Reports

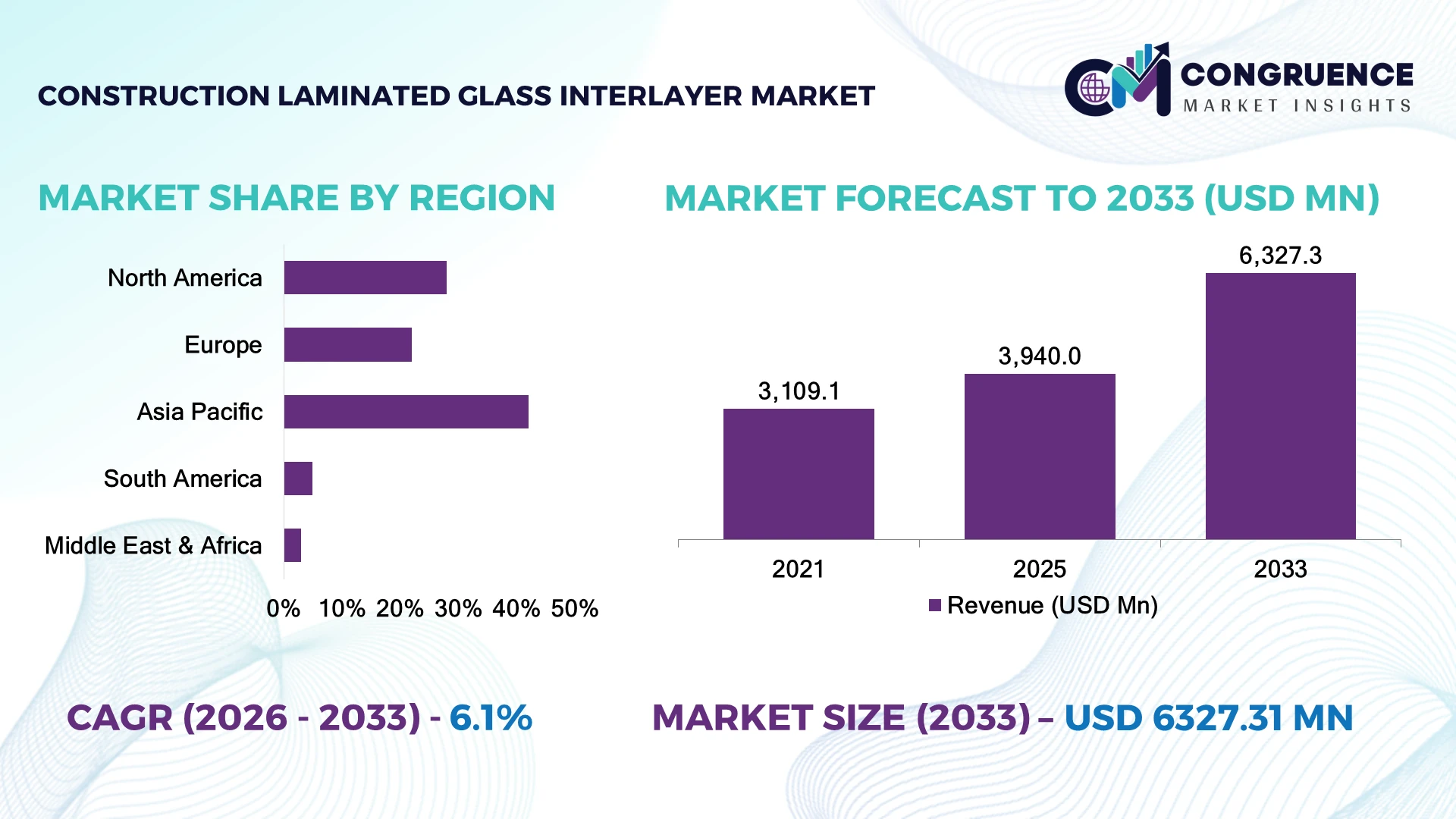

The Global Construction Laminated Glass Interlayer Market was valued at USD 3,940.0 Million in 2025 and is anticipated to reach a value of USD 6,327.3 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Growth is driven by stricter building safety codes, rising adoption of acoustic glazing, and increased use of advanced PVB and ionomer interlayers in energy-efficient architectural projects.

China dominates the market with nearly 35% share, supported by large-scale urban redevelopment, high-rise construction, and investments exceeding USD 100 billion annually in building infrastructure. The country’s smart building adoption exceeds 40%, while the United States accounts for around 25% share through premium architectural glazing demand and stringent safety standards. Compared with India’s rapidly expanding construction sector, China maintains over 30% higher laminated glass production capacity.

Strategic investments in advanced interlayer manufacturing and sustainable glazing solutions will determine future competitive positioning.

Market Size & Growth: USD 3.94 Billion (2025) to USD 6.33 Billion (2033) at 6.1% CAGR, driven by advanced safety glazing and energy-efficient construction trends.

Top Growth Drivers: Building safety regulations (35%), green construction adoption (30%), and acoustic insulation demand (25%) are the leading growth factors.

Short-Term Forecast: By 2028, automated interlayer processing reduces production waste by 15% while improving manufacturing efficiency by 20%.

Emerging Technologies: Advanced PVB formulations, ionomer interlayers, AI-based quality inspection, and automated glass processing are reshaping production.

Regional Leaders: Asia Pacific reaches USD 2.6 Billion with smart cities expansion; North America reaches USD 1.7 Billion through premium glazing adoption; Europe reaches USD 1.3 Billion through ESG-focused construction.

Consumer/End-User Trends: Over 45% of commercial building projects increasingly specify laminated glazing for safety, noise reduction, and thermal performance.

Pilot/Case Example: In 2024, high-performance laminated glazing projects in urban commercial buildings achieved nearly 20% improvement in acoustic insulation performance.

Competitive Landscape: Leading manufacturers hold approximately 40% combined share, with key players including Kuraray, Eastman Chemical Company, Sekisui Chemical, Trosifol, and Everlam.

Regulatory & ESG Impact: Green building policies improve adoption, with energy-efficient glazing contributing up to 30% reduction in building heat gain.

Investment & Funding: Over USD 5 Billion is directed toward advanced construction material expansion, automation, and sustainable glass manufacturing partnerships.

Innovation & Future Outlook: Next-generation interlayers with enhanced durability, solar-control capability, and recyclable material integration are shaping long-term market strategies.

The Construction Laminated Glass Interlayer Market is becoming increasingly important as architects and developers prioritize safer, quieter, and more energy-efficient buildings. Demand is accelerating across commercial towers, transportation infrastructure, and residential complexes, with advanced interlayers improving structural resilience and occupant comfort. Approximately 50% of new premium glazing projects now incorporate enhanced interlayer technologies, reflecting a shift toward performance-driven construction materials. Supply-chain diversification after recent global disruptions and regional manufacturing expansion are encouraging producers to establish localized production networks while improving material availability.

Construction laminated glass interlayers are becoming strategically important as building regulations, urban density, and sustainability requirements transform architectural design standards. Developers are increasingly shifting toward high-performance glazing systems that combine safety, thermal control, and acoustic benefits, creating new opportunities for advanced material manufacturers.

A major market shift is the transition from conventional PVB solutions toward engineered ionomer and acoustic interlayers. Modern interlayers deliver approximately 25% higher impact resistance and improved durability compared with traditional systems, reducing replacement requirements in demanding applications. Europe emphasizes sustainable renovation programs, while Asia Pacific leads large-scale commercial and infrastructure deployment through rapid urban modernization.

Operational adoption is expanding through smart manufacturing, automated quality monitoring, and regional production partnerships. For example, major glass processors are integrating automated lamination systems to reduce defects and improve production consistency by nearly 15%. Companies are prioritizing collaborations with construction firms and expanding localized facilities to strengthen supply resilience. Strategic positioning in advanced interlayer technologies will define competitive advantage as global construction markets move toward safer, greener, and higher-performance building solutions.

Rising adoption of high-performance laminated glazing is accelerating as governments enforce stricter building safety and energy-efficiency standards. In China, more than 40% of new commercial buildings incorporate advanced glazing solutions, while premium PVB and ionomer interlayers improve impact resistance by nearly 25% compared with conventional materials. The expansion of smart cities and high-rise construction is increasing demand for durable architectural materials. Companies are responding by investing in automated lamination facilities, localized production capacity, and partnerships with glass processors to deliver customized interlayer solutions. The strategic advantage is shifting toward manufacturers capable of combining safety performance, acoustic control, and sustainable material innovation.

Construction laminated glass interlayer producers face pressure from fluctuating polymer feedstock prices, limited specialty material suppliers, and complex international logistics. Raw material costs represent approximately 50–60% of total interlayer production expenses, creating profitability challenges during supply disruptions. European and Asian manufacturers experienced supply-chain constraints after global logistics disruptions, increasing lead times by nearly 20% for specialized materials. These conditions affect pricing stability and project scheduling for large construction developments. Companies are reducing exposure through supplier diversification, regional manufacturing investments, and long-term procurement agreements. A key operational challenge remains balancing cost control with consistent delivery of high-performance interlayer formulations.

Emerging opportunities are developing through advanced acoustic, solar-control, and recyclable interlayer technologies designed for sustainable construction applications. Green building projects represent more than 50% of premium commercial developments in major urban markets, increasing demand for energy-efficient glazing systems. Smart interlayers with enhanced UV protection and thermal performance are gaining adoption, improving building comfort while reducing operational energy consumption by approximately 20%. Companies are expanding R&D programs, forming partnerships with architectural firms, and developing customized solutions for transportation, residential, and commercial projects. A significant opportunity lies in integrating digital building models with performance-based glazing selection, enabling manufacturers to influence early-stage construction decisions.

Maintaining consistent quality across advanced laminated glass interlayers remains a major execution challenge as applications require precise optical clarity, durability, and environmental resistance. Approximately 15% of production losses in some processing environments are linked to defects caused by temperature control and lamination inconsistencies. Countries such as India and Brazil face additional challenges from limited specialized processing infrastructure and skilled workforce availability. Increasing demand for customized architectural glazing also raises integration complexity across different glass systems and construction standards. Companies must invest in automated inspection technologies, workforce training, and collaborative testing programs to ensure reliable deployment. Long-term competitiveness depends on achieving scalable manufacturing without compromising performance certification requirements.

Smart Interlayer Performance Shift Advanced PVB, ionomer, and acoustic interlayers are gaining adoption in premium construction projects, with high-performance glazing solutions improving sound insulation by 20–30% and enhancing impact resistance by nearly 25%. Developers in China, the United States, and Germany are integrating multifunctional interlayers into commercial towers and transport infrastructure. Companies are responding through formulation upgrades, automated production lines, and partnerships with architectural glass processors to improve customization and reduce processing losses.

Sustainable Building Material Transition Green construction requirements are accelerating demand for recyclable and low-carbon interlayer solutions, with more than 50% of premium building projects prioritizing energy-efficient glazing specifications. European renovation programs and stricter environmental standards are pushing manufacturers toward bio-based materials and improved recycling workflows. Companies are restructuring product portfolios around sustainable formulations, while suppliers are expanding regional manufacturing networks to manage supply-chain pressure and reduce material transportation impacts.

Automated Lamination Expansion Glass processors are increasingly adopting automated lamination and inspection systems, reducing production defects by approximately 15% and improving manufacturing consistency by 20%. Labor shortages in advanced manufacturing markets are encouraging investment in robotics, digital quality monitoring, and predictive maintenance technologies. Leading producers are scaling automated facilities to increase output reliability and meet growing demand for customized architectural glazing systems.

Architectural Safety Integration Building codes and urban development trends are increasing the integration of laminated glass interlayers in high-rise, commercial, and public infrastructure projects. More than 40% of newly developed premium buildings in major urban centers specify safety glazing solutions as a standard requirement. Companies are expanding technical collaborations with construction firms to deliver application-specific interlayers for earthquake resistance, security glazing, and acoustic performance.

Polyvinyl Butyral (PVB) interlayers dominate the Construction Laminated Glass Interlayer Market, accounting for approximately 65% market share, due to their established manufacturing ecosystem, optical clarity, safety performance, and compatibility with large-scale architectural glazing. PVB remains the preferred choice for commercial buildings, residential projects, and transportation applications because of its cost efficiency and proven durability. EVA interlayers represent around 20% share, supported by increasing use in decorative glazing and specialty applications requiring flexible processing. Ionomer interlayers are the fastest-growing segment, expanding as architects demand higher strength, improved edge stability, and enhanced performance in structural glazing systems. Adoption is rising in premium buildings where performance requirements exceed conventional materials. Companies are increasing investment in advanced polymer research, customized formulations, and regional production capabilities to capture high-value applications. The market shift indicates growing investment toward multifunctional interlayers that combine safety, energy efficiency, and architectural design flexibility.

Architectural glazing leads the application landscape with approximately 70% market share, driven by widespread use in commercial towers, residential complexes, airports, and institutional buildings. Increasing urbanization and stricter safety requirements are accelerating laminated glass adoption in facades, windows, and curtain wall systems. Commercial construction projects increasingly prioritize acoustic and thermal performance, with more than 40% of premium developments incorporating advanced glazing solutions. Transportation glazing is the fastest-growing application segment, supported by expansion of rail networks, electric mobility infrastructure, and safety-focused vehicle design. Demand for specialty interlayers in rail stations, airports, and automotive glazing is increasing as manufacturers seek lightweight and durable solutions. Decorative and security glazing applications continue developing through customized designs and higher-performance materials. Companies are expanding application-specific product lines, partnering with glass fabricators, and integrating digital design tools to improve project efficiency and material selection.

Commercial construction represents the largest end-user segment with approximately 55% market share, supported by extensive deployment in office buildings, shopping complexes, hotels, and high-rise developments. Large developers prioritize laminated glass interlayers for safety compliance, acoustic control, and premium architectural appearance. More than 45% of modern commercial projects now include advanced glazing requirements within design specifications. Infrastructure projects are the fastest-growing end-user category, driven by airport expansions, railway modernization, and public facility upgrades. Governments in countries such as China and India are increasing investments in urban infrastructure, creating demand for durable glazing systems with enhanced safety characteristics. Residential construction continues expanding through energy-efficient housing initiatives, while automotive and specialty users focus on customized performance solutions. Companies are targeting these segments through strategic partnerships with developers, construction contractors, and glass processors while expanding localized supply capabilities.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of7.2% between 2026 and 2033.

North America accounted for approximately 28% of the global Construction Laminated Glass Interlayer Market, supported by strong demand from commercial buildings, transportation infrastructure, and high-performance architectural projects. The United States remains the major contributor due to advanced glass processing capabilities, stringent safety standards, and widespread adoption of energy-efficient building materials. Nearly 45% of premium commercial developments specify laminated glazing solutions for safety and acoustic performance. Manufacturers are expanding production partnerships with architectural glass processors and investing in automated lamination technologies to improve consistency and reduce processing time. Infrastructure modernization programs and green building certifications continue influencing material selection across major construction projects.

United States Market Outlook: The United States represents the most strategically important market in North America due to its mature construction ecosystem and advanced glazing adoption. More than 40% of newly developed commercial projects in major cities incorporate performance-oriented glazing systems. Strong demand from office towers, airports, and institutional buildings is encouraging companies to expand customized interlayer solutions and strengthen domestic supply capabilities.

Europe accounted for nearly 22% of the global market, driven by renovation activities, energy-efficient building policies, and demand for sustainable architectural materials. Countries including Germany, France, and the United Kingdom are increasing adoption of advanced laminated glazing in commercial and public infrastructure projects. Around 50% of new premium building developments incorporate energy-performance requirements that support advanced interlayer usage. Manufacturers are focusing on recyclable materials, low-emission formulations, and partnerships with construction firms to meet evolving sustainability objectives. Modernization of aging buildings across European cities is creating additional demand for acoustic and thermal performance solutions while strengthening local production capabilities.

Germany Market Outlook: Germany leads Europe through advanced manufacturing expertise, engineering capabilities, and strong adoption of sustainable construction technologies. More than 45% of commercial renovation projects prioritize energy-efficient glazing solutions. The country’s established glass processing industry and focus on green building standards position it as a key market for innovative interlayer technologies and high-performance laminated glass applications.

Asia-Pacific accounted for approximately 42% of the global market, supported by large-scale construction activity, expanding manufacturing capacity, and rapid urban development. China, India, Japan, and South Korea represent major demand centers, with China contributing the largest share through high-rise construction and smart city projects. The region accounts for more than 50% of global laminated glass production capacity, creating strong supply advantages for interlayer manufacturers. Companies are increasing investments in regional production facilities, automation systems, and supply-chain localization strategies. Infrastructure expansion, commercial real estate development, and transportation projects are accelerating deployment of advanced laminated glazing solutions across major urban centers.

China Market Outlook: China dominates the Asia-Pacific market due to its extensive construction ecosystem and large-scale glass manufacturing base. The country contributes nearly 35% of global laminated glass production capacity and continues expanding smart building projects across major cities. Local manufacturers are investing in advanced polymer formulations and automated processing technologies to support growing demand for high-performance architectural glazing.

South America represents an emerging market supported by infrastructure upgrades, commercial development, and increasing adoption of safety glazing standards. Brazil and Argentina account for a significant portion of regional demand, with commercial buildings, transportation facilities, and residential developments driving usage. The region contributes approximately 5% of global market demand, with adoption concentrated in major urban centers. Limited domestic production capacity and dependence on imported specialty materials influence supply consistency. Companies are strengthening distribution networks, forming regional partnerships, and improving inventory strategies to manage supply challenges. Growing investment in airports, urban redevelopment, and public infrastructure projects is creating new opportunities for laminated glass interlayer suppliers.

Brazil Market Outlook: Brazil is the leading South American market due to its construction scale, commercial development activity, and infrastructure requirements. Major cities are increasing adoption of safety glazing in commercial and public buildings, with more than 30% of premium construction projects incorporating advanced glass solutions. Manufacturers are expanding local partnerships to improve availability and project support.

Middle East & Africa is gaining importance through large-scale infrastructure investments, luxury real estate developments, and modernization programs. The region accounts for approximately 3% of global demand, with adoption concentrated in Gulf countries including Saudi Arabia and the United Arab Emirates. Major urban developments and tourism infrastructure projects are increasing demand for durable, energy-efficient glazing systems. More than 40% of premium commercial projects in Gulf markets incorporate advanced architectural glass solutions. Companies are expanding regional partnerships, establishing distribution channels, and supporting customized glazing requirements for extreme climate conditions. Infrastructure transformation initiatives are creating demand for interlayers with improved thermal control and long-term durability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a key market due to large-scale urban development programs, commercial expansion, and infrastructure modernization. The country’s major construction projects increasingly integrate advanced glazing technologies to improve building efficiency and aesthetics. Investment in new cities, hospitality developments, and public infrastructure is encouraging suppliers to establish stronger regional partnerships and technical support networks.

The Construction Laminated Glass Interlayer Market features competition between global interlayer specialists and regional material suppliers. Leading players such as Kuraray, Eastman, Sekisui Chemical, and specialty glass material producers compete through technology leadership, while regional manufacturers focus on pricing and supply flexibility. The top five companies collectively account for approximately 55% of market influence. Competition is based on advanced formulations, customization, manufacturing reliability, and supply-chain control, with premium interlayers improving performance by 20–30% over conventional solutions. Companies are expanding production capacity, forming glass processor partnerships, and integrating digital quality systems. The competitive landscape is shifting toward sustainable materials, traceable supply networks, and higher-performance acoustic and safety solutions. Entry barriers remain high due to formulation expertise, certification requirements, and customer qualification cycles. Winning requires continuous material innovation, localized production strength, and the ability to deliver application-specific interlayer solutions.

Eastman Chemical Company

Sekisui Chemical Co., Ltd.

Everlam NV

Trosifol (Kuraray Advanced Interlayer Solutions)

Huakai Plastic Co., Ltd.

ChangChun Group

Wuhan Honghui New Material Technology Co., Ltd.

Kingboard Holdings Limited

Nippon Gohsei Co., Ltd.

Solutia (Saflex brand heritage)

Advanced PVB and ionomer interlayers are becoming central technologies in high-performance laminated glazing, replacing conventional materials through improved strength, acoustic control, and optical quality. Modern formulations deliver approximately 25% higher impact performance and 20% better sound insulation compared with standard solutions. Adoption is increasing in premium commercial buildings, airports, and smart infrastructure projects where performance-based materials are prioritized.

Digital manufacturing technologies are reshaping production workflows through automated lamination control, AI-based inspection, and predictive quality monitoring. These systems reduce manufacturing defects by nearly 15% and improve process consistency by around 20%. Large manufacturers benefit through higher throughput, reduced waste, and stronger customization capabilities, creating advantages over cost-focused suppliers relying on traditional processing methods.

Between 2026 and 2028, recyclable interlayers, smart glazing integration, and low-carbon material development will influence competitive positioning. Companies investing in sustainable polymer chemistry and automated production platforms will gain stronger access to green construction projects. The technology shift favors suppliers combining material innovation with digital manufacturing, enabling faster deployment, improved durability, and stronger alignment with evolving building performance standards.

September 2025 Kuraray introduced enhanced Trosifol interlayer solutions selected for advanced vehicle glazing applications, strengthening its specialty interlayer portfolio. The technology supports improved design flexibility and integration performance, with adoption in premium applications increasing through OEM collaborations and advanced glazing partnerships. Source: www.kuraray.com

September 2025 Kuraray announced blockchain-based traceability capabilities for critical laminate applications, improving material authentication and supply-chain transparency. The initiative strengthens quality control processes and supports customers requiring verified material tracking across advanced laminated glass production networks. Source: www.trosifol.com

October 2024 Sekisui Chemical adjusted S-LEC PVB interlayer pricing globally by 6–15% due to rising manufacturing and logistics costs. The action reflected supply-chain pressure management while maintaining stable availability of laminated glass interlayer products for construction and industrial applications. Source: www.sekisuichemical.com

April 2026 Kuraray announced a 10% price adjustment for Trosifol PVB interlayers and Mowital resin products globally due to increased raw material, transportation, and energy costs. The move highlights ongoing supply-chain cost management across advanced interlayer manufacturing.

The Construction Laminated Glass Interlayer Market Report covers detailed analysis across material types including PVB, EVA, and ionomer interlayers, along with applications such as architectural glazing, transportation glazing, decorative glazing, and security solutions. The report evaluates adoption patterns across commercial construction, residential development, infrastructure projects, and specialty end-user segments.

The study includes regional assessment across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing capabilities, technology adoption, supply-chain dynamics, and competitive positioning. It examines advanced technologies, sustainability-focused materials, automation trends, and emerging application areas to support investment planning, expansion strategies, supplier evaluation, and long-term competitive decision-making through 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,940.0 Million |

| Market Revenue (2033) | USD 6,327.3 Million |

| CAGR (2026–2033) | 6.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Eastman Chemical Company; Sekisui Chemical Co., Ltd.; Everlam NV; Trosifol (Kuraray Advanced Interlayer Solutions); Huakai Plastic Co., Ltd.; ChangChun Group; Wuhan Honghui New Material Technology Co., Ltd.; Kingboard Holdings Limited; Nippon Gohsei Co., Ltd.; Solutia (Saflex brand heritage) |

| Customization & Pricing | Available on Request (10% Customization Free) |