Reports

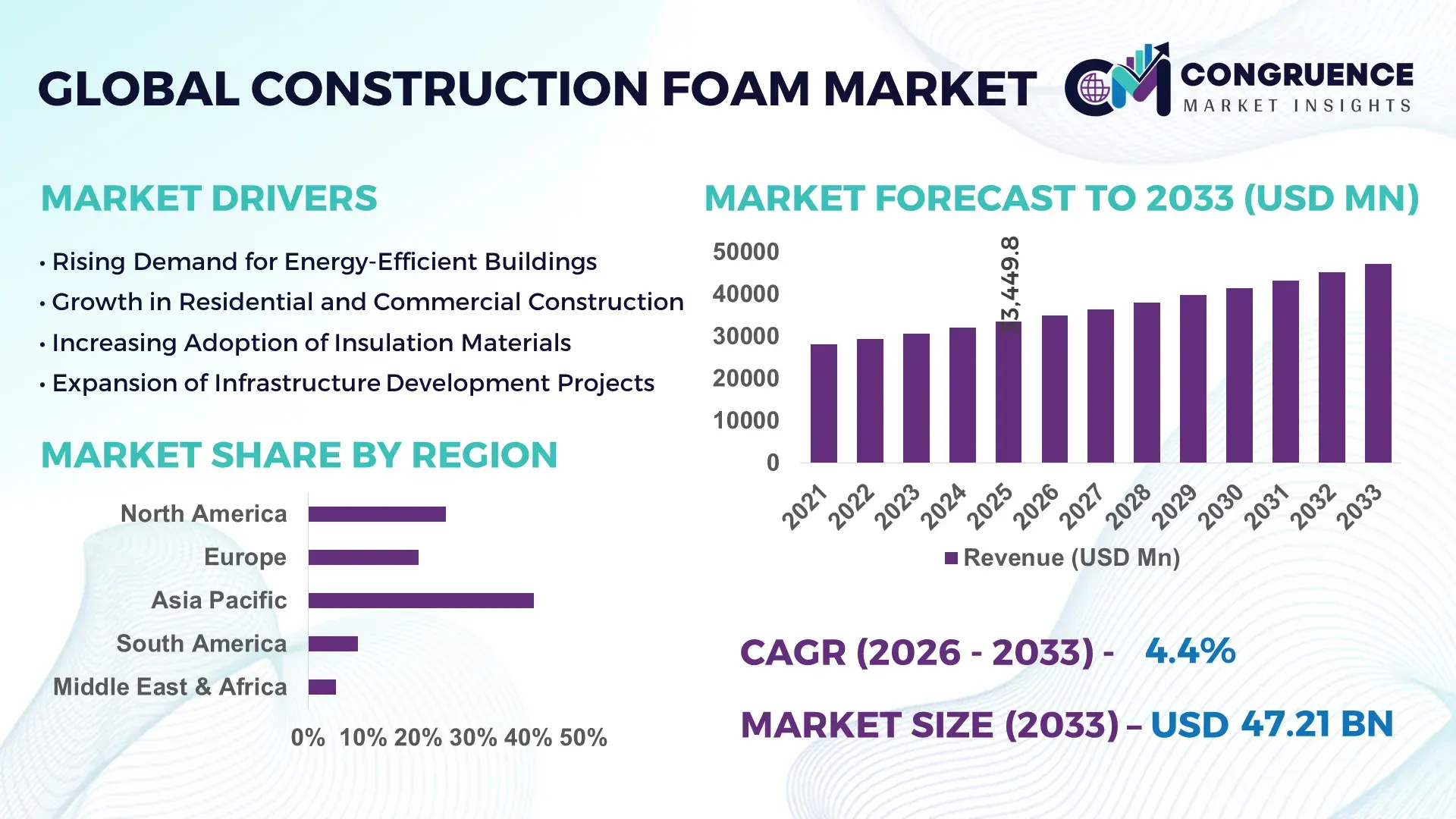

The Global Construction Foam Market was valued at USD 33449.76 Million in 2025 and is anticipated to reach a value of USD 47205.97 Million by 2033 expanding at a CAGR of 4.4% between 2026 and 2033. Growth is supported by increasing demand for advanced insulation solutions that enhance building energy efficiency, structural sealing performance, and long-term durability in modern infrastructure projects.

The United States maintains extensive production and technological deployment of construction foam across insulation, roofing systems, wall assemblies, and industrial construction applications. The country hosts more than 120 large manufacturing and formulation facilities producing polyurethane and specialty foam materials, with annual output exceeding 6 million metric tons used in building insulation systems. Spray foam adoption has expanded significantly, accounting for over 35% of newly constructed energy-compliant residential buildings and a growing portion of commercial retrofits. Infrastructure modernization investments exceeding USD 1 trillion between 2023 and 2026 have supported wider use of high-performance insulation materials. In addition, advancements in closed-cell foam technology, automated application equipment, and low-emission chemical formulations are improving installation efficiency and thermal performance across large-scale construction developments.

Market Size & Growth: Valued at USD 33449.76 Million in 2025 and projected to reach USD 47205.97 Million by 2033, registering a CAGR of 4.4%, supported by increasing demand for high-efficiency building insulation and advanced sealing materials in global construction projects.

Top Growth Drivers: Green building adoption increasing by 42%, insulation efficiency improvement reaching 30%, and modular construction integration growing by 26% across residential and commercial developments.

Short-Term Forecast: By 2028, advanced spray foam installation technologies are expected to lower installation costs by 18% and improve thermal insulation performance by approximately 22% in large building projects.

Emerging Technologies: Rapid development of bio-based polyurethane foam, automated spray foam robotics, and smart insulation systems with thermal monitoring capabilities.

Regional Leaders: Asia-Pacific projected to reach USD 18.6 Billion by 2033 driven by large housing developments; North America forecast to reach USD 15.2 Billion with strong retrofit demand; Europe expected to approach USD 9.4 Billion supported by strict energy-efficiency regulations.

Consumer/End-User Trends: Residential builders represent nearly 48% of construction foam usage, followed by commercial infrastructure developers and industrial facility operators prioritizing advanced thermal and moisture control performance.

Pilot or Case Example: In 2024, a large-scale urban housing insulation initiative achieved a 27% reduction in building energy consumption after installing high-density spray foam insulation across multi-unit residential structures.

Competitive Landscape: Market leadership estimated around 19% share held by a major global chemicals manufacturer, followed by several multinational materials, insulation, and polymer solution providers operating across construction supply chains.

Regulatory & ESG Impact: Expanding building energy codes, sustainability certifications, and low-emission material requirements are accelerating adoption of eco-efficient construction foam products globally.

Investment & Funding Patterns: More than USD 4.8 Billion invested in recent years toward manufacturing capacity expansion, advanced insulation technologies, and sustainable building material development initiatives.

Innovation & Future Outlook: Growth supported by recyclable foam technologies, carbon-reduction manufacturing processes, and integration of insulation systems into smart and energy-efficient infrastructure projects.

Construction foam demand is expanding across residential housing, commercial real estate, industrial facilities, and infrastructure modernization projects worldwide. Insulation applications account for approximately 52% of market demand, followed by sealing and gap-filling solutions at around 28% and structural reinforcement materials near 20%. Recent product innovations include ultra-low-global-warming-potential blowing agents, high-density insulation foam designed for extreme climate regions, and hybrid insulation systems integrated with prefabricated construction modules. Environmental regulations promoting energy-efficient buildings, combined with rapid urbanization in Asia-Pacific and large-scale infrastructure development programs in emerging economies, continue to influence regional consumption patterns. At the same time, renovation activity in developed markets and adoption of advanced installation technologies are strengthening long-term demand for high-performance construction foam materials.

The Construction Foam Market holds strategic importance in modern infrastructure development due to its role in improving energy efficiency, structural durability, and climate-resilient building systems. Advanced insulation and sealing materials are increasingly integrated into commercial complexes, industrial facilities, and large-scale residential projects to reduce heat transfer, minimize air leakage, and enhance building lifecycle performance. Industry adoption has accelerated alongside global green building programs, where high-performance insulation materials can lower building energy consumption by nearly 25–30% compared with conventional insulation practices. A key strategic shift involves advanced closed-cell spray polyurethane technology, where high-density insulation systems deliver 28% improvement in thermal resistance compared to traditional fiberglass insulation. This improvement is particularly relevant for large urban developments and energy-efficient smart buildings. Regionally, Asia-Pacific dominates in volume due to rapid urban construction and infrastructure expansion, while Europe leads in adoption with nearly 41% of construction enterprises implementing advanced insulation standards aligned with energy-efficiency frameworks.

Digital construction technologies are also influencing future pathways of the market. By 2028, automated spray application systems and AI-assisted building envelope design are expected to improve installation precision and reduce material wastage by approximately 20%. In addition, sustainability commitments are reshaping manufacturing practices, as firms are committing to ESG targets such as a 35% reduction in volatile emissions and recycling of polyurethane materials by 2030. A practical micro-scenario illustrates this shift: in 2024, large-scale retrofit housing programs in Germany achieved a 24% improvement in building insulation efficiency through deployment of advanced spray foam insulation technologies and digitally monitored installation processes. With continuous innovation, regulatory alignment, and investment in sustainable materials, the Construction Foam Market is increasingly positioned as a pillar of resilience, compliance, and long-term sustainable growth across the global construction ecosystem.

The global push toward energy-efficient infrastructure is a primary driver of the Construction Foam Market. Buildings account for nearly 36% of global energy consumption, prompting governments and developers to adopt insulation technologies that reduce heating and cooling loads. Construction foam provides high thermal resistance and airtight sealing, making it suitable for residential complexes, commercial buildings, and industrial facilities. In several advanced housing programs, foam-based insulation has reduced building heat loss by up to 40% compared with conventional insulation layers. Adoption is also expanding in smart city projects and green-certified construction, where materials that improve indoor climate control and energy savings are prioritized. In addition, increasing construction of cold-storage facilities, data centers, and logistics hubs is driving demand for specialized foam insulation systems that maintain temperature stability and operational efficiency.

Environmental regulations and chemical safety concerns present notable restraints for the Construction Foam Market. Certain foam formulations rely on chemical blowing agents and petrochemical-based inputs that face regulatory scrutiny due to their environmental impact. Governments in multiple regions have implemented stricter emissions standards and restrictions on high-global-warming-potential compounds used in insulation materials. Compliance requirements often require manufacturers to redesign formulations, upgrade production lines, and adopt alternative chemicals, which increases operational complexity. Additionally, improper installation practices can result in indoor air quality concerns and reduced insulation effectiveness, discouraging adoption among some construction stakeholders. Waste management and recycling challenges for polyurethane foam also remain an issue, as only a limited percentage of construction waste currently undergoes material recovery processes in many regions.

The shift toward sustainable construction presents significant opportunities for the Construction Foam Market. Developers are increasingly adopting green building certifications that require high-performance insulation materials capable of reducing energy consumption and environmental impact. Bio-based polyurethane foams derived from renewable feedstocks are gaining traction, with pilot production lines demonstrating up to 20% lower carbon intensity compared with conventional foam manufacturing processes. Expansion of prefabricated and modular construction is also opening new demand channels, as these projects rely on lightweight and easily applied insulation materials. Rapid infrastructure growth across Asia and the Middle East, including smart city developments and climate-resilient housing projects, is further creating opportunities for advanced foam insulation systems designed for extreme temperature and humidity conditions.

The Construction Foam Market faces operational challenges linked to fluctuating raw material prices and workforce limitations in specialized installation services. Key inputs such as polyols and isocyanates are influenced by global petrochemical supply conditions, causing periodic price instability for manufacturers and construction contractors. At the same time, spray foam installation requires trained professionals and precise application techniques to ensure performance and safety standards. In many regions, certified installation specialists remain limited, slowing project execution timelines. Additionally, large infrastructure and housing programs demand consistent material supply and standardized installation processes, which can be difficult to maintain during supply chain disruptions. These factors create operational pressures for market participants while encouraging investment in automated application technologies and workforce training initiatives.

• Rapid adoption of modular and prefabricated construction increasing insulation material demand by 55% in new projects. The adoption of modular construction is reshaping demand dynamics in the Construction Foam market as developers prioritize faster project delivery and lower operational costs. Approximately 55% of newly initiated building projects have reported cost benefits after integrating modular and prefabricated construction practices. Off-site manufacturing processes now handle nearly 40% of structural component preparation in advanced projects, reducing on-site labor needs by around 30%. Construction foam materials are increasingly integrated into prefabricated wall panels, roof assemblies, and floor insulation systems, enabling precise thermal control and improved structural sealing. Europe and North America collectively account for more than 60% of modular construction activity, where automated fabrication and energy-efficient materials are becoming standard across residential and commercial building developments.

• Growth of high-performance spray foam insulation improving building energy efficiency by up to 30%. Modern construction projects are shifting toward advanced spray foam technologies designed to enhance building envelope performance. High-density closed-cell spray foam systems can reduce air leakage by nearly 50% and improve thermal insulation performance by about 30% compared with older insulation layers. Around 48% of newly constructed energy-efficient residential buildings now incorporate spray foam insulation within walls, roofs, or foundations. Adoption is particularly strong in urban redevelopment zones where retrofitting aging structures requires materials capable of sealing irregular surfaces. Additionally, construction contractors are deploying automated spray equipment that increases installation accuracy by nearly 20%, enabling faster project completion across large commercial developments and high-rise infrastructure projects.

• Increasing use of low-emission and sustainable foam materials reducing environmental impact by nearly 35%. Environmental sustainability is influencing product innovation across the Construction Foam market, particularly in chemical formulations and production methods. Manufacturers are transitioning toward low-global-warming-potential blowing agents and recyclable polyurethane components, enabling approximately 35% reduction in lifecycle emissions for some insulation materials. Around 42% of newly launched construction foam products are now designed to meet green building standards or environmental certification requirements. Demand for sustainable insulation materials is rising across Asia-Pacific and Europe, where stricter building efficiency regulations are accelerating the shift toward eco-friendly construction practices. Furthermore, industrial facilities and large commercial complexes are adopting environmentally compliant insulation solutions to meet internal sustainability targets.

• Expansion of smart construction technologies improving installation productivity by 22%. Digitalization and advanced construction technologies are influencing how foam insulation systems are installed and managed across modern infrastructure projects. Smart construction platforms integrated with digital modeling and automated equipment are improving installation productivity by nearly 22% while reducing material waste by around 18%. Approximately 37% of large-scale construction projects are now using digital planning tools that optimize insulation placement and performance simulations before installation begins. Robotics-assisted spray foam application and sensor-based monitoring systems are also gaining traction in complex building environments such as data centers, cold storage facilities, and industrial warehouses, where precision insulation performance directly impacts operational efficiency and long-term energy management.

The Construction Foam Market demonstrates a diversified segmentation structure shaped by material formulations, application requirements, and end-user demand patterns across global construction activities. Product segmentation includes polyurethane foam, polystyrene foam, polyolefin foam, and phenolic foam, each serving specific insulation, sealing, and structural reinforcement roles. Polyurethane-based materials dominate large-scale infrastructure projects due to superior thermal resistance and moisture control performance. Application segmentation is primarily concentrated in insulation systems, sealing and gap filling, roofing systems, and structural support solutions integrated within modern buildings. Insulation applications alone account for more than half of installed construction foam usage globally, reflecting increasing energy-efficiency standards across commercial and residential construction. From an end-user perspective, residential construction remains the largest consumer segment, followed by commercial real estate developers and industrial facility operators who require temperature-controlled environments and durable building envelopes. Growing urbanization, retrofitting initiatives, and stricter building efficiency standards continue to influence how construction foam products are selected and deployed across diverse project categories worldwide.

Polyurethane foam remains the leading product category within the Construction Foam Market, accounting for approximately 52% of total product adoption due to its high thermal insulation capacity, structural strength, and compatibility with modern spray application technologies. Polystyrene foam holds about 23% adoption across large-scale building insulation projects, particularly in wall panels and foundation systems where rigid insulation performance is essential. However, polyolefin foam is emerging as the fastest-growing type, expanding at an estimated 6.8% annual growth rate as manufacturers introduce lightweight, recyclable materials suitable for sustainable construction and modular building systems. Phenolic foam and other specialty foam products together contribute nearly 25% of the market, serving niche applications such as fire-resistant insulation and industrial building envelopes requiring enhanced safety standards. Polyurethane foam continues to gain traction in high-performance building systems because it can improve insulation efficiency by nearly 30% compared with traditional mineral wool insulation in several controlled building performance tests. In addition, advanced closed-cell foam formulations are increasingly used in extreme climate construction zones due to superior moisture resistance and structural durability.

Insulation applications dominate the Construction Foam Market with approximately 56% adoption, driven by increasing demand for energy-efficient buildings and climate-controlled infrastructure. Sealing and gap-filling applications account for about 21% of usage, particularly in window installation, roofing systems, and structural joints where airtight construction is required. Roofing insulation and protective structural reinforcement represent emerging segments, with roofing applications becoming the fastest-growing category, expanding at an estimated 7.1% annual growth rate as commercial infrastructure projects adopt advanced weather-resistant insulation materials. Combined, other applications such as pipeline insulation, cold storage facilities, and transportation-related construction account for around 23% of total application demand. The growth of insulation-focused construction projects is also influenced by large-scale building renovation programs in urban regions, where older buildings require improved thermal performance to meet modern efficiency standards.

Residential construction represents the leading end-user segment in the Construction Foam Market, accounting for approximately 48% of global adoption as housing developers increasingly prioritize insulation performance and long-term energy efficiency in modern residential projects. Commercial construction follows with around 32% adoption, particularly in office buildings, retail complexes, hospitals, and data centers where building envelope performance directly impacts operational costs. Industrial infrastructure is emerging as the fastest-growing end-user category, expanding at an estimated 6.5% annual growth rate as manufacturing facilities, cold storage plants, and logistics hubs integrate advanced insulation technologies to improve environmental control and operational efficiency. Other sectors including institutional buildings, public infrastructure, and specialized construction projects collectively contribute about 20% of the market landscape. Furthermore, commercial developers are adopting foam insulation systems to support green building certifications, leading to higher adoption rates in large urban construction programs where sustainability and operational efficiency remain key priorities.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Asia-Pacific continues to dominate due to rapid urbanization, infrastructure development exceeding 65 million square meters of new commercial and residential construction annually, and increasing insulation adoption across manufacturing hubs. North America held approximately 27% of the market supported by renovation projects covering more than 18 million housing units requiring upgraded insulation materials. Europe accounted for nearly 22% driven by energy-efficiency directives impacting over 75% of new building permits issued in 2025. South America represented about 6% of the market with expanding infrastructure programs across transportation corridors exceeding 9,000 km of development projects. Middle East & Africa captured roughly 4% share but recorded the highest construction project pipeline growth, with more than 4,500 large-scale commercial developments underway. Increased adoption of advanced spray foam technologies, rising green building certifications by 35%, and improved building insulation standards across more than 40 national construction frameworks are strengthening regional demand patterns globally.

How are advanced building standards and large-scale renovations accelerating demand for high-performance insulation systems?

North America Construction Foam Market accounted for approximately 27% of the global market volume in 2025, supported by strong residential renovation activity and commercial infrastructure upgrades. Construction sectors such as housing retrofits, logistics warehouses, and cold-storage facilities are key industries driving demand, with more than 18 million residential units undergoing insulation improvements across the region. Regulatory frameworks such as updated building energy codes have increased adoption of high-efficiency insulation materials in nearly 60% of newly approved construction projects. Digital construction tools and automated spray insulation technologies are improving installation productivity by nearly 20%. A notable example includes initiatives by Dow Inc. expanding advanced polyurethane foam production and application technologies for energy-efficient building envelopes. Regional consumer behavior indicates higher adoption of advanced insulation solutions within commercial real estate and healthcare infrastructure where operational energy savings can reach 25% after insulation upgrades.

What factors are accelerating energy-efficient building materials adoption across advanced construction ecosystems?

Europe Construction Foam Market represented around 22% of global demand in 2025, with major contributions from Germany, United Kingdom, and France. These markets collectively account for more than 58% of regional construction insulation installations. Sustainability initiatives aligned with building efficiency directives have influenced over 70% of new commercial developments to integrate advanced insulation materials. Regional regulatory frameworks emphasize reduced emissions, improved thermal efficiency, and recyclable building materials, encouraging adoption of low-emission foam technologies. Digital construction planning platforms are being used in about 36% of large urban infrastructure projects to optimize insulation deployment and building performance simulations. A local industry example includes Saint-Gobain investing in next-generation insulation materials designed for high-performance building envelopes. Consumer behavior across the region shows strong preference for environmentally compliant construction materials that meet strict regulatory requirements and long-term building efficiency goals.

Why is rapid urban infrastructure development transforming insulation demand across emerging construction economies?

Asia-Pacific Construction Foam Market ranks first globally in volume consumption, accounting for nearly 41% of global installation across building projects. Leading consuming countries include China, India, and Japan, which together contribute more than 65% of regional construction material demand. Rapid expansion of urban housing projects exceeding 80 million square meters annually and industrial infrastructure development across manufacturing corridors are driving adoption of foam insulation systems. Regional innovation hubs are introducing automated building technologies and modular construction methods used in approximately 38% of large-scale developments. A notable example includes major regional manufacturers increasing capacity for spray polyurethane insulation products to support expanding smart city initiatives. Consumer behavior trends show strong demand for cost-efficient insulation solutions that improve durability and energy performance in dense urban housing developments.

How are infrastructure expansion and policy initiatives shaping advanced insulation adoption in emerging construction sectors?

South America Construction Foam Market accounted for approximately 6% of the global market volume, led primarily by Brazil and Argentina. Infrastructure development programs across transportation networks, residential housing, and logistics hubs exceeding 9,000 km of active construction projects are increasing the use of insulation materials. Government incentives promoting energy-efficient building practices and tax benefits for sustainable construction materials have influenced nearly 28% of new commercial developments. The energy and industrial sectors are adopting foam insulation systems for temperature-controlled facilities and storage infrastructure. Local manufacturers and building material distributors are expanding product availability and technical installation services across major urban centers. Regional consumer behavior indicates that demand is closely tied to expanding media, infrastructure, and urban housing sectors requiring durable and energy-efficient building materials.

What role do mega infrastructure projects and industrial diversification play in shaping advanced insulation demand?

Middle East & Africa Construction Foam Market held roughly 4% of global demand in 2025 but is witnessing rapid expansion in construction and industrial development. Major growth countries include United Arab Emirates and South Africa where large infrastructure projects, commercial complexes, and industrial facilities are increasing the need for advanced insulation materials. The region has more than 4,500 ongoing construction projects ranging from smart city developments to logistics and tourism infrastructure. Demand is also supported by oil, gas, and industrial sectors requiring temperature-resistant insulation for large facilities. Technological modernization such as automated construction equipment and energy-efficient building designs is gaining traction in approximately 30% of large-scale developments. Local building material suppliers are expanding insulation product lines to support these projects. Consumer behavior reflects growing interest in durable insulation solutions that withstand extreme climate conditions and improve building efficiency.

China – 24% market share in the Construction Foam Market due to large-scale infrastructure development, extensive manufacturing capacity, and strong construction demand across residential and industrial projects.

United States – 19% market share in the Construction Foam Market supported by advanced building technologies, widespread renovation activity, and high adoption of energy-efficient insulation systems.

The Construction Foam market is characterized by a moderately fragmented competitive structure with more than 120 active global and regional manufacturers involved in the production of polyurethane, polystyrene, and specialty insulation foams used in construction applications. The top 5 companies collectively account for approximately 46% of total global market activity, indicating strong competition alongside a broad presence of mid-sized producers and specialized material innovators. Leading participants focus heavily on advanced insulation technologies, sustainable chemical formulations, and automated installation systems designed to improve building performance and energy efficiency.

Strategic initiatives across the industry include more than 35 product innovation launches recorded in recent development cycles focusing on low-emission foam, recyclable insulation materials, and high-density structural foam systems. Partnerships between chemical manufacturers and construction technology providers have increased by nearly 28% as companies aim to integrate smart building technologies with insulation solutions. Mergers and supply-chain collaborations are also shaping the market, particularly in regions where construction demand is growing rapidly, such as Asia-Pacific and the Middle East. In addition, over 40 manufacturing facility expansions and capacity upgrades have been implemented globally to support increasing demand from residential and infrastructure development projects.

BASF SE

Dow Inc.

Huntsman Corporation

Covestro AG

Saint-Gobain

Recticel

Kingspan Group

Foam Supplies Inc.

Armacell International

JSP Corporation

Technological innovation is playing a significant role in shaping the Construction Foam Market, particularly through advancements in material science, automated installation systems, and sustainable chemical engineering. One of the most impactful developments is the evolution of closed-cell spray polyurethane foam systems that provide thermal resistance values up to 6.5 per inch of thickness, enabling buildings to reduce energy loss by approximately 30% compared with conventional insulation materials. These advanced formulations also enhance moisture resistance, structural rigidity, and long-term durability, making them suitable for complex building envelopes and high-performance construction projects.

Automation is also transforming installation processes within the industry. Robotic spray foam systems and digitally controlled application equipment are now being deployed in large infrastructure and industrial construction environments. These systems improve installation accuracy by nearly 22% while reducing material wastage by around 18%. In addition, digital modeling platforms integrated with building information modeling tools are being used in approximately 40% of large-scale construction projects to simulate insulation placement and optimize building energy performance before actual installation begins.

Another major technological trend is the development of low-global-warming-potential blowing agents and bio-based polyurethane foam materials. New-generation insulation products incorporating these materials can reduce lifecycle emissions by nearly 35% while maintaining high structural performance standards. Manufacturers are also exploring recyclable foam technologies that allow recovery of up to 25% of polyurethane material from demolition waste for reuse in insulation production. These innovations align with stricter environmental regulations and sustainability targets being implemented across multiple construction markets.

• In March 2025, BASF expanded its Elastopor® and Elastopir® insulation foam production capacity at its manufacturing facilities to support increasing demand for energy-efficient building materials in construction projects. The expansion focuses on improved insulation performance and lower-emission formulations for modern buildings. Source: www.basf.com

• In October 2024, Covestro introduced new climate-neutral polyurethane foam solutions using mass-balance technology to reduce fossil raw material usage in insulation applications. The innovation is designed for construction and refrigeration insulation systems and supports improved lifecycle sustainability targets in building materials. Source: www.covestro.com

• In May 2024, Kingspan Group launched advanced next-generation insulation products designed for high-performance building envelopes, improving thermal efficiency and moisture resistance for commercial and residential construction projects across Europe and North America. The products focus on supporting low-energy building standards. Source: www.kingspan.com

• In January 2025, Saint-Gobain announced the development of new sustainable insulation materials integrating improved fire safety and energy efficiency performance for large infrastructure and building renovation programs, supporting modern building compliance requirements across multiple construction markets. Source: www.saint-gobain.com

The Construction Foam Market Report provides a comprehensive analysis of the industry by examining multiple segments, technological developments, regional demand structures, and evolving construction practices shaping global adoption of insulation materials. The report evaluates more than 15 product categories and sub-types including polyurethane foam, polystyrene foam, polyolefin foam, phenolic foam, and specialty insulation materials designed for structural sealing, roofing insulation, and advanced thermal management systems. These products are assessed across key application areas such as building insulation, sealing and gap filling, roofing systems, infrastructure construction, and industrial facility insulation where thermal efficiency improvements can reach up to 30% compared with conventional insulation methods.

Geographically, the report covers over 25 major construction markets distributed across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional consumption trends, infrastructure investments, and technology adoption levels. The analysis also examines more than 40 major regulatory frameworks influencing building energy efficiency and environmental compliance standards across global construction projects. Additionally, the report includes insights into emerging technological innovations such as automated spray foam installation, smart insulation monitoring systems, and low-emission foam manufacturing technologies now being adopted in nearly 35% of modern building developments.

Industry coverage extends across residential construction projects exceeding tens of millions of new housing units annually, commercial real estate developments including logistics and data center facilities, and industrial infrastructure requiring advanced insulation performance. The report further reviews supply chain dynamics, manufacturing capacity expansions across more than 100 production facilities worldwide, and the role of sustainable materials in supporting next-generation building efficiency programs. This structured scope enables decision-makers to evaluate growth opportunities, technology adoption trends, and competitive positioning across the evolving Construction Foam Market landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Dow Inc. , Huntsman Corporation, Covestro AG , Saint-Gobain, Recticel, Kingspan Group , Foam Supplies Inc., Armacell International, JSP Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |