Reports

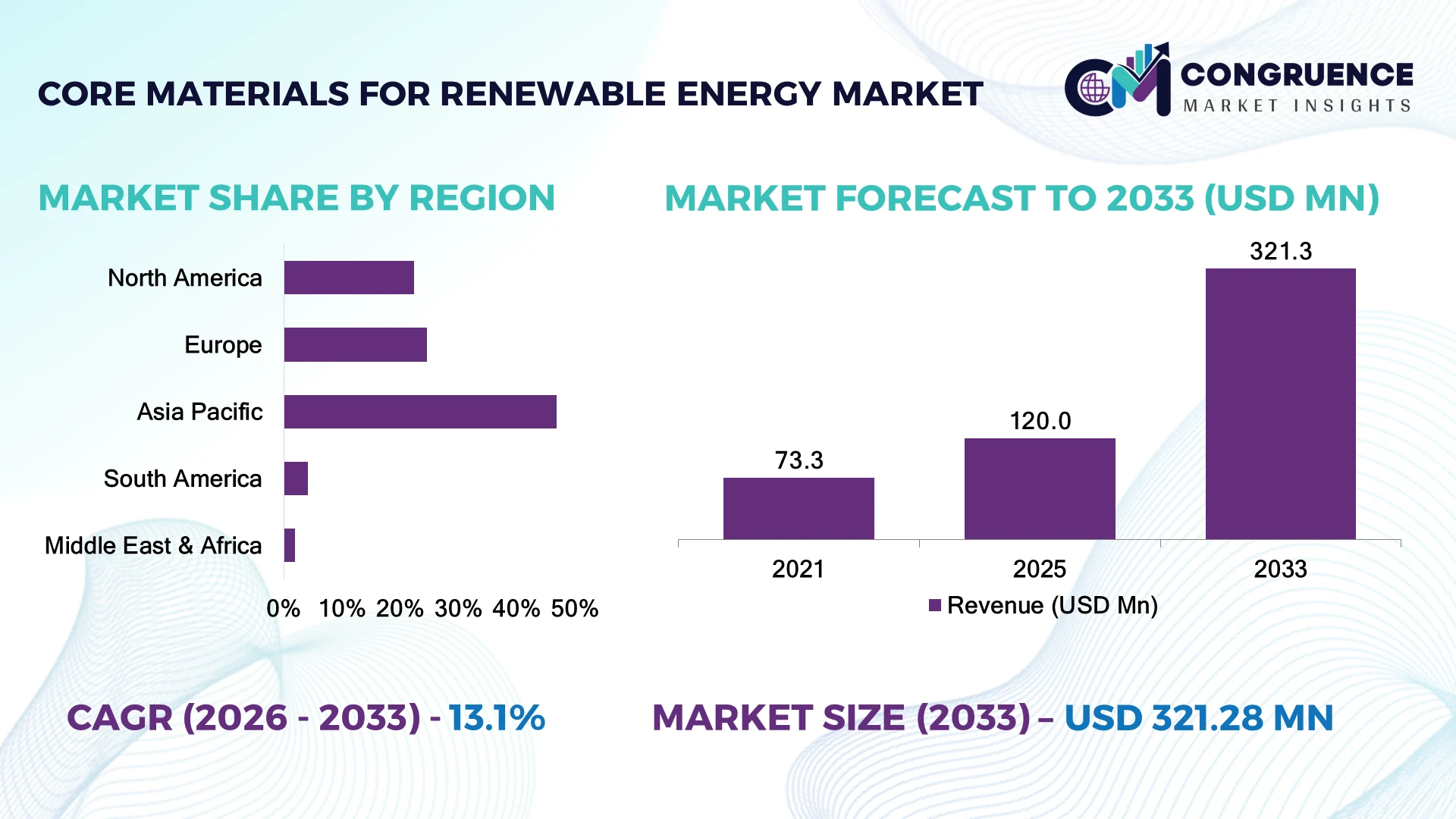

The Global Core Materials for Renewable Energy Market was valued at USD 120.0 Million in 2025 and is anticipated to reach a value of USD 321.3 Million by 2033 expanding at a CAGR of 13.1% between 2026 and 2033. Rising deployment of larger offshore wind turbines and lightweight composite blade architectures is accelerating the adoption of high-performance foam and balsa core materials across renewable energy manufacturing.

China dominates the market with approximately 38% of global renewable energy core material consumption, supported by more than 430 GW of installed wind capacity, continuous investments in composite manufacturing, and large-scale blade production facilities. In comparison, Germany emphasizes advanced recyclable composite technologies for offshore projects, while China's production capacity remains over 3× larger, strengthening its leadership in industrial-scale deployment and material innovation.

This competitive landscape reinforces the importance of localized manufacturing, resilient raw material sourcing, and advanced composite technologies for long-term strategic positioning.

Market Size & Growth: USD 120.0 Million in 2025, projected to reach USD 321.3 Million by 2033 at 13.1% CAGR, supported by expanding offshore wind blade manufacturing and advanced composite adoption.

Top Growth Drivers: Offshore wind installations (+22%), recyclable composite adoption (+18%), and lightweight blade engineering (+15%) continue to reshape industry demand.

Short-Term Forecast: By 2028, composite processing waste is expected to decline by nearly 20% through automated manufacturing and optimized material utilization.

Emerging Technologies: Automated resin infusion, recyclable PET foam cores, and AI-enabled quality inspection are improving manufacturing precision and production efficiency.

Regional Leaders: Asia Pacific approaches USD 145 Million, Europe exceeds USD 92 Million, and North America reaches nearly USD 56 Million, supported by offshore expansion and localized supply chains.

Consumer/End-User Trends: More than 62% of next-generation wind blade manufacturers are integrating lightweight structural core materials to improve turbine efficiency.

Pilot/Case Example: In 2024, offshore wind blade production programs using recyclable PET core materials reduced manufacturing waste by approximately 18%.

Competitive Landscape: The top five manufacturers collectively account for nearly 55% market share, led by DIAB Group alongside Gurit, 3A Composites, Armacell, and Evonik.

Regulatory & ESG Impact: European sustainability regulations have increased recyclable composite adoption by nearly 24% across new renewable energy component manufacturing.

Investment & Funding: More than USD 1.8 Billion has been invested globally in composite manufacturing expansion, driven by strategic partnerships and regional production facilities.

Innovation & Future Outlook: Advanced recyclable sandwich structures, digital production monitoring, and bio-based core materials are strengthening next-generation renewable energy manufacturing competitiveness.

Core Materials for Renewable Energy Market continues to expand through offshore wind blade manufacturing, floating renewable platforms, and lightweight structural applications. Manufacturers are introducing recyclable PET foam cores, automated composite processing, and digital inspection technologies that improve production consistency. More than 60% of newly designed offshore blades incorporate advanced core materials, while regional supply-chain localization is becoming a strategic priority amid evolving trade and manufacturing policies.

The Core Materials for Renewable Energy Market has become strategically important as renewable infrastructure developers prioritize lightweight, durable, and recyclable composite structures for next-generation wind energy systems. Supply-chain diversification, regional manufacturing expansion, and renewable infrastructure modernization are reshaping competitive dynamics. Companies are increasingly establishing localized production facilities to improve delivery reliability while reducing dependence on long-distance raw material sourcing.

Modern PET and high-performance PVC foam cores provide approximately 15–20% lower structural weight than several conventional alternatives while maintaining comparable mechanical performance, enabling longer wind turbine blades and improved operational efficiency. Asia Pacific continues to lead in production scale through integrated composite manufacturing, whereas Europe remains at the forefront of recyclable material innovation and offshore deployment technologies. Over the next two to three years, automated composite processing and digital quality inspection are expected to become standard across large manufacturing facilities.

Manufacturers are expanding partnerships with wind turbine OEMs to accelerate development of recyclable composite solutions and optimize production efficiency. Several offshore wind projects have already integrated advanced foam core structures to improve blade durability and reduce lifecycle maintenance requirements. Organizations that combine localized manufacturing, sustainable material innovation, and advanced production technologies will strengthen competitive positioning while supporting long-term renewable energy infrastructure development.

The transition toward larger offshore wind turbines is significantly increasing demand for lightweight structural core materials capable of improving blade stiffness while minimizing weight. More than 70% of newly installed offshore turbines now exceed 8 MW capacity, while blade lengths have expanded by over 35% during the past decade, requiring higher-performance PVC and PET foam solutions. China's expanding offshore wind manufacturing ecosystem and the European Union's renewable energy deployment targets continue to reshape supplier investment priorities. This shift improves turbine efficiency, lowers transportation complexity, and extends operational life. Leading manufacturers are expanding automated composite production, establishing localized foam processing facilities, and forming long-term partnerships with turbine OEMs. A key strategic advantage lies in vertically integrated manufacturing that strengthens supply security while shortening production lead times.

The market continues to face structural constraints from dependence on petrochemical feedstocks and specialty balsa wood supplies, exposing manufacturers to raw material volatility. PVC resin prices have experienced fluctuations exceeding 20% during recent supply disruptions, while transportation expenses for imported composite materials have increased by nearly 18% in several manufacturing corridors. Ecuador remains a primary global supplier of structural balsa, creating procurement concentration risks for wind blade producers. These pressures directly affect production planning, operating margins, and contract execution for composite manufacturers. Companies are responding by qualifying alternative PET foam materials, securing multi-year procurement agreements, and expanding localized manufacturing facilities. Diversified sourcing strategies are becoming essential for maintaining production continuity and improving commercial resilience.

Growing investment in recyclable composite technologies is opening new commercial opportunities beyond conventional wind blade manufacturing. More than 40% of new material development programs now prioritize recyclable thermoplastic core structures, while automated composite manufacturing has improved material utilization by approximately 18%. Germany continues to accelerate circular economy initiatives through advanced composite recycling infrastructure, encouraging broader industrial adoption of sustainable structural materials. Manufacturers are investing in bio-based foam technologies, digital production monitoring, and collaborative research partnerships with turbine developers. An emerging opportunity exists in supplying lightweight structural cores for floating offshore wind platforms, where improved durability and reduced maintenance requirements deliver measurable operational advantages throughout long-term infrastructure deployment.

Maintaining consistent product quality across rapidly expanding composite manufacturing networks remains a major execution challenge. Manufacturing defects can account for nearly 12% of blade quality deviations when production parameters are not tightly controlled, while skilled composite technicians remain in limited supply across several industrial hubs. The United States and several European manufacturers continue investing in automated inspection systems to improve process reliability for increasingly complex blade structures. Inconsistent production quality affects certification timelines, deployment schedules, and long-term asset performance. Companies must strengthen digital manufacturing, workforce development, robotic inspection, and standardized production protocols to ensure scalable, repeatable manufacturing while preserving competitiveness in next-generation renewable energy infrastructure.

Recyclable Foam Materials Expand Recyclable PET foam continues replacing conventional structural cores as manufacturers target circular production models. Nearly 34% of newly developed composite blade programs now incorporate recyclable foam structures, while production scrap has declined by approximately 18% through optimized processing. European sustainability regulations and OEM procurement standards are accelerating adoption. Companies are expanding recyclable material portfolios, investing in closed-loop manufacturing, and restructuring sourcing strategies to improve compliance while reducing lifecycle environmental impact.

Automation Reshapes Composite Manufacturing Automated resin infusion, robotic trimming, and AI-enabled inspection systems are transforming production workflows. Composite manufacturing cycle times have improved by nearly 20%, while inspection accuracy exceeds 95% in digitally monitored facilities. Labor shortages in Germany and the United States continue driving automation investments. Manufacturers are integrating digital quality management platforms and predictive production analytics to improve throughput, minimize defects, and maintain consistent structural performance across large-scale blade manufacturing.

Localized Supply Networks Strengthen Renewable energy manufacturers are increasingly regionalizing supply chains to reduce logistics risk and procurement delays. Average material lead times have declined by approximately 16%, while local sourcing has increased by nearly 24% across strategic production hubs. Geopolitical trade uncertainty and shipping disruptions have accelerated this transition. Companies are establishing regional foam processing plants, expanding supplier partnerships, and qualifying multiple raw material sources to improve manufacturing continuity and operational resilience.

Larger Turbine Platforms Emerge Wind turbine platforms exceeding 12 MW are accelerating demand for higher-strength lightweight sandwich structures capable of supporting longer blades. Structural core thickness requirements have increased by nearly 22%, while advanced composite utilization has expanded by approximately 28% across offshore projects. Chinese blade manufacturers are redesigning production processes for larger platforms. Material suppliers are introducing customized high-density foam grades and collaborative engineering programs to optimize blade durability, transportation efficiency, and lifecycle performance.

PET Foam holds the leading position with approximately 36% of the market, supported by its excellent strength-to-weight ratio, recyclability, and compatibility with automated composite manufacturing. Wind blade manufacturers increasingly prefer PET foam because it combines structural performance with sustainability objectives while reducing production waste. PVC Foam remains widely adopted for its established processing characteristics and cost competitiveness, whereas Balsa Wood continues serving premium structural applications requiring superior stiffness despite supply concentration risks. SAN Foam represents the fastest-growing segment as offshore wind projects increasingly require improved fatigue resistance and higher thermal stability for larger blade architectures. PMI Foam continues gaining traction in specialized high-performance applications where weight optimization is critical, while the Others category supports customized engineering solutions for niche renewable energy systems. Manufacturers are expanding recyclable foam production, introducing higher-density material grades, and strengthening strategic partnerships with turbine OEMs. Approximately 42% of newly qualified blade materials now emphasize recyclability alongside structural performance, reflecting shifting procurement priorities toward sustainable composite technologies.

Wind Energy accounts for approximately 72% of total demand as modern turbine blades require lightweight sandwich structures capable of supporting greater blade lengths and higher mechanical loads. Larger offshore installations continue increasing consumption of advanced core materials to improve stiffness, durability, and operational efficiency. Solar Energy maintains steady demand through lightweight mounting structures and composite panel applications, while Hydropower utilizes structural cores in selected composite infrastructure components requiring corrosion resistance. Tidal & Wave Energy represents the fastest-growing application as governments invest in marine renewable demonstration projects requiring durable composite materials capable of withstanding harsh operating environments. The Others category includes emerging renewable technologies adopting advanced structural composites for specialized engineering applications. Material suppliers are expanding application-specific product portfolios, investing in engineering support services, and collaborating with renewable equipment manufacturers. Nearly 30% of advanced composite development projects now target offshore renewable applications beyond conventional wind energy, highlighting diversification across renewable infrastructure.

Wind Turbine Manufacturers represent the largest end-user group with approximately 61% market share, reflecting their continuous demand for lightweight structural materials used in larger rotor blade production. High manufacturing volumes, advanced composite integration, and ongoing blade redesign programs maintain this segment's leadership. Renewable Energy Developers remain important buyers by specifying advanced materials during project procurement, while EPC Companies increasingly influence material selection through engineering optimization and construction efficiency requirements. Renewable Energy Developers constitute the fastest-growing end-user segment as offshore wind and integrated renewable infrastructure projects expand across China, the United Kingdom, and the United States. Utilities continue strengthening procurement standards for durable composite components supporting long-term asset reliability, while the Others segment includes research organizations and specialized renewable equipment manufacturers. Companies are responding through customized engineering services, long-term supply agreements, and collaborative product qualification programs. More than 48% of strategic supplier partnerships now include joint material development initiatives that shorten product qualification cycles and improve deployment readiness.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

North America represents approximately 22.4% of the global market, supported by expanding domestic composite manufacturing, offshore wind development, and increasing localization of renewable energy supply chains. The United States continues investing in advanced blade manufacturing and automated composite processing to reduce dependence on imported structural materials. Large turbine manufacturers are strengthening partnerships with foam core suppliers to improve production reliability and shorten procurement cycles. More than 30% of newly commissioned blade manufacturing capacity now incorporates automated inspection technologies that enhance product consistency and operational efficiency. Public infrastructure initiatives and industrial decarbonization programs continue encouraging renewable manufacturing investments, while regional producers prioritize recyclable composite materials to meet evolving sustainability expectations and long-term procurement requirements.

United States Market Outlook: The United States remains the regional leader through large-scale wind energy deployment, advanced composite manufacturing capability, and expanding domestic supply-chain investments. Offshore wind projects along the Atlantic coast continue increasing demand for lightweight structural core materials, while manufacturing facilities are adopting digital production technologies to improve quality consistency. More than 150 GW of installed wind power supports continuous material demand, and manufacturers are expanding partnerships with domestic suppliers to strengthen localized production and reduce logistics-related risks.

Europe accounts for approximately 24.6% of global demand, supported by advanced offshore wind deployment, strict sustainability regulations, and continuous innovation in recyclable composite materials. Countries across the region are investing in next-generation blade technologies that prioritize recyclable foam cores and efficient manufacturing processes. Collaborative development between material suppliers and turbine OEMs has accelerated commercialization of circular composite solutions. More than 35% of recently commissioned blade production lines now integrate digital quality monitoring systems that improve manufacturing precision and reduce material waste. Industrial modernization, renewable energy targets, and coordinated supply-chain investments continue strengthening Europe's competitive position in advanced structural composite technologies.

Germany Market Outlook: Germany leads the European market through strong engineering expertise, advanced composite manufacturing, and continued investment in offshore wind infrastructure. Domestic research institutions and industrial manufacturers are accelerating development of recyclable sandwich structures for next-generation turbine blades. More than 65 GW of installed wind capacity supports continuous innovation, while collaborative projects between material suppliers and turbine manufacturers reinforce Germany's position as a leading technology and manufacturing hub.

Asia-Pacific leads the global market with approximately 46.8% share, driven by extensive composite manufacturing capacity, integrated renewable energy supply chains, and large-scale wind turbine production. China, India, and South Korea continue expanding production infrastructure to support growing domestic and export demand. Manufacturers are increasing automation, optimizing material processing, and investing in high-volume foam core production to improve competitiveness. More than 55% of global wind blade manufacturing capacity is concentrated within the region, enabling efficient large-scale deployment and strong export performance. Regional enterprises continue expanding vertically integrated manufacturing models that improve operational flexibility and strengthen supply-chain resilience.

China Market Outlook: China remains the dominant country through its extensive wind turbine manufacturing ecosystem, integrated composite supply chain, and large domestic renewable deployment pipeline. Major manufacturers continue expanding advanced foam production facilities while investing in automated composite processing technologies. Installed wind capacity exceeding 430 GW and continuous offshore project development sustain long-term demand, enabling Chinese suppliers to strengthen both domestic market leadership and international export competitiveness.

South America represents approximately 4.2% of the global market, supported primarily by expanding onshore wind developments and increasing investment in renewable infrastructure. Brazil continues strengthening regional demand through utility-scale wind projects and localized renewable manufacturing initiatives. Although composite material production remains comparatively limited, international suppliers are expanding commercial partnerships to improve regional product availability. Wind project installations continue encouraging adoption of lightweight structural materials that enhance turbine performance and reduce maintenance requirements. Infrastructure constraints and imported raw material dependence remain operational challenges, yet growing industrial investment and improving logistics networks are gradually enhancing regional manufacturing capability.

Brazil Market Outlook: Brazil leads regional demand through extensive wind resource development and continuous renewable infrastructure expansion. The country's northeastern states remain major centers for wind energy deployment, supporting increasing procurement of advanced composite materials for turbine manufacturing. Installed wind capacity exceeding 37 GW continues attracting international investment, while equipment manufacturers are strengthening regional partnerships to improve supply reliability and technical support for large renewable energy projects.

The Middle East & Africa accounts for approximately 2.0% of global demand, with renewable diversification strategies and infrastructure modernization supporting gradual market expansion. Gulf countries are integrating renewable energy into long-term industrial strategies while increasing procurement of advanced composite components for utility-scale projects. International partnerships continue improving regional access to specialized structural materials and engineering expertise. Several renewable developments exceeding 1 GW capacity are encouraging broader adoption of advanced composite technologies across emerging projects. Although manufacturing remains limited, governments continue supporting industrial diversification through localized production initiatives, technology transfer agreements, and infrastructure investment programs.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's most strategically significant market through ambitious renewable deployment targets, industrial diversification initiatives, and large infrastructure investments. Utility-scale renewable projects are increasing demand for advanced structural materials, while international partnerships are strengthening local engineering capability. Renewable energy programs targeting more than 50 GW of installed capacity are encouraging greater localization of manufacturing activities and long-term investment in advanced composite technologies.

The market is led by DIAB Group, Gurit, Armacell, 3A Composites, and Evonik, competing directly with regional composite material manufacturers and specialized foam suppliers for renewable energy contracts. The top five players collectively control approximately 56% of the market, creating a moderately consolidated structure. Competition centers on lightweight material performance, manufacturing scale, supply-chain reliability, and customized engineering rather than price alone. Advanced recyclable core materials improve production efficiency by nearly 18%, while automated quality inspection reduces manufacturing defects by approximately 15%. Companies are expanding regional production facilities, signing long-term supply agreements with wind turbine OEMs, investing in recyclable PET foam technologies, and strengthening vertical integration to secure raw material availability. Competitive momentum is shifting toward sustainable composite innovation and localized manufacturing as customers prioritize resilient procurement. High qualification standards, material certification requirements, and specialized processing expertise remain major entry barriers. Winning requires scalable manufacturing, proven engineering capability, localized supply resilience, and continuous material innovation.

Gurit Holding AG

Armacell International S.A.

3A Composites

Evonik Industries AG

Changzhou Tiansheng New Materials Co., Ltd.

SABIC

CoreLite Inc.

Airex AG

DIAB North America

Carbon-Core Corporation

JSP Corporation

Advanced recyclable PET foam, high-performance SAN foam, and digital composite manufacturing are redefining structural core material production. Automated resin infusion and robotic trimming have improved production efficiency by nearly 20%, while AI-enabled inspection systems reduce quality deviations by approximately 15%. More than 45% of newly commissioned blade manufacturing lines now integrate automated quality monitoring, allowing manufacturers to increase consistency while lowering material waste and production delays.

Compared with conventional PVC-focused manufacturing, recyclable PET core technologies deliver approximately 18% better material utilization and improved end-of-life recyclability without compromising structural performance. Digital twin platforms and predictive process monitoring are enabling manufacturers to optimize curing cycles and reduce rework requirements. Global wind turbine OEMs and advanced composite suppliers benefit most from these technologies through faster product qualification, improved operational reliability, and stronger compliance with evolving sustainability requirements.

Between 2026 and 2028, greater adoption of bio-based structural cores, automated composite inspection, and closed-loop recycling technologies will strengthen competitive differentiation. Manufacturers investing in smart production systems, advanced material engineering, and collaborative product development will improve supply resilience, accelerate innovation cycles, and secure long-term positions in next-generation renewable energy infrastructure markets.

September 2024 – Evonik Industries AG announced that ROHACELL® high-performance foam production at its Darmstadt, Germany facility now operates using 100% renewable electricity, reducing annual CO₂ emissions by approximately 3,400 metric tons. The initiative strengthens the sustainability profile of lightweight structural foam supplied to advanced composite applications, including renewable energy. Source: www.evonik.com

2024 (Sustainability Update) – Gurit Holding AG reported that its PET structural core business recycled 891 million post-consumer PET bottles and 10,890 tonnes of PET waste from its own operations. Gurit's PET core materials, manufactured with up to 100% recycled PET, support lower-carbon composite structures for renewable energy applications. Source: www.gurit.com

September 2025 – Armacell International S.A. released its 2024 Sustainability Report, highlighting continued progress in environmental performance and engineered foam solutions, with expanded ESG measurement and reporting across global operations. The update reinforces Armacell's strategic focus on lightweight engineered foams supporting energy-efficient and renewable applications.

2025 (Product Portfolio Update) – DIAB Group expanded the commercial positioning of its Divinycell® PET portfolio, emphasizing recyclable PET foam cores produced from post-consumer and post-industrial recycled PET for wind energy and other composite markets. The enhanced portfolio improves processing efficiency, dimensional stability, and circular-material adoption across renewable energy manufacturing. Source: www.diabgroup.com

This report delivers comprehensive analysis of the Core Materials for Renewable Energy Market across PVC Foam, PET Foam, Balsa Wood, SAN Foam, PMI Foam, and Other structural core materials. It evaluates demand across wind energy, solar energy, hydropower, tidal and wave energy, and additional renewable applications while assessing procurement trends among wind turbine manufacturers, renewable energy developers, EPC companies, utilities, and other end users. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational, manufacturing, and technology assessments.

The study examines advanced recyclable composites, automated manufacturing, digital quality inspection, and lightweight structural engineering, highlighting adoption patterns exceeding 45% across modern blade production. It evaluates competitive positioning, deployment priorities, supply-chain resilience, investment direction, and enterprise strategies between 2026 and 2033. Strategic insights help stakeholders identify expansion opportunities, benchmark competitors, optimize sourcing decisions, strengthen manufacturing capabilities, and align product development with evolving renewable energy infrastructure requirements.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 120.0 Million |

| Market Revenue (2033) | USD 321.3 Million |

| CAGR (2026–2033) | 13.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | DIAB Group; Gurit Holding AG; Armacell International S.A.; 3A Composites; Evonik Industries AG; Changzhou Tiansheng New Materials Co., Ltd.; SABIC; CoreLite Inc.; Airex AG; JSP Corporation; Carbon-Core Corporation; Gurit Services AG |

| Customization & Pricing | Available on Request (10% Customization Free) |