Reports

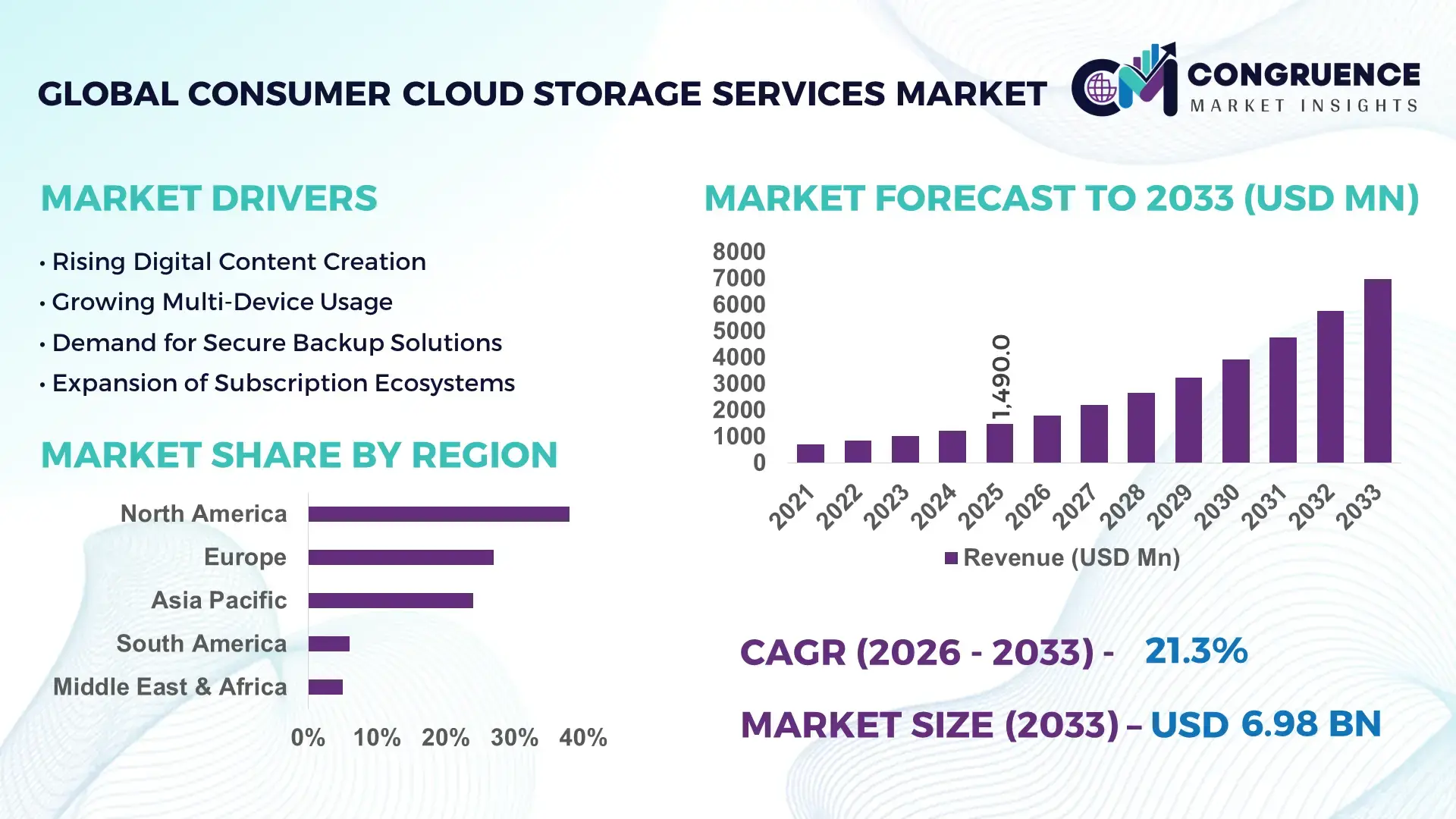

The Global Consumer Cloud Storage Services Market was valued at USD 1,490.0 Million in 2025 and is anticipated to reach a value of USD 6,983.5 Million by 2033 expanding at a CAGR of 21.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by exponential growth in personal digital content creation, increasing smartphone penetration exceeding 6.9 billion users globally, and rising demand for secure, scalable, and device-agnostic storage solutions.

The United States dominates the Consumer Cloud Storage Services Market in terms of infrastructure scale, technological innovation, and enterprise-backed consumer ecosystems. The country hosts over 45% of the world’s hyperscale data centers, with more than 5,000 operational facilities supporting large-scale consumer storage platforms. U.S.-based providers manage exabyte-level consumer data traffic annually, driven by high per-capita digital content generation exceeding 2.5 TB per internet user per year. Consumer adoption of paid cloud storage subscriptions in the U.S. exceeds 38% among internet users, significantly higher than the global average. The presence of advanced AI-driven storage optimization, edge data integration, and multi-device synchronization technologies further strengthens the country’s production capacity and service scalability across personal media, gaming backups, and smart home ecosystems.

Market Size & Growth: USD 1,490.0 Million (2025) projected to reach USD 6,983.5 Million by 2033 at 21.3% CAGR, fueled by rapid growth in digital media storage demand and cross-device synchronization needs.

Top Growth Drivers: 62% surge in mobile data generation, 48% increase in remote work adoption, 35% rise in paid subscription upgrades.

Short-Term Forecast: By 2028, AI-based storage optimization is expected to reduce redundant storage usage by 28% and improve retrieval speeds by 32%.

Emerging Technologies: AI-driven data classification, end-to-end zero-knowledge encryption, decentralized edge-cloud hybrid storage models.

Regional Leaders: North America projected at USD 2,750.0 Million by 2033 with high paid subscription penetration; Asia-Pacific at USD 2,100.0 Million driven by 70%+ mobile-first users; Europe at USD 1,650.0 Million supported by strict data compliance frameworks.

Consumer/End-User Trends: Over 58% of users prioritize automatic photo/video backup; multi-device households average 4.3 connected devices per user.

Pilot or Case Example: In 2024, a U.S.-based provider implemented AI deduplication tools reducing storage redundancy by 30% and improving upload efficiency by 25%.

Competitive Landscape: Market leader holds approximately 28% share, followed by Dropbox, Apple iCloud, Microsoft OneDrive, and Box.

Regulatory & ESG Impact: Data localization laws and GDPR-style compliance increased encrypted storage adoption by 40% across Europe.

Investment & Funding Patterns: Over USD 3.2 Billion invested globally in consumer cloud infrastructure expansion and edge data facilities during 2023–2025.

Innovation & Future Outlook: Integration with AI assistants, smart home ecosystems, and automated media categorization is reshaping premium subscription models.

Consumer Cloud Storage Services Market demand is primarily led by individual consumers (approx. 72%), followed by small home-based businesses and freelancers (18%), and digital creators (10%). AI-enabled file compression and intelligent indexing solutions have improved storage efficiency by nearly 30%. Regulatory frameworks such as GDPR and regional data protection acts are accelerating encrypted storage adoption. Asia-Pacific exhibits strong mobile-first consumption patterns, while North America shows higher paid-tier penetration. The market outlook remains strong with decentralized and hybrid storage ecosystems emerging as next-generation deployment models.

The Consumer Cloud Storage Services Market has become strategically critical as digital content generation surpasses 120 zettabytes globally, driven by high-resolution media, IoT-connected devices, and hybrid work ecosystems. Organizations increasingly integrate consumer-grade storage platforms with enterprise collaboration tools, creating unified personal–professional storage environments. AI-based intelligent tiering delivers 35% faster file retrieval compared to traditional block-based storage systems, improving user productivity and system efficiency.

North America dominates in volume of deployed infrastructure, while Asia-Pacific leads in adoption with over 64% of smartphone users actively utilizing some form of cloud backup service. By 2028, AI-powered predictive storage allocation is expected to reduce storage inefficiencies by 30% and lower energy consumption in hyperscale data centers by 18%. Firms are committing to ESG metrics including 40% renewable-powered data center operations by 2030 to reduce carbon intensity per stored terabyte.

In 2024, a leading U.S. cloud provider achieved a 27% reduction in server energy consumption through AI-based cooling optimization and workload balancing. Comparative benchmarks indicate that AI-driven deduplication systems deliver 30% higher storage optimization compared to legacy compression-only standards. The Consumer Cloud Storage Services Market is positioned as a pillar of digital resilience, regulatory compliance, and sustainable infrastructure modernization, ensuring long-term scalability and secure global data mobility.

The Consumer Cloud Storage Services Market is shaped by exponential personal data generation, mobile-first internet access, increasing cybersecurity awareness, and cross-platform ecosystem integration. Over 85% of smartphone users capture high-resolution photos and videos daily, significantly increasing storage consumption per user. Integration with productivity suites, smart home devices, and gaming platforms has expanded use cases beyond simple backup to real-time collaboration and media streaming. Edge computing and AI-based optimization are improving storage efficiency and reducing latency. Simultaneously, regulatory pressures around data privacy, encryption mandates, and cross-border data transfers are influencing infrastructure deployment strategies. Subscription-based pricing models and freemium tiers remain dominant, while premium upgrades are increasingly driven by enhanced security, family-sharing features, and AI-based organization tools.

Global smartphone shipments exceed 1.2 billion units annually, and users generate over 2.5 quintillion bytes of data daily. The average consumer owns more than four connected devices, increasing synchronization needs across smartphones, tablets, laptops, and smart TVs. Over 58% of internet users automatically back up photos and videos to cloud platforms. Additionally, 4K and 8K video adoption has increased storage requirements per user by nearly 40% in the past three years. The expansion of remote and hybrid work models, covering over 48% of knowledge workers globally, further amplifies demand for secure and accessible personal storage systems.

More than 2,200 data breaches were reported globally in a single recent year, exposing billions of records. Consumer trust remains sensitive to encryption standards and cross-border data transfer practices. Approximately 37% of users cite privacy concerns as a barrier to upgrading paid storage plans. Compliance with GDPR, CCPA, and other regional regulations increases operational complexity and infrastructure costs. Encryption, multi-factor authentication, and zero-knowledge architecture require continuous technological upgrades, creating technical and financial burdens for smaller service providers.

AI-powered deduplication, automated tagging, and predictive storage management can reduce redundant storage by up to 30%. Intelligent compression algorithms improve storage density while maintaining media quality. Voice-assisted file retrieval and AI-based content categorization enhance user engagement and premium subscription conversion rates. Emerging markets in Southeast Asia and Africa, where smartphone penetration exceeds 65% but paid storage adoption remains below 20%, represent significant untapped potential. Integration with decentralized storage and blockchain-based identity systems also opens avenues for secure peer-to-peer storage ecosystems.

Hyperscale data centers consume approximately 1–1.5% of global electricity production. Storage expansion to handle exabyte-scale data growth requires substantial capital expenditure in servers, cooling systems, and renewable integration. Energy costs per terabyte stored have increased by nearly 15% due to rising power tariffs in several regions. Environmental scrutiny and carbon reduction commitments require providers to invest in green infrastructure, which may increase upfront operational expenditure while balancing sustainability targets.

AI-Based Intelligent Storage Optimization Improving Efficiency by 30%: Advanced AI deduplication and automated indexing systems are reducing redundant file storage by nearly 30%, while improving retrieval speeds by 25%. Over 60% of premium users now rely on AI-generated file categorization and smart search functions, increasing user engagement and platform stickiness.

Zero-Knowledge Encryption Adoption Surpassing 40% of Premium Users: Consumer demand for enhanced privacy has pushed encrypted storage adoption beyond 40% among paid subscribers. Multi-factor authentication usage increased by 52% year-over-year, strengthening account-level protection and regulatory compliance alignment.

Edge-Integrated Cloud Backup Reducing Latency by 35%: Deployment of localized edge nodes has reduced file upload and retrieval latency by up to 35% in high-density urban regions. Asia-Pacific markets report over 70% mobile-first storage access, accelerating edge-cloud hybrid infrastructure investments.

Family and Multi-User Subscription Models Growing by 45%: Shared subscription plans covering up to 6 users per account have expanded by 45%, driven by multi-device households averaging 4.3 connected devices. Bundled ecosystems integrating storage with productivity and entertainment services are increasing customer retention by over 28%.

The Consumer Cloud Storage Services Market is segmented by type, application, and end-user, reflecting diversified usage patterns and evolving consumer storage behavior. Service-based models dominate deployment structures, supported by multi-device synchronization, AI-enabled content management, and secure backup features. Applications span personal media storage, file sharing and collaboration, and device backup, each driven by rising digital content creation and mobile-first access trends. End-user segmentation highlights individual consumers as primary adopters, followed by freelancers, digital creators, and small home-based enterprises leveraging scalable storage for professional workflows. Increasing demand for encrypted storage, family subscription plans, and ecosystem-integrated services further shapes segmentation dynamics. Decision-makers are observing a shift toward premium, value-added storage tiers offering AI classification, automatic backup, and cross-platform integration. Regional consumption patterns also vary, with North America showing high paid-tier adoption while Asia-Pacific leads in mobile-centric usage intensity.

The Consumer Cloud Storage Services Market by type includes Free (Freemium) Storage Services, Paid Subscription Storage Services, and Hybrid/Bundle Storage Services integrated with digital ecosystems. Paid subscription services currently account for approximately 54% of adoption, driven by increasing demand for higher storage limits, advanced encryption, and family-sharing features. Free storage services represent around 32%, functioning as entry-level platforms that encourage upgrades through limited storage caps and advertising-based monetization. Hybrid and bundled services—often integrated with productivity suites, smartphone ecosystems, or streaming platforms—collectively contribute about 14% but are expanding rapidly. While paid subscriptions lead in share, bundled ecosystem storage is the fastest-growing type, expanding at an estimated CAGR of 24.8% due to integration with smartphones, operating systems, and collaborative productivity tools. Consumers increasingly prefer seamless synchronization across 4–5 connected devices, encouraging bundled offerings that combine storage with value-added services such as AI-powered file organization. Other niche types, including decentralized peer-to-peer storage models, are emerging but currently represent a small portion of total adoption, contributing to innovation rather than scale dominance.

In 2024, the U.S. Federal Trade Commission highlighted that over 60% of major mobile device users rely on pre-integrated cloud storage services bundled with their operating systems, reinforcing the dominance of subscription and ecosystem-based storage models.

By application, the market includes Personal Media Backup, File Sharing & Collaboration, Device Backup & Synchronization, and Archival Storage. Personal media backup leads with approximately 46% share, as high-resolution photo and video generation per user has increased by nearly 40% over the past three years. Consumers prioritize automatic backup features for smartphones and tablets, especially with 4K and 8K video adoption increasing file sizes significantly. File sharing and collaboration account for nearly 28% of usage, driven by hybrid work models and freelance digital content creation. Device backup and synchronization represent about 18%, supporting cross-device continuity across smartphones, laptops, and smart home devices. Archival storage comprises the remaining 8%, primarily used for long-term document retention and secure storage of sensitive files. While personal media backup leads, file sharing and collaboration is the fastest-growing application segment, projected to expand at a CAGR of 23.6% due to the expansion of remote work, which now covers over 48% of knowledge workers globally. In 2025, more than 41% of freelancers reported using cloud-based collaboration tools integrated with storage platforms. Additionally, over 58% of consumers enable automatic media backup features on mobile devices.

In 2025, the European Commission’s Digital Economy report noted that more than 65% of EU households actively use cloud-based file sharing and backup services for personal and professional activities, reflecting strong application-level integration.

End-user segmentation includes Individual Consumers, Freelancers & Digital Creators, Small Home-Based Businesses, and Students/Educational Users. Individual consumers dominate with approximately 72% share, reflecting widespread smartphone adoption and daily media generation. This group primarily utilizes services for automatic photo/video backup and multi-device synchronization. Freelancers and digital creators account for roughly 14%, leveraging scalable storage for high-resolution media files, design assets, and client collaboration. Small home-based businesses represent around 9% of adoption, relying on secure storage for document management and customer communications. Students and educational users contribute nearly 5%, often using freemium services integrated with productivity platforms. While individual consumers lead in scale, freelancers and digital creators represent the fastest-growing end-user group, expanding at an estimated CAGR of 25.1%, supported by the growth of the creator economy, which now includes over 200 million active content creators globally. In 2025, more than 38% of micro-enterprises reported integrating consumer-grade cloud storage into daily operations. Additionally, over 60% of Gen Z users prefer platforms offering AI-based search and automatic categorization features.

In 2024, the U.S. National Telecommunications and Information Administration reported that 73% of American households used at least one cloud storage service, highlighting strong consumer-level adoption across demographic segments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 23.9% between 2026 and 2033.

North America’s leadership is supported by over 5,000 operational data centers and paid subscription penetration exceeding 40% among internet users. Europe follows with approximately 27% share, driven by strong data protection frameworks and over 65% household cloud usage in digitally advanced economies. Asia-Pacific holds nearly 24% share, supported by more than 1.8 billion smartphone users and rapid mobile-first adoption patterns. South America accounts for about 6%, with Brazil contributing over 45% of the regional demand. The Middle East & Africa collectively represent 5%, supported by increasing digital infrastructure investments exceeding USD 15 billion in recent years. Regional consumption patterns show higher premium-tier upgrades in North America, regulatory-driven encrypted storage demand in Europe, and mobile-centric freemium adoption models in Asia-Pacific.

North America holds approximately 38% of the global Consumer Cloud Storage Services Market share, supported by high broadband penetration exceeding 92% and smartphone usage above 85% of the population. Key industries driving demand include healthcare, finance, media & entertainment, and remote professional services, where secure personal–professional file synchronization is critical. Regulatory frameworks such as the California Consumer Privacy Act (CCPA) and evolving federal cybersecurity standards have increased encrypted storage adoption by nearly 40% among paid users. Technological advancements include AI-driven file classification, zero-knowledge encryption, and energy-efficient hyperscale data centers reducing cooling energy consumption by up to 25%. A leading regional provider, Apple iCloud, continues expanding private relay and end-to-end encryption features, supporting over 1 billion active devices globally. Consumer behavior shows higher premium subscription upgrades, with average paid storage plans exceeding 200 GB per user, reflecting strong willingness to invest in secure, scalable digital ecosystems.

Europe represents around 27% of the Consumer Cloud Storage Services Market, with Germany, the United Kingdom, and France accounting for more than 60% of regional demand. Over 65% of EU households use at least one cloud-based storage service. Strict regulatory oversight under GDPR has driven encrypted and regionally hosted storage solutions, increasing demand for compliance-centric platforms. Sustainability initiatives aligned with the European Green Deal have encouraged energy-efficient data centers, with renewable energy usage in some facilities exceeding 50%. AI-powered content indexing and privacy-focused storage architectures are widely adopted. A prominent European provider, pCloud, has expanded zero-knowledge encryption offerings and localized data hosting facilities to comply with cross-border data transfer restrictions. Consumer behavior reflects high sensitivity to privacy, leading to above-average adoption of encrypted premium tiers compared to global averages.

Asia-Pacific accounts for approximately 24% of the global market and ranks as the fastest-growing regional segment. China, India, and Japan collectively contribute over 65% of regional consumption, supported by more than 1.8 billion smartphone users. Rapid 5G rollout—covering over 70% of urban populations in advanced economies—has accelerated cloud synchronization speeds and high-definition media uploads. Infrastructure expansion includes hyperscale data center investments across Singapore, India, and South Korea. Regional technology hubs are integrating AI-driven storage optimization into super-app ecosystems. Alibaba Cloud has expanded consumer storage integration within digital payment and e-commerce platforms, enhancing user retention. Consumer behavior is predominantly mobile-first, with over 72% of users accessing storage primarily through smartphones, and freemium models driving large-scale onboarding before paid-tier conversion.

South America represents nearly 6% of the global Consumer Cloud Storage Services Market, with Brazil accounting for approximately 45% of regional usage, followed by Argentina and Chile. Rising broadband penetration—now exceeding 74% in Brazil—has supported growing cloud adoption. Media streaming, social networking, and localized language content creation are major demand drivers. Government-backed digital inclusion initiatives and tax incentives for data infrastructure have encouraged regional data center development. Local technology firms are partnering with global providers to enhance localized hosting capabilities. Consumer behavior is closely tied to multimedia storage, with over 60% of users utilizing cloud services primarily for video and social media backups, emphasizing affordability and language localization features.

The Middle East & Africa region contributes around 5% of global demand, led by the UAE, Saudi Arabia, and South Africa. Regional digital transformation investments exceed USD 20 billion across smart city and e-government initiatives. Oil & gas, construction, and public sector modernization projects increasingly integrate cloud-backed consumer interfaces for documentation and media management. Technological modernization includes localized cloud zones and renewable-powered data centers. In the UAE, data localization regulations have encouraged regional hosting expansion. A leading regional telecom-backed cloud provider has expanded consumer storage bundles integrated with mobile plans, increasing adoption among smartphone subscribers. Consumer behavior indicates rapid uptake of bundled storage services, particularly where mobile operators include 50–100 GB free tiers within premium data packages.

United States – 34% Market Share: It leads due to hyperscale data center concentration, high paid subscription penetration, and advanced AI-driven storage ecosystems.

China – 18% Market Share: It is driven by massive smartphone user volume, super-app ecosystem integration, and rapid domestic cloud infrastructure expansion.

The Consumer Cloud Storage Services Market is moderately consolidated, with more than 50 active global and regional service providers competing across freemium, premium subscription, and bundled ecosystem models. The top five companies collectively account for approximately 68% of total global adoption, reflecting strong platform-based dominance supported by integrated device ecosystems and productivity suites. Market leaders differentiate through storage capacity tiers ranging from 5 GB free plans to multi-terabyte premium offerings exceeding 2 TB per user.

Competition is driven by AI-enabled file management, zero-knowledge encryption, cross-platform synchronization, and bundled digital services. Strategic initiatives between 2023 and 2025 include infrastructure expansion across hyperscale data centers, renewable-powered hosting commitments exceeding 40% clean energy usage in certain regions, and integration of AI-driven search and categorization tools improving retrieval speeds by up to 30%.

Partnerships with telecom providers have increased bundled storage adoption by nearly 35% in emerging markets. Product launches emphasize family plans supporting up to 6 users per subscription, now accounting for over 20% of premium accounts. Mergers and technology acquisitions are focused on cybersecurity and encryption startups to enhance compliance readiness. Competitive intensity is further amplified by pricing differentiation, where average entry-level paid plans range between 100–200 GB, while premium tiers exceed 5 TB for professional creators.

Apple iCloud

Microsoft OneDrive

Amazon Drive

Sync.com

pCloud

Mega

IDrive

Tresorit

MediaFire

Degoo

Koofr

Internxt

The Consumer Cloud Storage Services Market is undergoing rapid technological evolution centered on artificial intelligence, advanced encryption protocols, and edge-integrated infrastructure. AI-driven deduplication and automated indexing reduce redundant storage by up to 30%, optimizing server utilization and lowering storage density costs. Machine learning algorithms now categorize over 90% of uploaded photos and documents automatically, enhancing user retrieval efficiency.

Zero-knowledge encryption and end-to-end encryption protocols are increasingly embedded, with more than 40% of premium users opting for enhanced privacy tiers. Multi-factor authentication adoption has increased by over 50% year-over-year in several developed markets.

Edge computing integration is reducing latency by 25–35% in high-density urban regions by enabling localized data caching. Additionally, object storage architectures capable of handling exabyte-scale datasets are replacing traditional block storage systems in hyperscale facilities. Renewable-powered data centers are gaining prominence, with leading providers targeting over 60% renewable energy utilization across operations.

Blockchain-based decentralized storage pilots are emerging to enhance data sovereignty and resilience, though adoption remains below 5%. Meanwhile, API integrations with productivity platforms enable real-time collaboration and synchronization across an average of 4–5 connected devices per user. These technological shifts position cloud storage platforms as intelligent data management ecosystems rather than simple file repositories.

• In November 2025, Google Drive launched a Data Migration Service that enables streamlined transfer of files from Dropbox and Microsoft OneDrive into Google Drive while preserving folder structures and permissions for up to 100 users or site migrations at a time, enhancing multi-platform onboarding efficiency. Source: www.techradar.com

• In October 2025, Dropbox announced the planned full integration of its Dash AI assistant into the core Dropbox storage experience, offering natural language search, intelligent file organization, and contextual summaries directly within the cloud platform to improve user search and management capabilities. Source: www.theverge.com

• In August–October 2025, Dropbox confirmed the phased shutdown of its Dropbox Passwords service, beginning August 28 with disabled edits and autofill functionality, followed by a full shutdown and secure deletion of stored credentials by October 28, 2025 as part of a strategic shift to focus on core storage-related innovations. Source: www.techradar.com

• In Early 2025, Microsoft OneDrive announced a major upcoming revamped Windows app with a full photo gallery view, AI-powered Photos Agent for intelligent photo search/album creation, and expanded editing tools for mobile platforms under its consumer cloud storage service roadmap. Source: www.theverge.com

The Consumer Cloud Storage Services Market Report provides comprehensive coverage across service types, application areas, end-user segments, and geographic regions. The analysis encompasses freemium, subscription-based, and ecosystem-bundled storage models, covering capacities ranging from entry-level 5 GB tiers to multi-terabyte plans exceeding 5 TB. Applications analyzed include personal media backup, collaborative file sharing, cross-device synchronization, and archival storage.

Geographically, the report evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global demand distribution. The scope includes assessment of over 50 active providers operating hyperscale, regional, and decentralized infrastructures. It also covers technological dimensions such as AI-based content indexing, encryption standards, edge computing deployment, renewable-powered data centers, and blockchain storage pilots.

Industry focus areas include smartphone-driven data generation exceeding billions of gigabytes daily, multi-device households averaging more than four connected devices, and subscription conversion dynamics within digital ecosystems. The report further evaluates regulatory compliance frameworks, cybersecurity integration, telecom partnerships, and emerging mobile-first storage consumption patterns. Decision-makers gain strategic insight into competitive positioning, innovation pipelines, infrastructure expansion strategies, and evolving consumer adoption behavior shaping the long-term trajectory of the Consumer Cloud Storage Services Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,490.0 Million |

| Market Revenue (2033) | USD 6,983.5 Million |

| CAGR (2026–2033) | 21.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Google Drive; Dropbox; Box; Apple iCloud; Microsoft OneDrive; Amazon Drive; pCloud; Sync.com; Mega; IDrive; Tresorit; MediaFire; Koofr; Internxt |

| Customization & Pricing | Available on Request (10% Customization Free) |