Reports

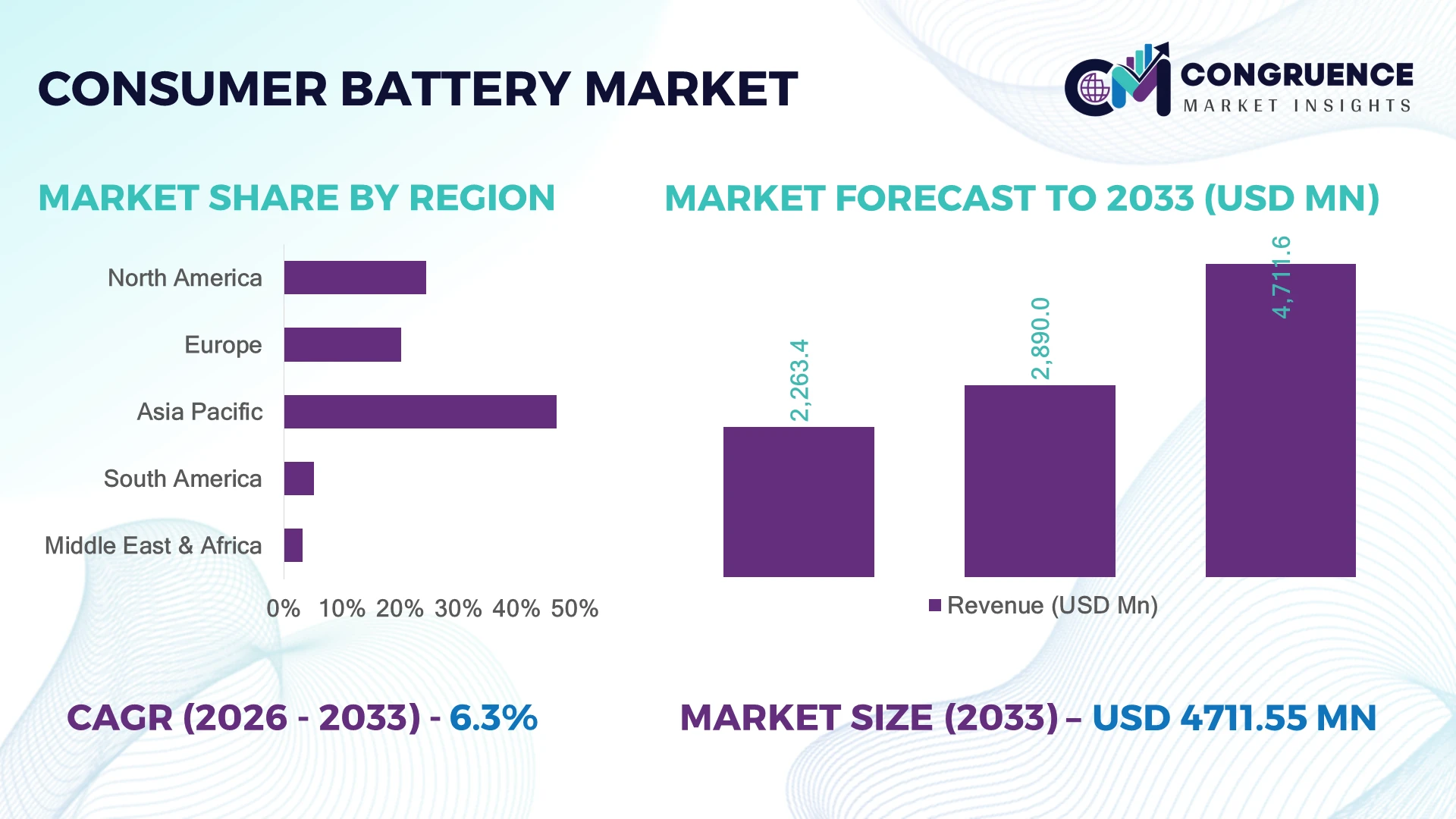

The Global Consumer Battery Market was valued at USD 2,890.0 Million in 2025 and is anticipated to reach a value of USD 4,711.6 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033. Growing adoption of portable electronics, expanding smart home ecosystems, and continuous improvements in rechargeable lithium-ion battery chemistry are accelerating product replacement cycles and strengthening long-term demand across consumer applications.

China dominates the global consumer battery landscape with nearly 42% of global manufacturing capacity, supported by investments exceeding USD 15 billion in advanced battery production and integrated supply chains serving consumer electronics. Compared with Japan's highly specialized premium battery ecosystem, China delivers significantly larger production volumes while South Korea leads in high-energy-density cell innovation. Ongoing localization initiatives following global supply-chain diversification are reinforcing production resilience and technology leadership.

These dynamics position manufacturers to prioritize localized production, advanced battery chemistries, and strategic supplier partnerships to strengthen long-term competitiveness.

Market Size & Growth: USD 2,890.0 Million (2025) to USD 4,711.6 Million (2033) at 6.3% CAGR, supported by rising rechargeable battery adoption in advanced consumer electronics.

Top Growth Drivers: Rechargeable battery demand (+28%), wireless device penetration (+24%), and smart home device adoption (+19%) continue to accelerate market expansion.

Short-Term Forecast: By 2028, battery energy density improves by nearly 15%, while manufacturing waste declines by around 10% through process optimization.

Emerging Technologies: AI-enabled battery management, silicon-enhanced anodes, and solid-state research improve safety, charging speed, and lifecycle performance.

Regional Leaders: Asia Pacific exceeds USD 2.2 Billion, North America approaches USD 1.1 Billion, and Europe surpasses USD 0.8 Billion, driven by localized manufacturing expansion.

Consumer/End-User Trends: More than 68% of premium portable electronics now utilize rechargeable lithium-based batteries to improve operating life and sustainability.

Pilot/Case Example: In 2024, automated battery manufacturing upgrades improved production efficiency by approximately 18% while reducing quality defects.

Competitive Landscape: Top manufacturers collectively account for nearly 55% of market share, led by Panasonic, Duracell, Energizer, LG Energy Solution, and GP Batteries.

Regulatory & ESG Impact: Recycling initiatives increase battery material recovery by over 25%, supported by stricter circular economy regulations and supply-chain transparency.

Investment & Funding: More than USD 8 Billion has been directed toward capacity expansion, localization, and advanced battery material development amid global supply-chain shifts.

Innovation & Future Outlook: Fast-charging cells, sustainable materials, and intelligent battery management systems are redefining next-generation consumer battery performance and product differentiation.

The Consumer Battery Market continues to expand across portable electronics, wearables, gaming devices, smart home products, and cordless household appliances. Manufacturers are introducing silicon-enhanced lithium-ion cells, faster charging technologies, and improved battery management systems to extend operating life and safety. More than 60% of new premium portable devices now incorporate advanced rechargeable batteries, while supply-chain diversification and stronger battery recycling initiatives are reshaping procurement strategies and supporting long-term industry resilience, setting the stage for broader strategic transformation.

The Consumer Battery Market has become strategically important as manufacturers compete through battery performance, production efficiency, and resilient supply chains rather than price alone. Rapid expansion of connected consumer electronics, stricter sustainability expectations, and supply-chain restructuring are encouraging companies to localize manufacturing and diversify critical material sourcing. These changes are strengthening operational resilience while improving responsiveness to regional demand.

Advanced lithium-ion batteries now deliver approximately 25% higher energy density and up to 30% faster charging than conventional nickel-based technologies, enabling longer device operation and improved user experience. Asia-Pacific continues to lead large-scale manufacturing and cost-efficient production, while North America and Europe emphasize premium battery innovation, recycling infrastructure, and localized manufacturing capabilities. Over the next two to three years, automated production lines are expected to reduce manufacturing defects by nearly 15% while improving throughput.

Leading battery producers are expanding strategic partnerships with consumer electronics manufacturers to accelerate product launches and secure long-term supply agreements. Investments are increasingly focused on high-performance rechargeable chemistries, advanced battery management software, and recycling technologies that recover valuable raw materials. Companies combining manufacturing scale, technological innovation, and sustainable operations will strengthen competitive positioning and achieve greater long-term operational advantage in the evolving global consumer battery ecosystem.

The accelerating transition toward rechargeable, high-energy-density batteries across portable electronics is fundamentally reshaping the Consumer Battery Market. More than 68% of newly launched premium consumer devices now utilize rechargeable lithium-ion cells, while fast-charging adoption has increased by nearly 30% over the past three years. China's continued investment in integrated battery manufacturing and raw material processing has shortened production lead times and strengthened supply reliability despite ongoing geopolitical trade realignments. This structural shift enables manufacturers to introduce thinner, longer-lasting products with enhanced power efficiency. In response, leading battery suppliers are expanding automated production capacity, investing in silicon-anode research, and establishing long-term partnerships with consumer electronics brands to improve product differentiation and secure strategic supply contracts.

Dependence on lithium, graphite, and cobalt continues to expose battery manufacturers to procurement uncertainty and margin pressure. China currently refines over 70% of global graphite materials, while battery-grade lithium prices have experienced fluctuations exceeding 40% during recent market cycles, complicating procurement planning. Environmental compliance requirements and stricter material traceability standards further increase sourcing complexity for multinational manufacturers. These structural constraints affect production scheduling, inventory management, and long-term contract negotiations. To mitigate operational risks, companies are diversifying supplier networks across Australia and Canada, expanding localized processing capabilities, and increasing recycled material content to reduce dependence on highly concentrated upstream supply chains while improving procurement resilience.

Battery recycling, silicon-enhanced anodes, and sodium-ion technologies are creating new competitive opportunities beyond conventional cell manufacturing. Advanced recycling processes now recover up to 95% of valuable metals from end-of-life batteries, while silicon-based anodes can improve energy density by approximately 20% compared with conventional graphite designs. Japan and South Korea continue accelerating research into next-generation battery chemistries through public-private innovation programs supporting sustainable manufacturing. Companies are strengthening R&D collaborations, expanding closed-loop recycling ecosystems, and integrating digital battery traceability platforms to improve material utilization. A less obvious advantage lies in lowering raw material procurement risk while simultaneously strengthening ESG compliance and reducing lifecycle production costs.

Maintaining consistent battery quality during high-volume production remains a major operational challenge as manufacturers pursue increasingly compact and higher-capacity cells. Even minor manufacturing defects can reduce battery lifespan by more than 15%, while automated inspection systems increase quality detection rates by nearly 25% compared with conventional manual inspection. South Korea and Japan continue investing heavily in precision manufacturing and AI-based quality control to maintain premium product standards. Companies must simultaneously modernize production infrastructure, enhance workforce expertise in advanced battery engineering, and deploy predictive manufacturing analytics. Successfully balancing manufacturing scale, product safety, and process consistency will determine long-term competitiveness as consumer expectations and regulatory performance standards continue to evolve.

Advanced Cell Chemistry Adoption Battery manufacturers are accelerating deployment of silicon-enhanced lithium-ion cells and high-density cathode materials, improving energy density by nearly 20% while reducing charging time by approximately 30%. Consumer electronics brands are redesigning products around slimmer battery architectures, while Chinese manufacturers continue scaling automated cell production to improve consistency and reduce manufacturing waste. These upgrades strengthen product differentiation and shorten innovation cycles.

Localized Manufacturing Expansion Supply-chain diversification is driving battery producers to establish regional manufacturing hubs outside traditional sourcing centers. More than 35% of recent capacity announcements emphasize localized assembly, while production lead times have declined by nearly 18% through integrated supplier networks. Companies are expanding partnerships with component suppliers and automation providers to improve procurement flexibility and minimize disruptions triggered by evolving trade policies and logistics constraints.

Battery Recycling Integration Circular manufacturing practices are becoming a standard operational strategy as advanced recycling facilities recover up to 95% of lithium, nickel, and cobalt from spent batteries. Regulatory initiatives promoting material traceability are encouraging manufacturers to integrate recycled inputs into production. A less obvious advantage is improved long-term procurement stability, enabling companies to reduce exposure to raw material price fluctuations while strengthening sustainability performance.

Intelligent Battery Management Systems AI-enabled battery monitoring and predictive management software are improving charging efficiency by approximately 15% while extending operational lifespan by nearly 25%. Consumer device manufacturers are embedding intelligent battery diagnostics into smartphones, wearables, and cordless appliances to optimize performance. Companies are responding through software partnerships, cloud-connected energy analytics, and digital lifecycle management that enhance customer experience and reduce warranty-related costs.

Rechargeable Batteries remain the leading segment, accounting for nearly 44% of overall demand due to their long operating life, lower lifetime ownership cost, and widespread integration across smartphones, laptops, wearables, and cordless appliances. Their ability to support repeated charging cycles and fast-charging technologies makes them the preferred choice for premium consumer electronics. Lithium-ion Batteries represent the fastest-growing segment, with adoption increasing by approximately 18% annually across portable devices because of higher energy density and lighter weight. Manufacturers continue investing in advanced cathode materials, silicon-anode development, and automated production lines to improve battery safety and operational efficiency. Primary Batteries continue serving remote controls, flashlights, emergency equipment, and low-drain applications where extended shelf life remains critical. Alkaline Batteries maintain strong demand through household usage, while Nickel Metal Hydride Batteries retain strategic importance in rechargeable consumer products requiring dependable cycle performance. Zinc-Carbon Batteries remain relevant within cost-sensitive markets, whereas Others include emerging chemistries supporting niche applications. Companies are adjusting product portfolios toward premium rechargeable technologies while maintaining diversified offerings to address varying consumer requirements.

Consumer Electronics constitute the dominant application segment, representing approximately 52% of battery consumption as smartphones, tablets, laptops, wireless earbuds, and gaming devices require higher-capacity rechargeable power solutions. Increasing integration of AI-enabled features and high-resolution displays continues raising battery performance requirements. Wearable Devices represent the fastest-growing application, supported by nearly 22% annual shipment expansion for smartwatches and fitness trackers. Manufacturers are introducing compact, lightweight batteries with enhanced charging efficiency to accommodate continuous health monitoring and connected functionality. Household Appliances continue expanding battery utilization in cordless vacuum cleaners, kitchen appliances, and smart home products, while Medical Devices benefit from improved battery reliability supporting portable diagnostic equipment and home healthcare devices. Toys & Games increasingly incorporate rechargeable power systems to enhance usability and reduce replacement frequency. Others include specialized portable products requiring customized battery configurations. Companies are strengthening manufacturing flexibility, integrating advanced battery management systems, and collaborating with consumer electronics brands to address evolving application requirements.

Residential Consumers represent the largest end-user segment, contributing nearly 60% of total battery demand as households increasingly rely on smartphones, tablets, wireless accessories, portable entertainment systems, and smart home devices. Frequent product upgrades and growing dependence on rechargeable electronics continue supporting consistent battery replacement and purchasing activity. Healthcare is emerging as the fastest-growing end-user segment, with battery adoption increasing by approximately 17% as portable medical equipment, home monitoring devices, and wearable health technologies become more widely deployed. Manufacturers are responding through customized battery designs emphasizing safety, reliability, and extended operating life.Commercial users continue utilizing batteries across retail electronics, office equipment, and service applications requiring dependable portable power. Industrial buyers prioritize batteries for handheld instruments, inspection equipment, and communication devices, while Retail remains strategically important through expanding omnichannel battery distribution and premium product positioning. Others encompass specialized portable equipment across education and public services. Companies are strengthening distribution partnerships, introducing application-specific battery solutions, and optimizing pricing strategies to improve customer retention across multiple end-user segments.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.9% between 2026 and 2033.

North America represents a strategically important Consumer Battery Market driven by domestic battery manufacturing expansion, advanced consumer electronics demand, and resilient supply-chain development. The region accounts for approximately 24.5% of global market activity, supported by increasing investment in localized battery production and recycling infrastructure. Growing deployment of AI-enabled portable devices and premium wearables continues strengthening demand for high-performance rechargeable batteries. Recent investments in automated battery assembly facilities have improved production efficiency by nearly 18%, while partnerships between battery manufacturers and electronics companies are shortening product commercialization timelines. Companies continue prioritizing regional sourcing strategies and intelligent manufacturing technologies to strengthen operational resilience and reduce external supply dependence.

United States Market Outlook: The United States remains the regional technology leader due to its strong consumer electronics ecosystem, expanding battery recycling infrastructure, and advanced manufacturing investments. More than 65% of North America's premium portable electronics demand originates from the country, encouraging manufacturers to establish localized production and research facilities. Federal support for domestic battery supply chains and increasing enterprise collaboration on next-generation battery technologies continue improving manufacturing competitiveness while strengthening long-term supply security.

Europe continues strengthening its Consumer Battery Market through circular economy initiatives, advanced battery recycling, and stricter sustainability regulations. The region contributes approximately 20.2% of global market demand, supported by increasing deployment of rechargeable batteries across consumer electronics and household appliances. New battery traceability requirements are accelerating digital supply-chain management while encouraging manufacturers to expand recycled material utilization. Several battery production facilities are integrating automated quality control systems capable of reducing manufacturing defects by nearly 15%. Companies are aligning product development with environmental compliance while investing in localized production capacity to improve strategic autonomy.

Germany Market Outlook: Germany serves as Europe's principal battery manufacturing and innovation hub, supported by advanced industrial automation, precision engineering, and established electronics manufacturing capabilities. The country continues expanding battery research partnerships between industrial enterprises and academic institutions while increasing investment in automated production technologies. Approximately 30% of Europe's advanced battery development projects involve German organizations, reinforcing the country's leadership in premium rechargeable battery technologies and sustainable manufacturing practices.

Asia-Pacific dominates the Consumer Battery Market through unmatched manufacturing capacity, vertically integrated supply chains, and large-scale consumer electronics production. The region accounts for approximately 46.8% of global market activity and produces well over 70% of rechargeable consumer batteries. Continuous investments in gigafactory-scale production, automated manufacturing systems, and advanced material processing have improved production efficiency by nearly 20%. Strong export capabilities and integrated supplier ecosystems enable manufacturers to rapidly scale production while maintaining competitive costs. Enterprises continue expanding regional manufacturing footprints and investing in next-generation battery chemistries to preserve global leadership.

China Market Outlook: China remains the world's largest consumer battery manufacturing center with extensive control across battery materials, cell production, and consumer electronics supply chains. The country produces more than 40% of global lithium-ion battery output for consumer applications while continuing large-scale investments in intelligent manufacturing and battery recycling infrastructure. Strong government support for industrial modernization and integrated supplier networks enables rapid commercialization of advanced battery technologies and sustained manufacturing competitiveness.

South America is witnessing steady Consumer Battery Market expansion as smartphone penetration, cordless appliances, and portable electronic devices become increasingly widespread. The region contributes approximately 5.2% of global market demand while gradually strengthening battery assembly and distribution capabilities. Infrastructure limitations and dependence on imported battery cells continue affecting production scalability; however, regional distributors are improving logistics efficiency through localized warehousing and supply-chain partnerships. Consumer demand for rechargeable batteries has increased by approximately 16%, encouraging manufacturers to broaden product availability and strengthen retail distribution networks.

Brazil Market Outlook: Brazil represents the largest Consumer Battery Market within South America due to its sizeable consumer electronics industry, extensive retail infrastructure, and expanding digital economy. Domestic electronics manufacturers continue increasing procurement of rechargeable battery technologies while distributors strengthen localized inventory management. Battery demand from smartphones, household appliances, and portable consumer devices remains strong, encouraging international battery manufacturers to expand commercial partnerships and improve regional product availability.

The Middle East & Africa Consumer Battery Market is advancing through digital infrastructure development, rising smartphone adoption, and expanding consumer electronics distribution. The region represents approximately 3.3% of global market activity, supported by increasing investments in retail modernization and logistics infrastructure. Growth in e-commerce platforms has improved battery product accessibility, while deployment of automated distribution centers has reduced delivery times by nearly 20%. Companies continue strengthening regional partnerships and expanding localized distribution channels to improve operational efficiency despite varying infrastructure maturity across different countries.

United Arab Emirates Market Outlook: The United Arab Emirates has emerged as the region's leading commercial hub for consumer battery distribution owing to its advanced logistics infrastructure, free trade ecosystem, and strong electronics retail sector. Increasing investment in smart retail, digital commerce, and automated warehousing has strengthened battery supply efficiency across domestic and export markets. The country's strategic trade connectivity and expanding premium consumer electronics market continue attracting international battery manufacturers seeking broader regional market access.

The Consumer Battery Market is characterized by competition between global technology leaders including Panasonic Energy, Energizer Holdings, Duracell, Samsung SDI, and LG Energy Solution versus regional manufacturers such as GP Batteries and VARTA. The top five companies collectively control approximately 58% of the global market, reflecting moderate consolidation. Competition centers on battery performance, energy density, pricing, manufacturing scale, and supply-chain integration rather than cost alone. Premium manufacturers achieve up to 20% higher energy density through advanced lithium-ion technologies, while cost-focused suppliers compete with prices 15–18% lower in high-volume consumer electronics segments. Companies are strengthening market positions through localized manufacturing, long-term OEM partnerships, recycling investments, and vertical integration across battery materials and production. Competitive dynamics continue shifting toward advanced rechargeable technologies, intelligent battery management, and resilient sourcing strategies as supply security becomes a strategic differentiator. High capital investment requirements, battery safety certification, and proprietary cell technologies remain significant entry barriers. Winning requires manufacturing scale, continuous innovation, trusted OEM relationships, and diversified global supply networks.

Energizer Holdings

Duracell

Samsung SDI

LG Energy Solution

GP Batteries International Ltd.

VARTA AG

Maxell Ltd.

Toshiba Corporation

FDK Corporation

EVE Energy Co., Ltd.

Murata Manufacturing Co., Ltd.

Conventional alkaline and nickel-based batteries are steadily giving way to advanced lithium-ion platforms with higher energy density, faster charging, and improved lifecycle performance. Modern lithium-ion cells deliver nearly 25% greater energy density than previous-generation rechargeable batteries while reducing charging time by approximately 30%. More than 65% of premium consumer electronics now integrate intelligent battery management systems, enabling improved safety, optimized charging profiles, and longer operational life. Manufacturers adopting these technologies achieve stronger product differentiation and lower warranty costs.

Emerging technologies are reshaping product development priorities. Silicon-enhanced anodes increase energy density by approximately 20%, while AI-enabled battery diagnostics improve lifecycle prediction accuracy by nearly 15%. Solid-state battery research continues accelerating across Japan and South Korea as manufacturers pursue safer, higher-capacity consumer batteries. Digital manufacturing, automated inspection, and advanced recycling technologies are also improving production efficiency while strengthening material traceability and sustainability performance.

Between 2026 and 2028, commercialization of solid-state micro-batteries, sodium-ion platforms for cost-sensitive devices, and cloud-connected battery analytics will reshape competitive positioning. Early adopters with vertically integrated manufacturing, proprietary battery management software, and advanced materials expertise will benefit through faster product launches, improved operational efficiency, and stronger OEM partnerships. Companies delaying technology modernization risk losing premium market positioning as consumer electronics increasingly demand safer, lighter, and higher-performance battery solutions.

May 2025 – Panasonic Energy announced preparations to accelerate advanced cylindrical battery manufacturing and next-generation cell development to improve energy density by approximately 20%, strengthening long-term supply capability for high-performance battery applications and premium electronics. Source: www.batterypoweronline.com

December 2025 – Samsung SDI signed a lithium iron phosphate battery supply agreement valued at over 2 trillion won, repurposing U.S. production lines for energy storage batteries and strengthening manufacturing flexibility amid changing battery demand.

January 2026 – LG Energy Solution announced plans to secure more than 90 GWh of new energy storage battery orders while expanding production capacity beyond 60 GWh, reinforcing manufacturing competitiveness and advanced battery technology deployment.

February 2026 – LG Energy Solution and Samsung SDI expanded North American battery production strategies, with LG targeting over 80% of its energy storage capacity in the region while Samsung increased localized LFP battery production, improving supply resilience.

The report provides comprehensive analysis of the Consumer Battery Market across Rechargeable Batteries, Primary Batteries, Lithium-ion Batteries, Alkaline Batteries, Nickel Metal Hydride Batteries, Zinc-Carbon Batteries, and other emerging chemistries. It evaluates demand across Consumer Electronics, Household Appliances, Toys & Games, Wearable Devices, Medical Devices, and additional applications while assessing purchasing trends among Residential Consumers, Commercial, Industrial, Healthcare, Retail, and other end-user segments. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global industry activity.

The study examines manufacturing technologies, battery chemistry innovation, recycling developments, intelligent battery management systems, supply-chain transformation, and competitive positioning. It highlights deployment trends, production concentration, enterprise strategies, and technology adoption patterns supporting investment planning, capacity expansion, product development, and strategic partnerships. The report also identifies emerging market opportunities, competitive priorities, and operational benchmarks expected to influence business decisions and long-term market direction throughout the 2026–2033 forecast period.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,890.0 Million |

| Market Revenue (2033) | USD 4,711.6 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Panasonic Energy; Energizer Holdings; Duracell; Samsung SDI; LG Energy Solution; GP Batteries International Ltd.; VARTA AG; Maxell Ltd.; Toshiba Corporation; FDK Corporation; EVE Energy Co., Ltd.; Murata Manufacturing Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |