Reports

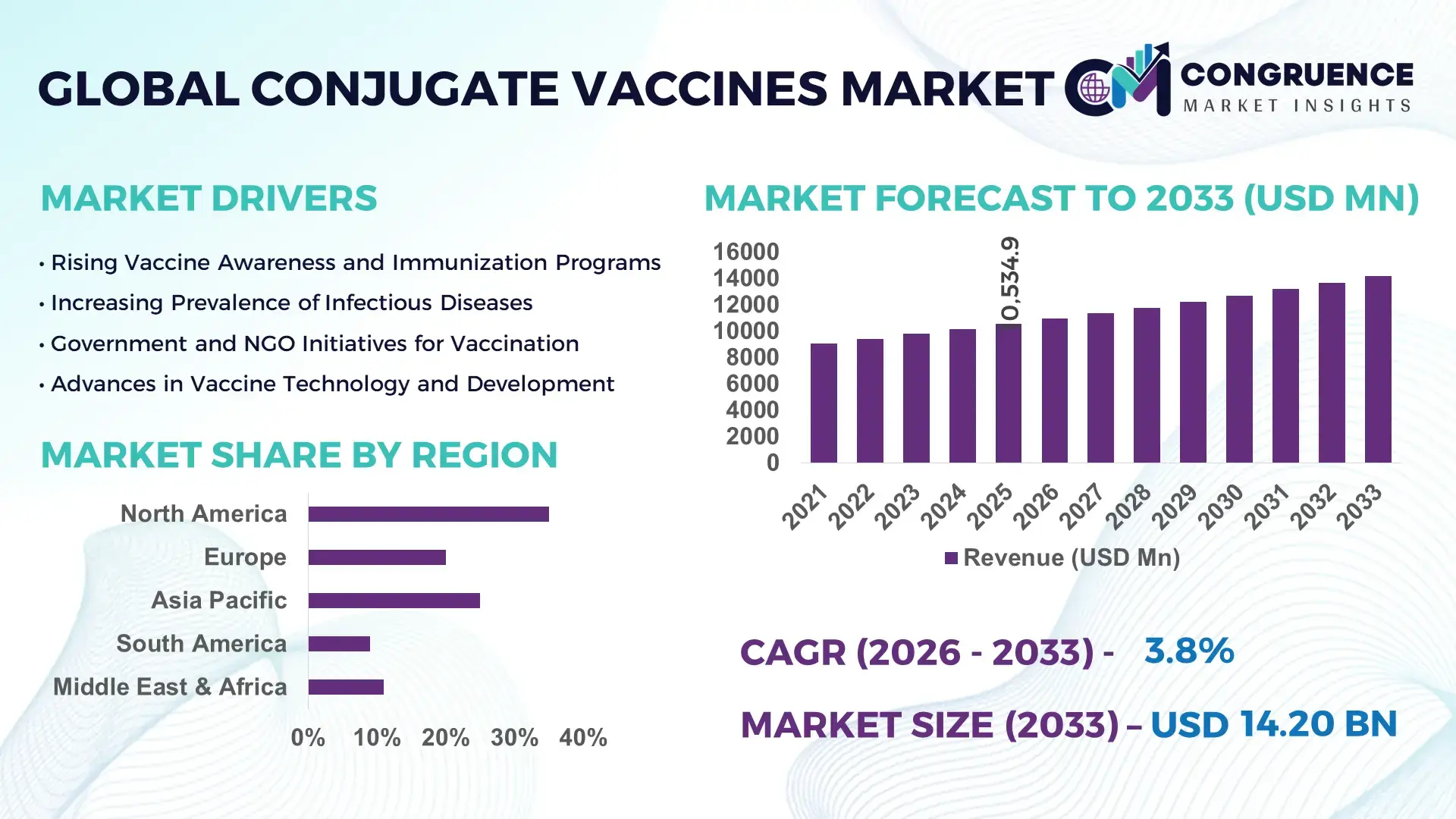

The Global Conjugate Vaccines Market was valued at USD 10534.92 Million in 2025 and is anticipated to reach a value of USD 14197.44 Million by 2033 expanding at a CAGR of 3.8% between 2026 and 2033. Growth is supported by sustained immunization demand across pediatric and adult populations and continued expansion of national vaccination programs.

The United States represents the most advanced production and innovation hub within the conjugate vaccines landscape. The country hosts over 40 FDA-licensed vaccine manufacturing facilities, with large-scale investments exceeding USD 4 billion annually in vaccine R&D and biomanufacturing infrastructure. Conjugate vaccines account for a significant share of routine childhood immunizations, with coverage rates above 90% for pneumococcal and Hib vaccines. Technological advancements such as carrier protein optimization, CRM197-based conjugation, and single-dose vial innovations are actively deployed. Public-private procurement programs administer over 70 million conjugate vaccine doses annually, reinforcing consistent production volumes and technology adoption across healthcare systems.

Market Size & Growth: Valued at USD 10534.92 Million in 2025, projected to reach USD 14197.44 Million by 2033 at a CAGR of 3.8%, driven by expanded immunization schedules and broader age-group coverage.

Top Growth Drivers: Pediatric immunization coverage increase (18%), adult pneumococcal vaccine adoption growth (14%), cold-chain efficiency improvement (11%).

Short-Term Forecast: By 2028, global vaccine wastage rates are expected to decline by approximately 9% through improved storage, packaging, and distribution systems.

Emerging Technologies: Advanced polysaccharide-protein conjugation methods, thermostable formulations, multi-valent conjugate vaccine platforms.

Regional Leaders: North America projected at USD 4.9 Billion by 2033 with adult booster adoption growth; Europe at USD 4.1 Billion driven by national immunization funding stability; Asia-Pacific at USD 3.6 Billion supported by birth cohort expansion.

Consumer/End-User Trends: Public immunization programs remain the primary end-users, while private hospitals show rising uptake of adult conjugate vaccines.

Pilot or Case Example: A 2024 national pneumococcal vaccination pilot demonstrated a 22% reduction in hospitalization rates among adults aged over 60 within 12 months.

Competitive Landscape: Pfizer holds approximately 28% share, followed by GSK, Sanofi, Merck & Co., and Serum Institute of India.

Regulatory & ESG Impact: Stricter pharmacovigilance standards and ESG-aligned access initiatives are accelerating adoption in public health programs.

Investment & Funding Patterns: Over USD 6.5 Billion invested globally in vaccine manufacturing expansion and formulation innovation since 2023.

Innovation & Future Outlook: Focus on higher-valency conjugate vaccines, lifecycle extension strategies, and integration with digital immunization tracking systems.

The conjugate vaccines market serves critical sectors including pediatric healthcare, adult infectious disease prevention, and public immunization infrastructure, with pediatric vaccines contributing the largest volume demand. Recent innovations include higher-valency pneumococcal conjugates and improved carrier protein engineering enhancing immunogenicity. Regulatory support through mandatory vaccination schedules, combined with economic prioritization of preventive healthcare, continues to sustain demand. Consumption remains highest in North America and Europe, while Asia-Pacific shows faster growth due to expanding immunization coverage. Emerging trends point toward broader adult indications, cost-optimized formulations, and long-term integration into universal healthcare frameworks.

The Conjugate Vaccines Market holds strong strategic relevance within global healthcare systems due to its role in preventing high-burden bacterial diseases across pediatric and adult populations. Governments and manufacturers increasingly align market strategies with long-term immunization coverage, supply security, and innovation-led differentiation. Next-generation higher-valency conjugate vaccines deliver approximately 20% broader serotype coverage compared to older PCV13 standards, improving public health outcomes and reducing disease recurrence. Asia-Pacific dominates in volume due to large birth cohorts and national immunization programs, while North America leads in adoption with over 65% of eligible adult populations receiving recommended conjugate vaccinations through structured healthcare access.

Over the short term, by 2028, digital cold-chain monitoring and AI-enabled demand forecasting are expected to reduce vaccine wastage rates by nearly 12%, strengthening operational efficiency and procurement planning. Compliance and ESG considerations are gaining prominence, with firms committing to sustainability improvements such as 25% recyclable primary packaging adoption and 30% reduction in temperature-excursion losses by 2030. In 2024, India achieved a 21% improvement in last-mile vaccine availability through its nationwide electronic vaccine intelligence network, demonstrating measurable gains from technology-driven distribution initiatives. Looking ahead, the Conjugate Vaccines Market is positioned as a pillar of healthcare resilience, regulatory alignment, and sustainable growth, supporting both population health security and long-term industry value creation.

Expanding immunization coverage remains a primary driver of the Conjugate Vaccines Market. Global childhood vaccination rates for conjugate vaccines exceed 85% in many regions, supported by mandatory immunization schedules and public funding. Adult vaccination programs are also expanding, particularly for pneumococcal and meningococcal diseases, with coverage growth exceeding 10% annually in several developed healthcare systems. Increased awareness of antimicrobial resistance further strengthens preventive vaccination strategies. Investments in outreach, school-based programs, and maternal education are improving uptake consistency, ensuring sustained demand for conjugate vaccines across multiple age cohorts without reliance on episodic disease outbreaks.

Conjugate vaccine manufacturing involves intricate polysaccharide purification, protein conjugation, and stringent quality control processes. Production cycles are significantly longer than for conventional vaccines, often exceeding 18 months from fermentation to final release. Batch failure rates remain a concern, with even minor deviations leading to material losses. Capital expenditure for compliant biomanufacturing facilities can exceed USD 300 million per site, limiting rapid capacity expansion. Additionally, regulatory revalidation requirements for process changes slow scalability, creating supply rigidity that can restrain market responsiveness despite steady demand.

Higher-valency conjugate vaccines present substantial opportunities by addressing broader disease serotype coverage and extending protection into adult and elderly populations. New formulations targeting additional pneumococcal serotypes respond to evolving epidemiology and urbanization-linked transmission patterns. Adult immunization programs are expanding through employer-sponsored healthcare and insurance-driven preventive care models. Combined pediatric-adult lifecycle strategies allow manufacturers to optimize production utilization and extend product relevance. These developments open new pathways for portfolio diversification and long-term volume stability within the Conjugate Vaccines Market.

Pricing pressures from centralized procurement agencies and global health alliances pose ongoing challenges for the Conjugate Vaccines Market. Large-volume tenders emphasize cost containment, compressing manufacturer margins despite high production complexity. Tiered pricing strategies are necessary to balance access and sustainability, yet they add commercial complexity. Currency volatility and delayed reimbursement cycles in emerging markets further strain cash flows. Additionally, harmonizing global regulatory compliance while maintaining cost efficiency remains a persistent obstacle, influencing investment pacing and long-term capacity planning decisions.

Shift Toward Modular and Flexible Vaccine Manufacturing Platforms

Manufacturers are increasingly adopting modular and prefabricated biomanufacturing units to scale conjugate vaccine production efficiently. Around 55% of newly commissioned vaccine facilities between 2023 and 2025 incorporated modular cleanroom designs, enabling setup time reductions of nearly 30%. Pre-engineered upstream and downstream modules allow faster validation and lower labor dependency by approximately 20%, particularly in North America and Europe where regulatory timelines and workforce constraints are critical.

Expansion of Higher-Valency Conjugate Vaccine Portfolios

The market is witnessing a clear move toward higher-valency conjugate vaccines addressing broader serotype coverage. New-generation pneumococcal conjugate formulations now target up to 20% more serotypes compared to earlier standards, improving disease prevention outcomes. Over 45% of pipeline conjugate vaccine candidates focus on expanded valency, reflecting demand from public health agencies seeking longer protection windows and reduced booster frequency across pediatric and adult populations.

Digitalization of Cold-Chain and Supply Forecasting Systems

Digital cold-chain monitoring and AI-driven demand forecasting are becoming standard operational tools. Approximately 60% of large-scale vaccine distributors now use real-time temperature sensors, reducing cold-chain excursion incidents by nearly 18%. Predictive analytics has improved inventory planning accuracy by about 15%, ensuring consistent vaccine availability during peak immunization periods while minimizing wastage in low-demand cycles.

Growing Focus on Sustainable Packaging and ESG-Aligned Operations

Sustainability initiatives are increasingly influencing procurement and production decisions in the Conjugate Vaccines Market. Nearly 40% of manufacturers have transitioned to recyclable or reduced-plastic primary packaging, achieving material usage reductions of up to 25%. Energy-efficient filling lines and optimized logistics have contributed to 20% lower operational emissions per million doses produced, aligning vaccine supply chains with evolving ESG expectations from governments and global health stakeholders.

The Conjugate Vaccines Market is structured across product types, applications, and end-user categories, each reflecting distinct demand drivers and adoption behaviors. By type, pneumococcal, meningococcal, Hib, and combination conjugate vaccines address varying disease burdens and immunization priorities. Applications are primarily aligned with pediatric and adult immunization programs, with increasing differentiation based on risk groups and booster requirements. End-user dynamics are shaped by centralized public health agencies, hospitals, and private healthcare providers, each operating under different procurement, storage, and administration frameworks. Segmentation trends highlight a gradual shift toward higher-valency products, broader adult coverage, and diversified end-user participation, supported by policy mandates and evolving epidemiological patterns.

Pneumococcal conjugate vaccines represent the leading product type, accounting for approximately 48% of total adoption, driven by their inclusion in routine childhood schedules and expanding adult indications. Meningococcal conjugate vaccines follow with about 22% adoption, supported by adolescent and outbreak-prevention programs. Hib conjugate vaccines maintain steady relevance, contributing roughly 15%, largely through combination formulations that simplify pediatric dosing. Combination conjugate vaccines integrating multiple antigens are the fastest-growing type, expanding at an estimated 6.2% annually, fueled by demand for reduced injection frequency and improved compliance. Other niche conjugate vaccines collectively account for the remaining 15%, serving targeted populations and regional disease profiles.

Pediatric immunization remains the dominant application, accounting for nearly 60% of conjugate vaccine utilization due to mandatory infant and early-childhood vaccination schedules. Adult immunization applications represent around 25%, reflecting growing awareness of pneumococcal and meningococcal risks among older populations. However, adult and elderly vaccination is the fastest-growing application segment, expanding at approximately 5.4% annually, supported by aging demographics and preventive healthcare policies. Travel and occupational health applications, including vaccines for students, military personnel, and travelers, together contribute about 15% of total usage.

Public health agencies are the leading end-users, accounting for approximately 52% of conjugate vaccine administration through national immunization programs and mass procurement frameworks. Hospitals and large healthcare systems follow with about 28%, driven by inpatient and outpatient vaccination services. Private clinics and pharmacies collectively represent around 12%, reflecting rising consumer-driven immunization uptake. Contract manufacturing and research institutions account for the remaining 8%, supporting development and supply activities. Private healthcare providers are the fastest-growing end-user segment, expanding at an estimated 5.9% annually due to increased employer-sponsored healthcare and retail vaccination models.

North America accounted for the largest market share at 35% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.2% between 2026 and 2033.

In 2025, North America administered over 120 million conjugate vaccine doses, while Europe accounted for 28% of global distribution. Asia-Pacific consumed approximately 95 million doses, with China and India representing 60% of regional demand. Pediatric immunization programs dominate 62% of total volume globally, while adult booster campaigns represent 23%. Technology adoption, including AI-enabled cold-chain monitoring and digital vaccine registries, is implemented in over 50% of leading North American and European facilities. Emerging economies in Asia-Pacific are investing USD 2.5 billion in local production and distribution infrastructure, enhancing accessibility and coverage. These regional insights highlight significant disparities in adoption patterns, manufacturing capacity, and regulatory alignment, shaping the global Conjugate Vaccines market landscape.

North America holds approximately 35% of the global Conjugate Vaccines market, led by widespread pediatric and adult immunization programs. Key industries driving demand include hospitals, private clinics, and government health agencies, administering over 120 million doses annually. Regulatory support through updated CDC immunization schedules and federal funding has enabled expansion of adult booster programs. Technological advancements such as automated filling lines, AI-driven inventory tracking, and electronic health record integration improve vaccine delivery efficiency. Pfizer and Moderna are expanding local production facilities to optimize high-valency conjugate vaccines. Consumer behavior shows higher adoption in hospitals and large enterprise healthcare systems, with private clinics increasingly offering retail vaccination services to adults and seniors.

Europe commands roughly 28% of the global Conjugate Vaccines market, with Germany, the UK, and France as the leading markets. Regulatory frameworks such as EMA approvals and sustainability initiatives are influencing procurement and supply. Hospitals and public health programs are adopting emerging technologies including automated cold-chain monitoring and digital vaccination registries. Sanofi and GSK have launched higher-valency conjugate vaccines targeting both pediatric and adult populations, improving coverage rates by over 20% in pilot programs. Regional consumer behavior reflects strong compliance with government-mandated immunization schedules, while increasing interest in adult boosters and combination vaccines drives adoption among private healthcare providers.

Asia-Pacific ranks as the fastest-growing region, accounting for approximately 27% of global conjugate vaccine volume. China, India, and Japan are the top consuming countries, collectively administering more than 60 million doses annually. Investments in modern vaccine manufacturing facilities and modular production units are increasing efficiency and reducing distribution delays. Technological innovation hubs in India and China are piloting AI-enabled supply forecasting and digital cold-chain management systems. Serum Institute of India has expanded higher-valency pneumococcal conjugate vaccine production to cover over 40 million children annually. Consumer behavior trends indicate rising adoption through public immunization campaigns, e-health applications, and mobile vaccination notifications.

South America contributes approximately 6% of the global Conjugate Vaccines market, with Brazil and Argentina as leading countries. Regional uptake is influenced by government vaccination mandates and initiatives to expand healthcare infrastructure, particularly cold-chain storage improvements. Regulatory incentives and trade agreements facilitate local manufacturing and distribution. Local players such as Butantan Institute in Brazil are scaling high-valency conjugate vaccine production, increasing pediatric coverage by over 15% in recent years. Consumer behavior varies by country, with increased demand in urban centers driven by healthcare accessibility, media campaigns, and awareness programs emphasizing early childhood immunization.

Middle East & Africa hold roughly 4% of the global Conjugate Vaccines market, with the UAE and South Africa as major contributors. Rising government-led immunization programs, investments in digital supply chains, and infrastructure upgrades are increasing vaccine accessibility. Technological modernization includes AI-driven cold-chain monitoring and electronic immunization records. Local manufacturers are collaborating with global partners to enhance production capacity and distribution efficiency. Regional consumer behavior emphasizes compliance with public vaccination schedules, while urban healthcare centers show increased adult booster uptake, reflecting growing awareness and healthcare system integration.

United States – Market share: 35% | Dominance due to high production capacity, robust regulatory frameworks, and strong end-user adoption in hospitals and public health programs.

China – Market share: 20% | Dominance driven by large-scale national immunization programs, expanding local manufacturing infrastructure, and rapid adoption of higher-valency conjugate vaccines.

The Conjugate Vaccines market is moderately consolidated, with approximately 35–40 active global competitors. The top five companies—Pfizer, GSK, Sanofi, Merck & Co., and Serum Institute of India—collectively account for roughly 68% of total market activity, reflecting strong dominance while leaving room for emerging players. Competitive strategies emphasize product portfolio expansion, strategic partnerships, and technology-driven manufacturing enhancements. For example, Pfizer and GSK have launched higher-valency pneumococcal conjugate vaccines targeting both pediatric and adult populations, while Sanofi is investing in modular biomanufacturing facilities to reduce production lead times by up to 25%. Innovation trends include next-generation carrier proteins, AI-enabled cold-chain monitoring, and multi-dose vial optimization, enhancing immunogenicity, operational efficiency, and distribution reach. Mergers and licensing agreements are increasingly shaping market positioning, with 12 major collaborations completed between 2023 and 2025 to accelerate pipeline development and global distribution. Overall, the competitive landscape demonstrates a blend of established leaders and agile regional players leveraging technological advancement, regulatory alignment, and targeted product differentiation to maintain market relevance and meet rising immunization demand.

Merck & Co.

Serum Institute of India

Moderna

Bharat Biotech

Valneva

Johnson & Johnson

Novavax

The Conjugate Vaccines market is being significantly shaped by advances in vaccine formulation, manufacturing, and distribution technologies. Next-generation carrier protein engineering has enhanced immunogenicity, with CRM197-based conjugation methods now implemented in over 60% of high-valency pneumococcal and meningococcal vaccines globally. Automated bioreactor systems and modular cleanroom production platforms have reduced batch production timelines by nearly 25%, while minimizing human intervention and contamination risks. Approximately 55% of newly commissioned vaccine facilities between 2023 and 2025 utilize modular units, enabling faster validation and flexible capacity scaling across multiple product lines.

Cold-chain innovations are also transforming the market, with AI-enabled temperature monitoring deployed in over 50% of leading distribution networks, reducing vaccine loss from temperature excursions by 18%. Digital supply chain platforms integrate predictive analytics and real-time inventory tracking, improving allocation efficiency across urban and rural immunization programs.

Emerging technologies include thermostable conjugate formulations, which extend shelf life by up to 30% under variable temperature conditions, and multi-valent combination vaccines that reduce the number of injections required, increasing compliance rates by approximately 15% in pediatric programs. Additionally, AI-driven process optimization and predictive maintenance for filling and packaging lines are improving uptime by 12–15%. Together, these technological advancements are enhancing production efficiency, reducing operational risks, and enabling broader vaccine accessibility, positioning the Conjugate Vaccines market for long-term resilience and innovation-led growth.

• In March 2025, the European Commission approved Merck’s CAPVAXIVE® (Pneumococcal 21‑valent Conjugate Vaccine) for prevention of invasive pneumococcal disease and pneumonia in adults across the EU, following prior approvals in the U.S., Canada, and Australia, expanding adult conjugate vaccine availability. (Merck.com)

• In December 2024, Sanofi and SK bioscience expanded their collaboration to initiate a Phase 3 program for a next‑generation PCV21 pneumococcal conjugate vaccine covering more than 20 serotypes in infants and toddlers, marking the first candidate of its kind at late‑stage development. (Sanofi)

• On February 15, 2025, FDA approved GSK’s Penmenvy, a five‑in‑one meningococcal conjugate vaccine for use in individuals aged 10–25 years, designed to protect against serogroups A, B, C, W, and Y and simplify immunization protocols for adolescents and young adults. (biopharminternational.com)

• In May 2025, the U.S. FDA expanded Sanofi’s MenQuadfi meningococcal conjugate vaccine indication to include infants as young as six weeks old, making it the only vaccine in its class approved for such early immunization across age groups, enhancing pediatric coverage options. (medthority.com)

The Conjugate Vaccines Market Report encompasses a holistic examination of product types, applications, and end‑user landscapes within the broader vaccine ecosystem. It covers detailed segmentation across pneumococcal, meningococcal, Hib, and combination conjugate vaccine types, providing insights into adoption patterns, coverage breadth by serotypes, and technological formulation advances. Geographic analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, quantifying regional consumption volumes, regulatory environments, and infrastructure readiness for vaccine deployment. The report also evaluates application areas including routine pediatric immunization programs, adult and elderly booster initiatives, and targeted risk group immunizations, alongside emerging use cases such as travel and occupational health vaccination campaigns.

Technological focus areas include modular manufacturing platforms, digital cold‑chain monitoring, predictive supply analytics, and thermostable formulation trends that reduce logistics constraints. Industry focus sections assess competitive strategy, innovation pipelines, clinical development programs, and collaborative efforts among key players, as well as adoption behaviors across public health agencies, hospitals, and private healthcare providers. Emerging and niche market segments—such as higher‑valency conjugate vaccines beyond 20 serotypes and combination vaccine constructs—are examined for their impact on future demand patterns. The report delivers actionable insights tailored to business decision‑makers, combining quantitative data with strategic context on regulatory, economic, and technological dimensions shaping the Conjugate Vaccines landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pfizer, GSK, Sanofi, Merck & Co., Serum Institute of India, Moderna, Bharat Biotech, Valneva, Johnson & Johnson, Novavax |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |