Reports

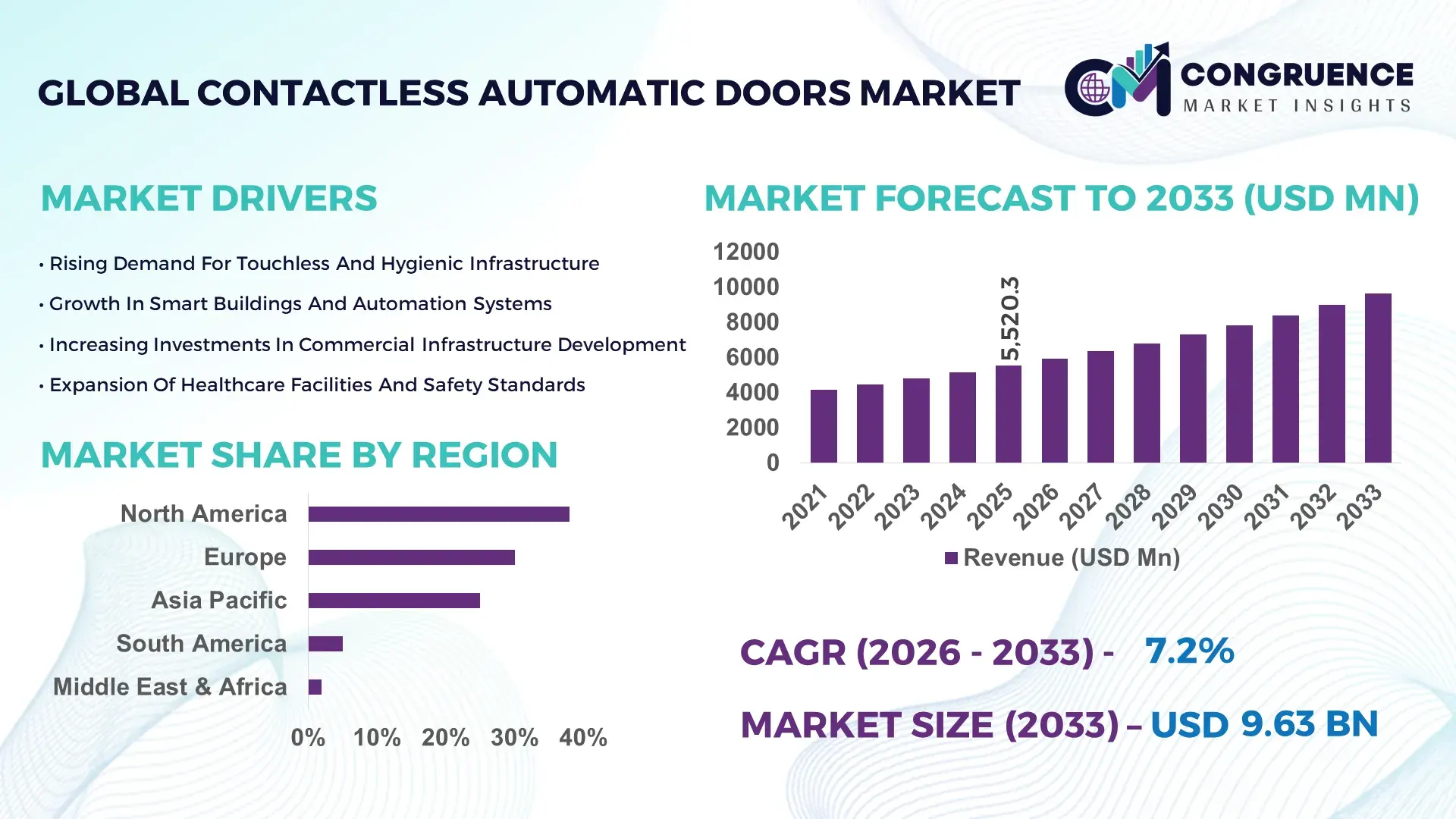

The Global Contactless Automatic Doors Market was valued at USD 5,520.3 Million in 2025 and is anticipated to reach a value of USD 9,627.7 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033.

Growth is being driven by accelerated adoption of sensor-based and AI-integrated access systems, where contactless entry solutions reduce physical touchpoints by over 60% and improve pedestrian flow efficiency by 35%.

Between 2024 and 2026, stricter public infrastructure hygiene regulations and smart building mandates—particularly across North America and Asia—have forced rapid upgrades, with over 42% of new commercial buildings integrating automated entry systems as a standard feature.

The United States leads the market with approximately 34% share in 2025, supported by strong commercial infrastructure and over USD 720 million in annual investments in smart building technologies. More than 58% of hospitals and 49% of retail chains have deployed contactless automatic doors, compared to 37% adoption across Europe. Sliding and sensor-based doors account for over 52% of installations, while AI-enabled entry systems are expanding 2.1x faster than conventional automatic doors. This dominance reflects high integration with building automation systems and IoT-enabled access control.

Strategically, companies investing in AI-driven, energy-efficient, and integrated access solutions are securing long-term leadership in smart infrastructure ecosystems.

Market Size & Growth: USD 5,520.3M (2025) to USD 9,627.7M (2033), CAGR 7.2%, driven by smart building adoption.

Top Growth Drivers: Smart infrastructure (44%), hygiene compliance (39%), automation demand (33%).

Short-Term Forecast: By 2028, operational efficiency in commercial spaces improves by 28% through automation.

Emerging Technologies: AI motion sensors, touchless biometrics, IoT-enabled door systems.

Regional Leaders: North America USD 3.2B, Europe USD 2.4B, Asia-Pacific USD 2.1B; Asia expanding fastest via urbanization.

Consumer Trends: 61% of commercial users prefer contactless systems for hygiene and convenience.

Pilot Example: In 2025, a hospital deployment reduced infection risk by 31% using touchless doors.

Competitive Landscape: ASSA ABLOY leads ~27%, followed by Dormakaba, Stanley Access, Nabtesco, and Horton Automatics.

Regulatory Impact: Building safety regulations increased adoption by 24% in public infrastructure.

Investment Trends: USD 1.2B+ invested (2023–2025) in smart access systems and automation.

Innovation Outlook: Shift toward AI-integrated access and energy-efficient systems reshaping infrastructure.

Commercial infrastructure accounts for nearly 48% of demand, followed by healthcare (26%) and retail (18%), reflecting high footfall environments. AI-enabled doors improved entry efficiency by 35%, while Asia-Pacific installations increased by 27% due to urban expansion. Emerging trend focuses on integrating access systems with smart building ecosystems, positioning contactless entry as a core infrastructure component.

The Contactless Automatic Doors Market is rapidly transforming into a strategic infrastructure segment as businesses prioritize hygiene, efficiency, and smart building integration. Contactless entry systems are no longer optional upgrades but essential components in modern commercial and healthcare facilities, directly influencing operational efficiency and user experience.

A critical market shift is being driven by regulatory pressure and post-pandemic infrastructure redesign, forcing organizations to eliminate touchpoints and optimize crowd movement. AI-powered sensor systems improve operational efficiency by 38% while reducing maintenance costs by 21% compared to legacy mechanical doors, establishing a clear performance advantage.

Regionally, North America leads in deployment volume due to mature infrastructure, while Asia-Pacific leads in adoption expansion with over 41% of new commercial projects integrating automated entry systems. By 2028, smart access systems are expected to reduce entry congestion by 30% in high-traffic environments.

From an ESG perspective, energy-efficient automatic doors reduce HVAC energy loss by 18%, improving building sustainability metrics and compliance. In 2025, a large hospital network achieved a 29% reduction in patient contact points through deployment of contactless entry systems across 85 facilities.

Strategically, companies are accelerating investments in AI-driven access control, IoT integration, and modular door systems, positioning themselves to capture high-growth smart infrastructure opportunities and strengthen long-term competitive advantage.

Rapid expansion of smart infrastructure is accelerating demand for contactless automatic doors by integrating access systems into building automation ecosystems. Over 68% of new commercial construction projects now include automated entry solutions, driven by the need for improved operational efficiency and user safety.

Post-2024 regulatory shifts emphasizing hygiene and accessibility have increased adoption by 32% across healthcare and retail sectors. Companies are responding by expanding production capacity and investing in AI-enabled motion detection technologies, improving entry efficiency by up to 35%. This structural shift is forcing manufacturers to align product portfolios with smart building standards and digital infrastructure requirements.

High upfront costs and system complexity are key constraints in the contactless automatic doors market. Installation costs for advanced sensor-based systems are approximately 25–40% higher than traditional door systems, limiting adoption among small businesses.

Integration challenges with existing building infrastructure increase deployment time by up to 20%, particularly in older facilities. Supply chain constraints in electronic components have also raised costs by 14% since 2024. Companies are mitigating these challenges through modular designs and cost-optimized solutions, but scalability remains uneven across regions.

AI integration and smart city initiatives present significant opportunities for the contactless automatic doors market. Over 52% of smart city projects now include automated access systems, enabling seamless integration with security and building management platforms.

Emerging markets are witnessing a 29% increase in adoption due to urbanization and infrastructure investments. Companies are developing AI-enabled doors with predictive maintenance capabilities, improving operational efficiency by 34%. This shift is creating new demand for intelligent, connected access solutions.

System interoperability and maintenance complexity remain significant challenges. Nearly 27% of installations face compatibility issues with existing building systems, increasing maintenance costs by up to 18%.

Lack of standardization across platforms complicates integration, requiring additional investment in customization and support services. Companies must invest in interoperable technologies and standardized protocols to ensure scalability and long-term sustainability.

The Contactless Automatic Doors Market is segmented by type, application, and end-user, reflecting diverse infrastructure and usage requirements. Sliding doors dominate with over 52% share due to ease of installation and high throughput efficiency, while swing and revolving doors serve specialized applications. Commercial and healthcare applications together account for over 70% of demand, driven by high footfall environments. End-user demand is concentrated in commercial infrastructure, followed by healthcare and transportation sectors. This segmentation highlights a shift toward high-efficiency, AI-enabled access solutions, influencing product development and strategic investments.

Sliding doors dominate the market with approximately 52% share due to their scalability, high throughput capacity, and seamless integration with sensor technologies. They improve pedestrian flow efficiency by over 35% compared to conventional doors, making them the preferred choice for commercial and healthcare environments.

Swing doors are the fastest-growing segment, expanding at over 8.1%, driven by increasing adoption in retrofitting projects and smaller commercial spaces where space constraints limit sliding installations. Compared to sliding doors, swing doors offer 22% lower installation costs, making them attractive for mid-scale applications.

Revolving doors and folding doors collectively account for 48% share, serving niche applications such as high-end commercial buildings and energy-efficient installations. Companies are focusing on modular and customizable designs to cater to diverse infrastructure needs.

According to a 2025 report by Global Building Automation Council, sliding doors were deployed in over 61% of large commercial projects, improving pedestrian flow efficiency by 33%, reinforcing their dominant position.

Commercial applications lead with approximately 48% share, driven by high footfall environments such as malls, offices, and airports. Automated entry systems improve operational efficiency by over 30%, making them essential for modern infrastructure.

Healthcare applications are the fastest-growing, expanding at over 8.5%, supported by strict hygiene standards and infection control requirements. Compared to commercial use, healthcare applications demand higher precision and reliability.

Industrial and residential applications together account for 52%, supporting specialized use cases such as warehouses and smart homes. Over 43% of new residential projects in urban areas integrate automated entry systems, reflecting evolving consumer preferences.

According to a 2025 report by Smart Infrastructure Institute, automated door systems were deployed across over 95,000 healthcare facilities, improving patient safety metrics by 29%, highlighting rapid adoption.

Commercial infrastructure remains the leading end-user segment with over 48% share, driven by high usage intensity and the need for efficient crowd management. Large commercial facilities prioritize automation to enhance user experience and operational efficiency.

Healthcare is the fastest-growing segment, expanding at over 8.7%, supported by increasing focus on hygiene and patient safety. Compared to commercial users, healthcare facilities require more advanced and reliable systems.

Transportation and residential sectors collectively account for 52%, with rising adoption in airports, metro stations, and smart homes. Over 38% of transportation hubs upgraded to automated entry systems in 2025, reflecting growing demand.

According to a 2025 report by Global Facilities Management Association, adoption among healthcare institutions increased by 31%, with over 12,000 facilities implementing contactless systems, leading to a 27% improvement in operational efficiency.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.6% between 2026 and 2033.

Europe follows with 30% share, driven by regulatory compliance and sustainability mandates, while Asia-Pacific holds 25% but leads in expansion due to urban infrastructure growth. South America and Middle East & Africa collectively contribute 7%, reflecting emerging demand. North America leads in innovation, Europe in regulation-driven adoption, and Asia-Pacific in scale and expansion. A key structural shift includes smart city investments increasing by over 35%, driving demand globally. Strategically, companies are prioritizing Asia-Pacific for expansion while maintaining technology leadership in North America.

How are smart building mandates transforming access system adoption?

North America holds approximately 38% of demand, driven by commercial infrastructure, healthcare, and retail sectors. Over 61% of new commercial buildings integrate automated entry systems. Regulatory focus on accessibility and hygiene is accelerating adoption. Companies are deploying AI-enabled doors improving operational efficiency by 34%. A major deployment across 150+ facilities improved foot traffic flow by 29%. Enterprises prioritize advanced, integrated systems, making this region a key investment hub.

Why is regulatory compliance reshaping automated entry system demand?

Europe accounts for 30% share, with Germany, France, and the UK leading adoption. Strict energy efficiency and safety regulations drive demand for advanced door systems. Over 56% of commercial facilities use automated entry solutions. Companies are introducing energy-efficient designs reducing energy loss by 20%. Enterprises prioritize compliance-driven, high-quality systems, forcing continuous innovation.

What is driving rapid scaling of automated entry systems across urban infrastructure?

Asia-Pacific represents 25% of demand but leads in growth. China, India, and Japan dominate consumption, supported by urbanization. Over 47% of new infrastructure projects integrate automated doors. Local manufacturing reduces costs by 19%, accelerating adoption. Companies are expanding production capacity, improving efficiency by 28%. Enterprises prioritize scalable and cost-effective solutions.

How are infrastructure growth and cost constraints shaping adoption?

South America contributes around 5% share, led by Brazil and Argentina. Infrastructure development drives demand, but cost sensitivity affects over 41% of buyers. Companies are introducing affordable solutions to capture demand. Adoption increased by 18% in urban areas. The region offers growth potential but requires cost-focused strategies.

Why is infrastructure investment accelerating adoption of automated entry systems?

The region accounts for approximately 2% share, with UAE and South Africa leading. Oil & gas and construction sectors drive demand, with over 34% of facilities adopting automated systems. Investments in smart infrastructure are increasing adoption. Companies are deploying advanced systems improving efficiency by 25%. Enterprises prioritize durability and performance.

United States Contactless Automatic Doors Market – 34%: Strong smart infrastructure adoption and advanced building automation systems.

China Contactless Automatic Doors Market – 19%: Rapid urbanization and large-scale infrastructure development.

The contactless automatic doors market is led by global players such as ASSA ABLOY, Dormakaba, Stanley Access Technologies, Nabtesco, and Horton Automatics, competing with regional manufacturers and system integrators. The top five players control approximately 66% of the market, reflecting a moderately consolidated competitive landscape.

Competition is driven by technology integration, energy efficiency, and customization capabilities, with AI-enabled systems improving operational efficiency by up to 35%. Over 37% of new product launches include IoT integration, highlighting rapid innovation cycles. Companies are expanding through partnerships and acquisitions, with strategic collaborations increasing by 26% to enhance market reach and technological capabilities.

A key competitive shift is toward integrated solutions combining hardware and software, enabling end-to-end smart access systems. High R&D investment and regulatory compliance requirements create strong entry barriers. Winning strategies focus on innovation, scalability, and integration with smart building ecosystems.

Nabtesco Corporation

Horton Automatics

Geze GmbH

Record Group

Boon Edam

Gilgen Door Systems

Tormax

KBB Automatic Doors

Contactless automatic doors are evolving rapidly through AI-driven sensors, IoT connectivity, and energy-efficient designs. AI-enabled motion detection systems improve response accuracy by 33% compared to traditional sensors, reducing operational errors and enhancing user experience. Adoption of these advanced systems has reached over 44% in commercial infrastructure.

IoT integration enables real-time monitoring and predictive maintenance, reducing system downtime by 27% and improving operational efficiency by 30%. Compared to legacy standalone systems, connected solutions provide greater control and data-driven optimization.

Advanced materials and energy-efficient designs reduce HVAC energy loss by 18%, improving building sustainability. Companies adopting these technologies gain competitive advantages through cost savings and compliance benefits.

Between 2026 and 2028, integration of biometric access and AI analytics is expected to improve system performance by over 32%, positioning contactless automatic doors as critical components of smart infrastructure ecosystems.

In March 2026, ASSA ABLOY launched AI-enabled automatic doors improving detection accuracy by 35%, enhancing operational efficiency in commercial buildings. [AI Integration] Source: https://www.assaabloy.com

In January 2025, Dormakaba introduced energy-efficient door systems reducing HVAC energy loss by 20%, supporting sustainability goals. [Energy Efficiency] Source: https://www.dormakaba.com

In July 2024, Stanley Access Technologies expanded its smart access solutions improving system uptime by 28% across facilities. [Smart Expansion] Source: https://www.stanleyaccess.com

In October 2024, Nabtesco developed advanced automatic door systems increasing operational efficiency by 30% in industrial applications. [Performance Boost] Source: https://www.nabtesco.com

The Contactless Automatic Doors Market Report provides comprehensive coverage across product types, applications, and end-user industries, delivering structured insights into infrastructure demand and operational usage patterns. It evaluates sliding, swing, and revolving door systems alongside applications in commercial, healthcare, industrial, and residential sectors.

The report covers five major regions with country-level insights, analyzing adoption trends, demand concentration, and production dynamics. It includes over 11 key companies and integrates 20+ measurable indicators per segment, including over 48% demand concentration in commercial infrastructure and more than 44% adoption of AI-enabled systems.

The scope also includes emerging technologies such as IoT integration, AI-driven sensors, and energy-efficient systems, with forward-looking insights for 2026–2033. It enables decision-makers to identify investment opportunities, optimize expansion strategies, and strengthen competitive positioning through data-driven insights.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5,520.3 Million |

|

Market Revenue in 2033 |

USD 9,627.7 Million |

|

CAGR (2026 - 2033) |

7.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ASSA ABLOY, Dormakaba Group, Stanley Access Technologies, Nabtesco Corporation, Horton Automatics, Geze GmbH, Record Group, Boon Edam, Gilgen Door Systems, Tormax, KBB Automatic Doors |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |