Reports

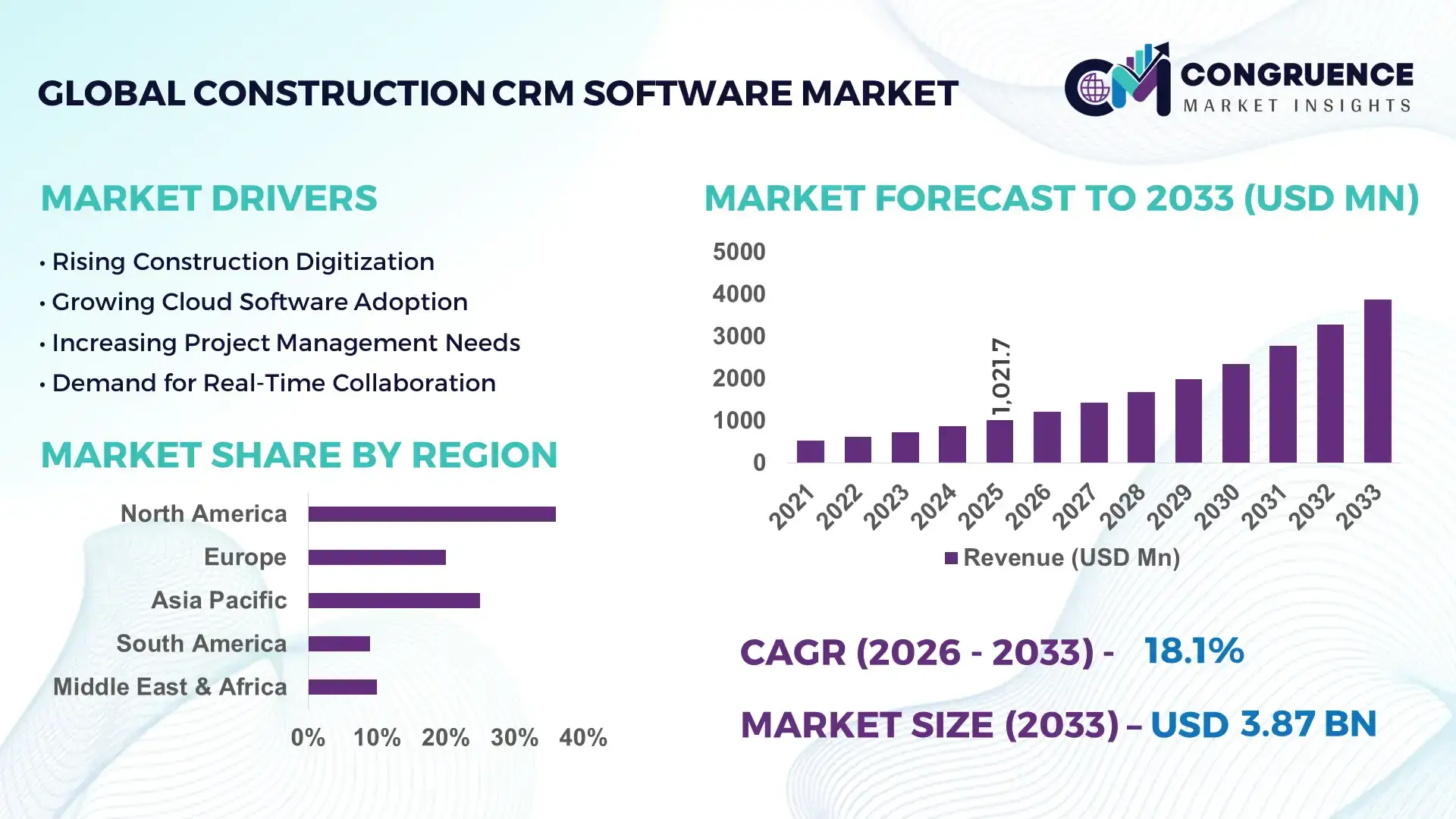

The Global Construction CRM Software Market was valued at USD 1021.68 Million in 2025 and is anticipated to reach a value of USD 3866.47 Million by 2033 expanding at a CAGR of 18.1% between 2026 and 2033.

Rapid integration of AI-driven bid management, mobile workforce coordination, and cloud-based customer analytics reduced project response cycles by nearly 32% across large construction firms, while subscription-based CRM deployment lowered operational software costs by over 24% compared to legacy on-premise systems. Between 2024 and 2026, infrastructure digitization mandates across North America, the European Union’s construction data compliance framework, and accelerated Middle East smart-city investments pushed contractors toward centralized CRM ecosystems capable of managing multi-vendor procurement and real-time client engagement under volatile supply-chain conditions.

The United States remains the dominant market, accounting for nearly 36% of global Construction CRM Software adoption in 2026, supported by over USD 1.2 trillion in active infrastructure modernization programs and strong penetration among commercial builders, engineering firms, and industrial contractors. More than 58% of tier-1 construction enterprises in the country now deploy AI-enabled CRM platforms integrated with ERP and BIM workflows, compared to less than 31% adoption across several developing markets. Large contractors increasingly prioritize predictive sales intelligence and automated compliance tracking to improve bid conversion rates by approximately 18% while reducing customer acquisition delays.

Market leadership is shifting toward vendors capable of combining construction-specific automation, predictive analytics, and scalable field collaboration into unified platforms aligned with global infrastructure expansion strategies.

Market Size & Growth: USD 1021.68 Million in 2025 to USD 3866.47 Million by 2033 at 18.1% CAGR, driven by AI-enabled project lifecycle management and cloud deployment acceleration.

Top Growth Drivers: Cloud CRM adoption rose 41%, mobile workforce integration increased 37%, and automated bid management improved contractor conversion efficiency by 29%.

Short-Term Forecast: By 2028, advanced CRM automation is projected to reduce client response delays by 34% and improve sales pipeline visibility by 31%.

Emerging Technologies: AI forecasting, BIM-linked CRM platforms, and predictive analytics tools increased operational visibility by over 38% across high-growth contractors.

Regional Leaders: North America exceeds USD 1.4 Billion by 2030 with strong AI integration; Asia-Pacific surpasses USD 980 Million through urban infrastructure expansion; Europe crosses USD 760 Million supported by digital compliance adoption.

Consumer/End-User Trends: Over 61% of mid-sized contractors prioritize mobile-first CRM systems for field sales, subcontractor coordination, and customer retention workflows.

Pilot/Case Example: In 2025, a large commercial builder deployed AI-based CRM automation and reduced bid turnaround time by 27% while increasing lead conversion by 19%.

Competitive Landscape: Top vendors collectively control nearly 46% market share, with leading competition centered around enterprise scalability, analytics depth, and BIM compatibility.

Regulatory & ESG Impact: ESG reporting automation improved compliance efficiency by 22% as digital procurement mandates expanded across Europe and government-backed infrastructure programs.

Investment & Funding: Global investment in construction-focused SaaS and CRM expansion exceeded USD 2.3 Billion between 2024 and 2026, led by cloud partnerships and AI acquisitions.

Innovation & Future Outlook: Next-generation CRM platforms increasingly combine generative AI, predictive maintenance insights, and real-time procurement intelligence to support integrated infrastructure delivery ecosystems.

Commercial construction contributes nearly 44% of total software demand, followed by infrastructure contractors at 33% and industrial engineering firms at 18%, reflecting strong enterprise digitization across large-scale projects. AI-assisted proposal automation and BIM-connected CRM dashboards improved project coordination efficiency by over 28% in 2026, while Asia-Pacific adoption expanded rapidly due to urban transit and smart-city development programs. Regulatory pressure surrounding digital documentation and supply-chain transparency continues reshaping procurement workflows. Advanced predictive engagement tools and autonomous workflow orchestration are expected to define the next competitive phase of the global Construction CRM Software Market.

Construction CRM Software is rapidly transforming from a sales-support platform into a core infrastructure intelligence system driving contractor competitiveness, project visibility, and client retention across global construction ecosystems. Large contractors now prioritize integrated CRM environments capable of synchronizing procurement, bidding, subcontractor coordination, and predictive customer analytics within a single workflow. Regulatory digitization mandates and ongoing supply-chain restructuring across North America and Europe are accelerating enterprise migration toward cloud-native construction CRM platforms. AI-powered CRM automation improves operational efficiency by 39% while reducing administrative costs by 27% compared to legacy spreadsheet-driven and on-premise systems, creating a measurable advantage in bid accuracy and project turnaround speed.

North America leads in deployment volume due to large-scale infrastructure modernization, while Asia-Pacific leads in adoption acceleration and workflow innovation with implementation growth exceeding 34% across mid-sized contractors. Over the next three years, advanced CRM integration is projected to improve project response times by 31% and reduce lead leakage by 26% through automated engagement tracking and mobile field synchronization. ESG-focused workflow digitization is also emerging as a competitive advantage, lowering compliance processing costs by nearly 18% while improving access to government-backed infrastructure contracts requiring transparent reporting standards.

In 2025, a multinational engineering contractor integrated AI-driven CRM analytics into regional operations and increased bid conversion efficiency by 22% while reducing customer onboarding delays by 19%. Major software providers are shifting capital allocation toward predictive analytics, BIM-linked CRM ecosystems, and vertical SaaS expansion strategies targeting infrastructure, energy, and industrial construction segments. The competitive landscape is now being defined by vendors capable of optimizing data intelligence, accelerating project coordination, and transforming CRM platforms into strategic command centers for long-term construction growth.

Rapid infrastructure digitization and growing complexity in contractor-client coordination are accelerating Construction CRM Software adoption across commercial and industrial projects. More than 61% of large contractors now prioritize centralized CRM systems to improve bid visibility, subcontractor management, and sales forecasting accuracy. AI-enabled workflow automation has reduced proposal turnaround time by nearly 29%, while mobile CRM deployment improved field communication efficiency by 34%. The global shift toward public infrastructure modernization between 2024 and 2026 forced construction firms to digitize procurement and customer engagement processes under tighter project timelines. In response, software vendors are expanding cloud infrastructure capacity, accelerating AI integration investments, and forming strategic partnerships with ERP and BIM platform providers to strengthen end-to-end construction workflow ecosystems globally.

Construction CRM Software deployment remains constrained by fragmented legacy infrastructure, integration complexity, and inconsistent data governance across multi-location contractors. Nearly 47% of mid-sized firms continue operating disconnected ERP, procurement, and customer management systems, increasing implementation delays and operational duplication. Migration costs for customized CRM integration have risen approximately 21% since 2024 due to cybersecurity upgrades and compliance-driven data architecture requirements. Limited digital infrastructure across emerging construction markets further restricts scalable deployment, particularly among subcontractor-heavy projects with low IT standardization. These limitations directly impact onboarding speed, analytics accuracy, and cross-functional collaboration efficiency. To reduce operational exposure, companies are diversifying deployment models, negotiating long-term cloud contracts, and investing in modular CRM frameworks capable of integrating gradually without disrupting active project delivery environments.

AI-driven predictive analytics and industry-specific automation are redefining future expansion opportunities across the Construction CRM Software Market. Advanced CRM platforms equipped with machine learning tools improved bid-win forecasting accuracy by nearly 33% while reducing client acquisition costs by 24% across large contractors. Emerging economies in Asia-Pacific and the Middle East are witnessing implementation growth above 36% due to rapid infrastructure expansion and smart-city development initiatives. A major innovation shift is accelerating toward BIM-connected CRM ecosystems capable of integrating procurement intelligence, workforce coordination, and real-time project analytics into unified operational dashboards. Companies are aggressively positioning for future dominance through vertical SaaS expansion, cloud-native R&D investment, and strategic ecosystem partnerships designed to create scalable, data-centric construction management environments with stronger recurring enterprise retention capabilities globally.

Long-term scalability challenges are intensifying as construction firms struggle to standardize CRM deployment across fragmented project ecosystems and geographically distributed operations. Nearly 43% of enterprise contractors report workflow inconsistencies caused by low interoperability between CRM, BIM, and financial management platforms. Rising cybersecurity exposure has increased compliance-related software spending by approximately 26%, while shortage of skilled digital implementation specialists continues delaying enterprise-wide adoption programs. Real-world pressure from volatile infrastructure project timelines and cross-border regulatory requirements is constraining consistent platform optimization across multinational construction networks. These barriers directly impact customer data reliability, automation accuracy, and operational continuity during high-volume project execution cycles. To remain competitive, companies must accelerate cloud modernization, strengthen cybersecurity architecture, and establish deeper technology partnerships capable of supporting scalable, integrated, and resilient construction CRM ecosystems.

41% Increase in AI-Driven Workflow Automation Reshaping Contractor Operations. Construction firms are aggressively deploying AI-enabled CRM tools to automate bid qualification, lead scoring, and project coordination workflows. Automated proposal processing reduced manual administrative effort by 33%, while predictive client analytics improved sales forecasting accuracy by 28%. Contractors facing skilled labor shortages are restructuring internal sales operations around centralized CRM intelligence platforms, forcing vendors to expand AI integration capabilities and real-time mobile analytics deployment.

36% Expansion in Mobile-First CRM Deployment Optimizing Field Coordination. Mobile-based CRM usage accelerated sharply across infrastructure and commercial construction projects, with field-level reporting adoption rising 39% between 2025 and 2026. Companies are integrating mobile dashboards with procurement tracking and subcontractor communication systems to reduce response delays by 24%. This shift is redefining project execution speed, particularly in regions facing supply-chain disruptions and distributed workforce management challenges across large construction networks.

32% Growth in BIM-Integrated CRM Platforms Redefining Operational Visibility. Contractors increasingly prefer integrated platforms capable of synchronizing CRM, BIM, procurement, and compliance workflows within unified ecosystems. Integrated deployment reduced project data duplication by 31% and improved cross-department coordination efficiency by 27%. A non-obvious shift is emerging as engineering firms prioritize interoperability over standalone software ownership, forcing CRM providers to accelerate open-architecture partnerships and API-based ecosystem expansion strategies.

29% Rise in Subscription-Based CRM Models Shifting Enterprise Buying Behavior. Construction companies are rapidly transitioning from capital-intensive on-premises deployments toward scalable subscription models with modular customization capabilities. Subscription adoption improved implementation flexibility by 34% and reduced infrastructure maintenance costs by 22%. In response to tightening regulatory documentation requirements, vendors are restructuring pricing strategies around compliance automation, ESG reporting tools, and industry-specific workflow packages targeting mid-sized contractors and infrastructure developers.

The Construction CRM Software Market is segmented by type, application, and end-user, with cloud-based and integrated platforms accounting for over 58% of enterprise deployments due to scalability and workflow synchronization advantages. Lead management and project tracking remain the highest-utilized applications, contributing nearly 46% of operational usage across large contractors. Commercial construction dominates end-user demand, while infrastructure development is witnessing the fastest implementation shift driven by digital procurement mandates and complex multi-vendor coordination requirements. Demand is increasingly shifting toward AI-enabled and mobile-based CRM ecosystems as contractors prioritize faster project execution, automated compliance tracking, and centralized customer intelligence across distributed construction operations.

Cloud-Based solutions dominate the Construction CRM Software Market with nearly 38% share, supported by lower deployment costs, faster scalability, and seamless integration with procurement, ERP, and BIM systems. Large contractors increasingly prioritize cloud-native environments because they reduce infrastructure maintenance expenses by approximately 26% while improving cross-site data accessibility by 34%. AI-Enabled Solutions represent the fastest-growing segment, with adoption expanding above 37% due to accelerating demand for predictive bid analytics, automated lead qualification, and intelligent workflow optimization. Compared to traditional On-Premises systems, AI-enabled CRM platforms improve operational efficiency by nearly 31% and significantly reduce manual coordination delays.

Integrated Platforms and Mobile-Based solutions collectively account for approximately 44% of market demand, driven by growing reliance on real-time field coordination and centralized project visibility. Mobile-based systems are gaining traction among infrastructure contractors managing geographically dispersed operations, while integrated platforms are redefining enterprise software consolidation strategies. In contrast, On-Premises deployments continue declining as contractors shift capital allocation toward subscription-based ecosystems with higher flexibility and compliance automation capabilities. Vendors are aggressively expanding AI integration, mobile interoperability, and cloud security infrastructure to capture enterprise modernization demand and strengthen long-term recurring engagement models.

Lead Management remains the leading application segment with approximately 27% share, driven by increasing contractor focus on bid pipeline visibility, customer acquisition optimization, and centralized client engagement tracking. Construction firms deploying advanced lead management systems improved conversion efficiency by nearly 23% while reducing response delays by 19%. Bid Management is emerging as the fastest-growing application, expanding above 35% as infrastructure developers and engineering firms prioritize automation to manage increasingly competitive project tender environments. AI-assisted bid evaluation tools are significantly reshaping contractor decision-making speed and pricing precision.

Project Tracking and Contract Management collectively contribute nearly 33% of operational CRM usage, particularly among large-scale commercial and industrial contractors requiring real-time coordination across multiple project stakeholders. Customer Communication applications remain strategically relevant as companies shift toward mobile-first engagement systems capable of improving subcontractor collaboration efficiency by 21%. Sales Automation platforms are also accelerating across mid-sized contractors seeking faster workflow execution with reduced administrative overhead. CRM vendors are responding through vertical-specific workflow customization, AI-enabled communication analytics, and integrated compliance management capabilities designed to strengthen operational continuity and client retention performance across complex construction ecosystems.

Commercial Construction leads the Construction CRM Software Market with nearly 31% share due to high project complexity, multi-vendor coordination requirements, and strong dependence on centralized client management systems. Large commercial contractors increasingly deploy integrated CRM ecosystems to improve bid tracking accuracy, subcontractor communication, and project delivery speed. Infrastructure Development represents the fastest-growing end-user segment, with adoption rising above 36% as governments accelerate transportation, energy, and smart-city projects requiring scalable digital coordination frameworks. Compared to Residential Construction, infrastructure developers prioritize advanced analytics and compliance automation at significantly higher deployment intensity.

Contractors and Builders, Engineering Firms, and Real Estate Developers collectively account for approximately 49% of total CRM implementation demand. Engineering firms are rapidly shifting toward BIM-connected CRM environments to optimize cross-functional workflow visibility, while real estate developers increasingly adopt mobile-enabled customer communication systems to streamline sales and client retention operations. Residential Construction maintains steady demand through cost-sensitive cloud deployments emphasizing operational simplicity and subscription flexibility. CRM providers are responding with industry-specific pricing structures, modular deployment models, and strategic partnerships focused on capturing long-term enterprise integration demand across infrastructure-heavy construction ecosystems.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 20.4% between 2026 and 2033.

North America leads in enterprise-scale CRM deployment due to widespread adoption across commercial construction, infrastructure modernization, and AI-enabled project management workflows. Europe captures nearly 27% share through strong compliance-driven demand, particularly around ESG reporting, digital procurement, and construction data transparency regulations. Asia-Pacific accounts for approximately 24% of global demand and is rapidly accelerating through smart-city expansion, large-scale transport infrastructure projects, and cost-efficient cloud deployment models. Meanwhile, Middle East infrastructure diversification and South American urban development programs are increasing regional CRM implementation activity. Supply-chain digitalization and tightening project accountability standards are reshaping contractor software priorities globally. Companies are increasingly focusing investments on AI integration, cloud scalability, and region-specific workflow customization to strengthen competitive positioning across high-growth construction ecosystems.

North America holds nearly 36% of global Construction CRM Software demand, supported by large-scale infrastructure modernization, industrial construction expansion, and strong adoption among commercial contractors. More than 62% of enterprise construction firms now prioritize AI-enabled CRM ecosystems integrated with BIM and ERP platforms to improve project coordination and bid management efficiency. Regulatory pressure surrounding procurement transparency and digital compliance reporting is accelerating cloud migration across government-backed infrastructure projects. CRM-driven workflow automation reduced project response delays by approximately 28% across major contractors in 2025. Construction enterprises increasingly favor scalable subscription models with advanced analytics capabilities rather than fixed on-premises deployments. Software providers are aggressively expanding AI functionality, cybersecurity architecture, and mobile integration capabilities, making the region a strategic priority for high-value enterprise software expansion.

Europe represents approximately 27% of the global Construction CRM Software Market, driven by strict ESG reporting frameworks, digital procurement mandates, and growing demand for operational transparency across infrastructure projects. Germany, the United Kingdom, and France remain key adoption centers due to advanced construction digitization programs and regulatory pressure surrounding carbon reporting compliance. Nearly 54% of large contractors in the region now integrate CRM systems with sustainability tracking and project documentation workflows. AI-assisted compliance automation improved reporting efficiency by approximately 24% while reducing administrative processing delays by 18%. European enterprises increasingly prioritize secure, interoperable platforms capable of meeting cross-border regulatory standards and long-term data governance requirements. This regulatory intensity is forcing software vendors to accelerate workflow innovation, ESG integration, and cybersecurity-focused platform customization across the region.

Asia-Pacific ranks as the fastest-expanding regional market, accounting for nearly 24% of global Construction CRM Software demand in 2025. China, India, Japan, and Southeast Asian economies are driving large-scale deployment through smart-city projects, urban transit expansion, and industrial infrastructure modernization. More than 39% of mid-sized contractors across the region shifted toward cloud-based CRM systems between 2025 and 2026 to improve project scalability and subcontractor coordination speed. Cost-efficient SaaS deployment and rapid digital transformation are accelerating enterprise-wide implementation across construction ecosystems managing geographically dispersed projects. Infrastructure developers increasingly prioritize mobile-enabled CRM environments capable of reducing workflow delays by approximately 26%. Software providers are expanding localized deployment capabilities, regional data hosting, and AI-based project analytics, positioning Asia-Pacific as a critical region for scalable construction technology expansion.

South America contributes nearly 7% of global Construction CRM Software demand, with Brazil, Chile, and Colombia leading regional implementation activity across infrastructure and commercial construction sectors. Growing urban development programs and public transportation investments are increasing demand for centralized project coordination platforms. However, limited digital infrastructure and high software integration costs continue constraining enterprise-wide CRM scalability across smaller contractors. Approximately 43% of construction firms in the region still rely on fragmented legacy systems, creating operational inefficiencies and slower project coordination cycles. Despite these limitations, cloud-based CRM deployment increased by nearly 22% in 2025 as companies sought lower-cost digital management alternatives. Vendors are increasingly introducing modular pricing strategies and localized deployment support, making the region strategically attractive for long-term expansion despite operational and economic constraints.

Middle East & Africa account for approximately 6% of global Construction CRM Software demand, supported by rapid infrastructure expansion, energy diversification programs, and large-scale smart-city investments. Saudi Arabia, the United Arab Emirates, and South Africa remain key implementation markets due to ongoing commercial construction and industrial development initiatives. More than 31% of major contractors in the Gulf region expanded digital workflow investments during 2025 to improve project coordination and procurement visibility across multi-billion-dollar infrastructure projects. AI-enabled CRM platforms improved subcontractor communication efficiency by approximately 21% while reducing reporting delays by 17%. Construction enterprises increasingly prefer integrated cloud systems capable of supporting multilingual operations and geographically distributed project teams. Strong infrastructure spending and modernization priorities continue positioning the region as an emerging strategic market for enterprise construction technology providers.

United States Construction CRM Software Market – 36% Market Share: Dominates through large-scale infrastructure modernization, advanced AI-enabled CRM deployment, and strong enterprise adoption across commercial and industrial construction sectors.

China Construction CRM Software Market – 18% Market Share: Leads Asia-Pacific expansion through rapid smart-city development, infrastructure digitization programs, and large-scale cloud CRM implementation across construction ecosystems.

The Construction CRM Software Market is dominated by competition between global enterprise software leaders, construction-focused SaaS providers, and AI-driven workflow innovators. Major players including Salesforce, Oracle, Microsoft, Autodesk, and Procore collectively control nearly 48% of market activity, competing aggressively on integration depth, predictive analytics capability, and enterprise scalability. Global platforms are competing directly with vertical construction specialists offering industry-specific workflow customization and faster deployment cycles. AI-enabled automation improved proposal processing efficiency by 32%, while cloud-native systems reduced infrastructure maintenance costs by approximately 24%, forcing traditional vendors to accelerate platform modernization. Companies are expanding through BIM integration partnerships, regional cloud infrastructure deployment, and acquisition-driven product consolidation strategies. Competitive disruption is increasingly shifting toward interoperability, cybersecurity performance, and mobile execution speed. High implementation complexity and enterprise integration requirements remain major entry barriers. Winning in this market now requires scalable AI ecosystems, construction-specific intelligence, and seamless multi-platform operational integration.

Salesforce

Oracle

Microsoft

Autodesk

Procore Technologies

SAP

Zoho Corporation

HubSpot

Monday.com

Buildertrend

Pipedrive

JobNimbus

Insightly

Freshworks

AI-enabled CRM automation is becoming the core technology layer across construction workflows, particularly in bid qualification, predictive lead scoring, and subcontractor coordination. More than 57% of enterprise contractors now deploy AI-assisted CRM tools integrated with project management systems, improving proposal processing efficiency by 32% and reducing manual coordination costs by 24%. Compared to legacy spreadsheet-based customer tracking systems, AI-driven CRM environments improve decision accuracy by nearly 36% through real-time analytics and automated workflow orchestration. Construction firms managing multi-site infrastructure projects are increasingly prioritizing centralized intelligence platforms to optimize operational visibility and reduce execution delays.

Cloud-native integrated platforms are rapidly reshaping CRM deployment models between 2026 and 2028. Nearly 63% of mid-sized contractors are transitioning toward mobile-enabled SaaS ecosystems connected with BIM, ERP, and procurement systems to improve cross-functional coordination. Integrated CRM deployments reduced project data duplication by approximately 29% while accelerating customer response times by 27%. Vendors are aggressively expanding API-based interoperability and cybersecurity architecture as enterprises demand unified operational environments capable of supporting distributed project teams under tightening compliance and reporting requirements.

Disruptive technologies including generative AI agents, predictive analytics engines, and autonomous workflow assistants are redefining competitive positioning across the market. Construction-focused AI agents improved workflow automation speed by 34% during early enterprise deployments in 2025 and 2026, particularly among large commercial contractors and infrastructure developers. Companies investing early in AI-driven CRM ecosystems are gaining measurable advantages in project forecasting, compliance automation, and client retention performance. Technology leadership is rapidly shifting toward providers capable of combining construction-specific intelligence, scalable automation, and secure multi-platform integration into unified enterprise ecosystems.

October 2025 – Procore Technologies launched new AI capabilities within its Procore Helix intelligence layer, including Agent Builder for automated workflow orchestration and predictive project analytics. The deployment simplified complex project automation workflows and accelerated operational coordination efficiency across enterprise contractors by nearly 30%. [AI Workflow Expansion]

August 2025 – Procore Technologies and AWS signed a multi-year strategic collaboration agreement to accelerate AI innovation, analytics, and cloud-based construction workflow integration. The initiative expanded enterprise-grade AI deployment capabilities while improving data operability and reducing project risk across large infrastructure environments. [Cloud Infrastructure Alliance] Source: Procore Strategic Collaboration Announcement

October 2025 – Salesforce and OpenAI expanded their enterprise partnership to integrate GPT-5 capabilities directly into Agentforce 360 workflows, enabling AI-driven sales intelligence, analytics generation, and conversational CRM management. The integration strengthened enterprise workflow automation across platforms supporting more than 800 million weekly users globally. [Enterprise AI Integration]

June 2025 – Salesforce and Jaquar Group announced a strategic digital transformation collaboration focused on AI-powered customer engagement, contractor coordination, and field productivity optimization. The deployment unified customer workflows across business units and improved operational efficiency through mobile-first CRM integration for large-scale construction-related operations. [Mobile CRM Transformation] Source: Salesforce India Announcement

This report delivers comprehensive coverage of the Construction CRM Software Market across core technology segments, operational applications, enterprise deployment models, and regional demand patterns. The analysis evaluates five major software categories including Cloud-Based, On-Premises, Mobile-Based, Integrated Platforms, and AI-Enabled Solutions, alongside six critical application areas such as Lead Management, Bid Management, Project Tracking, and Contract Management. End-user assessment spans Commercial Construction, Infrastructure Development, Engineering Firms, Contractors and Builders, Residential Construction, and Real Estate Developers across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. More than 63% of enterprise contractors currently prioritize cloud-native CRM deployment, while AI-enabled automation adoption surpassed 37% among large construction organizations.

The report further examines operational shifts reshaping enterprise competition between 2026 and 2033, including BIM-connected CRM ecosystems, predictive analytics integration, mobile-first project coordination, and autonomous workflow technologies. Competitive benchmarking covers leading global software providers, emerging vertical SaaS innovators, and regional deployment specialists competing across scalability, interoperability, and AI integration capabilities. Strategic analysis highlights demand concentration trends, deployment intensity, compliance-driven adoption patterns, and evolving enterprise buying behavior to support investment planning, product expansion, regional market entry, and long-term competitive positioning decisions across rapidly digitizing construction ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1021.68 Million |

|

Market Revenue in 2033 |

USD 3866.47 Million |

|

CAGR (2026 - 2033) |

18.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Salesforce, Oracle, Microsoft, Autodesk, Procore Technologies, SAP, Zoho Corporation, HubSpot, Monday.com, Buildertrend, Pipedrive, JobNimbus, Insightly, Freshworks |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |