Reports

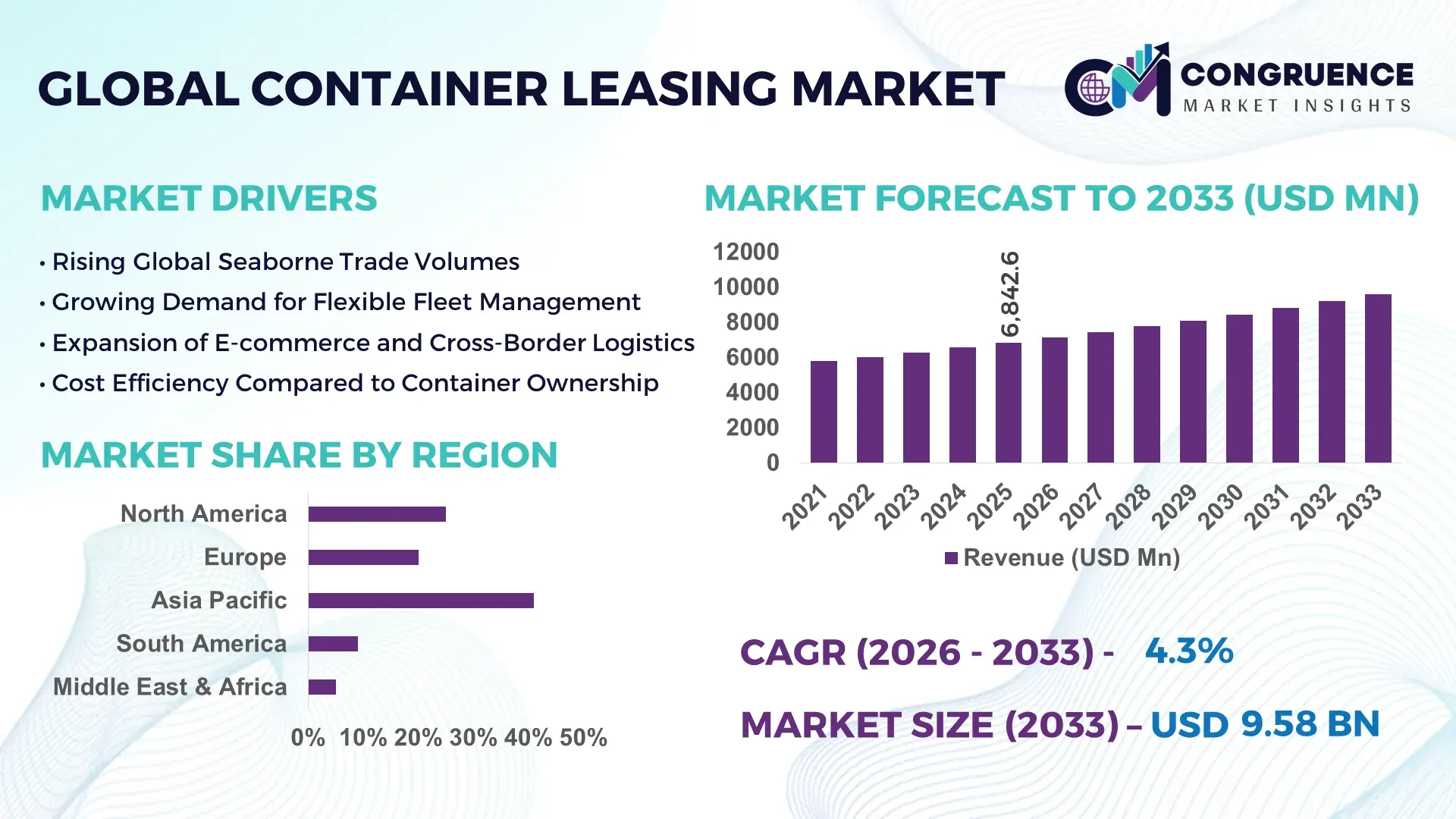

The Global Container Leasing Market was valued at USD 6842.57 Million in 2025 and is anticipated to reach a value of USD 9582.82 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. Rising international seaborne trade volumes and increasing preference for asset-light logistics models are accelerating demand for flexible container leasing solutions across global supply chains.

The United States continues to play a pivotal role in the container leasing ecosystem through strong capital deployment, advanced intermodal infrastructure, and extensive port operations. Major U.S.-based lessors collectively manage container fleets exceeding 15 million TEUs, supporting high-frequency trade routes across Asia-Pacific, Europe, and Latin America. Annual private equity and institutional investments in maritime equipment financing exceed USD 3 billion, strengthening fleet modernization initiatives. Advanced digital fleet tracking systems, IoT-enabled smart containers, and predictive maintenance technologies are increasingly deployed across U.S. ports such as Los Angeles and Long Beach, which together handle over 17 million TEUs annually. Container leasing in the country is widely utilized across retail imports, automotive logistics, and temperature-controlled pharmaceutical supply chains, reinforcing operational efficiency in high-volume trade corridors.

Market Size & Growth: USD 6842.57 Million in 2025, projected to reach USD 9582.82 Million by 2033 at a CAGR of 4.3%, driven by expanding global trade networks and cost-efficient fleet outsourcing strategies.

Top Growth Drivers: 28% rise in e-commerce containerized shipments, 22% increase in intermodal freight adoption, 18% improvement in fleet utilization through leasing models.

Short-Term Forecast: By 2028, optimized fleet management platforms are expected to reduce container idle time by 15% and improve asset turnover rates by 12%.

Emerging Technologies: IoT-enabled smart containers, blockchain-based cargo documentation, AI-driven predictive maintenance systems.

Regional Leaders: Asia-Pacific projected to exceed USD 3.8 Billion by 2033 with strong manufacturing exports; North America to reach USD 2.7 Billion driven by intermodal rail integration; Europe expected to surpass USD 2.1 Billion supported by sustainable logistics initiatives.

Consumer/End-User Trends: Retail, FMCG, automotive, and pharmaceuticals increasingly favor long-term leasing contracts to optimize working capital and enhance supply chain agility.

Pilot or Case Example: In 2024, a large-scale digital container tracking deployment reduced cargo dwell time by 14% and improved real-time visibility across trans-Pacific routes.

Competitive Landscape: Market leader Triton International holds approximately 27% share, followed by Textainer, CAI International, Seaco Global, and Florens Container Leasing.

Regulatory & ESG Impact: IMO emissions targets and carbon reporting mandates are encouraging adoption of energy-efficient refrigerated containers and eco-friendly materials.

Investment & Funding Patterns: Over USD 5 billion in structured financing and asset-backed securities issued recently to support fleet expansion and container refurbishment programs.

Innovation & Future Outlook: Growth in modular container design, sustainable reefer technologies, and integrated digital leasing platforms will redefine operational efficiency and asset lifecycle management.

Container leasing services are widely utilized across key industry sectors, including retail and consumer goods contributing approximately 35% of demand, manufacturing and industrial equipment at nearly 25%, automotive logistics around 15%, and temperature-controlled pharmaceuticals and food supply chains representing close to 12%. Technological advancements such as GPS-integrated telematics, remote reefer monitoring, and corrosion-resistant lightweight steel alloys are enhancing durability and asset visibility. Environmental regulations promoting low-emission transport and circular economy practices are stimulating demand for refurbished and energy-efficient containers. Asia-Pacific leads consumption due to export-intensive economies, while North America emphasizes intermodal integration and Europe advances sustainable logistics compliance. Emerging trends include flexible short-term leasing contracts, data-driven fleet optimization, and hybrid financing structures that improve capital efficiency for global shipping lines and freight operators.

The Container Leasing Market holds strategic relevance as global supply chains increasingly prioritize asset flexibility, capital efficiency, and risk mitigation. Shipping lines and freight forwarders are shifting toward long-term leasing contracts to avoid high upfront container procurement costs that can exceed USD 3,000 per standard dry container and over USD 12,000 per advanced refrigerated unit. This strategic transition enables balance sheet optimization while maintaining scalable fleet capacity aligned with fluctuating trade volumes.

Digitally enabled smart containers integrated with IoT sensors deliver 25% improvement in real-time cargo visibility compared to manual tracking and paper-based documentation systems. Asia-Pacific dominates in shipment volume due to export-driven manufacturing economies, while Europe leads in adoption with over 45% of logistics enterprises integrating digital container monitoring platforms into fleet management operations.

By 2028, AI-driven predictive maintenance systems are expected to cut container downtime by 18% and improve utilization rates by 15%, strengthening operational continuity in high-density trade corridors. Firms are committing to ESG performance metrics such as a 30% reduction in lifecycle carbon emissions by 2030 through lightweight steel designs, container refurbishment programs, and eco-efficient reefer technologies. In 2024, a U.S.-based leasing operator achieved a 16% reduction in idle container repositioning through AI-enabled route optimization and demand forecasting tools, demonstrating measurable operational gains. Looking ahead, the Container Leasing Market is positioned as a foundational pillar of supply chain resilience, regulatory compliance, and sustainable global trade expansion.

Global containerized trade volumes have demonstrated consistent expansion, with container throughput surpassing 180 million TEUs annually across major ports. E-commerce-driven cross-border shipments have increased container movement intensity by nearly 28% over the past five years. Retail, automotive, and consumer electronics sectors rely heavily on containerized shipping to maintain just-in-time inventory systems. Leasing allows carriers to scale fleets rapidly without committing to long-term capital expenditure, especially during seasonal peaks where utilization rates can exceed 90%. Refrigerated container demand has also grown by approximately 20% due to rising pharmaceutical and perishable food exports. As supply chains become more time-sensitive and diversified, leasing offers operational flexibility and improved asset turnover, directly strengthening the Container Leasing Market’s expansion trajectory.

Periodic oversupply of containers presents structural challenges for leasing providers. During periods of trade slowdown, global idle container capacity can exceed 15% of the active fleet, leading to downward pressure on lease rates. Freight volatility and declining spot shipping rates influence customer renegotiations and shorter lease tenures. Additionally, container production surges during high-demand cycles—such as when annual manufacturing output surpasses 5 million TEUs—can create excess inventory in subsequent years. Storage, repositioning, and maintenance costs increase when utilization declines, affecting profitability and cash flow stability. These cyclical imbalances introduce pricing uncertainty and intensify competition among lessors, constraining steady operational performance in the Container Leasing Market.

Digital fleet optimization represents a high-value growth opportunity within the Container Leasing Market. Integration of IoT tracking, blockchain documentation, and AI-based demand forecasting can improve container turnaround time by 15% and reduce repositioning expenses by up to 20%. Advanced analytics platforms enable precise allocation of containers to high-demand trade lanes, enhancing utilization efficiency. Growing adoption of temperature-controlled smart reefers supports pharmaceutical and fresh food supply chains, which require real-time condition monitoring. Emerging trade corridors in Southeast Asia, Africa, and Latin America are also expanding infrastructure investments, creating new demand pools. Flexible leasing models, including short-term and on-demand digital contracts, are further unlocking value for small and mid-sized logistics providers.

Increasing regulatory scrutiny on maritime emissions and cargo safety standards is raising compliance costs for leasing operators. International maritime environmental frameworks require energy-efficient refrigeration units and corrosion-resistant materials, increasing production costs by 10–15% for advanced container models. Maintenance, inspection, and refurbishment programs must align with stricter safety protocols, particularly for tank and reefer containers. Port congestion and geopolitical disruptions also elevate repositioning and storage expenditures. Insurance premiums for high-value cargo containers have risen in volatile trade routes, adding further financial strain. These cost pressures demand strategic capital allocation and operational efficiency improvements to sustain competitiveness within the Container Leasing Market.

• Smart Container Integration Surpasses 40% of New Fleet Additions:

Digital transformation is rapidly reshaping the Container Leasing Market, with over 40% of newly manufactured containers now equipped with IoT-enabled tracking devices. Smart containers improve real-time cargo visibility by 25% and reduce theft or cargo loss incidents by nearly 18%. Advanced sensor-based monitoring in refrigerated units enhances temperature accuracy within ±0.5°C, minimizing spoilage risk for pharmaceuticals and perishable goods. Leasing operators deploying predictive analytics platforms have reported up to 15% faster container turnaround times, strengthening operational efficiency across high-volume Asia–Europe and trans-Pacific routes.

• Refrigerated Container Leasing Expands by 20% Amid Cold Chain Growth:

Demand for refrigerated container leasing has increased by approximately 20% due to rising pharmaceutical exports and global food trade expansion. Over 30% of temperature-sensitive pharmaceutical shipments now rely on leased reefer containers equipped with remote monitoring systems. Energy-efficient reefer units consume nearly 12% less power compared to older compressor-based models, supporting sustainability objectives. Leasing firms are expanding specialized reefer fleets by more than 10% annually to accommodate vaccine distribution, biologics transport, and high-value food exports across North America and Asia-Pacific corridors.

• Asset-Light Shipping Models Reduce Capital Burden by 35%:

Shipping companies are increasingly adopting leasing strategies to reduce upfront capital expenditure by nearly 35% compared to direct container ownership. More than 55% of global container fleets are now managed through leasing agreements, reflecting the growing preference for flexible capacity management. Short-term and master lease contracts have improved fleet utilization rates by 12–18%, particularly during seasonal trade peaks. This shift enables carriers to respond quickly to fluctuating demand without overextending balance sheets, reinforcing liquidity and financial resilience.

• Sustainability-Driven Refurbishment Programs Cut Lifecycle Emissions by 28%:

Environmental compliance and ESG commitments are influencing procurement decisions across the Container Leasing Market. Refurbishment and recycling initiatives now extend container lifecycle by 5–7 years, reducing steel consumption by approximately 22%. Lightweight high-tensile steel designs decrease overall container weight by 8%, improving fuel efficiency during transport. Leasing operators investing in green container technologies have achieved up to 28% reduction in lifecycle carbon emissions. Increasing regulatory mandates for emission reporting are further accelerating adoption of eco-efficient containers across Europe and North America.

The Container Leasing Market is segmented by type, application, and end-user, reflecting the diversified requirements of global trade and logistics ecosystems. By type, dry containers dominate due to their universal applicability in transporting manufactured goods, electronics, textiles, and industrial components. Refrigerated containers are expanding rapidly in response to pharmaceutical and perishable food logistics, while tank and specialized containers cater to chemicals, liquids, and hazardous materials.

From an application perspective, international maritime transport accounts for the largest deployment, supported by containerized trade exceeding 180 million TEUs annually. Intermodal rail and road integration is strengthening inland container movement, particularly in North America and Europe. End-user insights indicate that global shipping lines represent the largest demand base, followed by freight forwarders, third-party logistics providers, and specialized cold chain operators. Increasing preference for long-term leasing contracts and digital fleet optimization tools is reshaping procurement strategies across these segments.

Dry containers currently account for approximately 62% of total leased units, making them the leading segment due to their standardized 20-foot and 40-foot configurations widely used across retail, manufacturing, and industrial trade lanes. Their versatility and high turnover rates contribute to consistent utilization levels above 85% during peak shipping cycles. Refrigerated containers hold nearly 23% of adoption, driven by pharmaceutical exports and temperature-sensitive food shipments. However, refrigerated container leasing is the fastest-growing segment, expanding at an estimated CAGR of 6.1%, supported by a 20% rise in global cold chain trade and increasing biologics transportation requirements. Tank containers and specialized containers, including open-top and flat-rack units, collectively represent around 15% of the fleet, serving chemical, energy, and heavy machinery sectors where customized cargo handling is essential. These niche categories demonstrate stable demand linked to industrial production volumes.

International maritime transport remains the dominant application, accounting for nearly 68% of total container leasing utilization, supported by expanding Asia–Europe and trans-Pacific trade corridors. Intermodal transportation, including rail and truck integration, represents approximately 22% of adoption, particularly in North America where over 30% of containerized imports are moved inland by rail networks. However, inland logistics integration is rising fastest, expanding at an estimated CAGR of 5.4%, driven by infrastructure modernization and automated terminal operations. Offshore energy and specialized industrial applications contribute the remaining 10%, including the use of tank containers for chemical transport and modular container solutions for remote operations. These segments provide strategic diversification for leasing providers.

Global shipping lines constitute the largest end-user segment, accounting for approximately 55% of leased container demand due to their extensive international route networks and asset-light fleet strategies. Freight forwarders and third-party logistics providers collectively hold around 27% adoption, leveraging leasing models to enhance working capital efficiency and reduce ownership risks. However, cold chain logistics operators represent the fastest-growing end-user segment, expanding at an estimated CAGR of 6.3%, driven by a 25% increase in temperature-sensitive pharmaceutical and food exports over recent years. Industrial manufacturers and chemical companies contribute the remaining 18%, particularly for tank and specialized container leasing in hazardous material transportation. Adoption rates among multinational retailers exceed 40% for long-term leasing agreements to support seasonal demand spikes and inventory optimization.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by container throughput exceeding 110 million TEUs annually across major ports in China, Singapore, and South Korea. China alone handles over 30% of global container traffic, while India’s containerized exports increased by 12% year-on-year, strengthening leasing demand. North America represents approximately 26% of total leased container deployment, with major ports processing more than 55 million TEUs annually. Europe accounts for nearly 22%, supported by integrated rail freight systems moving over 4 million TEUs inland each year. South America holds around 6% share, driven by agricultural exports from Brazil and Argentina, while the Middle East & Africa contribute roughly 5%, supported by transshipment hubs in the UAE and growing trade corridors across South Africa. Infrastructure modernization projects exceeding USD 50 billion globally are further enhancing port automation, digital container tracking, and intermodal connectivity, reinforcing regional competitiveness within the Container Leasing Market.

How Is Advanced Intermodal Infrastructure Strengthening Market Expansion?

This region accounts for approximately 26% of global leased container utilization, supported by extensive rail-road integration and port automation systems. Over 35% of imported containers are transported inland via double-stack rail networks, improving transit efficiency by 18%. Key demand originates from retail, automotive, agriculture, and pharmaceutical sectors, which collectively represent over 60% of containerized imports. Regulatory frameworks such as stricter emissions standards and port decarbonization programs are accelerating adoption of energy-efficient refrigerated containers. Digital transformation is advancing rapidly, with more than 48% of logistics enterprises deploying IoT-enabled tracking for leased fleets. A leading regional player, Triton International, manages millions of TEUs and continues expanding smart container programs to improve utilization rates by over 12%. Consumer behavior in this region reflects higher enterprise adoption across healthcare and retail sectors, where just-in-time inventory strategies drive consistent leasing demand.

Why Is Sustainability Compliance Reshaping Competitive Dynamics?

Europe contributes nearly 22% of global container leasing deployment, with Germany, the UK, and France leading containerized trade volumes exceeding 25 million TEUs collectively. Sustainability mandates under regional environmental frameworks are influencing procurement strategies, pushing adoption of lightweight steel containers that reduce emissions by 8% per voyage. Over 45% of logistics operators have integrated digital cargo documentation systems to meet regulatory transparency requirements. Intermodal rail accounts for more than 30% of inland container movement, supporting efficient cross-border trade. A prominent regional operator, Seaco Global, is expanding eco-friendly reefer fleets to meet rising cold chain demand. Consumer behavior variations indicate strong preference for ESG-compliant leasing contracts, as regulatory pressure drives enterprises toward explainable and sustainable fleet management solutions.

What Drives High-Volume Manufacturing and Export-Linked Leasing Demand?

Holding 41% of global container leasing share, this region processes over 110 million TEUs annually, with China, India, and Japan serving as the top consuming markets. China’s ports alone handle more than 290 million TEUs in total throughput, reinforcing large-scale container circulation. Rapid manufacturing output, electronics exports, and e-commerce shipments growing by 20% annually are strengthening dry container leasing demand. Infrastructure investments exceeding USD 30 billion in port expansion and smart logistics hubs are modernizing operations. Local players such as COSCO Shipping Leasing are scaling fleet capacities and implementing AI-driven route optimization systems to reduce repositioning costs by 15%. Consumer behavior in this region reflects strong growth driven by export manufacturing and cross-border e-commerce platforms.

How Are Agricultural Exports Influencing Fleet Utilization Patterns?

This region represents approximately 6% of the global Container Leasing Market, with Brazil and Argentina accounting for over 70% of regional containerized exports. Agricultural commodities such as soybeans, meat, and coffee drive demand for both dry and refrigerated containers, particularly during peak harvest seasons where utilization rates exceed 85%. Infrastructure modernization projects in Brazil’s major ports have improved handling capacity by 10%. Government trade agreements and export incentives are supporting logistics sector expansion. Regional operators are investing in reefer container refurbishment to extend lifecycle by 5 years. Consumer behavior indicates demand closely tied to commodity cycles and language-specific trade documentation processes, influencing short-term leasing contracts.

How Are Energy and Transshipment Hubs Expanding Strategic Opportunities?

Contributing roughly 5% to the global Container Leasing Market, this region is supported by oil, gas, and construction-related cargo movements. The UAE and South Africa are major growth countries, with transshipment hubs handling over 25 million TEUs annually. Port modernization programs have improved container turnaround times by 14%, enhancing leasing attractiveness. Trade partnerships across Gulf and African nations are facilitating corridor expansion, while free trade zones encourage container fleet deployment. Regional operators are integrating digital tracking to enhance cross-border cargo transparency. Consumer behavior reflects project-based demand, particularly in energy infrastructure and construction supply chains requiring flexible short-term leasing models.

China – 32% market share: Strong manufacturing output, over 290 million TEUs port throughput, and large-scale export-driven container circulation reinforce China’s leadership in the Container Leasing Market.

United States – 24% market share: Advanced intermodal networks, high pharmaceutical and retail import volumes, and widespread smart container adoption sustain the United States’ dominant position in the Container Leasing Market.

The Container Leasing Market is moderately consolidated, characterized by the presence of approximately 25–30 active global and regional leasing companies managing fleets exceeding 50 million TEUs collectively. The top five companies account for nearly 72% of total leased container capacity, reflecting strong scale advantages, access to structured financing, and long-term contracts with major shipping lines. Large lessors typically manage fleets surpassing 4 million TEUs individually, enabling optimized procurement and lower per-unit maintenance costs by 10–15% compared to smaller operators.

Strategic initiatives are shaping competitive dynamics, including multi-year supply agreements with container manufacturers, digital fleet optimization partnerships, and asset-backed securities exceeding USD 5 billion issued in recent financing cycles. Leading players are investing in smart container technologies, with over 40% of new fleet additions incorporating IoT-enabled tracking systems. Mergers and portfolio acquisitions have also intensified, enhancing fleet diversification across dry, reefer, and tank containers. Competitive positioning increasingly depends on global depot networks spanning more than 400 locations worldwide, ensuring efficient repositioning and refurbishment. Innovation in eco-efficient refrigerated units and modular container designs is further differentiating market leaders, as ESG compliance and lifecycle management become critical procurement criteria among shipping lines and logistics enterprises.

Triton International

Textainer Group Holdings Limited

CAI International

Seaco Global

Florens Container Leasing

Beacon Intermodal Leasing

SeaCube Container Leasing

Touax Group

Blue Sky Intermodal

CARU Containers

Technology transformation is redefining operational efficiency, asset utilization, and risk management across the Container Leasing Market. Over 40% of newly manufactured containers are now equipped with IoT-enabled telematics devices that provide real-time location tracking, door status alerts, shock detection, and temperature monitoring. These smart container systems improve cargo visibility by up to 25% and reduce theft or loss incidents by nearly 18%. For refrigerated units, sensor-based temperature monitoring maintains accuracy within ±0.5°C, significantly lowering spoilage risks for pharmaceuticals and perishable goods.

Artificial intelligence and predictive analytics platforms are increasingly integrated into fleet management systems. AI-driven demand forecasting models have demonstrated up to 15% improvement in container allocation efficiency and reduced empty repositioning costs by approximately 20%. Machine learning algorithms analyze historical trade flows, port congestion levels, and seasonal demand to optimize lease pricing and deployment strategies. Automated maintenance scheduling powered by predictive diagnostics can reduce unplanned downtime by 12%, extending container lifecycle by 3–5 years.

Blockchain-based digital documentation is gaining adoption, particularly in Europe and North America, where more than 30% of logistics operators are piloting electronic bills of lading to reduce paperwork processing time by 50%. Lightweight high-tensile steel technology has reduced container weight by 8%, improving fuel efficiency during transport. Additionally, energy-efficient reefer units now consume nearly 12% less power than previous-generation models. Collectively, these technological advancements are strengthening supply chain transparency, sustainability compliance, and long-term asset performance within the Container Leasing Market.

• In February 2024, Triton International announced a long-term lease agreement with a major global shipping line covering over 100,000 TEUs of new dry and refrigerated containers, strengthening its contracted utilization above 95% and expanding deployment across Asia–Europe trade lanes. Source: www.tritoninternational.com

• In May 2024, Textainer Group Holdings Limited completed the acquisition of approximately 80,000 TEUs of containers from a regional lessor portfolio, enhancing fleet diversification across dry, tank, and reefer segments and expanding its global depot network beyond 400 locations. Source: www.textainer.com

• In September 2024, Seaco Global introduced an upgraded energy-efficient refrigerated container line featuring improved insulation technology that reduces power consumption by up to 10%, supporting cold chain logistics and ESG-focused fleet modernization initiatives. Source: www.seacoglobal.com

• In March 2025, Florens Container Leasing expanded its smart container program by deploying IoT-enabled tracking devices across more than 50,000 units, enabling real-time monitoring and improving container repositioning efficiency by 15% across trans-Pacific and intra-Asia routes. Source: www.florens.com

The Container Leasing Market Report provides a comprehensive assessment of global container fleet dynamics, covering more than 50 million TEUs under active leasing arrangements worldwide. The report analyzes segmentation by container type, including dry containers representing over 60% of leased fleets, refrigerated units accounting for nearly 20–25%, and specialized tank and flat-rack containers comprising the remaining share.

Geographic coverage spans Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with detailed evaluation of high-volume trade corridors processing over 180 million TEUs annually. The report assesses regional port infrastructure capacity, intermodal integration rates exceeding 30% in developed markets, and transshipment hub performance handling more than 25 million TEUs per major port cluster.

Application coverage includes international maritime shipping, inland intermodal transport, offshore energy logistics, and temperature-controlled pharmaceutical distribution. Technological analysis addresses IoT-enabled smart containers adopted in over 40% of new fleets, blockchain-based documentation systems reducing paperwork processing time by up to 50%, and predictive analytics platforms lowering repositioning costs by nearly 20%.

The report further evaluates regulatory and ESG frameworks influencing container lifecycle management, including refurbishment programs extending service life by 5–7 years and lightweight steel innovations reducing container weight by 8%. Emerging segments such as short-term digital leasing platforms and green reefer technologies are also examined, offering strategic insights for investors, shipping lines, logistics providers, and financial institutions seeking data-driven decision support within the Container Leasing Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Triton International, Textainer Group Holdings Limited, CAI International, Seaco Global, Florens Container Leasing, Beacon Intermodal Leasing, SeaCube Container Leasing, Touax Group, Blue Sky Intermodal, CARU Containers |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |