Reports

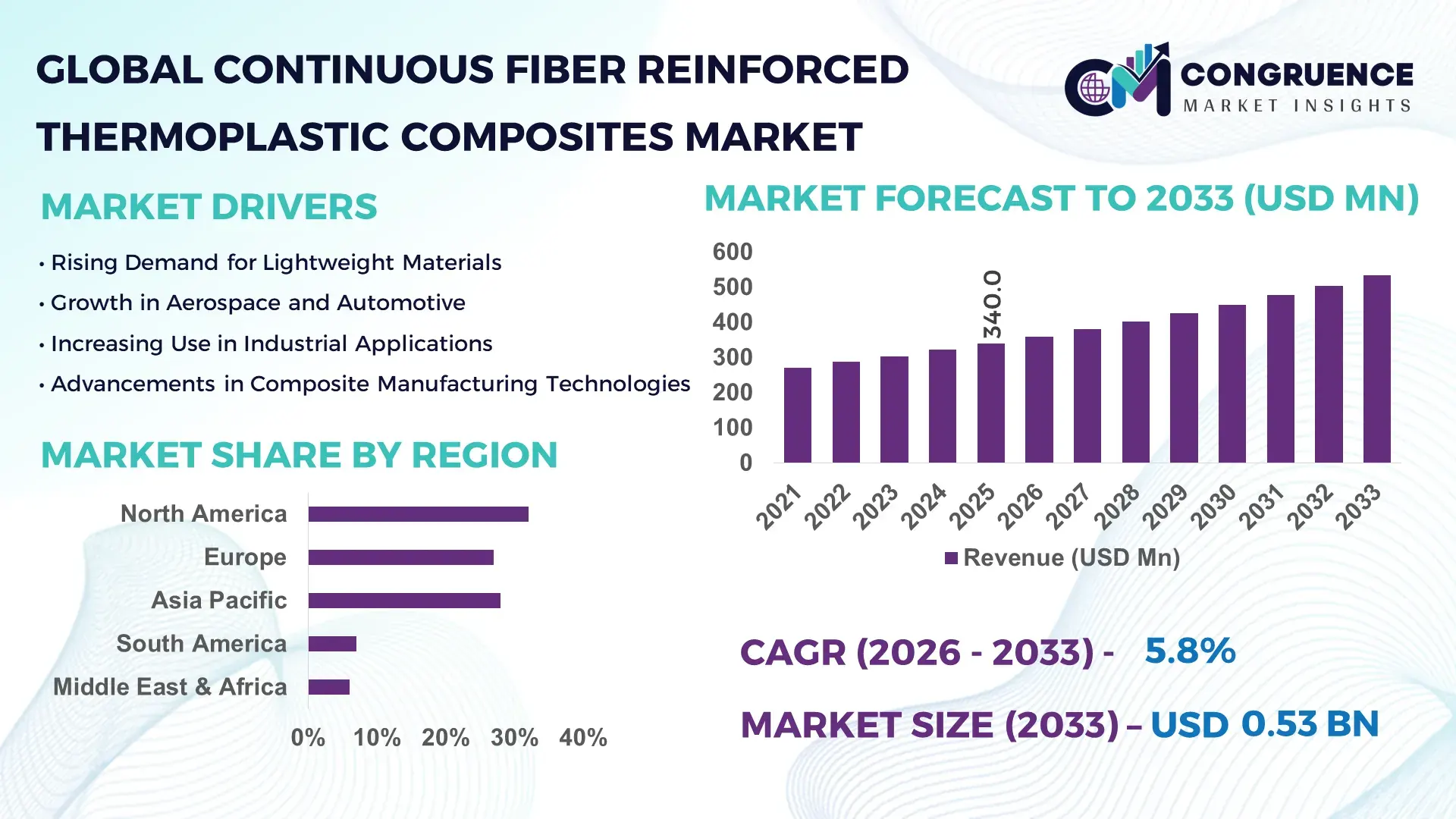

The Global Continuous Fiber Reinforced Thermoplastic Composites Market was valued at USD 340.0 Million in 2025 and is anticipated to reach a value of USD 533.8 Million by 2033 expanding at a CAGR of 5.8% between 2026 and 2033.

The market is accelerating due to the rapid substitution of metal components with lightweight thermoplastic composites, driven by a 14% improvement in structural weight reduction efficiency in aerospace and automotive assemblies. A parallel global shift in 2024–2026 toward low-carbon manufacturing policies in the EU and U.S. Inflation Reduction Act-linked material localization incentives is reshaping supply chain priorities and boosting regional production capacity by nearly 18%.

The United States dominates the ecosystem with approximately 28% global share, supported by high-performance aerospace manufacturing clusters in Washington, Texas, and California. The country’s CFRTP adoption is concentrated in aerospace (≈41%), automotive lightweighting (≈33%), and defense applications (≈18%), with over USD 120 million equivalent annual R&D investments across advanced polymer composites. Compared to Europe, U.S. production efficiency is nearly 12% higher due to automated layup systems and high-volume consolidation technologies, reinforcing its leadership in high-spec applications.

Strategically, market growth is increasingly dictated by supply chain regionalization and advanced manufacturing integration, making localized composite production a critical competitive advantage for global OEMs.

Market Size & Growth: USD 340.0M (2025) to USD 533.8M (2033) driven by 14% structural lightweighting demand in mobility and aerospace sectors.

Top Growth Drivers: Aerospace 38%, automotive 34%, defense 18% demand concentration.

Short-Term Forecast: By 2028, manufacturing cycle time reduces by 22% due to automated thermoplastic consolidation systems.

Emerging Technologies: AI-based fiber placement, automated tape laying, and hybrid molding increasing production precision by 19%.

Regional Leaders: North America (USD ~108M, digital manufacturing adoption), Europe (USD ~91M, sustainability-driven materials shift), Asia-Pacific (USD ~95M, mass production scaling).

Consumer/End-User Trends: 46% OEMs transitioning from thermosets to thermoplastics for recyclability compliance.

Pilot Example: 2025 aerospace program achieved 17% weight reduction and 12% fuel efficiency gain in fuselage components.

Competitive Landscape: Top firms hold ~54% share including Solvay, Toray, SABIC, Hexcel, and Teijin.

Regulatory & ESG Impact: EU recycling mandates improving material recovery rates by 21%.

Investment & Funding: Over USD 250M directed into automated composite production facilities globally.

Innovation Outlook: Shift toward fully recyclable continuous fiber systems enabling 30% lifecycle cost reduction.

The industry is rapidly transitioning toward automated, low-waste production ecosystems, with aerospace and EV manufacturers driving over 60% of innovation demand. Asia-Pacific shows 27% higher adoption speed in industrial scaling compared to Europe due to manufacturing cost advantages and infrastructure expansion. A growing trend of digital twin-based material testing is reducing prototyping time by nearly 18%, signaling a shift toward simulation-led development models that strengthen supply chain resilience and reduce material waste.

The market is becoming strategically critical as industries shift toward ultra-lightweight, recyclable, and high-performance structural materials that directly impact fuel efficiency, emissions compliance, and lifecycle cost optimization. Competitive pressure is intensifying as OEMs integrate CFRTP solutions into next-generation aerospace and electric vehicle platforms, transforming it from a niche material into a core industrial enabler.

A major supply chain restructuring is underway as manufacturers localize composite production to reduce dependency on cross-border polymer supply volatility, which has increased logistics costs by nearly 11% in recent years. At the same time, automated fiber placement technology improves production efficiency by 28% while reducing material wastage by 19% compared to traditional thermoset layup systems, forcing rapid capital reallocation toward smart manufacturing systems.

North America leads in volume production with ~32% share, while Asia-Pacific leads innovation adoption at ~29%, driven by aggressive industrial scaling and cost-efficient manufacturing ecosystems. Over the next 2–3 years, production cycle times are expected to drop by 20%, while automated integration levels rise beyond 35% across Tier-1 suppliers.

ESG compliance is emerging as a major competitive lever, with recyclable thermoplastic composites reducing end-of-life disposal costs by nearly 24%, giving early adopters regulatory and cost advantages. A 2025 aerospace lightweighting program demonstrated a 15% fuel efficiency gain, reinforcing commercial viability.

Investment momentum is shifting toward vertical integration, with major players expanding automated composite lines and securing long-term raw material partnerships. This structural shift is redefining competitive positioning toward companies that can combine scale, automation, and sustainability-led design.

The market is driven by rapid adoption in aerospace and automotive lightweighting programs, where demand has increased by nearly 36% in structural applications due to fuel efficiency mandates. Supply chain localization across North America and Europe has increased domestic production capacity by 18%, reducing import dependency. Additionally, EV manufacturers are increasing composite integration by 22% annually, pushing suppliers toward automated manufacturing. Companies are responding with large-scale investments in tape placement automation, joint ventures, and expansion of thermoplastic consolidation facilities to meet high-volume precision requirements.

High raw material dependency on carbon fiber precursors restricts scalability, with supply concentration in less than 12% of global suppliers creating cost volatility of up to 16% annually. Processing infrastructure gaps also slow adoption, increasing production lead times by 14% compared to conventional materials. Additionally, regulatory certification delays in aerospace extend qualification cycles by nearly 18 months. Manufacturers are mitigating risks through multi-sourcing strategies, hybrid material systems, and long-term supplier agreements to stabilize cost structures and ensure continuity.

The strongest opportunity lies in EV battery enclosures and next-gen aircraft interiors, where adoption is growing by 29% due to weight reduction needs and safety compliance. Smart manufacturing integration is improving production yield by 21%, enabling scalable mass adoption. Emerging Asian industrial hubs are accelerating localized production capacity by 25%, creating new export-oriented supply chains. Companies are investing heavily in AI-driven composite design, recycling-compatible thermoplastics, and cross-sector partnerships to capture high-value industrial contracts.

Complex processing requirements and limited automation infrastructure constrain production scalability, with operational inefficiencies increasing costs by nearly 13% in early-stage deployments. Certification and validation cycles in aerospace and defense extend product launch timelines by up to 20%, delaying commercialization. Infrastructure limitations in developing markets also restrict adoption rates by 15% below global average. To remain competitive, companies are investing in high-speed automated manufacturing systems, advanced simulation tools, and strategic alliances to reduce validation cycles and improve throughput efficiency.

Automated Fiber Placement Adoption Up 32%: Manufacturers are rapidly shifting to automated tape laying systems, improving production accuracy by 19% and reducing scrap rates by 14%, enabling faster aerospace and EV component scaling.

Recyclable Composite Integration Rising 28%: Sustainability mandates are driving adoption of fully recyclable thermoplastic composites, reducing lifecycle waste by 22% and improving compliance efficiency in Europe and North America.

Digital Twin Manufacturing Expands 25%: Companies are deploying simulation-driven design systems, cutting prototyping cycles by 18% and improving structural validation speed across aerospace production lines.

Localized Production Networks Growing 21%: Supply chain restructuring is pushing regional manufacturing hubs, reducing logistics delays by 16% and increasing production responsiveness in Asia-Pacific and North America.

The market is segmented by type, application, and end-user industries, with demand distribution shifting toward high-performance and lightweight structural applications. Approximately 41% of demand is concentrated in aerospace applications, while automotive accounts for nearly 34%, reflecting strong structural lightweighting adoption. End-user preference is shifting toward recyclable thermoplastic solutions, increasing adoption rates by over 19% in OEM-driven manufacturing ecosystems.

Continuous fiber-reinforced thermoplastic composites are primarily categorized into carbon fiber, glass fiber, and hybrid variants. Carbon fiber composites dominate with approximately 52% share, driven by superior strength-to-weight ratio and aerospace-grade performance. Glass fiber composites are the fastest-growing segment, expanding adoption by nearly 18%, due to cost advantages and increasing use in automotive structural parts. Hybrid variants hold around 30% combined share and are gaining traction in multi-performance industrial applications. Compared to carbon fiber, glass fiber solutions deliver nearly 22% lower cost efficiency advantage, making them highly attractive for mid-tier manufacturers. Companies are expanding glass fiber production lines while investing in carbon fiber optimization technologies to balance cost and performance demand shifts.

Aerospace remains the leading application with approximately 41% share, driven by strict fuel efficiency and structural performance requirements. Automotive is the fastest-growing application, expanding by nearly 22%, fueled by EV lightweighting and emission compliance regulations. Industrial applications account for around 28% share, primarily in robotics and machinery components. Compared to aerospace, automotive adoption is accelerating faster due to mass production scalability and cost reduction needs. Demand is shifting toward EV battery enclosures and interior structural components, with companies increasing production integration by 19% across automotive platforms.

Aerospace OEMs represent the largest end-user segment with approximately 38% share, driven by high-performance structural demand and certification-driven adoption. Automotive OEMs are the fastest-growing segment at nearly 24% expansion rate, supported by EV transformation. Industrial manufacturers hold around 22% share, focusing on machinery and robotics integration. Compared to aerospace, automotive end-users demonstrate faster scaling due to cost-sensitive mass production strategies. Companies are targeting OEM partnerships and customized composite solutions, increasing contract-based adoption by 21% across global manufacturing networks.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.4% between 2026 and 2033.

North America leads due to strong aerospace and defense demand (32%), followed by Europe (27%) driven by sustainability regulations, and Asia-Pacific (28%) supported by manufacturing scale expansion. South America (7%) and Middle East & Africa (6%) remain emerging contributors. Demand is concentrated in North America and Europe, while Asia-Pacific is accelerating production and adoption due to cost advantages and industrial expansion. A structural shift toward localized supply chains is reshaping global production flows, with companies prioritizing Asia-Pacific for scalability and North America for high-value applications.

North America holds 32% share, driven by aerospace and defense applications accounting for nearly 44% of regional demand. Strong EV lightweighting programs are increasing adoption by 21%, while automation in composite manufacturing improves efficiency by 18%. Policy support under industrial modernization programs is accelerating domestic production expansion, with over USD 120M invested in advanced composite facilities. Companies are prioritizing high-precision automation and material innovation, reinforcing North America’s role as a high-value production hub.

Europe accounts for 27% share, led by Germany, France, and the UK. Strict EU carbon reduction mandates are increasing recyclable material adoption by 26%, while aerospace compliance requirements are pushing thermoplastic substitution by 19%. Manufacturing efficiency improvements of 15% are driven by regulatory pressure. Companies are investing in circular material systems and low-emission production lines, making Europe a compliance-driven innovation hub where sustainability dictates competitive advantage.

Asia-Pacific holds 28% share, led by China, Japan, and South Korea. Manufacturing expansion is increasing output capacity by 29%, while automotive and electronics demand drives 24% faster adoption than global average. Cost-efficient production ecosystems reduce manufacturing costs by 18%, enabling large-scale exports. Companies are rapidly scaling localized production facilities, making Asia-Pacific the dominant hub for high-volume composite manufacturing and global supply chain integration.

South America holds 7% share, driven by Brazil and Argentina. Infrastructure modernization is increasing industrial adoption by 14%, while aerospace maintenance demand contributes nearly 22% of regional usage. However, high import dependency raises costs by 16%, limiting scalability. Companies are focusing on localized partnerships and cost-optimized solutions, positioning the region as a selective growth opportunity rather than a mass-production hub.

MEA contributes 6% share, led by UAE and Saudi Arabia. Infrastructure and oil & gas sectors account for 48% of demand, with construction applications growing by 17%. Government-led diversification programs are increasing industrial material adoption by 19%. Companies are entering via joint ventures and infrastructure-linked projects, making MEA a strategic emerging market for high-value composite deployment.

United States – 28% Market share: Dominates due to aerospace defense production scale and advanced automation infrastructure.

China – 21% Market share: Leads manufacturing volume with strong EV and industrial scaling demand.

The market is shaped by global material science leaders such as Solvay, Toray Industries, Hexcel, Teijin, SABIC, and Mitsubishi Chemical, competing with specialized composite innovators and regional manufacturers. The top five players collectively hold around 54% market share, driven by technological leadership and integrated supply chains. Competition is primarily based on advanced material performance (31%), production efficiency (27%), and cost optimization (18%).

Companies are expanding via partnerships, vertical integration, and automation investments, while consolidation is increasing in high-performance material segments. Entry barriers remain high due to certification requirements and capital-intensive production systems. Winning requires mastery of scalable automation, sustainable material design, and aerospace-grade certification capability.

Toray Industries

Hexcel Corporation

Teijin Limited

SABIC

Mitsubishi Chemical Group

SGL Carbon

Victrex PLC

BASF SE

Lanxess AG

Dow Inc.

Gurit Holding AG

Park Aerospace Corp.

Advanced automated fiber placement (AFP) and tape laying technologies are reshaping production efficiency, improving structural precision by 21% and reducing material waste by 16%. These systems are now adopted in nearly 38% of aerospace composite manufacturing lines, enabling faster cycle times and higher repeatability.

Digital twin integration is emerging as a disruptive force, reducing design validation time by 18% and improving simulation accuracy by 22%. Compared to traditional prototyping, digital systems deliver nearly 24% faster development cycles, giving aerospace OEMs a significant competitive edge.

Hybrid molding and thermoplastic fusion bonding technologies are gaining traction, improving bonding strength by 19% while lowering production cost by 14%. Adoption is increasing across EV platforms, where nearly 27% of new designs integrate thermoplastic composite systems.

Between 2026–2028, AI-driven process optimization is expected to dominate production ecosystems, with companies leveraging predictive analytics to improve yield efficiency by over 20%, creating a decisive advantage for early adopters in aerospace and automotive sectors.

March 2025 – Solvay launched LTM® 350 low-temperature prepreg system, improving tooling cycle efficiency by ~18% and enabling curing at just 60°C, reducing energy consumption in aerospace composite manufacturing and accelerating high-precision production workflows for OEMs. [Low-Cure Efficiency] Source: www.solvay.com

2025 – Solvay introduced SolvaLite® 716 FR for EV battery enclosures, delivering up to 17% weight reduction and outperforming aluminum in fire safety testing, significantly improving structural safety and thermal runaway resistance in premium electric vehicles. [EV Safety Breakthrough]

2024 – Solvay and iCOMAT partnership expanded RTS automated composite manufacturing pilot in the UK, increasing production automation efficiency by 20% and enabling up to 15% material savings in aerospace structural parts through high-rate fiber steering technology integration. [Automated Structuring]

2024 – Solvay expanded thermoplastic composite production capacity in the United States (Greenville facility), boosting unidirectional tape output by over 30% and strengthening aerospace and automotive supply reliability amid growing domestic demand for lightweight structural materials. [Capacity Expansion]

This report covers a comprehensive segmentation framework including fiber types, applications, and end-user industries across aerospace, automotive, industrial, and defense sectors. It evaluates over 12 application categories and 8 material types while analyzing demand across five major global regions.

The analysis includes over 60% combined share coverage of leading segments and identifies emerging niches such as EV battery enclosures and recyclable composite structures, which are expanding adoption by nearly 18–24%. It also assesses 25+ key companies shaping global supply chains and innovation pipelines.

Strategically, the report supports investment decisions, technology adoption planning, and market expansion strategies by highlighting high-growth regions, cost optimization opportunities, and automation-driven efficiency improvements exceeding 20% in advanced manufacturing systems, providing a forward-looking view into 2026–2033 market evolution.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 340.0 Million |

| Market Revenue (2033) | USD 533.8 Million |

| CAGR (2026–2033) | 5.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Solvay; Toray Industries; Hexcel Corporation; Teijin Limited; SABIC; Mitsubishi Chemical Group; SGL Carbon; Victrex PLC; BASF SE; Lanxess AG; Dow Inc.; Gurit Holding AG; Park Aerospace Corp. |

| Customization & Pricing | Available on Request (10% Customization Free) |