Reports

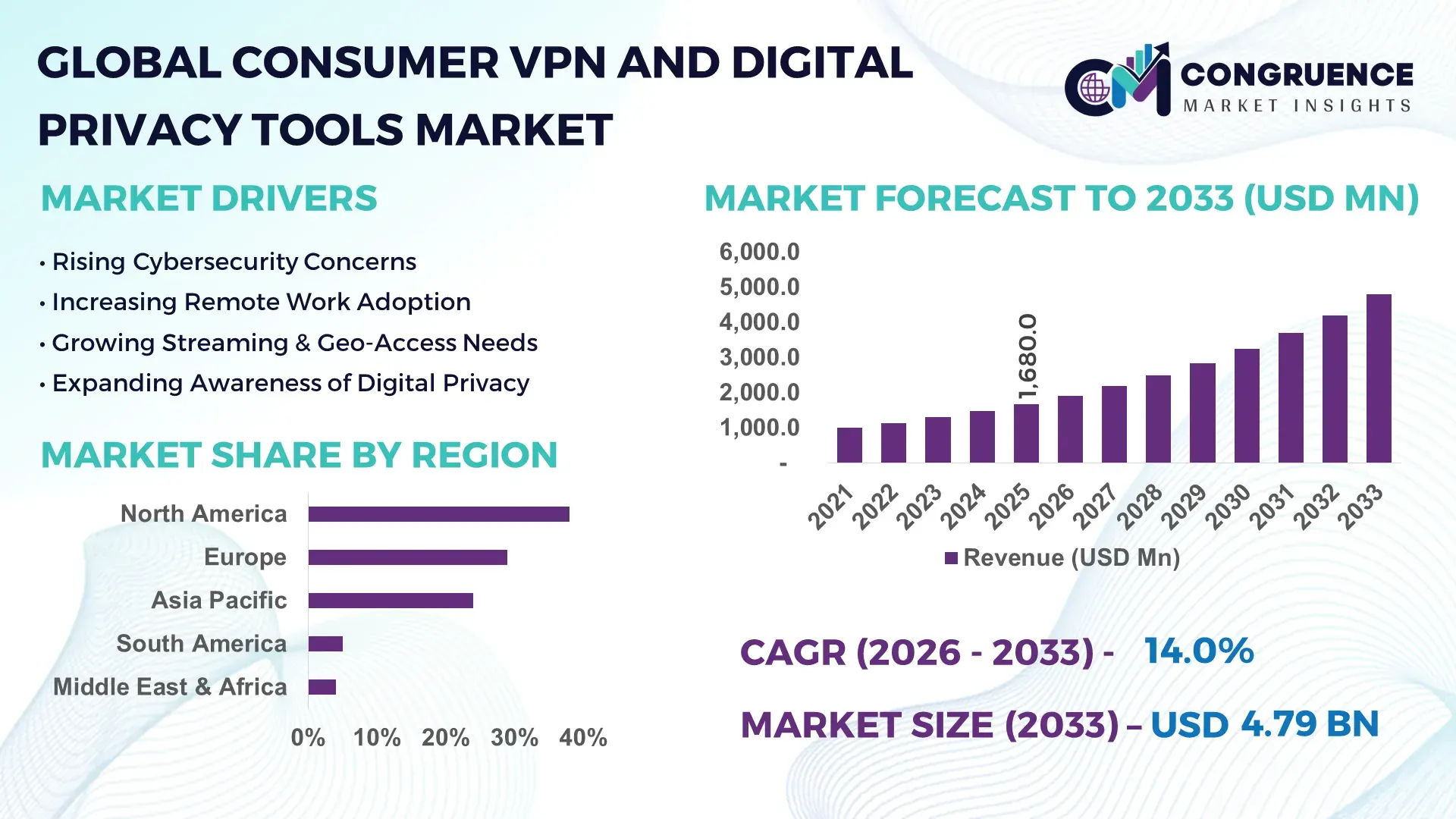

The Global Consumer VPN and Digital Privacy Tools Market was valued at USD 1,680.0 Million in 2025 and is anticipated to reach a value of USD 4,792.3 Million by 2033 expanding at a CAGR of 14% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding steadily due to rising cybersecurity threats, growing digital surveillance concerns, and increasing consumer awareness regarding online data protection across personal and professional digital environments.

The United States represents the dominant country in the Consumer VPN and Digital Privacy Tools Market, supported by a strong cybersecurity infrastructure and high digital service penetration. Over 92% of U.S. households have internet access, and approximately 46% of adult internet users report using a VPN at least once for streaming, data security, or remote access. The country hosts more than 35% of the world’s leading consumer cybersecurity and VPN solution providers, with annual private cybersecurity investments exceeding USD 20 billion. Advanced encryption standards such as AES-256 are widely adopted, and AI-driven threat detection systems are integrated into over 60% of premium privacy tools. Increasing enterprise-to-consumer spillover of Zero Trust frameworks is accelerating adoption among individuals, freelancers, and remote workers.

Market Size & Growth: USD 1,680.0 Million (2025) projected to reach USD 4,792.3 Million by 2033 at 14% CAGR, driven by escalating cyber threats and increased remote digital activity.

Top Growth Drivers: 68% rise in remote/hybrid workforce adoption, 57% increase in public Wi-Fi usage risks, 49% growth in identity theft incidents.

Short-Term Forecast: By 2028, AI-based privacy tools are expected to improve threat detection accuracy by 35% and reduce breach response time by 30%.

Emerging Technologies: AI-driven behavioral analytics, quantum-resistant encryption protocols, decentralized VPN (dVPN) architecture using blockchain.

Regional Leaders: North America projected at USD 1.9 Billion by 2033 with high premium subscription penetration; Europe at USD 1.4 Billion driven by GDPR-compliant tools; Asia-Pacific at USD 1.1 Billion fueled by 65% mobile-first VPN adoption.

Consumer/End-User Trends: Over 52% of VPN users access services for streaming geo-restricted content, while 44% prioritize identity protection and secure transactions.

Pilot or Case Example: In 2024, a U.S.-based VPN provider implemented AI-based traffic filtering, achieving 28% latency reduction and 40% malware blocking improvement.

Competitive Landscape: Market leader holds approximately 22% share, followed by NordVPN, ExpressVPN, Surfshark, Proton VPN, and CyberGhost.

Regulatory & ESG Impact: GDPR and CCPA enforcement increased privacy compliance adoption by 38%; 30% of providers committed to carbon-neutral server operations by 2030.

Investment & Funding Patterns: Over USD 3.5 Billion invested globally in consumer cybersecurity startups between 2022–2025, with rising venture capital focus on privacy SaaS platforms.

Innovation & Future Outlook: Integration of VPNs with identity monitoring, password management, and AI-based privacy dashboards is reshaping bundled subscription ecosystems.

Consumer VPN services account for approximately 58% of total market deployment, followed by encrypted messaging and anti-tracking software at 27% and identity protection tools at 15%. North America contributes nearly 40% of global consumption, while Asia-Pacific records over 65% mobile-based VPN usage. Recent innovations include RAM-only servers, multi-hop encryption, and AI-powered phishing detection, aligning with tightening data protection regulations and rising digital payment volumes.

The Consumer VPN and Digital Privacy Tools Market holds strong strategic relevance as digital ecosystems expand across finance, healthcare, education, and entertainment platforms. With more than 5.3 billion global internet users and over 1.5 billion cyberattack incidents reported annually, personal data protection has become a business-critical requirement rather than a discretionary expense. Organizations are increasingly integrating consumer-grade VPN services into employee remote-access policies, expanding the addressable market beyond individual subscriptions.

AI-based traffic analysis delivers 35% faster anomaly detection compared to traditional signature-based firewall systems, improving proactive threat mitigation. North America dominates in deployment volume, while Asia-Pacific leads in user adoption growth with over 65% of new VPN subscriptions originating from mobile devices. Europe remains compliance-focused, with over 70% of privacy tool vendors aligning product architecture with GDPR requirements.

By 2028, AI-driven automated encryption management is expected to reduce manual security configuration errors by 40% and cut response times to cyber incidents by 30%. ESG initiatives are also shaping strategies, with firms committing to 25% energy efficiency improvements in data center operations by 2030. In 2024, a leading U.S. provider achieved a 32% improvement in connection stability through AI-based server load balancing.

Going forward, the Consumer VPN and Digital Privacy Tools Market will serve as a pillar of digital resilience, regulatory compliance, and sustainable cybersecurity infrastructure, positioning privacy technologies as foundational assets in the global digital economy.

The Consumer VPN and Digital Privacy Tools Market is shaped by accelerating digitization, regulatory enforcement, and growing cybersecurity awareness among individuals and small enterprises. Increasing remote work participation—estimated at over 30% of the global workforce—has expanded reliance on encrypted connectivity solutions. Rising cybercrime costs, which exceed USD 8 trillion globally, are prompting both consumers and service providers to prioritize secure communication channels. Mobile-based VPN usage now accounts for more than 60% of total subscriptions in emerging economies, reflecting the dominance of smartphone internet access. Additionally, streaming platforms, fintech services, and e-commerce ecosystems are driving demand for secure browsing environments. Technological convergence, including AI-powered anomaly detection and multi-layer encryption, is transforming product capabilities while intensifying competitive differentiation across subscription tiers.

Cybercrime incidents have increased by over 38% globally in the past three years, with phishing and ransomware accounting for more than 60% of reported attacks. Identity theft cases surpassed 1.1 million annually in major digital economies, driving individuals to adopt encrypted browsing and IP-masking tools. Over 70% of public Wi-Fi networks remain unsecured, exposing consumers to data interception risks. VPN adoption among remote workers rose by 45% since 2022, reflecting enterprise-to-consumer behavioral spillover. Increased digital payment penetration—crossing 80% usage in developed markets—has further heightened the need for secure transaction environments. These measurable risk indicators directly stimulate demand for robust privacy tools integrated with advanced encryption and malware filtering features.

Despite growing demand, nearly 48% of internet users rely on free VPN services, which limits premium subscription conversion rates. Consumer subscription fatigue is rising, with average digital service subscriptions exceeding 12 platforms per household in developed markets. Free tools often compromise speed by up to 35% and restrict bandwidth usage, yet remain attractive due to zero upfront cost. Additionally, 41% of users cite performance lag and latency as key concerns when using encrypted connections. Regulatory scrutiny on data retention practices has also led to compliance costs increasing by approximately 20% for providers, impacting pricing flexibility and operational margins. These structural constraints slow widespread premium adoption.

Mobile internet users exceed 4.5 billion globally, with over 65% of VPN subscriptions now initiated through mobile app stores. The surge in digital banking—used by more than 2.8 billion people—creates substantial demand for secure mobile browsing environments. Emerging markets report smartphone penetration rates above 75%, offering scalable deployment opportunities for lightweight, app-based VPN services. Integration of privacy dashboards with password managers and identity monitoring tools can improve cross-selling rates by up to 30%. Additionally, decentralized VPN architectures leveraging blockchain-based node distribution reduce central server dependence by 25%, enhancing resilience and unlocking new subscription models for privacy-conscious consumers.

Encryption standards are evolving rapidly, with quantum computing advancements threatening traditional RSA-based protocols. Transitioning to quantum-resistant encryption may increase infrastructure costs by 18–25% over the next five years. Regulatory divergence between regions—such as data localization mandates in parts of Asia and strict privacy compliance rules in Europe—requires multi-layered compliance strategies. Approximately 33% of providers report operational strain due to cross-border data transfer restrictions. Furthermore, internet service providers in certain countries impose bandwidth throttling, reducing VPN speeds by up to 40%, affecting user experience. Balancing performance, compliance, and cost efficiency remains a critical operational challenge.

AI-Powered Threat Detection Improving Accuracy by 35%: Advanced AI algorithms now analyze user traffic patterns in real time, reducing false positives by 28% and improving malware detection rates by 35%. Over 60% of premium VPN providers have integrated machine learning engines to enhance intrusion prevention and predictive risk scoring.

Rapid Mobile VPN Adoption Surpassing 65% of New Subscriptions: Mobile-first deployment models dominate new user acquisitions, with app-based subscriptions growing 42% year-over-year. In Asia-Pacific, over 70% of VPN sessions originate from smartphones, reflecting the shift toward portable digital security ecosystems.

Multi-Hop and RAM-Only Servers Enhancing Data Protection by 40%: More than 55% of leading providers now operate RAM-only servers, eliminating persistent data storage. Multi-hop encryption configurations improve anonymity layers, reducing traceability risk by approximately 40% compared to single-server routing.

Bundled Privacy Suites Increasing Customer Retention by 30%: Integrated offerings combining VPN, password management, encrypted cloud storage, and identity monitoring have improved subscriber retention rates by 30%. Around 48% of new users prefer bundled cybersecurity packages over standalone VPN solutions, indicating a shift toward comprehensive digital protection ecosystems.

The Consumer VPN and Digital Privacy Tools Market is segmented across type, application, and end-user dimensions, reflecting evolving user priorities and technological sophistication. Product-level differentiation is increasingly centered on encryption strength, data retention policies, multi-device compatibility, and AI-driven threat detection capabilities. Applications range from secure browsing and streaming access to identity protection and encrypted communications, with usage intensity varying by geography and digital maturity. End-user segmentation highlights individual consumers as the dominant base, while freelancers, remote workers, SMEs, and digital content creators represent rapidly expanding cohorts. Over 65% of total subscriptions are now mobile-based, underscoring device-driven segmentation trends. Additionally, more than 48% of users prefer bundled privacy ecosystems combining VPN, password management, and identity monitoring, indicating convergence across product categories. Decision-makers are increasingly assessing segmentation not only by functionality but also by compliance alignment, latency performance, and integration with zero-trust frameworks, shaping procurement and subscription strategies globally.

The market is segmented into Standalone VPN Services, Bundled Privacy Suites (VPN + Password Manager + Identity Monitoring), Encrypted Messaging & Communication Tools, and Anti-Tracking & Ad-Blocking Software. Standalone VPN services currently account for approximately 54% of total adoption due to their simplicity, affordability, and high demand for IP masking and geo-unblocking capabilities. Bundled privacy suites hold nearly 26% share, driven by increasing consumer demand for comprehensive cybersecurity packages. However, decentralized VPN (dVPN) and blockchain-based privacy architectures are rising fastest, expanding at an estimated CAGR of 18%, as users seek distributed node infrastructure and reduced central data dependency. Encrypted messaging and anti-tracking tools collectively contribute around 20% of the market, serving niche yet critical roles in secure communications and browser-level privacy enhancement. While standalone VPNs dominate in volume, bundled ecosystems demonstrate stronger retention rates—improving subscription continuity by nearly 30% compared to single-feature offerings.

In 2024, a leading cybersecurity standards agency reported that over 60% of premium VPN providers adopted RAM-only server technology, eliminating persistent storage and enhancing data security compliance across global deployments.

Applications include Secure Browsing & Public Wi-Fi Protection, Streaming & Geo-Content Access, Digital Payments & Financial Transactions Security, Identity Theft Protection, and Encrypted Communication for Remote Work. Secure browsing and public Wi-Fi protection represent the leading application, accounting for approximately 38% of total usage, primarily due to the fact that over 70% of public Wi-Fi hotspots remain unsecured. Streaming and geo-content access hold about 29% share, reflecting increasing consumer demand for cross-border digital entertainment access. However, digital payment and fintech transaction security is the fastest-growing application segment, expanding at an estimated CAGR of 16%, supported by the fact that more than 80% of adults in developed economies use online banking platforms. Identity protection and encrypted communication applications collectively contribute around 33% of market activity. In 2025, nearly 44% of VPN users reported using services primarily for financial transaction protection, while over 52% cited streaming access as a key driver. More than 60% of Gen Z users prefer privacy-enabled browsing tools integrated into mobile ecosystems.

In 2024, a national cybersecurity agency documented that consumer VPN activation during peak online retail events increased by 47%, reducing reported phishing-related incidents by nearly 25% compared to previous cycles.

End-users are categorized into Individual Consumers, Remote Workers & Freelancers, Small and Medium Enterprises (SMEs), and Digital Content Creators & Influencers. Individual consumers represent the leading segment, accounting for approximately 62% of total subscriptions due to widespread adoption for streaming, browsing, and identity protection. Remote workers and freelancers hold about 18% share, driven by hybrid work models where over 30% of the global workforce operates partially remotely. SMEs are the fastest-growing end-user segment, expanding at an estimated CAGR of 17%, as small businesses adopt consumer-grade VPN solutions to secure distributed teams and cloud-based operations. Digital content creators and influencers contribute nearly 20% combined, leveraging VPNs for geo-testing content distribution and protecting intellectual property. In 2025, more than 38% of SMEs globally reported piloting encrypted connectivity tools for remote workforce management. Additionally, 58% of freelancers indicated that secure VPN access is mandatory when handling client data across borders.

In 2024, a recognized global technology advisory firm reported a 22% increase in cybersecurity tool adoption among SMEs, enabling over 500 small enterprises to strengthen encrypted remote access and secure cloud collaboration frameworks.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 16% between 2026 and 2033.

North America’s leadership is supported by over 92% internet penetration, with nearly 46% of adult internet users reporting VPN usage at least once. Europe follows with approximately 29% market share, driven by strict data privacy enforcement and cross-border data protection compliance frameworks. Asia-Pacific holds around 24% share, fueled by more than 65% mobile-based VPN subscriptions and over 2.5 billion smartphone users. South America contributes nearly 5%, while the Middle East & Africa collectively account for about 4%, supported by rising digital banking penetration exceeding 55% in key economies. Across all regions, more than 60% of new VPN subscriptions are app-based, while nearly 48% of users prefer bundled privacy ecosystems. Regional differences are shaped by regulatory stringency, mobile-first adoption trends, fintech growth, and the maturity of digital infrastructure.

North America holds approximately 38% market share in the Consumer VPN and Digital Privacy Tools Market, reflecting high digital maturity and strong consumer awareness. The United States and Canada collectively report internet penetration above 90%, while nearly 46% of internet users have engaged with VPN services. Key demand drivers include healthcare, financial services, e-commerce, and remote workforce ecosystems, where over 30% of employees operate in hybrid models. Regulatory developments such as the California Consumer Privacy Act (CCPA) and evolving federal cybersecurity directives have strengthened demand for encrypted browsing and identity monitoring solutions. Technological advancements include widespread adoption of AES-256 encryption, AI-driven threat analytics, and RAM-only server infrastructure, now implemented by more than 60% of premium providers. A leading regional player, Proton VPN’s U.S. operations, has expanded secure core server infrastructure, improving connection stability by nearly 30% during peak traffic periods. Consumer behavior indicates higher enterprise spillover, particularly in healthcare and finance, where secure remote access remains mandatory for compliance.

Europe accounts for approximately 29% of the global Consumer VPN and Digital Privacy Tools Market, with major markets including Germany, the United Kingdom, and France. Over 70% of digital service providers operating in the region align product architecture with GDPR compliance requirements. VPN usage penetration exceeds 35% among adult internet users, particularly in Western Europe. Regulatory bodies such as the European Data Protection Board have intensified enforcement actions, leading to a 38% increase in privacy tool subscriptions among compliance-sensitive users. Emerging technologies include quantum-resistant encryption pilots and multi-hop routing configurations adopted by over 45% of premium providers. A notable regional provider, NordVPN (European operations), expanded its RAM-only server network across more than 60 European cities, reducing data retention risks. Consumer behavior in Europe is strongly compliance-oriented, with increased demand for explainable privacy policies and transparent data handling frameworks, especially among financial services and digital health sectors.

Asia-Pacific represents approximately 24% of the global market volume, ranking third in total share but first in growth momentum. Key consuming countries include China, India, Japan, South Korea, and Australia. The region hosts over 2.5 billion smartphone users, and more than 65% of VPN subscriptions are mobile-app based. India alone records internet user growth exceeding 8% annually, contributing significantly to subscription expansion. Infrastructure trends include 5G deployment across more than 15 major economies, supporting high-speed encrypted traffic. Regional innovation hubs in Singapore, Bangalore, and Tokyo are investing heavily in AI-powered cybersecurity solutions. A leading provider in the region, Surfshark’s Asia-Pacific expansion, increased localized server capacity by 40% in 2024, enhancing streaming and fintech security performance. Consumer behavior reflects strong demand from e-commerce and mobile AI applications, where digital payment penetration surpasses 70% in urban centers.

South America contributes approximately 5% of the global Consumer VPN and Digital Privacy Tools Market, with Brazil and Argentina as key markets. Brazil accounts for over 60% of regional VPN subscriptions, supported by internet penetration nearing 80% in urban areas. Streaming consumption has grown by more than 25% year-over-year, driving demand for geo-access and IP masking tools. Infrastructure improvements include fiber broadband expansion across more than 12 metropolitan areas, improving encrypted connection stability. Government-backed digital inclusion programs have increased online banking usage above 55%, reinforcing the need for secure browsing. Regional trade policies promoting digital services have also expanded cross-border platform access. Consumer behavior indicates demand closely tied to media localization and multilingual streaming content, with nearly 48% of users citing entertainment access as a primary use case.

The Middle East & Africa region accounts for nearly 4% of global market share, with the UAE, Saudi Arabia, and South Africa leading adoption. Internet penetration exceeds 99% in the UAE and over 70% in South Africa, creating a foundation for encrypted digital services. Rapid digital transformation in oil & gas, construction, and financial services sectors is increasing cybersecurity awareness. Technological modernization initiatives, including smart city projects and 5G rollout across Gulf Cooperation Council countries, support secure data exchange. Digital banking adoption exceeds 65% in the UAE, reinforcing demand for VPN protection. A regional cybersecurity firm expanded secure cloud-based VPN offerings by 35% in 2024, targeting SMEs and freelancers. Consumer behavior reflects rising awareness of cross-border data protection, particularly among expatriate populations and mobile-first users.

United States – 34% Market Share: It is driven by high internet penetration above 92%, strong cybersecurity investment exceeding USD 20 billion annually, and widespread remote workforce adoption.

Germany – 9% Market Share: It benefits from strict GDPR enforcement, strong digital infrastructure, and over 85% household broadband penetration supporting encrypted connectivity adoption.

The Consumer VPN and Digital Privacy Tools Market is moderately fragmented, with more than 150 active global and regional competitors offering VPN, encrypted communication, identity protection, and bundled cybersecurity solutions. The top five companies collectively account for approximately 58% of total market share, indicating partial consolidation at the premium tier while long-tail providers compete aggressively on pricing and niche specialization. Market leaders differentiate through server footprint scale—leading providers operate 3,000 to 6,000+ servers across 60–100 countries—and advanced encryption protocols such as AES-256 and WireGuard-based architectures.

Strategic initiatives in 2024–2025 have focused on RAM-only server expansion, quantum-resistant encryption testing, and AI-driven threat detection integration. Over 60% of premium providers now offer multi-hop routing and kill-switch functionality as standard features. Mergers and acquisitions have increased, with cybersecurity holding groups consolidating smaller VPN brands to expand global reach and subscription bundling capabilities. Partnerships with cloud infrastructure providers and data center operators have improved latency performance by up to 30% in high-traffic regions.

Competitive positioning is increasingly ecosystem-driven, with nearly 48% of premium users preferring bundled privacy suites integrating VPN, password management, and identity monitoring. Innovation cycles are shortening, with major providers launching feature updates every 6–9 months to enhance encryption resilience and user interface performance. Pricing competition remains strong in emerging markets, where freemium conversion rates average 22–28%.

Proton VPN

CyberGhost

Private Internet Access (PIA)

IPVanish

TunnelBear

Windscribe

VyprVPN

Mullvad VPN

Hide.me

Avira Phantom VPN

Bitdefender VPN

Kaspersky VPN

McAfee Secure VPN

Technological evolution in the Consumer VPN and Digital Privacy Tools Market is centered on encryption efficiency, latency optimization, and AI-driven risk mitigation. Over 70% of leading providers now support the WireGuard protocol, delivering up to 40% faster connection speeds compared to legacy OpenVPN implementations. AES-256 encryption remains the dominant standard, adopted in more than 90% of premium offerings, while post-quantum cryptographic pilots are being tested to address emerging quantum computing risks.

RAM-only server infrastructure has gained prominence, with more than 60% of tier-1 providers eliminating persistent data storage to enhance privacy compliance. Multi-hop routing—implemented by over 55% of premium platforms—adds additional anonymity layers, reducing IP traceability risks by approximately 35–40%. AI-based traffic pattern analysis tools now detect anomalous behavior in real time, reducing false positives by 28% and improving malware detection accuracy by 35%.

Cloud-native deployment models enable rapid scaling across 80+ global data center locations, while edge computing integration reduces latency by up to 25% in high-demand regions. Mobile-first optimization is critical, as more than 65% of new subscriptions originate from smartphone applications. Biometric authentication integration and zero-knowledge architecture are emerging as differentiators, with nearly 45% of premium users prioritizing no-log transparency audits. Technological convergence with password managers, encrypted cloud storage, and identity monitoring tools is reshaping competitive positioning toward holistic digital privacy ecosystems.

• In 2025, Surfshark also expanded its global server network to over 4,500 servers across major regions, improving connectivity options and route diversity. The expansion also included patented self-healing infrastructure (Everlink) and route optimization technologies to maintain stable, uninterrupted VPN sessions. Source: www.surfshark.com

• In October 2025, Surfshark launched the world’s first 100 Gbps VPN servers in Amsterdam, representing a ten-fold increase in bandwidth capacity compared to the standard 10 Gbps servers. This infrastructure upgrade supports faster, more stable VPN connections for high-demand use cases like 4K/8K streaming, gaming, and large file transfers, helping future-proof VPN performance.

• In 2025, NordVPN expanded its security suite with a new email protection feature that scans inbox links in real time to warn users about phishing and malware risks, enhancing overall user cybersecurity. This was added to its growing suite of privacy and threat protection tools across platforms.

• In February 2026, NordVPN announced it had passed its sixth independent no-logs assurance engagement, reaffirming that it does not collect or retain user connection logs, thereby strengthening trust in its privacy policy and technical practices.

The Consumer VPN and Digital Privacy Tools Market Report provides a comprehensive assessment of product categories, deployment models, applications, end-user segments, regional performance, and technological innovations shaping the global privacy ecosystem. The report evaluates standalone VPN services, bundled privacy suites, encrypted messaging platforms, anti-tracking software, and decentralized VPN architectures. It analyzes usage patterns across secure browsing, digital payments, streaming access, identity protection, and remote workforce connectivity.

Geographically, the study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, accounting for over 95% of global digital connectivity penetration. The report examines mobile-first adoption trends, noting that more than 65% of VPN subscriptions are initiated through app-based platforms, and evaluates enterprise spillover effects where over 30% of remote employees rely on consumer-grade VPN tools.

Technology coverage includes WireGuard protocol deployment, RAM-only server infrastructure, AI-driven threat analytics, multi-hop encryption, biometric authentication integration, and quantum-resistant cryptography pilots. The scope further assesses compliance frameworks, including GDPR and regional data protection mandates affecting more than 70% of international providers.

Additionally, the report reviews competitive positioning of over 150 active vendors, subscription model innovations, freemium conversion dynamics averaging 22–28%, and the growing preference for bundled cybersecurity ecosystems among nearly 48% of premium subscribers. Emerging niches such as decentralized VPN networks, privacy dashboards, and integrated identity risk scoring platforms are also examined to provide forward-looking strategic insights for decision-makers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,680.0 Million |

| Market Revenue (2033) | USD 4,792.3 Million |

| CAGR (2026–2033) | 14% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia‑Pacific; South America; Middle East & Africa |

| Key Players Analyzed | NordVPN; ExpressVPN; Surfshark; Proton VPN; CyberGhost; Private Internet Access (PIA); IPVanish; TunnelBear; Windscribe; VyprVPN; Mullvad VPN; Hide.me; Avira Phantom VPN; Bitdefender VPN; Kaspersky VPN; McAfee Secure VPN |

| Customization & Pricing | Available on Request (10% Customization Free) |