Reports

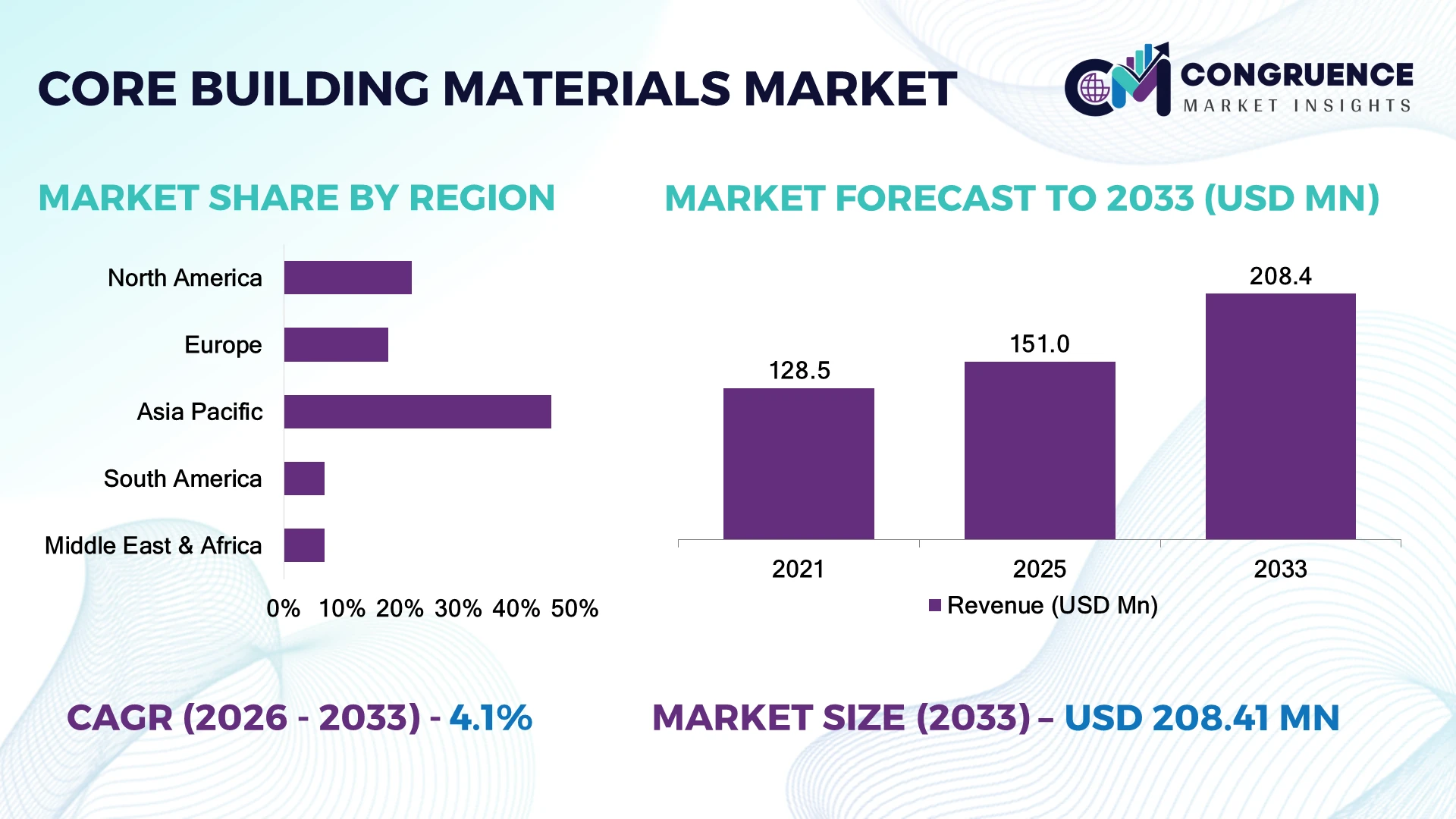

The Global Core Building Materials Market was valued at USD 151.0 Million in 2025 and is anticipated to reach a value of USD 208.4 Million by 2033 expanding at a CAGR of 4.11% between 2026 and 2033. Growth is driven by low-carbon cement innovation, automated manufacturing, recycled construction inputs, and rising investments in resilient infrastructure projects.

China dominates the core building materials landscape with over 35% of global cement production capacity and extensive infrastructure modernization programs, while India follows with more than 8% cement capacity share and rapid urban construction expansion. China’s Belt and Road Initiative continues supporting material demand across emerging economies, whereas India’s smart city and industrial corridor projects are accelerating adoption of advanced construction solutions. North America prioritizes sustainable materials, with green building adoption exceeding 40% in major commercial developments. These regional differences are reshaping supplier strategies, technology investments, and global production networks.

Companies that align material innovation with sustainability targets and regional infrastructure priorities gain a stronger competitive advantage in the evolving construction ecosystem.

Market Size & Growth: Valued at USD 151.0 Million in 2025 and projected at USD 208.4 Million by 2033, driven by low-carbon materials and automated production systems.

Top Growth Drivers: Green construction adoption (40%+), infrastructure investment growth (35%+), and recycled material utilization (25%+).

Short-Term Forecast: By 2028, digital manufacturing adoption improves production efficiency by 15% and reduces material waste by 10%.

Emerging Technologies: AI-based material optimization, robotic construction systems, and advanced composite building materials are transforming operations.

Regional Leaders: Asia Pacific leads with infrastructure expansion; North America advances sustainable materials; Europe accelerates circular construction practices.

Consumer/End-User Trends: Over 45% of commercial developers prioritize energy-efficient and sustainable construction materials.

Pilot/Case Example: 2024 automated concrete manufacturing projects achieved nearly 20% reduction in material waste and improved production consistency.

Competitive Landscape: Leading suppliers including Holcim, CEMEX, Heidelberg Materials, and Saint-Gobain compete through sustainable product portfolios.

Regulatory & ESG Impact: Carbon reduction policies are pushing manufacturers toward solutions that lower construction emissions by 20%–30%.

Investment & Funding: More than USD 100 billion is directed toward global infrastructure modernization, supporting advanced material expansion and partnerships.

Innovation & Future Outlook: Next-generation materials, circular supply chains, and digital construction platforms are redefining long-term industry competitiveness.

The Core Building Materials Market is witnessing stronger demand for sustainable cement alternatives, lightweight composites, and digitally monitored construction materials. Advanced production technologies are enabling manufacturers to reduce waste and improve resource efficiency, with recycled material usage increasing by nearly 25% across developed markets. Supply-chain diversification following global logistics disruptions and stricter environmental regulations are encouraging companies to localize production, develop low-emission products, and expand partnerships across emerging construction hubs.

The Core Building Materials Market is becoming strategically important as infrastructure modernization, decarbonization goals, and construction technology transformation reshape global competition. Manufacturers are moving beyond traditional materials toward low-emission cement, engineered composites, and digitally optimized production systems to improve cost control and environmental performance.

Supply-chain restructuring and stricter carbon regulations are accelerating investments in regional manufacturing capabilities. Automated production facilities deliver measurable advantages over conventional systems, reducing material waste by approximately 15%–20% while improving operational consistency. In comparison, traditional construction material processes rely more heavily on manual quality controls and higher resource consumption.

Asia Pacific maintains the largest deployment scale due to urban expansion and infrastructure programs, while Europe leads innovation through circular construction models and carbon reduction initiatives. North America continues increasing adoption of smart construction technologies, supported by commercial redevelopment projects.

Companies are expanding partnerships with technology providers, investing in recycling facilities, and upgrading production networks to meet evolving demand. For example, automated concrete batching and digital monitoring systems are improving project efficiency across large infrastructure developments. Strategic positioning in sustainable materials, regional supply resilience, and advanced manufacturing capabilities will determine long-term market leadership.

The shift toward sustainable construction is accelerating demand for low-carbon cement, recycled aggregates, and advanced composite materials, with green building adoption exceeding 40% in major commercial projects. China’s infrastructure renewal programs and India’s industrial corridor developments are increasing demand for high-performance materials, while manufacturers are investing heavily in energy-efficient production systems. Companies are expanding alternative fuel usage, digital quality monitoring, and carbon-reduction technologies to address stricter environmental standards. Cement producers implementing renewable energy integration have achieved operational emission reductions of 15%–25%, creating cost advantages while improving compliance readiness. The strategic focus is moving from volume production toward resource-efficient material ecosystems.

Core building material manufacturers face persistent challenges from fluctuating energy costs, raw material dependency, and transportation disruptions. Energy-intensive materials such as cement and steel remain exposed to fuel price changes, with energy accounting for nearly 20%–30% of production costs in heavy manufacturing operations. Countries dependent on imported mineral inputs experience greater supply instability, affecting project timelines and procurement efficiency. European manufacturers continue adjusting operations due to carbon pricing mechanisms, while Asian producers are increasing local sourcing strategies. Companies are reducing exposure through supplier diversification, long-term procurement agreements, and regional production expansion. The key operational challenge is maintaining cost predictability without compromising sustainability investments.

The integration of automation, artificial intelligence, and advanced materials is creating new opportunities across the construction value chain. Digital manufacturing systems can reduce material waste by 15%–20%, while predictive analytics improve production planning and inventory efficiency. India’s smart infrastructure initiatives and China’s construction automation investments are accelerating adoption of intelligent building solutions. Manufacturers are developing lightweight composites, self-healing concrete, and recycled material technologies to improve durability and reduce lifecycle costs. Companies are strengthening R&D partnerships with technology firms and expanding sustainable product portfolios. A significant opportunity lies in localized circular material networks, enabling manufacturers to reduce logistics costs and create resilient supply chains in rapidly developing construction markets.

The transition toward advanced building materials faces execution challenges related to production scalability, technology integration, and workforce capability gaps. Automated construction and digital manufacturing adoption remains uneven, with many developing markets operating below 30% technology penetration in material production processes. Companies face difficulties integrating new systems with legacy facilities, managing capital requirements, and ensuring consistent product quality across locations. Skilled labor shortages in advanced manufacturing and green construction practices are affecting implementation speed in markets such as India and Southeast Asia. Manufacturers must invest in workforce training, smart factory upgrades, and technology partnerships to achieve reliable deployment. Long-term competitiveness depends on balancing innovation adoption with operational scalability and supply chain resilience.

Low-Carbon Material Transition: Cement and concrete producers are accelerating adoption of alternative binders, recycled aggregates, and carbon-reduction processes, with green material usage increasing by 20%–30% across major construction markets. Regulatory pressure from emission reduction frameworks in Europe and Asia is pushing companies to restructure production methods, expand sustainable product lines, and integrate renewable energy into manufacturing operations.

Smart Manufacturing Expansion: Building material manufacturers are deploying AI-based monitoring, robotics, and automated production systems to improve operational efficiency, with factories achieving 15%–25% reductions in material waste and 10%–20% productivity improvements. Companies in China and India are scaling smart factories and digital supply-chain platforms to strengthen quality control and reduce production variability.

Circular Construction Growth: Recycling-based material supply chains are gaining traction as demolition waste management becomes a strategic priority, with recycled material adoption rising by nearly 25% in developed construction markets. Companies are investing in material recovery facilities, closed-loop production models, and partnerships to reduce dependency on virgin raw materials and improve resource efficiency.

Localized Supply Chain Restructuring: Global logistics disruptions and raw material volatility are encouraging manufacturers to regionalize production networks, with more than 40% of large suppliers expanding local sourcing initiatives. Companies are establishing regional plants, securing long-term supplier agreements, and optimizing inventory strategies to improve resilience and maintain consistent material availability.

Cement-based materials represent the leading segment, accounting for approximately 45% of the core building materials market, supported by extensive use in residential, commercial, and infrastructure projects due to durability, scalability, and cost efficiency. Concrete solutions maintain strong demand because they integrate easily with modern construction systems, while steel, aggregates, bricks, and engineered materials continue supporting structural applications. Steel-based materials hold nearly 20% share, driven by high-strength applications in industrial facilities and urban developments. Advanced composites and recycled construction materials are emerging as the fastest-growing categories, with adoption increasing by approximately 15%–20% as builders prioritize lightweight structures, sustainability, and lifecycle efficiency. Companies are expanding low-carbon cement portfolios, investing in recycled material processing, and forming technology partnerships to improve product performance. The market shift indicates increasing investment toward materials that balance structural strength with environmental compliance.

Infrastructure construction represents the dominant application segment, capturing approximately 40% of demand due to extensive requirements for roads, bridges, transportation networks, and public facilities. Large-scale infrastructure modernization programs in China, India, and the United States continue supporting high-volume material consumption. Residential construction follows with nearly 30% share, supported by urban expansion and housing development initiatives. Commercial and industrial construction applications are emerging as faster-growing areas, with demand rising by approximately 15%–18% as companies prioritize energy-efficient buildings and advanced structural solutions. Data centers, manufacturing facilities, and logistics hubs are increasing requirements for specialized concrete, insulation, and composite materials. Manufacturers are adapting through customized product development, digital project integration, and expanded distribution networks to meet sector-specific requirements.

Construction companies represent the largest end-user segment, contributing approximately 50% of market demand due to direct involvement in residential, commercial, and infrastructure development projects. Their purchasing decisions are influenced by material availability, durability requirements, project timelines, and compliance standards. Government infrastructure agencies account for nearly 20% share, supported by transportation upgrades, urban development programs, and public construction initiatives. Industrial manufacturers and real estate developers are among the fastest-growing end-user groups, with adoption expanding by around 15%–20% as industries invest in specialized facilities and sustainable building solutions. Real estate developers are increasingly adopting advanced materials to achieve green certification targets and improve long-term asset value. Companies are responding through dedicated enterprise solutions, strategic supplier partnerships, and customized material offerings.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of5.2% between 2026 and 2033.

North America represents approximately 22% of the global core building materials market, supported by large-scale infrastructure renewal, commercial redevelopment, and increasing adoption of low-carbon construction solutions. The United States contributes the majority of regional demand through transportation upgrades, data center construction, and advanced manufacturing facility expansion. Sustainable cement alternatives and recycled aggregates are gaining traction, with green-certified buildings representing more than 40% of new commercial developments in major urban centers. Manufacturers are investing in automated production facilities, regional supply networks, and carbon-efficient manufacturing partnerships to improve resilience. Infrastructure modernization programs and stricter environmental requirements are accelerating demand for advanced materials with improved lifecycle performance.

United States Market Outlook: The United States remains the leading North American market due to its extensive construction ecosystem, industrial capacity, and technology-driven building practices. More than 50% of large commercial developers are incorporating sustainable material requirements into procurement strategies. Domestic producers are expanding recycled material processing, smart manufacturing systems, and localized supply chains to improve operational efficiency and meet evolving construction standards.

Europe accounts for nearly 18% of global core building materials demand, driven by sustainable construction mandates, infrastructure renovation, and circular economy initiatives. Countries such as Germany, France, and Italy are prioritizing low-emission cement, recycled aggregates, and energy-efficient building materials to align with stricter environmental frameworks. Carbon pricing mechanisms and green building regulations are encouraging manufacturers to redesign production processes, with several producers targeting 20%–30% emission reductions through alternative fuels and renewable energy integration. Companies are strengthening partnerships with recycling firms and technology providers to improve material recovery and reduce dependence on traditional inputs. Modernization of aging infrastructure remains a key demand driver across the region.

Germany Market Outlook: Germany maintains a strategic position through its advanced industrial base, engineering expertise, and sustainable construction innovation. The country’s manufacturing sector increasingly integrates automated material processing and resource-efficient production methods, with over 35% of new commercial projects incorporating environmental performance criteria. German suppliers are focusing on premium materials, circular construction models, and energy-efficient manufacturing upgrades.

Asia-Pacific dominates the global core building materials landscape with approximately 46% market share, supported by massive construction activity, manufacturing capacity, and urban infrastructure development. China remains the largest producer of cement and construction materials, contributing more than 50% of global cement output, while India continues expanding industrial corridors, housing projects, and transportation infrastructure. Large-scale urbanization programs, renewable energy projects, and industrial facility construction are increasing demand for concrete, aggregates, and engineered materials. Manufacturers are investing in automated plants, digital quality systems, and regional production hubs to improve efficiency. Supply-chain localization and technology upgrades are becoming key competitive priorities as companies manage rising energy costs and sustainability requirements.

China Market Outlook: China leads the Asia-Pacific market through unmatched production capacity, infrastructure investment scale, and manufacturing integration. The country operates the world’s largest cement production network and continues upgrading facilities with energy-efficient technologies. More than 60% of large construction material producers are adopting digital monitoring and automation solutions to improve productivity, reduce waste, and support environmental compliance.

South America contributes approximately 7% of global core building materials demand, supported by infrastructure upgrades, mining activity, housing development, and industrial expansion. Brazil represents the largest market due to its construction sector scale, domestic material production base, and transportation infrastructure requirements. Public infrastructure programs and private industrial investments are increasing demand for cement, aggregates, and structural materials. However, logistics limitations and uneven infrastructure development continue affecting supply efficiency in several markets. Companies are responding through localized manufacturing, distribution network improvements, and partnerships with regional contractors. Investments in energy-efficient production and alternative materials are increasing as manufacturers seek operational cost advantages and improved environmental performance.

Brazil Market Outlook: Brazil dominates South America’s construction materials ecosystem through its large domestic market, cement production capacity, and infrastructure requirements. The country’s construction sector accounts for a significant share of industrial material consumption, with urban housing and transportation projects driving demand. Producers are expanding regional facilities and adopting digital supply-chain management to improve delivery efficiency.

Middle East & Africa represents approximately 7% of global core building materials demand, with growth concentrated around infrastructure modernization, urban development, and large-scale investment programs. Saudi Arabia, the United Arab Emirates, and South Africa are key markets driving demand through smart cities, transportation networks, commercial developments, and industrial projects. Construction activity linked to economic diversification programs is increasing demand for advanced concrete solutions, sustainable materials, and efficient manufacturing systems. The region is also attracting investment into local production capacity to reduce import dependency, with several countries expanding domestic cement and material manufacturing facilities. Companies are establishing regional partnerships, upgrading plants, and improving logistics capabilities to support major development initiatives.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic market due to large infrastructure programs, urban transformation projects, and construction investment momentum. National development initiatives are supporting significant material demand, with major projects requiring millions of tons of cement and structural materials. Manufacturers are expanding production capacity and adopting sustainable technologies to align with long-term infrastructure objectives.

The Core Building Materials Market features competition between global leaders such as Holcim, Heidelberg Materials, CEMEX, and Saint-Gobain against regional producers, specialty material suppliers, and low-cost manufacturers. The top five players collectively account for approximately 30%–35% of market influence, with competition centered on production scale, carbon efficiency, supply reliability, and product customization. Global companies are investing in low-carbon cement, automated plants, and circular material solutions, while regional players compete through pricing advantages and localized distribution networks. Around 20%–30% of manufacturers are accelerating digital manufacturing adoption to improve operational efficiency. Companies are expanding through acquisitions, renewable energy integration, strategic partnerships, and vertical supply-chain control. The competitive landscape is shifting toward sustainability leadership, technology-driven production, and regional supply security. High capital requirements, regulatory compliance, and access to raw materials create strong entry barriers. Winning players must combine scale, innovation, cost discipline, and resilient supply networks.

Heidelberg Materials

CEMEX

Saint-Gobain

CRH plc

Vulcan Materials Company

China National Building Material Company

Anhui Conch Cement Company

UltraTech Cement

Buzzi Unicem

Taiheiyo Cement Corporation

Etex Group

Core building materials production is shifting toward smart manufacturing, artificial intelligence-based quality monitoring, robotics, and automated batching systems. Digital production platforms improve operational visibility and reduce material waste by 15%–20%, while automated inspection systems increase consistency by nearly 10%. Adoption is strongest among large cement and construction material manufacturers upgrading legacy plants.

Low-carbon technologies including alternative fuels, carbon capture systems, recycled aggregates, and engineered composites are transforming material performance. Compared with conventional production methods, advanced energy-efficient processes reduce emissions intensity by approximately 20%–30%. More than 40% of major construction suppliers are incorporating sustainability-driven product development into expansion strategies, creating advantages for companies with advanced environmental capabilities.

Between 2026 and 2028, AI-enabled supply forecasting, digital twins, and circular material platforms will become competitive differentiators. Global manufacturers benefit through scale and technology investment, while regional producers gain advantages through localized recycling networks and flexible production models. Companies acting early on automation, sustainability technologies, and intelligent supply chains will strengthen cost control, compliance readiness, and long-term market positioning.

June 2025 Heidelberg Materials inaugurated its Brevik CCS facility in Norway, becoming the first industrial-scale carbon capture and storage project in cement production. The facility is designed to capture around 400,000 tonnes of CO₂ annually, enabling lower-carbon cement production and establishing a scalable decarbonization model for the industry. Source: www.heidelbergmaterials.com

February 2026 Holcim reported progress in its sustainability and circular construction strategy, achieving 8 million tonnes of recycled construction and demolition materials processed during 2025. The initiative strengthens material circularity, reduces raw material dependency, and supports expansion of low-carbon building solutions across global markets. Source: www.holcim.com

September 2025 CEMEX continued advancing sustainable construction solutions through digital innovation and operational transformation programs across its cement and concrete businesses. The company’s technology initiatives support improved concrete performance measurement, with optimized concrete mixes enabling up to 13% CO₂ reduction in selected applications.

June 2025 Saint-Gobain expanded sustainable material innovation through its partnership with CarbiCrete to launch a cement-free concrete block production line in France. The project targets 20,000 tonnes annual production capacity from 2026, scaling toward 40,000 tonnes and reducing lifecycle carbon impact through carbon-storing construction materials. Source: www.saint-gobain.com

The Core Building Materials Market Report provides comprehensive coverage of material categories, including cement-based materials, aggregates, metals, bricks, composites, and sustainable alternatives. The analysis evaluates applications across infrastructure, residential, commercial, and industrial construction segments, along with end-users such as contractors, developers, government bodies, and industrial organizations. Regional assessment covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level strategic insights.

The report examines technology adoption trends, including automation, low-carbon manufacturing, recycled materials, and digital construction systems. It evaluates competitive positioning, supplier strategies, innovation priorities, and expansion opportunities. The study highlights adoption patterns, sustainability initiatives, supply-chain developments, and emerging niche opportunities to support investment decisions, market entry strategies, and long-term competitive planning through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 151.0 Million |

| Market Revenue (2033) | USD 208.4 Million |

| CAGR (2026–2033) | 4.11% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Holcim; Heidelberg Materials; CEMEX; Saint-Gobain; CRH plc; Vulcan Materials Company; China National Building Material Company; Anhui Conch Cement Company; UltraTech Cement; Buzzi Unicem; Taiheiyo Cement Corporation; Etex Group |

| Customization & Pricing | Available on Request (10% Customization Free) |