Reports

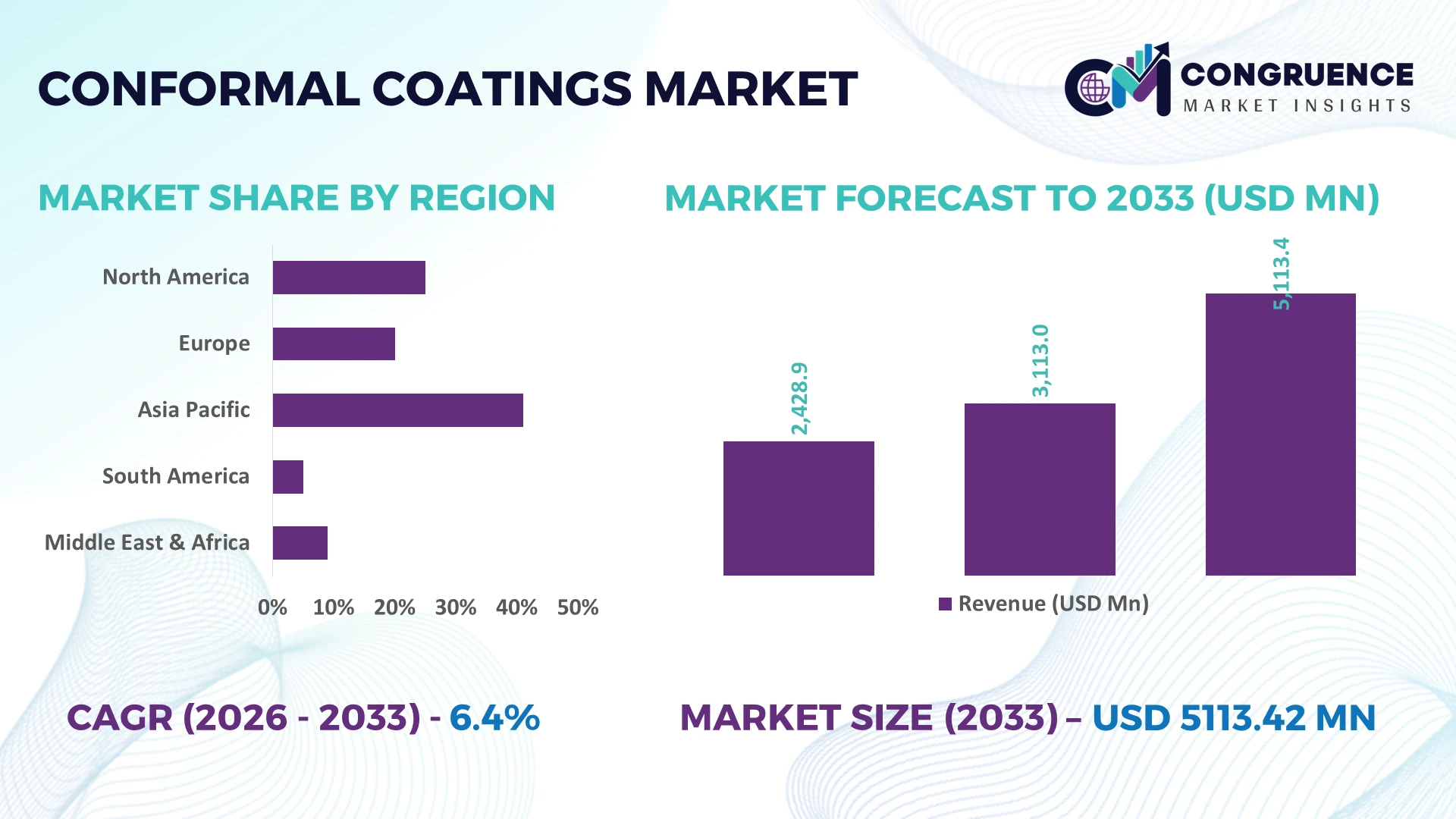

The Global Conformal Coatings Market was valued at USD 3113 Million in 2025 and is anticipated to reach a value of USD 5113.42 Million by 2033 expanding at a CAGR of 6.4% between 2026 and 2033. Growth is driven by rising deployment of high-reliability electronics in electric vehicles, aerospace systems, medical devices, and advanced semiconductor packaging requiring superior moisture, chemical, and thermal protection.

The United States dominates the global conformal coatings market with approximately 31% share, supported by over USD 52 billion in semiconductor manufacturing investments, strong aerospace production, and expanding EV electronics integration. Compared with China, which leads high-volume electronics manufacturing, the United States maintains higher adoption of premium coating technologies, with automated selective coating systems exceeding 68% utilization across advanced electronics facilities. Continued industrial policy supporting domestic semiconductor production strengthens long-term supply resilience and technology leadership.

Manufacturers should prioritize advanced coating formulations, automation capabilities, and regional production strategies to capture higher-value industrial electronics opportunities.

Market Size & Growth: USD 3113 Million (2025) to USD 5113.42 Million (2033) at 6.4% CAGR, supported by expanding EV electronics and semiconductor manufacturing.

Top Growth Drivers: EV electronics +24%, aerospace electronics +16%, industrial automation +19% accelerate global coating demand.

Short-Term Forecast: By 2028, automated coating processes improve production efficiency by 18% while reducing material waste by 15%.

Emerging Technologies: AI-enabled inspection, selective robotic coating, and UV-curable materials reduce defect rates by over 20%.

Regional Leaders: North America exceeds USD 1.6 billion, Asia-Pacific surpasses USD 2.1 billion, Europe approaches USD 1.1 billion through localized electronics expansion.

Consumer/End-User Trends: More than 62% of premium electronic assemblies adopt advanced protective coatings for longer service life.

Pilot/Case Example: 2026 manufacturing modernization projects improved coating consistency by 27% and reduced inspection failures by 21%.

Competitive Landscape: Top five companies control approximately 47% market share, led by Henkel, Chase Corporation, Dow, Shin-Etsu Chemical, and H.B. Fuller.

Regulatory & ESG Impact: Low-VOC coating adoption exceeds 38%, supporting stricter environmental compliance and cleaner manufacturing operations.

Investment & Funding: Over USD 2 billion supports production expansion, automation, and regional supply-chain diversification across high-growth electronics hubs.

Innovation & Future Outlook: Nano-coatings, bio-based formulations, and digital process monitoring strengthen product reliability amid global manufacturing realignment.

Growing electrification, miniaturized electronics, and mission-critical industrial equipment continue to expand demand for advanced conformal coatings across automotive, aerospace, telecommunications, and healthcare applications. UV-curable and silicone-based innovations improve production throughput, while automated selective coating adoption has surpassed 40% in advanced facilities. Ongoing regional manufacturing localization and evolving environmental compliance requirements are reshaping procurement strategies, setting the foundation for the strategic discussion.

Conformal coatings have become strategically important as electronic components continue to shrink while operating in increasingly harsh environments across electric vehicles, aerospace, industrial automation, telecommunications, and defense. Supply-chain restructuring since 2024 has accelerated localization of semiconductor and electronics manufacturing, encouraging coating suppliers to establish production closer to assembly hubs. This shift strengthens procurement resilience, reduces lead times, and supports manufacturers seeking consistent quality for high-reliability electronic assemblies.

Modern automated selective coating systems apply material with more than 95% placement accuracy while reducing coating consumption by nearly 25% compared with conventional manual spray methods, improving throughput and lowering rework costs. The United States leads in premium aerospace and defense applications with high automation adoption, whereas China maintains greater production scale through consumer electronics manufacturing. Over the next two to three years, automated inspection systems are expected to exceed 70% deployment across advanced electronics facilities, supported by AI-enabled quality control and digital manufacturing integration.

Automotive electronics manufacturers are increasingly deploying UV-curable coating lines that shorten curing cycles by over 60%, enabling faster production without compromising reliability. Companies are expanding localized manufacturing, strengthening material partnerships, and investing in environmentally compliant formulations to improve operational flexibility. Organizations that integrate advanced coating technologies with automated production and resilient supply networks will secure stronger competitive positioning in high-value electronics manufacturing.

Electrification, semiconductor localization, and industrial automation continue to accelerate adoption of conformal coatings across mission-critical electronics. More than 68% of advanced electronics manufacturers now integrate automated coating systems, while electric vehicle electronic content has increased by approximately 30% over recent vehicle generations. The United States and India are expanding domestic electronics manufacturing through industrial incentives, creating additional demand for premium protective coatings. This structural shift improves product reliability while reducing field failures in harsh operating conditions. Leading companies are expanding production capacity, introducing faster UV-curable formulations, and partnering with electronics manufacturers to deliver customized coating solutions. A notable strategic trend is the integration of coating processes directly into automated assembly lines, reducing production bottlenecks while improving quality consistency.

Fluctuating prices for specialty silicones, acrylic resins, and fluoropolymer materials continue to pressure production economics, while environmental regulations increase compliance costs for solvent-based formulations. Material procurement costs have experienced fluctuations exceeding 18% during recent supply disruptions, and low-VOC compliance investments have increased manufacturing expenses by nearly 12% for several producers. China remains an important supplier of specialty chemical intermediates, creating supply dependency during logistics disruptions. These factors directly affect pricing strategies, production scheduling, and inventory planning. Companies are responding through regional sourcing diversification, localized inventory management, long-term supplier contracts, and accelerated development of alternative formulations that maintain performance while improving supply stability and regulatory compliance.

Next-generation coating technologies are creating new opportunities through nano-engineered materials, bio-based formulations, and intelligent manufacturing systems. AI-enabled inspection platforms reduce coating defects by approximately 22%, while automated dispensing systems lower material consumption by nearly 20%. Japan continues advancing high-performance electronics manufacturing, encouraging greater adoption of precision coating technologies for semiconductor packaging and medical electronics. Companies are increasing R&D investments, expanding collaborative development with equipment suppliers, and integrating digital process monitoring into production lines. An emerging strategic opportunity lies in combining predictive analytics with automated coating control, allowing manufacturers to optimize material usage while improving long-term product reliability across high-value industrial applications.

Maintaining coating uniformity across increasingly compact electronic assemblies remains a significant execution challenge as component density continues to increase. More than 40% of production defects originate from process variation, while advanced inspection requirements can extend qualification cycles by nearly 15%. Germany's high-performance automotive electronics sector demands exceptionally strict quality validation, increasing operational complexity for global suppliers. Workforce shortages in precision manufacturing and process engineering further constrain production scalability. Companies must invest in advanced inspection technologies, workforce training, digital process validation, and collaborative automation partnerships to maintain consistent quality. Organizations that successfully standardize precision coating operations across multiple production facilities will strengthen long-term competitiveness and operational resilience.

AI-Driven Process Inspection: Electronics manufacturers are integrating AI-based optical inspection with automated conformal coating lines, reducing defect detection time by 35% and lowering rework by 22%. Semiconductor expansion in the United States and stricter quality validation requirements are accelerating deployment. Companies are connecting inspection software with manufacturing execution systems, enabling continuous process optimization and faster qualification across high-volume production facilities.

Selective Coating Automation Expansion: Automated selective coating systems now process nearly 40% more assemblies per shift while reducing coating material consumption by approximately 18% compared with conventional dispensing methods. Rising labor shortages in precision electronics manufacturing are encouraging automation investments, particularly in Japan and Germany. Equipment suppliers are expanding robotics partnerships and modular production platforms to improve throughput, repeatability, and operational flexibility across diverse electronic assemblies.

Transition Toward Sustainable Chemistries: Adoption of low-VOC and solvent-free coating formulations has increased by over 30% as environmental compliance becomes a purchasing requirement for multinational electronics manufacturers. Material optimization reduces hazardous waste generation by nearly 15% while maintaining long-term reliability. Coating suppliers are reformulating acrylic and silicone products, expanding localized production, and strengthening technical collaborations to meet evolving environmental standards without disrupting manufacturing performance.

Localized Supply Network Strategies: Electronics manufacturers are restructuring procurement networks, increasing regional material sourcing by approximately 25% to reduce logistics risks and improve delivery stability. Inventory lead times have declined by nearly 17% through localized distribution hubs supporting automotive and industrial electronics production. A notable shift involves coating suppliers establishing application laboratories near major manufacturing clusters, allowing faster formulation customization and accelerating product qualification for strategic customers.

Acrylic remains the leading conformal coating type because of its cost efficiency, rapid processing, and compatibility with high-volume electronics manufacturing, accounting for an estimated 36% of global coating demand. Its straightforward application and repair characteristics make it the preferred choice for consumer electronics and industrial equipment. Silicone continues to strengthen its position in automotive and outdoor electronics where thermal stability is essential, while urethane provides strong chemical resistance for demanding industrial environments. Epoxy retains strategic importance in applications requiring mechanical durability despite its relatively complex rework process.

Parylene represents the fastest-growing coating category as demand rises for ultra-thin, pinhole-free protection in medical electronics, aerospace assemblies, and advanced semiconductor packaging. Adoption of parylene deposition has increased by approximately 21% across high-reliability applications, while silicone-based coatings have expanded by nearly 16% in electric vehicle electronics. Companies are increasing investment in specialty coating technologies, expanding deposition capacity, and introducing application-specific formulations to strengthen differentiation and address evolving performance requirements across critical industries.

Consumer Electronics remains the largest application segment due to large-scale production of smartphones, computing devices, wearables, and connected home products requiring dependable moisture and contamination protection. The segment represents approximately 39% of coating consumption, supported by continuous product refresh cycles and increasing circuit density. Industrial Equipment maintains stable demand for factory automation systems, while Medical Devices require specialized coatings to improve reliability under sterilization and extended operating conditions. Aerospace & Defense continues emphasizing high-performance materials for mission-critical electronic assemblies.

Automotive Electronics is the fastest-growing application as vehicle electrification and advanced driver assistance systems significantly increase electronic content per vehicle. Conformal coating usage in automotive electronics has expanded by approximately 24%, while advanced power modules require nearly 18% higher protective coverage than previous generations. Manufacturers are expanding automated coating lines, integrating digital inspection technologies, and strengthening partnerships with automotive suppliers to improve production consistency and long-term component durability across evolving vehicle platforms.

Electronics represents the dominant end-user group, driven by large-scale production of consumer devices, telecommunications equipment, industrial controls, and semiconductor assemblies requiring consistent environmental protection. The segment accounts for approximately 44% of purchasing volume, supported by automated manufacturing and continuous miniaturization. Industrial Manufacturing remains a significant buyer through automation equipment and control systems, while Healthcare continues increasing procurement for diagnostic devices and implantable electronics requiring highly reliable protective coatings.

Automotive is the fastest-growing end-user as electric mobility, power electronics, and intelligent vehicle architectures expand coating requirements. Procurement volumes from automotive manufacturers have increased by approximately 23%, while Aerospace & Defense continues investing in premium formulations capable of performing under demanding environmental conditions. Suppliers are responding with customized product portfolios, localized technical support, strategic partnerships, and value-based pricing models that improve qualification speed and strengthen long-term customer relationships across high-performance manufacturing ecosystems.

North America accounted for the largest market share at 34.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 7.3% CAGR between 2026 and 2033.

Advanced Electronics Manufacturing Strengthens Premium Coating Demand

North America remains the leading regional market due to its concentration of semiconductor fabrication, aerospace manufacturing, defense electronics, and electric vehicle production. The region contributes over 34% of global demand, supported by high adoption of automated selective coating systems and stringent reliability standards. More than 70% of advanced electronics production lines utilize automated coating and inspection technologies to improve manufacturing consistency. Ongoing investments in domestic semiconductor capacity and electronics reshoring continue to increase demand for high-performance acrylic, silicone, and parylene coatings. Companies are expanding technical service centers, strengthening OEM partnerships, and integrating digital process monitoring to improve quality assurance and production efficiency.

United States Market Outlook: The United States remains the regional leader through its strong semiconductor ecosystem, aerospace manufacturing base, and expanding electric vehicle supply chain. Federal manufacturing initiatives continue supporting advanced electronics production, while automated coating deployment across high-value manufacturing facilities exceeds 68%. Domestic manufacturers increasingly prioritize premium protective materials for defense systems, industrial automation, and medical electronics. Coating suppliers are investing in localized production, collaborative product development, and application engineering capabilities to shorten qualification cycles and improve responsiveness for strategic customers.

Sustainability Standards Accelerate Material Innovation

Europe maintains a strong position through advanced automotive electronics, industrial automation, aerospace engineering, and strict environmental compliance requirements. The region represents approximately 27% of global market activity, with increasing preference for low-VOC and solvent-free coating technologies. More than 42% of newly qualified industrial coating formulations emphasize improved environmental performance while maintaining high durability. Electronics manufacturers continue modernizing production facilities through automation and precision dispensing technologies. Suppliers are expanding environmentally compliant product portfolios and strengthening partnerships with automotive and industrial equipment manufacturers to address evolving regulatory expectations and operational performance requirements.

Germany Market Outlook: Germany leads the European market through its highly developed automotive, industrial automation, and precision manufacturing industries. Advanced production facilities increasingly deploy automated coating systems to support complex electronic assemblies used in electric mobility and factory automation. More than 60% of premium automotive electronics production integrates automated protective coating processes. Manufacturers continue investing in digital manufacturing platforms, quality validation technologies, and sustainable production practices to maintain global competitiveness across high-performance industrial sectors.

Manufacturing Scale Drives Rapid Technology Deployment

Asia-Pacific represents the world's largest electronics manufacturing base and the fastest-expanding market for conformal coatings, supported by extensive consumer electronics, semiconductor packaging, telecommunications, and automotive electronics production. The region accounts for nearly 45% of global electronics manufacturing output, creating substantial demand for protective coating technologies. Automated coating installations have increased by approximately 24% across major manufacturing hubs as companies improve production consistency and throughput. Supply-chain diversification, localized material production, and expanding electronics exports continue strengthening regional manufacturing capabilities while encouraging investments in advanced coating technologies.

China Market Outlook: China dominates regional demand through its unmatched electronics manufacturing capacity, semiconductor packaging ecosystem, and expanding electric vehicle industry. Electronics production clusters continue integrating automated coating equipment to improve yield and reliability across high-volume assembly operations. Approximately 50% of the region's consumer electronics manufacturing is concentrated within China, supporting sustained demand for cost-efficient and high-performance coating materials. Domestic producers are expanding manufacturing capacity, investing in specialty formulations, and strengthening collaboration with global electronics brands to improve technology competitiveness.

Industrial Electronics Modernization Expands Demand

South America continues developing its conformal coatings market through industrial automation investments, automotive assembly expansion, renewable energy infrastructure, and growing electronics manufacturing capabilities. The region contributes approximately 6% of global market demand while gradually increasing deployment of protective coatings across industrial control systems and automotive electronics. Manufacturing modernization initiatives have improved automated coating adoption by nearly 15% in selected industrial facilities. Infrastructure limitations and dependence on imported specialty materials remain operational constraints, encouraging suppliers to strengthen regional distribution networks and technical support capabilities.

Brazil Market Outlook: Brazil serves as the primary regional market due to its established automotive manufacturing base, expanding industrial automation sector, and improving electronics production capabilities. Domestic manufacturers increasingly adopt advanced coating technologies to improve equipment reliability in demanding operating environments. Automotive electronics production continues expanding, supported by investments in localized component manufacturing and factory modernization. International suppliers are increasing partnerships with regional distributors and application specialists to strengthen technical support and improve product availability across strategic industrial sectors.

Industrial Diversification Supports Electronics Protection Technologies

The Middle East & Africa market is steadily advancing through industrial diversification, defense modernization, renewable energy investments, and expanding telecommunications infrastructure. The region contributes nearly 5% of global demand, with increasing adoption of conformal coatings for industrial electronics operating in high-temperature and corrosive environments. Electronics infrastructure projects have increased deployment of protected control systems by approximately 18% across strategic industrial facilities. Suppliers are strengthening regional distribution, technical training, and engineering support to address specialized operational requirements and improve long-term equipment reliability.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through industrial diversification programs, advanced manufacturing investments, and expanding defense and energy infrastructure. Smart manufacturing projects continue increasing demand for reliable electronic protection across automation systems and power infrastructure. Industrial facilities are accelerating deployment of digitally controlled equipment requiring durable protective coatings under challenging environmental conditions. Companies are expanding local partnerships, engineering support, and application capabilities to align with national manufacturing priorities and strengthen long-term operational resilience.

The competitive landscape is led by Henkel, Chase Corporation, Dow, Shin-Etsu Chemical, and H.B. Fuller, competing against regional formulation specialists and contract coating service providers. Global technology leaders compete through premium performance and application engineering, while regional manufacturers challenge primarily on pricing and delivery flexibility. The top five companies collectively account for approximately 47% of market share, creating a moderately consolidated structure. Competition increasingly depends on formulation performance, automated process compatibility, localized supply chains, and customization. Automated coating solutions improve production efficiency by nearly 20%, while low-VOC formulations reduce compliance costs by approximately 15%, strengthening supplier differentiation. Companies are expanding regional production, forming electronics OEM partnerships, investing in UV-curable and parylene technologies, and integrating technical support with material supply. The competitive shift favors vertically integrated suppliers capable of combining materials, equipment compatibility, and engineering expertise. High qualification requirements and customer validation cycles remain major entry barriers. Winning requires differentiated formulations, localized manufacturing, rapid technical support, and reliable supply resilience.

Henkel AG & Co. KGaA

Dow Inc.

Chase Corporation

Shin-Etsu Chemical Co., Ltd.

H.B. Fuller Company

MG Chemicals

Electrolube

KISCO Ltd.

Chemtronics

Dymax Corporation

CSL Silicones Inc.

Specialty Coating Systems, Inc.

ALTANA AG

Europlasma NV

Advanced conformal coating production is transitioning from conventional manual spray processes to automated selective coating, AI-enabled inspection, and digitally controlled dispensing platforms. Automated selective coating improves material utilization by approximately 18% while reducing process variation by nearly 25%. More than 65% of newly installed high-volume electronics production lines now incorporate robotic coating systems integrated with real-time quality monitoring. These technologies enable manufacturers to improve consistency, shorten production cycles, and reduce expensive field failures in mission-critical electronic assemblies.

Emerging technologies include nano-engineered coatings, UV-curable formulations, plasma surface activation, and digital process analytics. Compared with conventional solvent-based coating systems, UV-curable technologies reduce curing time by over 60% while lowering energy consumption by approximately 30%. Electronics manufacturers producing electric vehicle control modules, medical devices, and aerospace electronics gain the greatest operational advantage through faster qualification, reduced rework, and improved reliability. Suppliers are increasingly integrating automated inspection with predictive process control to strengthen production efficiency and quality assurance.

Between 2026 and 2028, intelligent manufacturing platforms will accelerate adoption of closed-loop coating systems combining machine vision, AI process optimization, and digital traceability. Deployment of predictive quality control is expected to exceed 70% across advanced electronics facilities. Companies investing early in smart coating ecosystems, specialty materials, and automation-compatible formulations will achieve stronger production scalability, faster customer qualification, and sustainable competitive differentiation as electronics manufacturing becomes increasingly precision-driven.

February 2026 – Henkel introduced the solvent-free LOCTITE Stycast UV 7998 conformal coating with UL 94 V-0 certification, requiring up to 4× less sprayed volume than conventional solvent-based coatings while enabling up to 40% lower CO₂ emissions, strengthening sustainable electronics manufacturing competitiveness. Source: henkel.com

April 2025 – Henkel showcased AI-enabled material simulation, advanced functional coatings, and digital battery manufacturing technologies at The Battery Show Europe, helping battery manufacturers reduce development cycles while accelerating product validation through AI-assisted engineering workflows for next-generation electric mobility applications. Source: henkel.com

March 2026 – Henkel announced the planned acquisition of Stahl Group, adding approximately €725 million in annual business scale across specialty coatings and strengthening its global high-performance coatings portfolio through broader technology capabilities and expanded industrial market reach. Source: henkel.com

October 2025 – Henkel presented its award-winning LOCTITE Stycast CC 8555 conformal coating for industrial power applications, highlighting enhanced protection against moisture and chemicals while expanding its electronics materials portfolio supporting high-reliability power, automation, telecommunications, and aviation systems. Source: electronicsmedia.info coverage

This report delivers comprehensive analysis of the global conformal coatings market across acrylic, silicone, urethane, epoxy, and parylene technologies, covering applications in consumer electronics, automotive electronics, industrial equipment, medical devices, and aerospace & defense. It evaluates purchasing trends across five major end-user industries and assesses competitive positioning across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 70% of the assessment focuses on operational adoption, manufacturing trends, technology evolution, and enterprise deployment strategies.

The study examines automation, selective coating systems, UV-curable materials, AI-enabled inspection, and sustainable formulation developments influencing production efficiency and product reliability between 2026 and 2033. It benchmarks leading manufacturers, investment priorities, regional manufacturing expansion, and supply-chain strategies while identifying emerging opportunities in high-reliability electronics, semiconductor packaging, electric mobility, and industrial automation. The report supports market entry planning, capacity expansion, competitive benchmarking, partnership evaluation, and long-term strategic decision-making through actionable business intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3113 Million |

Market Revenue in 2033 | USD 5113.42 Million |

CAGR (2026 - 2033) | 6.4% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Henkel AG & Co. KGaA, Dow Inc., Chase Corporation, Shin-Etsu Chemical Co., Ltd., H.B. Fuller Company, MG Chemicals, Electrolube, KISCO Ltd., Chemtronics, Dymax Corporation, CSL Silicones Inc., Specialty Coating Systems, Inc., ALTANA AG, Europlasma NV |

Customization & Pricing | Available on Request (10% Customization is Free) |