Reports

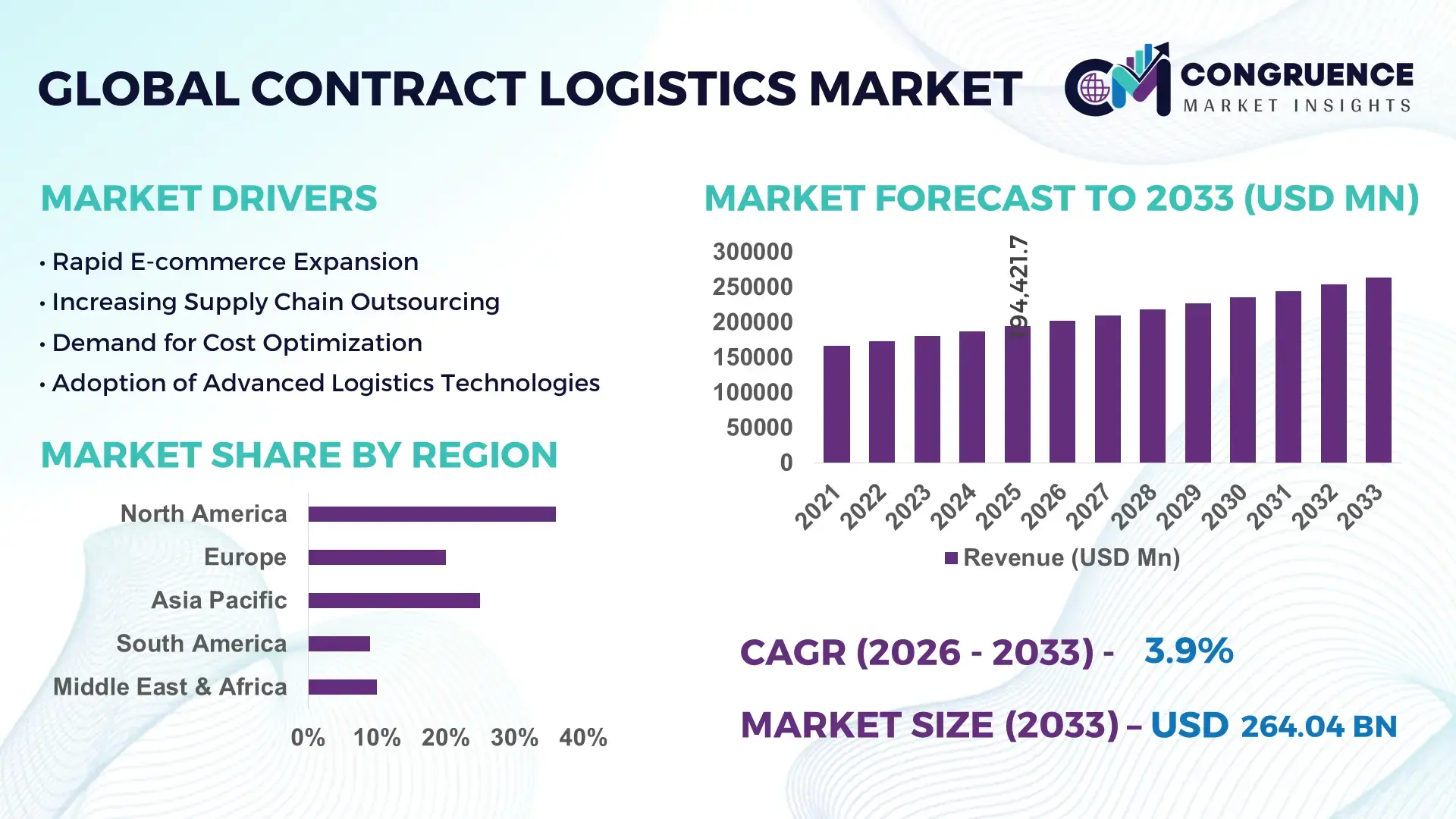

The Global Contract Logistics Market was valued at USD 194421.73 Million in 2025 and is anticipated to reach a value of USD 264039.67 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. This growth is primarily driven by increasing outsourcing of supply chain operations and rising demand for integrated logistics solutions across industries.

The United States continues to demonstrate strong operational scale in the contract logistics sector, supported by over 1.9 billion square feet of warehouse space and continuous investments exceeding USD 25 billion annually in logistics infrastructure. The country leads in advanced warehouse automation adoption, with more than 35% of large distribution centers integrating robotics and AI-based inventory systems. Key industries such as e-commerce, retail, and healthcare contribute significantly to logistics demand, with e-commerce alone accounting for over 40% of third-party logistics utilization. Additionally, cold chain logistics capacity in the U.S. has expanded by nearly 20% over the past three years, supporting pharmaceuticals and food supply chains.

Market Size & Growth: Valued at USD 194421.73 Million in 2025, projected to reach USD 264039.67 Million by 2033, growing at a CAGR of 3.9% driven by increased outsourcing and e-commerce expansion.

Top Growth Drivers: 45% rise in e-commerce logistics demand, 30% improvement in supply chain efficiency via outsourcing, 25% increase in warehouse automation adoption.

Short-Term Forecast: By 2028, digital logistics platforms are expected to reduce operational costs by 18% and improve delivery speed by 22%.

Emerging Technologies: AI-driven demand forecasting, autonomous mobile robots, blockchain-based supply chain tracking.

Regional Leaders: North America projected to reach USD 95 billion by 2033 with high automation adoption; Asia-Pacific to hit USD 85 billion driven by manufacturing hubs; Europe to reach USD 60 billion with sustainability-focused logistics.

Consumer/End-User Trends: Retail and e-commerce dominate with over 50% usage, followed by healthcare and automotive sectors adopting integrated logistics solutions.

Pilot or Case Example: In 2024, a global retailer achieved 28% warehouse efficiency gains using AI-enabled picking systems.

Competitive Landscape: DHL leads with approximately 18% share, followed by Kuehne+Nagel, DB Schenker, XPO Logistics, and Nippon Express.

Regulatory & ESG Impact: Carbon reduction mandates are driving 20% adoption of green warehousing and electric fleets.

Investment & Funding Patterns: Over USD 40 billion invested globally in logistics infrastructure and smart warehousing technologies in recent years.

Innovation & Future Outlook: Integration of IoT, predictive analytics, and digital twins is shaping next-generation contract logistics ecosystems.

Contract logistics services are widely utilized across retail, automotive, healthcare, and industrial manufacturing sectors, with retail and e-commerce contributing over half of total service demand due to high order volumes and last-mile delivery requirements. Technological innovations such as warehouse robotics, IoT-enabled asset tracking, and cloud-based logistics management platforms are transforming operational efficiency. Regulatory frameworks promoting emissions reduction and sustainable supply chains are accelerating adoption of green logistics practices, particularly in Europe. Asia-Pacific is witnessing rapid growth due to expanding manufacturing exports and rising domestic consumption. Future trends indicate increasing reliance on data-driven logistics, multi-modal transport optimization, and strategic partnerships to enhance resilience and scalability.

The contract logistics market is strategically vital for optimizing global supply chains, enabling businesses to enhance efficiency, reduce costs, and improve service levels through specialized third-party logistics providers. Advanced warehouse automation delivers up to 35% productivity improvement compared to traditional manual operations, significantly transforming fulfillment models. North America dominates in logistics volume, while Asia-Pacific leads in adoption with over 40% of enterprises integrating digital logistics platforms.

By 2028, AI-driven route optimization and predictive analytics are expected to reduce delivery times by 20% and inventory holding costs by 15%. Firms are committing to ESG targets, including a 30% reduction in carbon emissions and increased use of recyclable packaging materials by 2030. In 2024, a leading logistics provider in Germany achieved a 25% reduction in operational downtime through IoT-enabled fleet management systems.

The evolving contract logistics market is positioned as a cornerstone of supply chain resilience, compliance, and sustainable growth, driven by continuous technological innovation and global trade expansion.

The contract logistics market is influenced by rapid digital transformation, globalization of trade, and increasing complexity in supply chains. Businesses are shifting toward integrated logistics solutions to improve efficiency, reduce operational risks, and enhance customer satisfaction. Rising demand for last-mile delivery, coupled with expansion in cold chain logistics for pharmaceuticals and perishable goods, is shaping market trends. Automation, artificial intelligence, and data analytics are playing a crucial role in improving warehouse and transportation efficiency. Additionally, regulatory requirements for sustainability and carbon reduction are encouraging the adoption of eco-friendly logistics practices across developed and emerging economies.

The surge in global e-commerce activity has significantly increased demand for efficient warehousing, order fulfillment, and last-mile delivery services. Online retail sales now account for over 20% of total global retail, leading to higher reliance on third-party logistics providers for scalable operations. Contract logistics firms are deploying automated picking systems and real-time inventory management tools to handle large order volumes. Same-day and next-day delivery expectations have further accelerated investments in urban distribution centers, improving delivery speed by up to 25%. This transformation is making contract logistics a critical enabler of digital commerce ecosystems.

High capital investment requirements for advanced warehouse infrastructure, automation systems, and skilled labor pose significant challenges for market growth. Establishing smart warehouses can require investments exceeding USD 50 million per facility, limiting entry for smaller players. Additionally, fluctuating fuel prices and rising labor costs, which have increased by nearly 15% in major logistics markets, further strain operational budgets. Compliance with stringent safety and environmental regulations also adds to cost burdens. These factors collectively restrict scalability and profitability, particularly for mid-sized logistics service providers.

The integration of digital technologies such as AI, IoT, and blockchain presents substantial growth opportunities for contract logistics providers. Smart warehouses equipped with IoT sensors can improve inventory accuracy by up to 99%, while AI-driven demand forecasting reduces stockouts by nearly 30%. Blockchain enhances transparency and traceability across supply chains, especially in pharmaceuticals and food logistics. Emerging markets in Asia-Pacific and Latin America are witnessing increased adoption of digital logistics platforms, driven by expanding industrialization and trade activities. These advancements enable service providers to offer value-added, data-driven logistics solutions.

Frequent supply chain disruptions caused by geopolitical tensions, trade restrictions, and natural disasters significantly impact logistics operations. Delays in transportation and shortages of critical materials can reduce operational efficiency by up to 20%. Additionally, port congestion and limited container availability continue to create bottlenecks in global trade flows. Managing these disruptions requires advanced risk mitigation strategies and increased inventory buffers, which raise operational costs. Ensuring resilience while maintaining service quality remains a critical challenge for contract logistics providers operating in highly dynamic global environments.

• Surge in Warehouse Automation and Robotics Adoption: Automation technologies are transforming contract logistics operations, with over 38% of large-scale warehouses globally deploying robotics for picking, packing, and sorting functions. Automated storage and retrieval systems have improved operational efficiency by up to 30% while reducing labor dependency by nearly 25%. In North America and Europe, more than 45% of newly built distribution centers now integrate AI-driven warehouse management systems, enhancing order accuracy to above 99%. This trend is particularly evident in high-volume sectors such as e-commerce and retail, where speed and precision are critical.

• Expansion of Cold Chain Logistics Infrastructure: The growing demand for temperature-sensitive products has accelerated investments in cold chain logistics, with global refrigerated warehouse capacity increasing by over 20% in the last three years. Pharmaceuticals account for approximately 35% of cold chain usage, driven by vaccine distribution and biologics storage requirements. Additionally, food and beverage logistics contribute nearly 50% of demand, with strict compliance standards pushing adoption of real-time temperature monitoring systems that improve product integrity by 28%. Emerging markets in Asia-Pacific are witnessing double-digit expansion in cold storage facilities.

• Integration of Digital Supply Chain Platforms: Digitalization is reshaping contract logistics through cloud-based platforms and real-time data analytics, with over 50% of logistics providers implementing digital supply chain solutions. These platforms enable end-to-end visibility, reducing shipment delays by 18% and improving inventory turnover rates by 22%. Blockchain-based tracking systems are being adopted by nearly 15% of global logistics firms to enhance transparency and reduce fraud risks. This trend supports seamless coordination across suppliers, manufacturers, and distributors, strengthening overall supply chain resilience.

• Growth in Sustainable and Green Logistics Practices: Sustainability initiatives are becoming central to contract logistics, with over 40% of companies adopting eco-friendly practices such as electric delivery fleets and energy-efficient warehouses. Carbon emissions from logistics operations have been reduced by up to 20% through route optimization and alternative fuel usage. In Europe, more than 30% of logistics providers have committed to achieving carbon neutrality targets by 2030. Green warehousing, including solar-powered facilities and recyclable packaging solutions, is gaining traction as companies align with global environmental regulations and ESG goals.

The contract logistics market is segmented by type, application, and end-user, reflecting diverse operational requirements across industries. Transportation management and warehousing services dominate due to high demand for integrated logistics solutions, while value-added services such as packaging and inventory management are gaining traction. Applications are primarily concentrated in retail, e-commerce, healthcare, and automotive sectors, with retail and e-commerce accounting for a significant share due to increasing order volumes and last-mile delivery needs. End-user demand is driven by large enterprises, although small and medium-sized businesses are rapidly adopting outsourced logistics services to improve efficiency. Regional variations in adoption highlight strong demand in North America and Asia-Pacific due to industrial expansion and digital transformation initiatives.

The contract logistics market is categorized into transportation management, warehousing, distribution, and value-added services. Warehousing services lead the segment, accounting for approximately 42% of total adoption due to the growing need for inventory storage, order fulfillment, and distribution center operations. Transportation management follows with around 28% share, driven by demand for optimized freight movement and route planning. However, value-added services, including packaging, labeling, and reverse logistics, are the fastest-growing segment with an estimated growth rate exceeding 6% annually, supported by rising customization needs in e-commerce and retail sectors. Distribution services and other specialized logistics solutions collectively contribute nearly 30% of the segment, offering niche capabilities such as cross-docking and last-mile delivery optimization. Increasing adoption of integrated logistics platforms is enhancing coordination across these service types.

Applications in the contract logistics market include retail, e-commerce, healthcare, automotive, and industrial manufacturing. Retail and e-commerce dominate with a combined share of approximately 55%, driven by high order volumes and increasing consumer expectations for faster delivery. Healthcare applications account for nearly 18% of adoption, supported by demand for cold chain logistics and strict regulatory compliance for pharmaceutical distribution. Automotive logistics represents around 12%, focusing on just-in-time inventory and supply chain synchronization. E-commerce applications are the fastest-growing segment, with an estimated growth rate above 7% annually, fueled by rising online sales penetration and expanding last-mile delivery networks. Industrial manufacturing and other applications contribute the remaining 15%, supporting bulk transportation and supply chain optimization.

End-users in the contract logistics market include large enterprises, small and medium-sized enterprises (SMEs), and specialized industry operators. Large enterprises lead with approximately 60% share, leveraging contract logistics for global supply chain management, high-volume distribution, and advanced automation integration. SMEs account for nearly 25% of adoption, increasingly outsourcing logistics functions to reduce operational complexity and improve scalability. SMEs represent the fastest-growing segment, with an estimated growth rate exceeding 6.5% annually, driven by the need for cost-efficient logistics solutions and access to advanced technologies without heavy capital investment. Specialized operators, including healthcare and cold chain providers, contribute the remaining 15%, focusing on niche, high-value logistics services.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America operates over 1.8 billion square feet of warehouse capacity, while Europe holds approximately 28% share supported by cross-border logistics networks. Asia-Pacific contributes nearly 30% of global logistics demand, driven by manufacturing output exceeding 45% of global production. South America accounts for around 4%, while the Middle East & Africa collectively contribute close to 2%, with logistics investments exceeding USD 15 billion in infrastructure and smart warehousing projects across key economies.

North America holds approximately 36% market share, driven by strong demand from e-commerce, retail, and healthcare sectors. Regulatory frameworks supporting supply chain resilience and infrastructure funding exceeding USD 1 trillion have strengthened logistics networks. Over 45% of warehouses in the region use automation technologies such as robotics and AI-based inventory systems. A major logistics provider has implemented autonomous mobile robots across 200+ facilities, improving order processing speed by 25%. Consumer behavior shows high enterprise adoption, with over 60% of large organizations outsourcing logistics to optimize costs and delivery timelines.

Europe accounts for nearly 28% of the contract logistics market, with key contributions from Germany, the UK, and France. Regulatory mandates targeting carbon neutrality have led to over 35% adoption of green logistics practices, including electric fleets and energy-efficient warehouses. The European Union’s sustainability directives have pushed logistics firms to reduce emissions by up to 20%. Over 40% of logistics providers in the region have integrated digital supply chain platforms. A leading regional player has expanded its electric delivery fleet by 30%, reducing urban emissions significantly. Consumer behavior reflects strong preference for environmentally compliant logistics solutions.

Asia-Pacific ranks as the fastest-growing region, contributing nearly 30% of global demand, led by China, India, and Japan. Manufacturing output in the region exceeds 45% of global production, driving large-scale logistics requirements. Infrastructure investments surpass USD 500 billion, supporting ports, highways, and smart warehouses. Over 50% of logistics firms are adopting digital platforms for real-time tracking and analytics. A regional logistics company expanded automated fulfillment centers by 35%, enhancing delivery efficiency by 20%. Consumer behavior is driven by e-commerce growth, with online retail penetration exceeding 25% in major economies.

South America holds around 4% of the global contract logistics market, with Brazil and Argentina as key contributors. Infrastructure investments exceeding USD 80 billion are improving transportation networks and port connectivity. Government trade policies promoting exports have increased logistics demand by nearly 15% in recent years. Energy and agriculture sectors play a significant role in driving logistics activities. A regional logistics firm has expanded warehouse capacity by 18%, supporting agricultural exports. Consumer behavior reflects growing demand for efficient distribution networks, particularly in urban areas experiencing rapid population growth.

The Middle East & Africa region contributes approximately 2% of the global market, with strong demand from oil & gas, construction, and retail sectors. Countries such as the UAE and South Africa are investing over USD 50 billion in logistics infrastructure and free trade zones. Technological modernization, including smart warehouses and automated tracking systems, is being adopted by over 25% of logistics providers. A regional operator has implemented digital freight platforms, improving shipment tracking accuracy by 30%. Consumer behavior is evolving toward faster delivery expectations and increased reliance on organized retail supply chains.

United States Contract Logistics Market – 32% share, supported by extensive warehouse infrastructure and high adoption of advanced logistics technologies across industries.

China Contract Logistics Market – 21% share, driven by large-scale manufacturing output and rapid expansion of e-commerce and digital logistics platforms.

The contract logistics market is highly competitive and moderately fragmented, with over 150 active global and regional players competing across transportation, warehousing, and value-added services. The top five companies collectively account for approximately 45% of the market, indicating a balanced mix of consolidation and regional competition. Leading players are focusing on strategic partnerships, mergers, and acquisitions to expand geographic presence and service capabilities.

Digital transformation remains a key competitive factor, with more than 50% of major logistics firms investing heavily in automation, artificial intelligence, and real-time tracking systems. Companies are deploying robotics across distribution centers, improving operational efficiency by up to 30% and reducing order processing time by 20%. Sustainability is another critical differentiator, with over 40% of firms adopting green logistics initiatives such as electric fleets and energy-efficient warehouses.

Additionally, regional players are strengthening their positions by offering customized logistics solutions tailored to local market needs. Increasing investments in cold chain logistics, which have grown by over 20% in recent years, are further intensifying competition. The market continues to evolve with innovation, scalability, and service diversification shaping long-term competitive dynamics.

DHL Supply Chain

Kuehne + Nagel

DB Schenker

XPO Logistics

Nippon Express

CEVA Logistics

Ryder System

GEODIS

Expeditors International

DSV A/S

Penske Logistics

Hellmann Worldwide Logistics

Advanced technologies are rapidly transforming the contract logistics market, enhancing operational efficiency, visibility, and scalability. Warehouse automation has reached significant adoption, with over 40% of large distribution centers deploying robotics for picking, sorting, and palletizing, improving throughput by up to 30%. Autonomous mobile robots (AMRs) are increasingly used, reducing labor dependency by nearly 25% and improving order accuracy beyond 99%.

Artificial intelligence and predictive analytics are enabling demand forecasting accuracy improvements of up to 35%, minimizing stockouts and excess inventory. Internet of Things (IoT) devices are widely integrated into supply chains, with more than 50% of logistics providers using real-time tracking systems to monitor shipments, reducing delays by approximately 20%. Blockchain technology is gaining traction, with around 15% adoption among global players to enhance transparency and traceability in high-value sectors such as pharmaceuticals and food logistics.

Digital twin technology is emerging as a strategic tool, allowing simulation of logistics operations and improving network optimization by nearly 18%. Additionally, cloud-based logistics platforms are now utilized by over 55% of providers, enabling seamless coordination across global supply chains and supporting data-driven decision-making for improved operational resilience.

• In March 2025, DHL Supply Chain expanded its warehouse automation program across North America by deploying over 1,000 additional autonomous mobile robots, improving order picking efficiency by 25% and reducing manual labor dependency across multiple fulfillment centers. Source: www.dhl.com

• In September 2024, Kuehne+Nagel launched a digital logistics platform integrating AI-based predictive analytics to optimize inventory and transportation planning, enabling customers to reduce supply chain disruptions by 20% and improve delivery reliability across global operations. Source: www.kuehne-nagel.com

• In January 2025, DB Schenker announced the expansion of its electric vehicle fleet in Europe, adding over 1,500 electric delivery trucks to support last-mile logistics, contributing to a 15% reduction in carbon emissions across urban distribution networks. Source: www.dbschenker.com

• In November 2024, XPO Logistics introduced an advanced warehouse management system powered by machine learning, increasing inventory accuracy to 99% and reducing order processing time by 18% across its key distribution hubs. Source: www.xpo.com

The contract logistics market report provides a comprehensive analysis of key operational segments, including transportation management, warehousing, distribution, and value-added services such as packaging and reverse logistics, collectively supporting over 70% of global supply chain outsourcing activities. The report evaluates applications across major industries including retail, e-commerce, healthcare, automotive, and industrial manufacturing, with retail and e-commerce contributing more than 50% of logistics demand.

Geographically, the scope covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing diverse logistics infrastructure capacities ranging from over 1.8 billion square feet of warehousing in North America to rapidly expanding smart logistics hubs in Asia-Pacific. The report also analyzes technological advancements such as automation, artificial intelligence, IoT-enabled tracking, and blockchain integration, which are adopted by over 50% of logistics providers globally.

Additionally, the study includes emerging segments such as cold chain logistics, which has expanded by over 20% in recent years, and sustainable logistics solutions, with more than 40% of companies implementing green initiatives. The report delivers actionable insights for decision-makers by addressing evolving supply chain strategies, operational efficiencies, and future-ready logistics frameworks.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DHL Supply Chain, Kuehne + Nagel, DB Schenker, XPO Logistics, Nippon Express, CEVA Logistics, Ryder System, GEODIS, Expeditors International, DSV A/S, Penske Logistics, Hellmann Worldwide Logistics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |