industries rely heavily on corrosion resistant alloys to ensure operational reliability, extend equipment lifespan, and reduce maintenance costs in aggressive environments. For instance, offshore energy facilities often require alloy materials capable of withstanding saltwater corrosion and high-pressure operating conditions for more than 20 years.

Geographically, the report analyzes market activity across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. The study includes insights into industrial production capacity, infrastructure investments, and technology adoption patterns across major economies such as the United States, China, Germany, Japan, and India. Asia-Pacific is highlighted as a major manufacturing hub for specialty alloys due to strong steel production capacity and expanding industrial infrastructure projects.

In addition to core market segments, the report also examines emerging areas such as advanced additive manufacturing for alloy components, nano-engineered corrosion protection technologies, and materials designed for hydrogen energy infrastructure. These technologies are expected to influence the future development of corrosion resistant alloys used in energy transition systems, aerospace engineering, and high-performance industrial equipment. The scope also includes competitive landscape analysis, key company strategies, and technological innovation trends shaping the global corrosion resistant alloys industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Allegheny Technologies Incorporated, Carpenter Technology Corporation, Haynes International Inc., Nippon Steel Corporation, Outokumpu Oyj, Sandvik AB, ArcelorMittal, Aperam S.A., Voestalpine AG, Thyssenkrupp AG, Sumitomo Metal Mining Co. Ltd., Hitachi Metals Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |