Reports

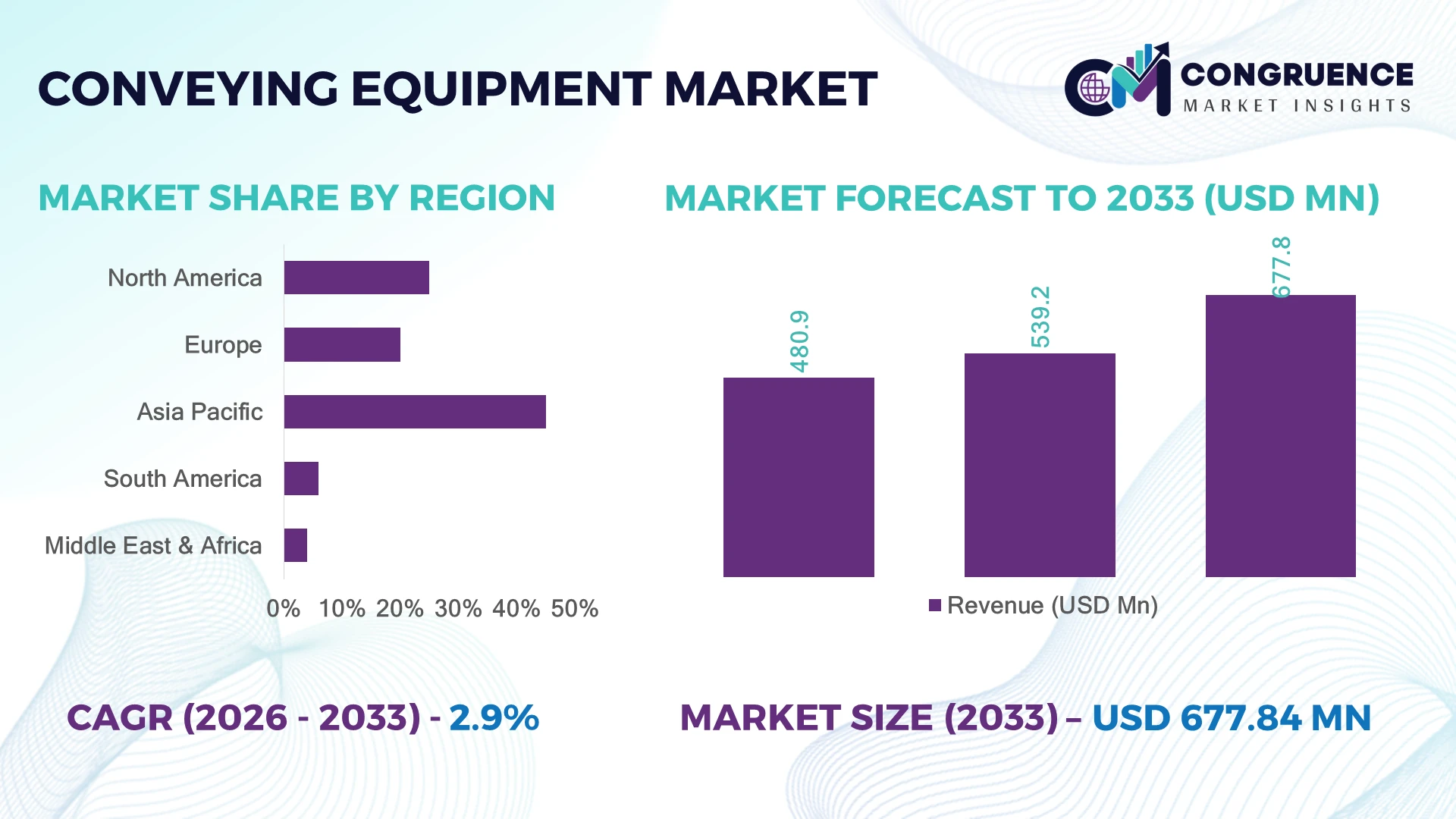

The Global Conveying Equipment Market was valued at USD 539.2 Million in 2025 and is anticipated to reach a value of USD 677.84 Million by 2033 expanding at a CAGR of 2.9% between 2026 and 2033. Rising warehouse automation, mining capacity expansion, and high-throughput manufacturing upgrades are accelerating demand for advanced conveying equipment integrated with AI-enabled monitoring, energy-efficient drives, and predictive maintenance systems across logistics, automotive, food processing, and bulk material handling operations.

China continues to dominate the global conveying equipment market with nearly 34% manufacturing share, supported by over USD 18 billion in industrial automation investments and rapid deployment across battery manufacturing, ports, and e-commerce fulfillment centers in 2026. The United States maintains stronger adoption of smart conveyor systems, with automated warehouse penetration exceeding 41% compared to China’s 33%, driven by labor optimization initiatives after Red Sea shipping disruptions and regional supply-chain restructuring. Germany remains a precision-engineering leader, where over 52% of new conveying installations now include Industry 4.0-enabled sensors and digital twin integration for operational efficiency gains.

Manufacturers prioritizing automated, low-energy, and digitally connected conveying systems are positioned to secure long-term contracts across high-growth industrial and logistics infrastructure projects.

Market Size & Growth: Global conveying equipment market advances from USD 539.2 Million in 2025 to USD 677.84 Million by 2033, supported by automated warehousing, mining modernization, and smart factory deployment.

Top Growth Drivers: Warehouse automation contributes 38% demand growth, mining expansion 27%, and food processing automation 21% across high-throughput industrial operations.

Short-Term Forecast: By 2028, AI-enabled conveyor monitoring reduces downtime by 24% while improving material handling efficiency by 18% in large-scale facilities.

Emerging Technologies: Advanced robotics integration, IoT-based predictive maintenance, and low-friction modular conveyor systems improve operational productivity by over 22%.

Regional Leaders: Asia-Pacific exceeds USD 250 Million with manufacturing expansion, North America crosses USD 180 Million through logistics automation, while Europe surpasses USD 145 Million via Industry 4.0 adoption.

Consumer/End-User Trends: Nearly 46% of logistics operators prioritize energy-efficient conveying systems to offset labor shortages and rising electricity costs.

Pilot/Case Example: In 2026, a large automotive facility deployment improved assembly-line throughput by 19% and reduced manual handling costs by 14%.

Competitive Landscape: Top manufacturers control nearly 44% market share, with leaders including Siemens, Daifuku, Honeywell, BEUMER Group, and SSI SCHAEFER.

Regulatory & ESG Impact: Energy-optimized conveyor systems lower facility power consumption by 17%, aligning with stricter industrial emissions and efficiency regulations.

Investment & Funding: More than USD 9 billion in industrial automation investments support conveyor modernization, regional manufacturing expansion, and smart logistics hubs.

Innovation & Future Outlook: Autonomous material flow systems, AI-driven sorting, and digital twin-enabled conveyor optimization are reshaping high-growth global supply-chain infrastructure.

Conveying equipment demand remains concentrated in e-commerce fulfillment centers, automotive production lines, mining operations, and food processing facilities requiring continuous material flow and reduced manual handling. In 2026, over 43% of new installations incorporated IoT-enabled monitoring and predictive diagnostics to improve uptime and energy efficiency. Regional manufacturing diversification and stricter operational efficiency standards are accelerating adoption of modular, automated conveying systems, strengthening the foundation for long-term strategic expansion discussions.

Conveying equipment is becoming strategically critical as manufacturers, logistics operators, and mining companies redesign production and distribution networks around automation, throughput optimization, and labor efficiency. Supply-chain restructuring after Red Sea shipping disruptions and nearshoring initiatives in Mexico and Southeast Asia accelerated investment in smart material-handling infrastructure during 2026. More than 48% of large warehouse operators now prioritize conveyor modernization to reduce fulfillment delays, improve inventory movement accuracy, and support round-the-clock operations. The market is increasingly tied to industrial competitiveness, particularly in automotive, battery manufacturing, food processing, and e-commerce fulfillment ecosystems.

AI-enabled conveyor systems integrated with predictive analytics reduce unplanned downtime by nearly 26% compared to legacy belt-driven systems while lowering maintenance costs by 18%. Japan and Germany continue leading in precision automation deployment, where over 50% of new installations incorporate digital twin simulation and sensor-based monitoring, while India and Vietnam focus on scalable modular conveyor deployment for expanding manufacturing clusters. In 2026, a major automotive production facility in Tennessee upgraded to automated conveying lines, improving assembly throughput by 21% and reducing material transfer bottlenecks during peak operations.

Over the next two to three years, companies are expected to prioritize localized manufacturing partnerships, robotics integration, and energy-efficient conveyor architecture to strengthen operational resilience. Firms expanding intelligent conveying networks with real-time tracking, modular retrofitting capability, and low-energy drive systems are securing stronger positioning in high-volume industrial and logistics infrastructure projects.

Industrial automation investment continues to accelerate conveying equipment deployment across manufacturing, logistics, and mining operations. In 2026, automated warehouse penetration exceeded 41% in the United States, while China expanded smart factory installations by nearly 29% across electronics and battery manufacturing clusters. Conveyor-integrated AI monitoring systems reduced operational downtime by 24% and improved material flow efficiency by 19%, directly supporting high-volume production targets. Labor shortages across Germany and Japan further intensified enterprise demand for automated handling systems capable of continuous operation with lower manual intervention. In response, major equipment manufacturers are expanding modular conveyor portfolios, increasing robotics partnerships, and investing in predictive maintenance software integration. A notable strategic shift involves conveyor suppliers aligning directly with industrial automation vendors to secure long-term contracts tied to factory modernization and regional supply-chain restructuring initiatives.

Steel price fluctuations, semiconductor dependency, and motor supply disruptions continue pressuring conveying equipment deployment economics. In 2026, industrial motor procurement costs increased by nearly 14%, while controller lead times extended beyond 20 weeks for several automation-dependent conveyor configurations. Legacy manufacturing facilities across India and Eastern Europe face interoperability limitations, where over 37% of installed material-handling infrastructure lacks compatibility with sensor-enabled automation systems. These constraints reduce deployment scalability and increase retrofit complexity, particularly for mid-sized manufacturers operating on narrow operating margins. Companies are responding through localized sourcing strategies, long-term supplier contracts, and alternative drive-system procurement diversification. A growing operational challenge involves balancing energy-efficient upgrades with short-term capital expenditure discipline, forcing manufacturers to phase conveyor modernization projects instead of executing full-scale infrastructure replacement programs.

Rapid expansion of automated fulfillment centers and intelligent manufacturing hubs is creating strong demand for modular, software-driven conveying systems. In 2026, nearly 44% of new logistics infrastructure projects incorporated IoT-enabled conveyor tracking, while autonomous sorting integration improved parcel handling speed by 28% in high-volume distribution centers. India’s industrial corridor expansion and Saudi Arabia’s infrastructure modernization initiatives are opening new deployment opportunities for scalable conveyor architecture supporting manufacturing diversification. Equipment suppliers are increasingly investing in digital twin simulation, low-friction conveyor materials, and cloud-based operational analytics to reduce maintenance cycles and energy consumption. A non-obvious opportunity is emerging in retrofit-as-a-service models, where manufacturers upgrade existing conveyor infrastructure incrementally rather than replacing entire systems, allowing faster adoption across cost-sensitive industrial facilities while strengthening recurring service revenue streams.

Advanced conveying systems increasingly depend on AI-enabled controls, robotics synchronization, and real-time operational analytics, creating integration and workforce capability challenges. In 2026, nearly 32% of industrial operators reported shortages of automation technicians capable of maintaining digitally connected conveyor infrastructure. Large-scale facilities integrating multi-vendor automation environments experienced commissioning delays averaging 17% due to software compatibility and cybersecurity validation requirements. The shift toward cloud-connected material-handling systems also raises operational exposure to industrial network disruptions and data-security vulnerabilities. Manufacturers in the United States and South Korea are expanding technical training partnerships and investing in standardized control architectures to improve deployment consistency. Long-term competitiveness will depend on solving interoperability gaps between legacy infrastructure and next-generation automation platforms while maintaining uptime reliability across increasingly complex industrial ecosystems.

AI-Driven Conveyor Intelligence AI-enabled conveyor analytics platforms are reshaping material flow optimization across automotive and warehouse operations. In 2026, nearly 39% of newly deployed conveyor systems integrated predictive maintenance software, reducing unplanned stoppages by 23% and lowering inspection costs by 17%. Germany-based manufacturers increasingly deploy sensor-rich conveyor architecture to address labor shortages and stricter uptime targets. Companies are expanding industrial software partnerships and embedding digital twin simulation into conveyor commissioning workflows to improve deployment precision and long-term asset utilization.

Modular Fulfillment Infrastructure Expansion E-commerce and third-party logistics operators are accelerating adoption of modular conveyor systems capable of rapid reconfiguration during seasonal demand spikes. In the United States, fulfillment centers using modular conveyor layouts improved parcel throughput by 21% while reducing retrofit downtime by 28%. Supply-chain diversification after Red Sea shipping disruptions pushed logistics operators in Mexico and Vietnam to scale localized distribution hubs. Conveyor manufacturers are responding with plug-and-play automation platforms and faster installation cycles designed for high-volume warehouse expansion programs.

Energy-Efficient Drive System Adoption Rising industrial electricity costs and tighter factory efficiency mandates are accelerating the shift toward low-energy conveyor technologies. In Japan, over 31% of new conveyor installations now incorporate regenerative drive systems capable of lowering energy consumption by 16%. Food processing companies are increasingly replacing pneumatic-heavy configurations with optimized belt and roller systems to reduce operating expenses. Equipment suppliers are prioritizing lightweight materials, variable-frequency drives, and smart load-balancing technologies to strengthen sustainability performance without compromising throughput reliability.

Autonomous Sorting Integration Growth High-speed autonomous sorting integration is becoming operationally critical in retail warehouses and parcel handling networks. In 2026, conveyor-linked robotic sorting installations increased by 27% across large-scale logistics facilities in China and South Korea, improving order accuracy by 19%. A non-obvious shift is emerging in pharmaceutical distribution centers, where conveyor-integrated vision systems are reducing compliance verification time during high-volume dispatch operations. Companies are increasing investment in robotics alliances, AI-enabled scanning systems, and cloud-connected warehouse orchestration platforms to support real-time inventory movement and precision fulfillment.

Belt conveyors continue leading the conveying equipment market due to their scalability, operational flexibility, and cost-efficient deployment across logistics, mining, and food processing environments. In 2026, belt conveyor systems accounted for nearly 38% of industrial material-handling installations, supported by growing warehouse automation and continuous-flow manufacturing requirements. Their ability to support long-distance transport with lower maintenance intensity strengthened adoption across large-scale automotive and e-commerce facilities in the United States and China. Manufacturers are expanding lightweight belt technologies, energy-efficient drives, and AI-enabled monitoring capabilities to improve throughput reliability and reduce downtime exposure.

Pneumatic conveyors are emerging as the fastest-growing segment, particularly in pharmaceutical, food, and chemical processing applications requiring contamination-controlled transport. Deployment increased by approximately 24% in high-purity manufacturing environments due to stricter hygiene and dust-control standards. Roller conveyors remain strategically relevant in parcel handling and distribution centers because of rapid installation capability and modular adaptability, while chain conveyors continue dominating heavy-duty automotive assembly operations. Screw conveyors retain steady demand in bulk material processing sectors where compact footprint and enclosed transport remain operational priorities. Equipment suppliers are increasingly diversifying product portfolios to target specialized industrial workflows and retrofit modernization programs.

Material handling remains the leading application segment due to widespread deployment across manufacturing plants, mining operations, and logistics infrastructure requiring continuous high-volume movement efficiency. In 2026, nearly 42% of conveying equipment installations supported core material-handling workflows, particularly in automotive and industrial manufacturing facilities where throughput optimization and labor reduction remain operational priorities. Companies are increasingly integrating conveyor-linked robotics and real-time monitoring systems to improve inventory movement visibility and reduce transfer delays across multi-stage production environments.

Warehouse automation is the fastest-growing application segment as e-commerce expansion and regional supply-chain restructuring intensify investment in high-speed fulfillment infrastructure. Automated conveyor deployment within retail and third-party logistics warehouses increased by approximately 29% during 2026, with sorting accuracy improvements exceeding 18% in large-scale facilities. Packaging applications are evolving toward compact modular conveyor layouts supporting flexible production runs, while assembly lines continue relying on synchronized conveyor architecture for precision manufacturing operations. Bulk material transport remains strategically important in mining and cement industries where durability and continuous operation are critical. Conveyor manufacturers are prioritizing scalable automation integration, software interoperability, and rapid deployment capability to strengthen competitive positioning in logistics-driven applications.

The manufacturing industry remains the dominant end-user segment due to extensive conveyor deployment across automotive, electronics, metal processing, and industrial assembly operations. In 2026, manufacturing facilities represented nearly 36% of total conveying equipment utilization, supported by rising automation investment and continuous production optimization initiatives. Germany and China expanded smart manufacturing deployments significantly, where AI-enabled conveyor systems improved material transfer efficiency by over 20% in high-volume production environments. Equipment suppliers are increasingly offering customized conveyor configurations, predictive maintenance integration, and modular retrofitting solutions to strengthen long-term industrial contracts.

Retail warehouses are emerging as the fastest-growing end-user segment as e-commerce fulfillment networks scale high-speed sorting and automated inventory movement infrastructure. Conveyor installations across large retail distribution hubs increased by approximately 31% in 2026, particularly in the United States and India where rapid delivery expectations intensified automation requirements. Logistics operators continue investing in conveyor-linked robotics and cloud-based orchestration systems, while the food and beverage industry prioritizes hygienic conveying technologies aligned with stricter processing standards. Mining applications maintain demand for heavy-duty bulk transport systems, and automotive manufacturers continue expanding synchronized conveyor deployment for flexible production lines. Companies are strengthening ecosystem partnerships and regional service capabilities to secure high-volume enterprise clients.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2026 and 2033.

Automation-Centric Logistics Modernization

North America remains a highly mature conveying equipment market driven by warehouse automation, automotive production upgrades, and advanced logistics infrastructure deployment. The region accounted for nearly 27% of global installations in 2025, supported by large-scale fulfillment center expansion and industrial automation investment across the United States and Mexico. More than 46% of newly commissioned distribution facilities integrated AI-enabled conveyor monitoring systems to improve throughput consistency and reduce manual handling dependency. Rising nearshoring activity in Mexico accelerated deployment of modular conveyor systems within electronics and automotive supply chains. Companies are strengthening regional manufacturing footprints and expanding robotics partnerships to support faster installation cycles, localized servicing capability, and operational resilience amid evolving cross-border supply-chain requirements.

United States Market Outlook: The United States continues leading regional conveyor deployment through high-volume logistics automation, automotive manufacturing expansion, and retail warehouse modernization. In 2026, automated warehouse penetration exceeded 41%, while large-scale parcel handling facilities expanded conveyor-linked robotic sorting capacity by approximately 24%. Industrial operators increasingly prioritize predictive maintenance integration and digital twin simulation to reduce downtime and improve fulfillment speed. Major enterprises are also investing in energy-efficient conveyor architecture to offset labor shortages and rising operational costs across nationwide distribution networks.

Industry 4.0 Integration Reshaping Operations

Europe’s conveying equipment market is defined by precision manufacturing, sustainability-focused industrial modernization, and high adoption of Industry 4.0-enabled automation systems. The region represented nearly 23% of global deployment activity in 2025, with Germany, Italy, and France driving demand through advanced manufacturing infrastructure. Over 52% of newly installed conveyor systems incorporated sensor-enabled diagnostics and smart control integration to optimize operational efficiency and reduce maintenance exposure. Stricter industrial energy-efficiency regulations accelerated deployment of low-energy drive systems and lightweight conveyor materials across food processing and automotive sectors. Companies are increasingly focusing on retrofit modernization programs, automation software partnerships, and localized engineering support to strengthen long-term industrial service contracts and compliance-driven equipment replacement demand.

Germany Market Outlook: Germany remains the region’s operational and technology leader due to its strong industrial automation ecosystem and advanced engineering capabilities. In 2026, nearly 58% of conveyor deployments within large manufacturing facilities incorporated AI-based monitoring and predictive servicing tools. Automotive and machinery production hubs continue investing in synchronized conveyor architecture supporting flexible manufacturing operations and precision assembly workflows. German enterprises are also expanding digital twin integration and energy-optimized conveyor retrofits to align with stricter factory efficiency targets and industrial decarbonization initiatives.

Large-Scale Manufacturing Expansion Dominates Demand

Asia-Pacific leads the global conveying equipment market through large-scale industrial manufacturing, mining activity, and rapid logistics infrastructure development. The region contributed approximately 41% of global market demand in 2025, supported by China, Japan, India, and South Korea. Manufacturing automation investment increased sharply across electronics, battery production, and e-commerce fulfillment ecosystems, where conveyor-integrated robotics improved material flow efficiency by over 22%. India’s industrial corridor development and Southeast Asia’s export manufacturing expansion accelerated deployment of modular conveyor systems within high-volume production environments. Companies are expanding localized manufacturing facilities, increasing automation partnerships, and strengthening after-sales service networks to capture rising enterprise demand tied to regional supply-chain diversification strategies.

China Market Outlook: China remains the largest single-country market due to extensive smart factory deployment, export-driven manufacturing scale, and aggressive warehouse automation investment. In 2026, over 33% of large industrial facilities integrated AI-enabled conveying systems to support high-speed production and logistics workflows. Battery manufacturing, automotive assembly, and e-commerce distribution centers continue driving conveyor demand through continuous infrastructure expansion. Domestic equipment suppliers are increasing investment in intelligent sorting systems, low-energy drives, and advanced control software to strengthen competitiveness against international automation providers.

Mining and Bulk Handling Drive Expansion

South America’s conveying equipment market is expanding steadily through mining modernization, agricultural export infrastructure upgrades, and industrial material-handling investments. Brazil and Chile continue driving deployment across bulk material transport and mineral processing operations, where conveyor systems improve operational continuity and reduce manual handling costs. In 2026, mining-linked conveyor deployment increased by nearly 18% across major copper and iron ore production facilities. Infrastructure bottlenecks and uneven automation capability still limit full-scale deployment consistency across certain industrial corridors. Companies are responding through localized servicing partnerships, modular conveyor offerings, and maintenance-focused support agreements designed for remote industrial environments and long-distance bulk transport operations.

Brazil Market Outlook: Brazil remains the region’s most strategically significant market due to its mining scale, agricultural export infrastructure, and expanding industrial manufacturing activity. Large mining operators are increasing adoption of heavy-duty conveyor systems capable of supporting continuous ore transport across remote extraction facilities. In 2026, automated conveyor utilization within major mining projects increased by approximately 21%, supported by operational efficiency targets and rising export throughput requirements. Domestic logistics modernization programs are also supporting conveyor deployment across food processing and port-linked material handling facilities.

Infrastructure Diversification Accelerates Investment

Middle East & Africa is emerging as a high-priority growth market due to infrastructure diversification, industrial corridor development, and large-scale logistics modernization initiatives. Gulf countries are increasing deployment of automated conveying systems across airports, ports, manufacturing zones, and retail distribution facilities to support economic diversification beyond hydrocarbons. In 2026, industrial automation-linked conveyor installations increased by nearly 26% across logistics and construction material handling projects. Mining operations in South Africa and infrastructure expansion in Saudi Arabia are strengthening regional equipment demand. Companies are increasing regional partnerships, establishing localized assembly operations, and expanding engineering support capabilities to secure long-term infrastructure and industrial modernization contracts.

Saudi Arabia Market Outlook: Saudi Arabia continues strengthening its position through large-scale industrial diversification programs, logistics infrastructure expansion, and smart manufacturing investments aligned with national economic transformation initiatives. Conveyor deployment across industrial cities and logistics hubs accelerated significantly in 2026, particularly within warehousing, food processing, and construction materials handling operations. More than 30% of newly commissioned logistics facilities incorporated automated conveyor and sorting systems to improve operational throughput and reduce labor dependency. International equipment providers are increasingly partnering with regional engineering firms to support localization requirements and long-term infrastructure deployment targets.

Global leaders such as Siemens, Daifuku, Honeywell, SSI SCHAEFER, and BEUMER Group compete directly against regional automation integrators and cost-focused conveyor manufacturers across logistics, mining, automotive, and industrial processing sectors. The top five players collectively control nearly 44% of the global market, with competition increasingly centered on intelligent automation capability, deployment speed, lifecycle servicing, and software integration efficiency. AI-enabled predictive maintenance systems improve operational uptime by approximately 24%, while modular conveyor architecture reduces installation time by nearly 19%, intensifying technology-led competition between premium OEMs and regional suppliers. Companies are expanding through warehouse automation partnerships, regional manufacturing facilities, robotics integration, and vertically integrated service ecosystems. Competitive pressure is shifting toward digital conveyor intelligence, cloud-connected material flow management, and energy-efficient system design. High capital requirements, industrial certification complexity, and long-term enterprise procurement cycles remain major entry barriers. Winning in this market requires scalable automation expertise, localized servicing strength, and high-efficiency conveyor ecosystems aligned with evolving industrial infrastructure demands.

Siemens

Daifuku Co., Ltd.

Honeywell Intelligrated

BEUMER Group

SSI SCHAEFER

Dematic

Interroll Holding AG

TGW Logistics Group

Vanderlande Industries

Murata Machinery Ltd.

Fives Group

FlexLink

Dorner Mfg. Corp.

Hytrol Conveyor Company

AI-enabled conveyor monitoring and IoT-connected material handling systems are becoming core technologies across logistics, automotive, and manufacturing operations. In 2026, nearly 39% of newly deployed conveyor systems integrated predictive maintenance analytics, reducing unplanned downtime by 24% and lowering maintenance costs by 18%. Smart motor-driven roller systems with run-on-demand functionality are replacing conventional continuously powered conveyors, improving energy efficiency by approximately 16%. Companies operating high-volume fulfillment centers benefit from faster throughput visibility, remote diagnostics, and lower operational interruptions, strengthening delivery consistency and warehouse utilization rates.

Emerging technologies including digital twins, machine vision sorting, and cloud-connected warehouse orchestration platforms are accelerating conveyor automation capability. Germany and Japan lead deployment of digital twin-assisted conveyor commissioning, where installation optimization improves system calibration accuracy by nearly 21% compared to legacy engineering workflows. Automated overhead conveyor systems integrated with robotics and autonomous mobile vehicles are expanding rapidly across retail warehouses and electronics manufacturing facilities. Conveyor suppliers are increasing partnerships with industrial software firms to deliver synchronized material flow management and intelligent asset tracking.

Between 2026 and 2028, modular conveyor ecosystems with AI-based routing and low-energy drive systems are expected to dominate industrial modernization strategies. Companies investing early in interoperable automation architecture, intelligent diagnostics, and scalable conveyor retrofits are positioned to secure stronger competitive advantage in high-speed logistics and smart manufacturing environments.

September 2025 – Daifuku completed expansion of its Hobart, Indiana manufacturing facility, increasing production capacity for conveyors and sorters by nearly 100% through a 25,000 m² addition. The expansion strengthens North American automation delivery capability and shortens industrial lead times significantly. Source: daifuku.com

April 2025 – Daifuku Intralogistics India launched a new Hyderabad manufacturing plant, expanding production space nearly fourfold for conveyors, AS/RS systems, and pallet sorters. The facility improves local production flexibility and supports rising industrial automation deployment across India’s manufacturing and distribution sectors. Source: daifuku.com

March 2026 – SSI SCHAEFER partnered with Schaeffler to build a highly automated logistics hub in Poland integrating robotics, AGVs, and intelligent conveyor-linked software systems. The project improves material flow reliability and accelerates global aftermarket fulfillment operations for industrial mobility and automotive supply chains. Source: ssi-schaefer.com

February 2026 – SSI SCHAEFER introduced the SSI Pallet Roaming Shuttle, a six-way autonomous pallet handling system supporting loads up to 1.5 tons. The modular design improves warehouse storage density and enables scalable automation deployment for space-constrained logistics and food processing facilities. Source: agencewepa.com

The conveying equipment market report delivers comprehensive analysis across belt conveyors, roller conveyors, chain conveyors, screw conveyors, and pneumatic conveyors, covering operational deployment trends across material handling, packaging, warehouse automation, assembly lines, and bulk material transport applications. The study evaluates demand concentration across manufacturing, logistics, mining, automotive, retail warehouses, and food processing industries, where over 45% of new installations now incorporate automation-linked monitoring and intelligent control systems. Regional assessment spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting industrial modernization, logistics infrastructure expansion, and automation deployment patterns.

The report further examines AI-enabled conveyor diagnostics, digital twin integration, robotics-linked material handling, and energy-efficient drive technologies shaping operational competitiveness between 2026 and 2033. It provides strategic insights into enterprise expansion priorities, localized manufacturing strategies, retrofit modernization opportunities, and automation partnerships influencing market positioning. Coverage also includes emerging deployment models, modular conveyor ecosystems, and evolving industrial procurement behavior supporting long-term investment planning and competitive differentiation.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 539.2 Million |

Market Revenue in 2033 | USD 677.84 Million |

CAGR (2026 - 2033) | 2.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Siemens, Daifuku Co., Ltd., Honeywell Intelligrated, BEUMER Group, SSI SCHAEFER, Dematic, Interroll Holding AG, TGW Logistics Group, Vanderlande Industries, Murata Machinery Ltd., Fives Group, FlexLink, Dorner Mfg. Corp., Hytrol Conveyor Company |

Customization & Pricing | Available on Request (10% Customization is Free) |