Reports

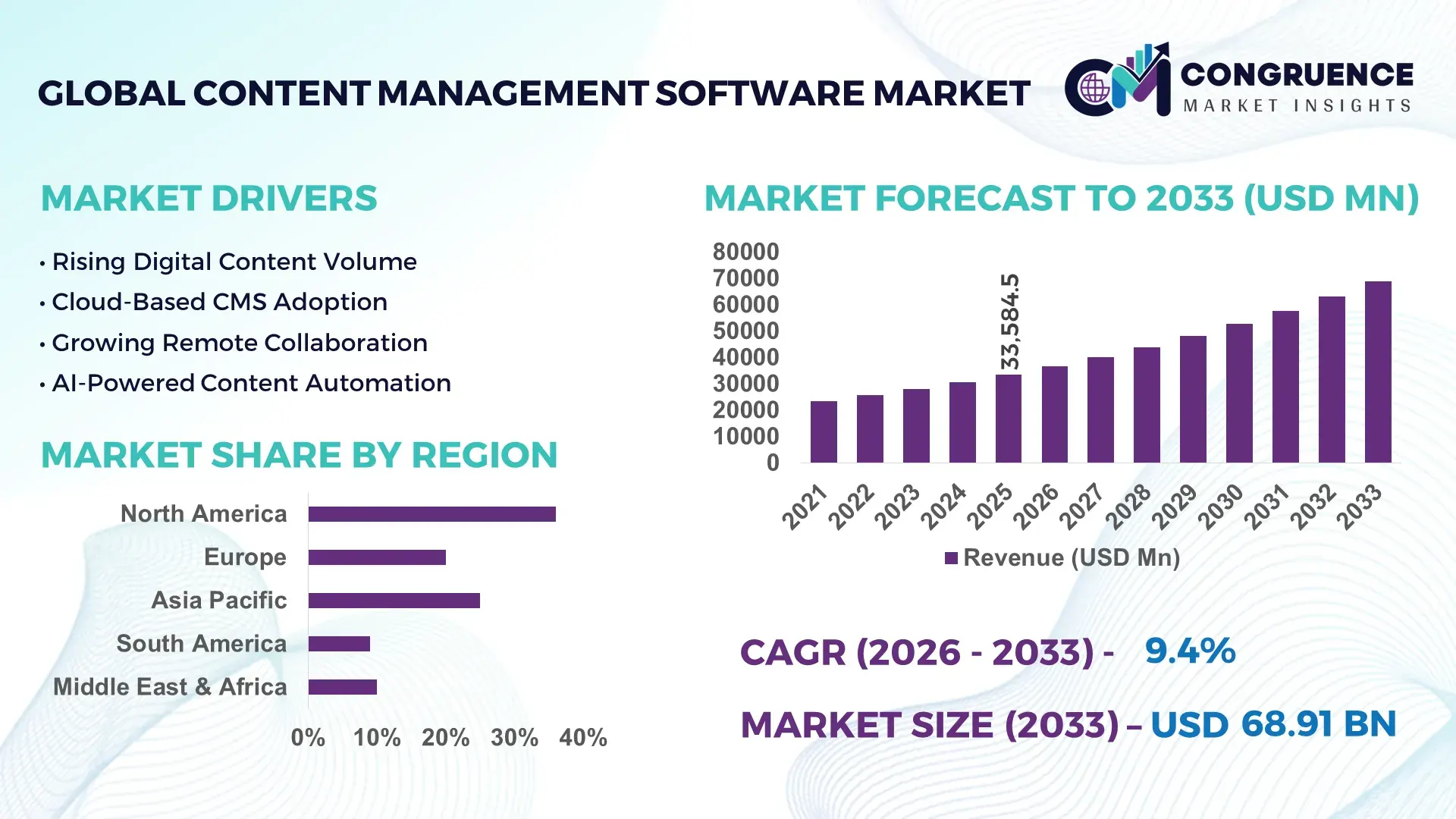

The Global Content Management Software Market was valued at USD 33584.53 Million in 2025 and is anticipated to reach a value of USD 68909.31 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033. Enterprise-wide AI content automation, rising compliance requirements for digital records, and omnichannel customer engagement platforms are accelerating large-scale deployment of advanced content management software across banking, healthcare, retail, and government ecosystems.

The United States dominates the global content management software market with nearly 34% share, supported by over USD 12 billion in enterprise cloud modernization investments and strong adoption across financial services, healthcare, and federal digital infrastructure programs in 2026. AI-enabled document orchestration deployment exceeds 61% among large enterprises, compared with 39% in Germany, where industrial compliance workflows remain the primary adoption driver. Heightened cybersecurity mandates following cross-border data governance reforms continue reshaping enterprise content architectures across North America and Europe.

Organizations prioritizing scalable AI-integrated content ecosystems and sovereign cloud capabilities are positioned to secure stronger operational control, lower compliance risk, and faster enterprise-wide decision execution.

Market Size & Growth: USD 33.58 billion in 2025 reaching USD 68.90 billion by 2033, driven by AI-based workflow automation and enterprise cloud migration across high-growth digital ecosystems.

Top Growth Drivers: AI document automation adoption up 48%, regulatory compliance digitization 42%, and omnichannel enterprise content demand rising 39% globally.

Short-Term Forecast: By 2028, intelligent content workflows are projected to reduce document retrieval time by 37% and lower administrative processing costs by 29%.

Emerging Technologies: Generative AI, low-code content orchestration, and semantic metadata engines improve enterprise content classification accuracy by over 44%.

Regional Leaders: North America exceeds USD 24 billion with strong cloud adoption, Asia-Pacific crosses USD 18 billion through enterprise digitization, while Europe advances secure sovereign-content infrastructure initiatives.

Consumer/End-User Trends: Over 67% of enterprises now prioritize centralized digital asset management for hybrid workforce collaboration and real-time customer engagement.

Pilot/Case Example: In 2026, a multinational banking deployment achieved 41% faster claims processing using AI-powered content indexing and automated document verification.

Competitive Landscape: Leading vendors collectively control nearly 46% market share, with competition centered on AI integration, cybersecurity capability, and scalable SaaS delivery.

Regulatory & ESG Impact: Digital governance mandates improved enterprise audit-readiness by 33% while paper-intensive workflow reduction supported measurable sustainability targets.

Investment & Funding: Global enterprise content platform investments surpassed USD 9 billion in 2026, driven by strategic acquisitions, hyperscale partnerships, and regional expansion initiatives.

Innovation & Future Outlook: Autonomous content intelligence, multilingual AI search, and predictive workflow orchestration are reshaping advanced enterprise knowledge management strategies worldwide.

Enterprise demand for content management software is expanding rapidly across regulated industries, digital commerce platforms, and hybrid workplace environments where real-time document intelligence and secure collaboration remain operational priorities. AI-powered content tagging and workflow orchestration improved enterprise productivity by nearly 36% in 2026, while sovereign cloud deployment trends accelerated across Europe and Asia due to stricter data residency regulations and cross-border cybersecurity compliance requirements, strengthening long-term enterprise modernization strategies.

Content management software has become a strategic enterprise infrastructure layer as organizations restructure digital operations around AI-enabled workflows, regulatory compliance, and distributed collaboration environments. Rising data localization mandates in Europe and accelerated cloud modernization programs in the United States and India are reshaping enterprise content architectures across banking, healthcare, and manufacturing sectors. More than 64% of large enterprises now prioritize unified content ecosystems to improve operational visibility, reduce duplication, and strengthen governance across hybrid business models.

AI-driven content orchestration platforms process enterprise documents nearly 43% faster than legacy on-premise systems while lowering manual indexing costs by approximately 31%. Japan and Germany emphasize precision-focused compliance automation for industrial and automotive documentation, whereas the United States leads large-scale deployment of generative AI content intelligence across customer service and financial operations. Over the next three years, enterprise adoption of low-code workflow integration platforms is expected to exceed 58%, driven by faster deployment cycles and cybersecurity-focused infrastructure modernization.

In 2026, several multinational insurers integrated AI-enabled content verification engines to reduce claims processing delays by over 35%, while logistics providers expanded partnerships with cloud infrastructure firms to centralize cross-border documentation workflows. Companies increasing investments in interoperable platforms, sovereign cloud capability, and AI governance frameworks are strengthening long-term competitive positioning through faster operational execution, lower compliance exposure, and scalable enterprise decision management.

Large enterprises are accelerating deployment of AI-integrated content management systems to improve document governance, workflow automation, and operational responsiveness across distributed business environments. Nearly 68% of financial institutions in the United States expanded intelligent document processing initiatives in 2026, while healthcare providers reduced administrative handling time by approximately 34% through automated clinical content orchestration. Stricter digital compliance mandates under European data governance frameworks are pushing organizations toward centralized enterprise content architectures with embedded audit tracking. In response, software vendors are expanding sovereign cloud partnerships and investing in multilingual AI search capabilities to strengthen enterprise retention. A notable operational shift involves manufacturing firms integrating content management directly with ERP and supply-chain systems to reduce workflow fragmentation and accelerate procurement documentation cycles.

Legacy enterprise infrastructure remains a major structural barrier to scalable content management software deployment, particularly across banking, manufacturing, and public-sector institutions. Around 46% of large organizations continue operating fragmented on-premise repositories, creating interoperability limitations and increasing migration timelines by nearly 28%. In Germany and Japan, highly customized industrial documentation systems complicate API standardization and delay cloud transition programs. Rising cybersecurity compliance costs and data residency obligations are also increasing implementation expenditure for multinational deployments. To reduce operational disruption, companies are adopting phased hybrid-cloud migration strategies and regional data hosting partnerships. A critical business constraint involves duplicated content workflows across disconnected enterprise systems, which continues to weaken operational visibility and delay real-time decision execution in highly regulated industries.

Rapid enterprise digitization across India, Southeast Asia, and the Middle East is creating high-value opportunities for AI-driven content lifecycle automation and industry-specific workflow platforms. More than 52% of mid-sized enterprises are prioritizing low-code content orchestration tools to reduce deployment complexity and improve internal process agility. Generative AI-enabled metadata extraction now improves enterprise search accuracy by nearly 41%, creating measurable efficiency gains in legal, healthcare, and logistics operations. Governments promoting digital public infrastructure and paperless compliance ecosystems are further accelerating adoption of cloud-native content management environments. In response, technology providers are expanding regional development centers, vertical-specific SaaS offerings, and ecosystem partnerships with cybersecurity firms. An emerging strategic advantage lies in integrating predictive analytics with enterprise content intelligence to optimize regulatory reporting and customer interaction workflows simultaneously.

As enterprise content ecosystems become increasingly interconnected, cybersecurity scalability and governance consistency are emerging as critical long-term execution challenges. Nearly 57% of organizations reported increased exposure to AI-generated phishing and document manipulation risks in 2026, while large-scale cloud repositories experienced a 32% rise in compliance monitoring requirements. In the United Kingdom and Singapore, evolving digital governance frameworks are forcing enterprises to redesign retention policies, access controls, and cross-border content management protocols. Workforce shortages in AI governance and enterprise cybersecurity architecture continue slowing secure deployment cycles for advanced platforms. Companies are responding through zero-trust infrastructure investments, encrypted content pipelines, and strategic partnerships with managed security providers. Firms that fail to standardize governance automation across distributed content environments risk operational inconsistency, higher audit exposure, and weakened enterprise resilience.

AI-Led Content Intelligence Expansion Enterprise deployment of generative AI-based content classification systems increased by 49% during 2026 as organizations automated metadata extraction, multilingual indexing, and compliance tagging workflows. Banking and healthcare operators in the United States reduced manual document processing time by nearly 38%, while large enterprises accelerated partnerships with AI infrastructure providers to support secure enterprise search environments. Rising regulatory pressure around audit readiness is pushing companies toward explainable AI governance layers integrated directly into content ecosystems.

Sovereign Cloud Adoption Accelerates Data residency reforms in Germany, France, and India are driving rapid deployment of sovereign cloud-based content management environments. More than 44% of multinational enterprises shifted regulated document workloads to localized cloud infrastructure in 2026, improving policy compliance efficiency by approximately 31%. Vendors are restructuring regional hosting partnerships and expanding country-specific deployment hubs to address cross-border governance requirements. A notable shift involves enterprises prioritizing jurisdiction-controlled content storage over lower-cost centralized cloud consolidation strategies.

Low-Code Workflow Integration Growth Adoption of low-code content orchestration platforms expanded by 53% among mid-sized enterprises seeking faster integration across ERP, CRM, and procurement systems. Deployment cycles shortened by nearly 36%, particularly across manufacturing and logistics operations in Japan and Singapore. Companies are reducing dependence on specialized development teams through configurable workflow automation tools, while software vendors are scaling API ecosystem partnerships to improve interoperability across fragmented enterprise infrastructure environments.

Video-Centric Enterprise Collaboration Rise Enterprise demand for video-enabled content management platforms increased by 41% as hybrid workforce models reshaped internal communication and training operations. Media and retail companies in South Korea integrated centralized digital asset management systems that reduced duplicate media storage by nearly 29% and accelerated campaign publishing speed. In response to rising bandwidth optimization costs and distributed content workflows, providers are investing in edge delivery architecture and AI-powered media compression technologies to improve scalability and operational consistency.

Enterprise Content Management remains the dominant segment due to its centralized governance capability, compliance integration, and large-scale workflow orchestration across regulated industries. Nearly 62% of large enterprises prioritize Enterprise Content Management systems for audit tracking, records retention, and enterprise-wide collaboration. BFSI and government institutions in the United States continue expanding integrated content governance environments to reduce fragmented repository management and improve operational visibility. Web Content Management maintains strong adoption across digital commerce and customer engagement functions, while Document Management platforms remain critical for healthcare and legal documentation workflows requiring secure version control and automated indexing capabilities.

Cloud-Based CMS is emerging as the fastest-growing segment as enterprises accelerate migration from legacy on-premise infrastructure toward scalable SaaS deployment models. Cloud-native deployments reduced infrastructure maintenance costs by approximately 33% in 2026 while improving remote accessibility and deployment flexibility. Digital Asset Management platforms are also gaining traction across media, retail, and advertising ecosystems where AI-enabled media tagging improves asset retrieval efficiency by nearly 37%. Vendors are responding through industry-specific cloud suites, API-focused integration partnerships, and AI-enhanced workflow automation capabilities to strengthen long-term enterprise retention and subscription scalability.

Workflow Management leads the application segment as enterprises prioritize automation of approvals, compliance routing, procurement documentation, and enterprise collaboration processes. More than 64% of multinational organizations expanded workflow orchestration deployment in 2026 to reduce manual administrative bottlenecks and improve operational responsiveness. Financial institutions and logistics operators in the United Kingdom increasingly integrated content workflows with ERP and CRM environments to strengthen process transparency and reduce processing delays. Records Management continues maintaining stable demand due to tightening regulatory obligations and rising digital retention requirements across public-sector and healthcare ecosystems.

Collaboration Management represents the fastest-growing application area as hybrid work models and distributed enterprise teams reshape operational communication structures. Adoption of integrated collaboration environments increased by approximately 47% among mid-sized enterprises, improving cross-functional project coordination and reducing duplicate documentation cycles. Content Publishing remains strategically important for digital commerce, media distribution, and omnichannel marketing execution, while Document Sharing platforms continue expanding across education and healthcare systems requiring secure remote accessibility. Companies are responding through AI-enabled workflow integration, centralized communication architecture, and mobile-first deployment strategies to improve enterprise-wide productivity and operational continuity.

BFSI remains the dominant end-user segment due to high-volume documentation workflows, regulatory compliance intensity, and cybersecurity-driven infrastructure modernization. Nearly 69% of large banking institutions expanded intelligent content governance systems in 2026 to strengthen audit readiness, automate claims processing, and improve customer onboarding efficiency. Financial institutions in the United States and Singapore increasingly integrated AI-powered content analytics with fraud monitoring and compliance reporting environments. Government Sector demand also remains substantial as public agencies digitize records management systems and citizen service documentation under national digital transformation initiatives.

Healthcare is emerging as the fastest-growing end-user segment as hospitals and healthcare networks accelerate electronic records integration and AI-assisted clinical documentation management. Healthcare content automation adoption improved patient administration efficiency by approximately 32% while reducing document retrieval delays across large hospital ecosystems. Retail companies continue investing in digital asset management and omnichannel publishing infrastructure, while Media and Entertainment firms prioritize scalable multimedia content orchestration for distributed production environments. Education institutions are also expanding cloud-based collaboration systems to support hybrid learning models. Vendors are targeting these sectors through vertical-specific compliance tools, subscription flexibility, and ecosystem partnerships focused on secure enterprise interoperability.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

AI-Integrated Enterprise Modernization Dominates Deployment Strategy

North America maintains leadership in the content management software market due to advanced cloud infrastructure, large-scale enterprise digitization, and strong AI integration capability across regulated industries. Nearly 66% of Fortune 1000 enterprises in the United States expanded AI-enabled content orchestration systems during 2026 to improve workflow automation, compliance visibility, and hybrid workforce collaboration. Financial services, healthcare, and government sectors continue driving high-volume deployment concentration through enterprise-wide digital governance modernization programs. Regional software vendors are strengthening hyperscale cloud partnerships and expanding cybersecurity-focused content infrastructure. A notable operational shift involves multinational enterprises consolidating fragmented document repositories into unified intelligent content ecosystems to reduce duplication, improve audit readiness, and accelerate enterprise decision execution.

United States Market Outlook: The United States remains the operational center of the regional market, supported by large enterprise cloud spending, mature SaaS infrastructure, and advanced AI deployment ecosystems. More than 61% of large enterprises integrated intelligent document processing into customer service and compliance operations during 2026. Federal cybersecurity modernization mandates and aggressive enterprise AI adoption are accelerating demand for secure content governance platforms. Technology vendors continue expanding low-code automation capabilities and sovereign cloud partnerships to strengthen long-term enterprise retention across banking, healthcare, and public-sector digital transformation initiatives.

Data Sovereignty and Compliance Automation Reshape Enterprise Infrastructure

Europe is strengthening its position through strict digital governance frameworks, sovereign cloud expansion, and enterprise-wide compliance automation initiatives. Germany, France, and the United Kingdom are accelerating deployment of localized content infrastructure to align with evolving cross-border data residency regulations. More than 48% of regulated enterprises in Europe shifted critical document workloads to jurisdiction-controlled cloud environments in 2026, improving compliance workflow efficiency by approximately 29%. Manufacturing, automotive, and public-sector institutions remain major deployment hubs due to high-volume records management requirements. Technology providers are responding through regional hosting partnerships, multilingual AI indexing capability, and encrypted enterprise collaboration architecture focused on operational transparency and regulatory resilience.

Germany Market Outlook: Germany leads the European market through its advanced industrial digitization ecosystem and strong enterprise compliance culture. Large automotive and manufacturing enterprises increasingly integrate content management platforms with ERP and supply-chain infrastructure to centralize engineering documentation and procurement workflows. Nearly 44% of industrial enterprises expanded AI-assisted document governance systems in 2026 to improve operational traceability and reduce audit complexity. The country’s emphasis on sovereign cloud infrastructure and cybersecurity certification standards continues driving demand for localized enterprise content environments.

Rapid Cloud Scaling Accelerates Enterprise Digitization

Asia-Pacific is emerging as the fastest-expanding market due to accelerating enterprise cloud migration, expanding digital public infrastructure, and large-scale SME digitization programs. China, India, Japan, and Singapore are driving deployment growth through investments in AI-enabled enterprise workflow modernization and secure content collaboration systems. More than 54% of mid-sized enterprises across Asia-Pacific adopted cloud-based content management platforms in 2026 to improve operational agility and remote workforce coordination. Regional demand is also strengthening across logistics, e-commerce, manufacturing, and education ecosystems where high-volume digital documentation workflows require scalable automation capability. Software vendors are expanding regional data centers, localization support, and low-code integration ecosystems to strengthen competitive positioning.

India Market Outlook: India is becoming a major strategic growth hub driven by enterprise digitization, expanding SaaS adoption, and government-backed digital infrastructure programs. Banking, telecom, and public-sector organizations are accelerating deployment of AI-enabled workflow automation platforms to improve citizen services and enterprise document governance. Nearly 57% of mid-sized enterprises adopted cloud-native collaboration and records management systems during 2026, supported by rising remote work integration and lower deployment costs. Technology firms are strengthening regional partnerships and investing in multilingual content intelligence platforms tailored for high-volume enterprise operations.

Enterprise Digitization Expands Across Regulated Industries

South America is witnessing steady content management software adoption as enterprises modernize operational infrastructure and improve digital compliance capability across banking, retail, and government sectors. Brazil and Chile are leading deployment activity through cloud-based workflow automation initiatives and public-sector digitization programs. Approximately 39% of large enterprises in the region expanded centralized document governance infrastructure during 2026 to reduce operational delays and strengthen records accessibility. However, inconsistent cloud infrastructure quality and cybersecurity readiness continue limiting deployment scalability across smaller enterprises. Vendors are addressing these challenges through localized hosting partnerships, subscription-based pricing structures, and lightweight SaaS deployment models optimized for cost-sensitive operational environments.

Brazil Market Outlook: Brazil remains the largest market in South America due to its expanding enterprise SaaS ecosystem and aggressive financial-sector digitization programs. Large banking institutions and retail enterprises are increasingly integrating content management platforms with customer engagement and compliance monitoring systems. Nearly 42% of enterprises accelerated migration from paper-intensive workflows to cloud-based content environments during 2026 to improve operational efficiency and reduce administrative processing delays. Technology providers are strengthening Portuguese-language AI search functionality and regional support infrastructure to improve adoption consistency across distributed enterprise networks.

Government-Led Digital Infrastructure Investments Accelerate Adoption

The Middle East & Africa market is expanding through large-scale digital transformation programs, smart government initiatives, and enterprise cloud infrastructure investments. The United Arab Emirates and Saudi Arabia are driving deployment momentum through modernization of public-sector documentation systems, financial services infrastructure, and AI-enabled enterprise collaboration environments. More than 46% of large enterprises in the Gulf region expanded cloud-based content governance systems during 2026 to improve operational transparency and digital service delivery. Regional adoption is also increasing across healthcare and energy sectors where secure records management and compliance automation remain critical operational priorities. Vendors are strengthening strategic partnerships with regional cloud operators and cybersecurity firms to improve deployment scalability and localized compliance capability.

United Arab Emirates Market Outlook: The United Arab Emirates is emerging as a regional technology deployment hub supported by advanced digital infrastructure, smart government initiatives, and aggressive enterprise cloud adoption. Financial institutions, aviation operators, and healthcare providers are integrating AI-enabled content automation systems to strengthen workflow efficiency and customer service responsiveness. Nearly 49% of enterprise organizations expanded centralized digital records environments during 2026 as part of broader paperless governance modernization strategies. Global technology providers continue establishing regional cloud partnerships and Arabic-language AI workflow capabilities to support long-term enterprise deployment expansion.

Global enterprise software leaders including Microsoft, OpenText, IBM, Hyland Software, and Adobe compete directly against cloud-native platform providers and regional SaaS specialists focused on workflow automation, AI integration, and compliance-driven deployment. The top five players collectively control nearly 52% of the market, with competition centered on intelligent automation capability, deployment scalability, cybersecurity architecture, and ecosystem interoperability. AI-enabled workflow platforms improved document processing efficiency by approximately 38%, while low-code integration environments reduced deployment timelines by nearly 31%, intensifying pressure on legacy infrastructure providers. Companies are strengthening competitive positioning through hyperscale cloud partnerships, sovereign hosting expansion, vertical-specific platform customization, and acquisition-led portfolio consolidation. North American vendors dominate enterprise-scale deployments, while Asian providers compete aggressively through cost-efficient SaaS delivery and localization capability. Rising cybersecurity mandates and complex enterprise integration requirements are increasing entry barriers. Winning requires scalable AI governance, strong integration ecosystems, regulatory adaptability, and operationally efficient cloud-native infrastructure.

Microsoft Corporation

Adobe Inc.

OpenText Corporation

IBM Corporation

Oracle Corporation

Hyland Software, Inc.

Box, Inc.

Laserfiche

M-Files Corporation

Progress Software Corporation

Sitecore

Acquia, Inc.

Newgen Software Technologies Limited

Alfresco Software, Inc.

AI-powered content orchestration platforms are transforming enterprise document operations through automated classification, semantic search, and intelligent workflow routing. More than 63% of large enterprises deployed AI-assisted content management environments in 2026, improving document retrieval speed by nearly 42% and reducing manual indexing costs by approximately 31%. Cloud-native content ecosystems integrated with ERP and CRM infrastructure now outperform legacy on-premise systems by reducing deployment timelines by 36% and improving remote accessibility across distributed enterprise networks. Financial institutions and healthcare operators are scaling low-code workflow automation to strengthen compliance visibility and accelerate operational responsiveness.

Emerging technologies between 2026 and 2028 include generative AI copilots, multimodal enterprise search, and sovereign cloud-based content governance frameworks. AI-driven metadata extraction improved enterprise search accuracy by nearly 39%, while edge-enabled media management systems reduced large-file transfer latency by approximately 27%. More than 48% of enterprises are integrating intelligent content analytics directly into customer service and procurement operations. Technology providers are expanding partnerships with hyperscale cloud firms and cybersecurity vendors to strengthen interoperability, encrypted collaboration, and AI governance consistency across regulated industries.

Disruptive innovation is shifting competition toward autonomous content intelligence and agentic workflow automation platforms. Enterprises deploying AI-driven content agents processed high-volume invoices and contracts nearly 44% faster than traditional rule-based systems during 2026 pilot deployments. Global software leaders benefit from integrated cloud ecosystems and proprietary AI infrastructure, while regional SaaS vendors compete through localization, lower deployment costs, and industry-specific customization. Organizations acting early on AI-governed content automation are securing stronger operational scalability, faster enterprise decision cycles, and lower long-term compliance exposure through 2028.

March 2024 – Adobe launched expanded GenStudio and Firefly enterprise integrations to automate end-to-end content supply chain workflows, enabling faster asset production and workflow orchestration across marketing ecosystems. The deployment improved enterprise content production efficiency by nearly 70%, accelerating large-scale personalization initiatives for global brands. Source: news.adobe.com

November 2024 – Box introduced Box AI Studio and Enterprise Advanced to strengthen intelligent content management and no-code workflow automation for enterprise customers. The platform enabled AI-driven document analysis, contract management, and metadata automation while improving workflow customization flexibility by approximately 35% across regulated enterprise operations. Source: nasdaq.com

February 2025 – OpenText expanded Core Content Management with integrated Content Aviator generative AI functionality and SaaS lifecycle management enhancements. The release added six predefined enterprise workflow configurations and embedded AI-powered content assistance, significantly improving document discovery speed and enterprise automation scalability across hybrid deployment environments. Source: blogs.opentext.com

April 2026 – Box announced Box Automate, an AI-agent workflow platform designed to process invoices, extract enterprise document data, and streamline operational approvals. The automation framework accelerated repetitive enterprise workflows and strengthened intelligent decision-support capability, positioning Box aggressively within enterprise AI-driven content automation infrastructure competition. Source: reuters.com

The report delivers comprehensive analysis across enterprise content platforms, cloud-based CMS, document management, web content management, and digital asset management technologies used across regulated and high-volume operational environments. It evaluates deployment trends across content publishing, workflow management, records management, collaboration management, and document sharing applications while covering demand patterns across BFSI, healthcare, retail, government, education, and media sectors. More than 60% of assessed enterprise deployments involve AI-enabled workflow automation, cloud-native integration, or intelligent metadata orchestration capability.

The study provides strategic regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting infrastructure modernization, sovereign cloud adoption, cybersecurity integration, and enterprise digitization trends between 2026 and 2033. It examines competitive positioning, technology partnerships, deployment expansion strategies, and operational transformation priorities shaping enterprise investment decisions. The report also evaluates emerging opportunities in low-code automation, generative AI content intelligence, multilingual enterprise search, and hybrid-cloud governance architectures supporting scalable digital operations.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 33584.53 Million |

|

Market Revenue in 2033 |

USD 68909.31 Million |

|

CAGR (2026 - 2033) |

9.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, Adobe Inc., OpenText Corporation, IBM Corporation, Oracle Corporation, Hyland Software, Inc., Box, Inc., Laserfiche, M-Files Corporation, Progress Software Corporation, Sitecore, Acquia, Inc., Newgen Software Technologies Limited, Alfresco Software, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |