Reports

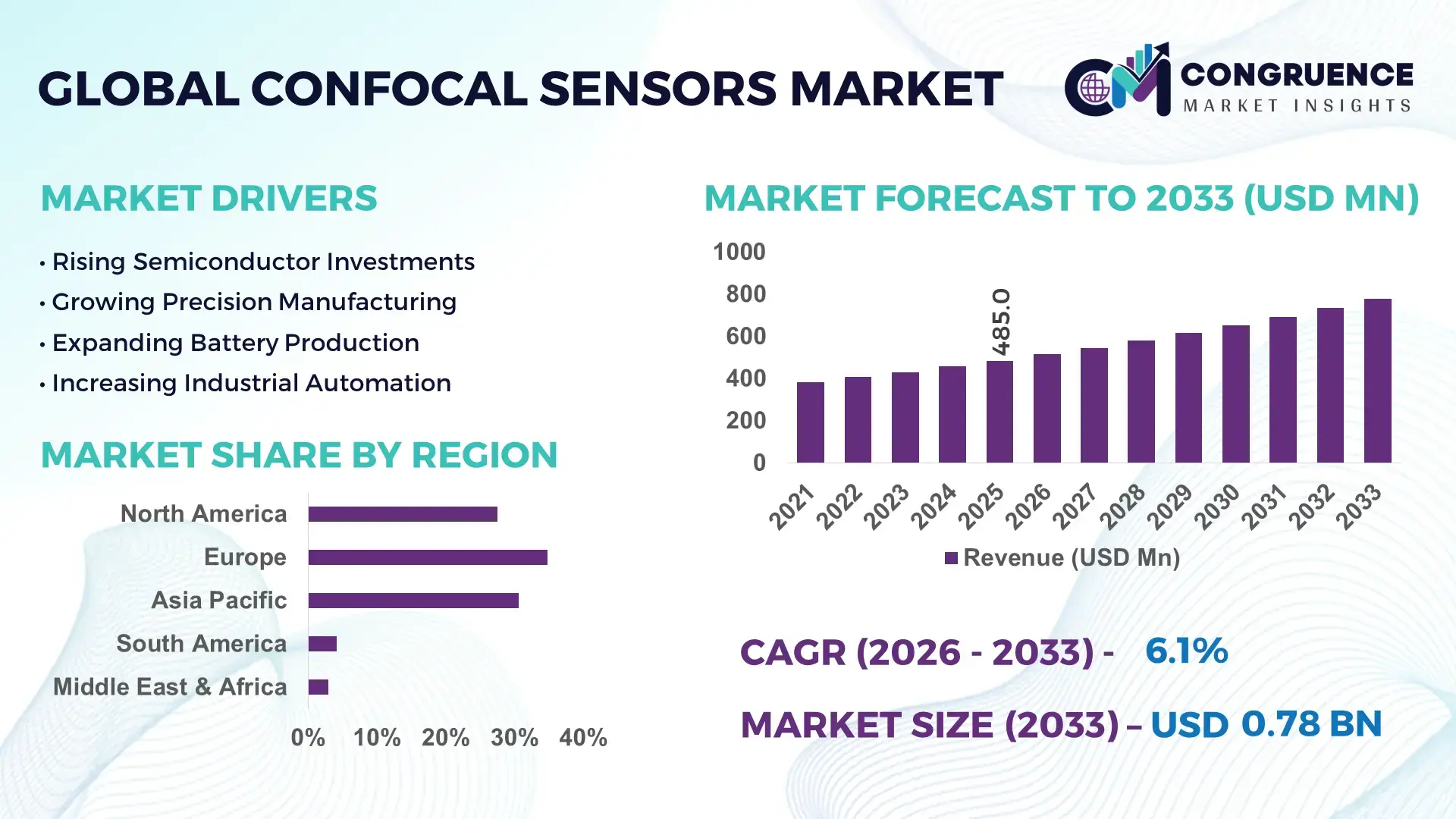

The Global Confocal Sensors Market was valued at USD 485 Million in 2025 and is anticipated to reach a value of USD 778.9 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. Growth is primarily driven by rising deployment of nanometer-level precision measurement systems across semiconductor wafer inspection, EV battery manufacturing, and automated electronics assembly lines requiring sub-micron dimensional accuracy.

Germany remains the dominant country in the global confocal sensors ecosystem, accounting for approximately 24% of high-precision industrial metrology equipment production, supported by over 48,000 advanced manufacturing facilities and strong investment in Industry 4.0 modernization. Germany's optical measurement equipment exports exceed those of Japan in several industrial inspection categories, while Japanese manufacturers maintain higher adoption across semiconductor fabrication environments with precision inspection rates exceeding 80% in leading fabs. The ongoing European industrial resilience initiatives following supply-chain realignments have further accelerated domestic automation investments.

Strategically, vendors that combine AI-enabled inspection analytics with ultra-precision sensing platforms are positioned to secure long-term competitive advantage across high-value manufacturing environments.

Market Size & Growth: USD 485 Million in 2025, reaching USD 778.9 Million by 2033, supported by increasing semiconductor inspection intensity and advanced manufacturing automation requirements.

Top Growth Drivers: Semiconductor inspection demand (+28%), industrial automation deployment (+22%), and EV battery production expansion (+19%) are accelerating sensor adoption.

Short-Term Forecast: By 2028, automated optical inspection efficiency is projected to improve by nearly 18% through integration of high-speed confocal measurement systems.

Emerging Technologies: AI-powered defect recognition, edge-computing analytics, and multi-axis robotic metrology are reshaping advanced sensing applications.

Regional Leaders: Europe (~USD 250 Million), Asia-Pacific (~USD 220 Million), and North America (~USD 180 Million) lead adoption through smart factory and semiconductor investments.

Consumer/End-User Trends: More than 65% of advanced electronics manufacturers prioritize non-contact dimensional inspection technologies for precision quality control.

Pilot/Case Example: A 2024 semiconductor inspection upgrade reduced measurement errors by 32% while improving throughput by 21% using confocal scanning systems.

Competitive Landscape: Leading suppliers collectively control nearly 45% of global market activity, with major participants including Keyence, Micro-Epsilon, Sensofar, Precitec, and NanoFocus.

Regulatory & ESG Impact: Precision inspection technologies contribute to material waste reductions of up to 15% in high-value manufacturing environments.

Investment & Funding: More than USD 1.2 Billion has been directed toward industrial automation, semiconductor expansion, and optical metrology infrastructure projects globally.

Innovation & Future Outlook: High-speed inline metrology, AI-assisted process control, and digital-twin-enabled inspection architectures are becoming key competitive differentiators.

Confocal sensors are becoming essential across semiconductor fabrication, precision electronics, EV battery production, and medical device manufacturing where sub-micron measurement accuracy is critical. Recent innovations include AI-assisted defect detection, ultra-fast chromatic confocal scanning, and integrated robotic inspection platforms. More than 60% of new smart-factory quality-control projects now prioritize non-contact metrology solutions, while ongoing semiconductor supply-chain localization initiatives continue to expand deployment opportunities, setting the stage for broader strategic adoption.

Confocal sensors are becoming strategically important because manufacturers increasingly compete on precision, yield optimization, and production consistency rather than volume alone. The transition toward highly automated semiconductor, electronics, and EV battery production has elevated demand for real-time dimensional inspection capabilities. Simultaneously, supply-chain restructuring across Europe, the United States, and Asia is encouraging localized advanced manufacturing investments that require next-generation metrology infrastructure.

Compared with conventional laser triangulation systems, advanced confocal sensors deliver up to 30% higher measurement accuracy on reflective and transparent surfaces while reducing inspection-related rework rates by approximately 20%. Japan and South Korea continue to lead deployment within semiconductor manufacturing, whereas Germany demonstrates stronger adoption across industrial automation and precision engineering applications. Over the next two to three years, factory-level implementation of AI-assisted inspection systems is expected to increase substantially as manufacturers prioritize process stability and defect prevention.

A practical example can be seen in EV battery manufacturing, where confocal sensors enable continuous electrode thickness verification and surface inspection without interrupting production flow. Companies are expanding partnerships with robotics integrators, machine-vision providers, and software developers to create complete quality-control ecosystems. Organizations that successfully integrate precision sensing, analytics, and automation platforms will strengthen operational efficiency, improve production yields, and secure long-term competitive positioning across advanced manufacturing value chains.

The rapid evolution of semiconductor manufacturing and high-precision industrial production is accelerating confocal sensor deployment. Advanced semiconductor facilities now inspect significantly more process layers than a decade ago, while wafer complexity has increased by over 40%, creating greater demand for sub-micron measurement systems. In EV battery manufacturing, automated inline quality-control installations have expanded by nearly 25% as producers seek tighter dimensional tolerances and lower defect rates. The global push toward digital manufacturing following supply-chain disruptions has also encouraged investments in smart inspection infrastructure. In response, sensor manufacturers are expanding production capacity, developing AI-enabled measurement software, and forming partnerships with robotics and machine-vision providers. A notable strategic advantage is the ability of confocal sensors to inspect reflective, transparent, and complex surfaces within a single measurement workflow, improving productivity and reducing quality-control bottlenecks.

Confocal sensor adoption remains constrained by significant implementation costs and integration complexity. Advanced industrial metrology systems can require capital expenditures 20–35% higher than conventional optical inspection solutions, particularly when combined with automation platforms and analytics software. More than 45% of small and medium-sized manufacturers cite integration expenses and calibration requirements as primary adoption barriers. Dependence on specialized optical components and precision lenses further exposes suppliers to procurement volatility and lead-time disruptions. In Germany and Japan, manufacturers have responded by increasing localization of critical optical components and establishing long-term supplier agreements. Companies are also introducing modular sensor architectures that reduce installation costs and simplify deployment. The key operational challenge remains balancing measurement precision with total ownership costs, particularly for mid-sized manufacturing facilities operating under strict capital allocation constraints.

The convergence of AI, machine vision, and industrial automation is creating substantial opportunities for confocal sensor vendors. More than 70% of newly commissioned advanced manufacturing facilities are incorporating digital quality-control systems capable of real-time data collection and analytics. AI-assisted inspection platforms can reduce false-defect identification rates by nearly 25%, improving throughput and production consistency. China's continued smart-manufacturing investments and India's growing electronics production ecosystem are creating attractive deployment opportunities beyond traditional industrial markets. Companies are investing heavily in software-defined metrology platforms, cloud-connected inspection systems, and autonomous production monitoring capabilities. A particularly valuable opportunity lies in predictive quality management, where confocal measurement data can identify process deviations before defects occur. Vendors building integrated ecosystems rather than standalone hardware solutions are positioned to capture higher-value industrial contracts and long-term service revenues.

A major challenge involves maintaining measurement consistency across increasingly automated and geographically distributed production networks. Modern manufacturing environments generate inspection datasets that have expanded by more than 50% over recent years, creating integration and data-management pressures. Approximately 38% of manufacturers report difficulties synchronizing sensor outputs with broader manufacturing execution systems and digital-twin platforms. As production lines become more interconnected, ensuring calibration stability, interoperability, and cybersecurity resilience becomes increasingly important. Semiconductor and electronics facilities operating across multiple countries face additional challenges related to standardization and workforce expertise. To address these issues, companies are investing in unified software architectures, advanced calibration technologies, and workforce training initiatives. Long-term competitiveness will depend on delivering scalable inspection ecosystems capable of maintaining accuracy, interoperability, and operational reliability across complex manufacturing environments.

AI-Enabled Inline Inspection Expansion — Manufacturers are embedding AI-assisted confocal measurement platforms directly into production workflows, with automated defect classification adoption rising by nearly 35% across semiconductor and electronics facilities. Inspection cycle times have declined by approximately 20%, while measurement repeatability has improved by over 15%. Driven by labor constraints and stricter quality requirements, companies are partnering with machine-vision software providers to create closed-loop inspection systems that reduce manual intervention and improve production consistency.

Semiconductor Localization Driving Deployment — Ongoing semiconductor capacity expansion in the United States, Japan, and India is accelerating demand for advanced optical metrology. More than 40% of newly commissioned wafer-processing lines now incorporate high-resolution confocal inspection systems at multiple process stages. Supply-chain diversification initiatives following global chip shortages have increased investment in domestic manufacturing infrastructure. Sensor suppliers are responding through localized service networks, production expansion, and strategic collaborations with semiconductor equipment manufacturers to support higher-volume deployments.

Multi-Sensor Automation Integration — Industrial users are increasingly combining confocal sensors with machine vision, laser scanning, and robotic positioning systems. Adoption of integrated metrology architectures has increased by nearly 28% since 2024, reducing inspection bottlenecks and improving throughput by approximately 18%. A notable shift involves replacing standalone inspection stations with synchronized automation cells. Companies are restructuring product portfolios toward interoperable platforms capable of supporting digital manufacturing environments and unified process-control workflows.

High-Precision EV Manufacturing Adoption — Electric vehicle battery and power electronics manufacturers are expanding use of confocal sensing for electrode, coating, and surface-quality inspection. Automated quality-control deployments within battery production environments have grown by nearly 30%, while scrap reduction rates have improved by approximately 12%. Increasing pressure to optimize material utilization and maintain production quality is encouraging manufacturers to deploy real-time measurement systems. Suppliers are scaling application-specific solutions and forming partnerships with battery equipment integrators to strengthen long-term market positioning.

Chromatic confocal sensors represent the leading type segment, accounting for an estimated 42% of total deployments due to their ability to measure transparent, reflective, and complex surfaces with exceptional accuracy. Their strong adoption across semiconductor wafer inspection, precision electronics, and medical device manufacturing supports continued dominance. Manufacturers favor these systems because they deliver non-contact measurement capabilities while reducing calibration complexity and inspection downtime. Laser confocal sensors maintain a substantial installed base in industrial automation and quality-control applications, particularly within Germany and Japan where precision engineering remains a key competitive advantage. White-light confocal sensors are emerging as the fastest-growing type segment, supported by increasing use in advanced materials inspection and multilayer surface characterization. Adoption rates within high-precision electronics manufacturing have increased by nearly 24% over the last two years. Meanwhile, hybrid confocal configurations are gaining strategic relevance as manufacturers seek flexible measurement architectures capable of supporting multiple production environments. Companies are expanding product portfolios, enhancing software integration, and investing in AI-assisted measurement platforms to differentiate performance and improve deployment scalability. These shifts are directing investment toward adaptable sensing technologies that support broader industrial automation objectives.

Semiconductor inspection represents the leading application segment, supported by increasing wafer complexity, shrinking feature sizes, and stricter quality-control requirements. Approximately 38% of confocal sensor deployments are linked to semiconductor production workflows, where non-contact measurement and nanoscale precision are operational necessities. Manufacturers continue expanding metrology capacity to improve process yields and reduce defect-related losses. Electronics assembly and precision engineering applications remain important contributors, particularly within automated production environments requiring continuous dimensional verification and surface-quality analysis. Battery manufacturing and advanced energy-storage inspection are emerging as the fastest-growing application segment. Adoption across battery electrode inspection and coating verification processes has increased by nearly 27% as producers prioritize manufacturing consistency and material efficiency. Medical device manufacturing is also expanding usage due to stricter dimensional compliance requirements and miniaturized component production. Companies are integrating confocal systems into automated quality-control workflows, strengthening deployment across mission-critical manufacturing processes. Demand is increasingly shifting toward applications where measurement speed, process traceability, and production optimization create direct operational advantages.

Electronics and semiconductor manufacturers constitute the dominant end-user segment, representing roughly 45% of global demand due to extensive use of high-precision inspection systems across fabrication, packaging, and assembly operations. These organizations operate highly automated production environments where dimensional accuracy directly influences product quality and yield performance. Their purchasing activity is supported by ongoing investments in advanced manufacturing infrastructure and increasing deployment of real-time quality-control systems. Industrial equipment manufacturers remain a significant buyer group, leveraging confocal sensors to enhance process reliability and automated inspection capabilities. Electric vehicle and battery manufacturers represent the fastest-growing end-user segment, with adoption levels increasing by approximately 26% as production capacity continues to expand globally. Medical technology companies are also strengthening procurement activity as miniaturized devices require tighter manufacturing tolerances and traceability standards. Aerospace and precision engineering firms continue to invest selectively in advanced metrology systems for mission-critical applications. Suppliers are responding through customized solutions, industry-specific partnerships, and integrated software ecosystems designed to improve customer retention and operational value. Future demand is increasingly concentrated among manufacturers pursuing automation-driven productivity gains and advanced quality-control strategies.

Europe accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.3% between 2026 and 2033.

North America represents approximately 27.5% of global confocal sensor demand, supported by semiconductor manufacturing expansion, aerospace production, and advanced industrial automation investments. The region continues to strengthen deployment of high-precision optical metrology systems across wafer fabrication, battery manufacturing, and medical device production. More than 40% of newly commissioned semiconductor process-control upgrades now incorporate advanced non-contact measurement technologies to improve yield performance and process stability. Growing investment in domestic chip manufacturing infrastructure and digital manufacturing initiatives is increasing demand for integrated inspection platforms. Companies are expanding partnerships with robotics, machine-vision, and automation providers to improve production efficiency while reducing inspection-related downtime across high-value manufacturing operations.

United States Market Outlook: The United States remains the dominant country market due to its concentration of semiconductor fabrication facilities, aerospace manufacturing hubs, and industrial automation deployments. Large-scale investments in domestic semiconductor production continue to strengthen demand for precision metrology systems. More than 50 advanced semiconductor expansion projects announced since recent industrial policy initiatives have increased requirements for inline inspection technologies. Manufacturers are prioritizing AI-enabled quality-control systems and automated process-monitoring infrastructure to support higher production yields and operational resilience.

Europe maintains the largest regional position, accounting for nearly 34.8% of global market activity due to its strong precision engineering base and advanced manufacturing ecosystem. Industrial automation modernization programs across automotive, electronics, and machinery sectors continue to increase deployment of confocal measurement technologies. Approximately 45% of precision manufacturing facilities undergoing digital transformation initiatives are integrating advanced optical metrology capabilities into production workflows. Sustainability-driven manufacturing optimization and stringent quality requirements are further supporting adoption. Enterprises are investing in smart-factory architectures that combine robotics, machine vision, and real-time inspection systems to improve productivity and reduce production variability.

Germany Market Outlook: Germany serves as the technological center of the European confocal sensors market through its leadership in industrial automation, precision engineering, and machine-tool manufacturing. The country accounts for roughly one-quarter of Europe's advanced manufacturing equipment output and maintains one of the world's highest concentrations of Industry 4.0 deployments. German manufacturers are increasingly integrating high-resolution optical metrology into automated production environments to improve process traceability, dimensional accuracy, and manufacturing consistency. Strong collaboration between industrial equipment suppliers and automation technology providers continues to support innovation and deployment expansion.

Asia-Pacific accounts for approximately 30.6% of global demand and represents the fastest-evolving deployment environment for confocal sensing technologies. Strong electronics manufacturing activity, semiconductor capacity additions, and EV battery production expansion continue to drive adoption across multiple industries. More than 55% of global semiconductor production capacity is concentrated within the region, creating sustained demand for advanced inspection infrastructure. Ongoing investment in smart manufacturing and factory automation is accelerating implementation of high-speed metrology systems. Manufacturers are increasingly integrating confocal sensors into automated production lines to enhance quality control, improve throughput, and support precision manufacturing objectives.

China Market Outlook: China remains the largest country market in Asia-Pacific due to its extensive electronics manufacturing ecosystem, semiconductor expansion strategy, and industrial modernization initiatives. The country continues to increase investment in advanced manufacturing technologies aimed at improving domestic production capabilities. Electronics and semiconductor facilities have expanded automated inspection deployments by more than 25% over recent years. Confocal sensing systems are increasingly utilized across battery production, consumer electronics assembly, and industrial automation applications as manufacturers prioritize production quality, process optimization, and technology localization objectives.

South America accounts for approximately 4.2% of global market activity and is gradually expanding adoption of advanced optical metrology solutions. Demand is primarily concentrated within automotive manufacturing, industrial machinery production, mining equipment maintenance, and electronics assembly operations. Manufacturers are increasingly investing in automated quality-control systems to improve productivity and reduce operational inefficiencies. Recent industrial modernization projects have increased deployment of advanced inspection technologies by nearly 15% across selected manufacturing sectors. While infrastructure limitations and capital investment constraints continue to affect adoption speed, growing automation initiatives are creating favorable conditions for technology deployment and long-term market development.

Brazil Market Outlook: Brazil represents the largest market within South America due to its diversified industrial base and expanding automation investments. Automotive manufacturing facilities, industrial equipment producers, and electronics assembly operations are increasingly adopting advanced metrology solutions to strengthen quality-control capabilities. Industrial automation installations have expanded steadily within major manufacturing corridors, particularly around São Paulo. Companies are focusing on production efficiency improvements and process modernization strategies, creating opportunities for precision measurement technologies that support operational optimization and manufacturing competitiveness.

The Middle East & Africa region accounts for approximately 2.9% of global demand but is steadily increasing adoption through industrial diversification and advanced manufacturing initiatives. Governments and enterprises are investing in automation, electronics production, aerospace development, and industrial modernization programs that require precision inspection capabilities. Several large-scale industrial projects have incorporated smart-manufacturing technologies, contributing to an estimated 18% increase in advanced quality-control deployments. Demand remains concentrated in specialized manufacturing applications, infrastructure development projects, and technology-focused industrial zones. Companies are establishing partnerships and technical support networks to improve deployment capabilities and strengthen regional market presence.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the most strategically significant country market due to ongoing industrial diversification efforts and substantial investment in advanced manufacturing infrastructure. National industrial development programs are supporting adoption of automation, precision engineering, and smart-factory technologies across multiple sectors. Manufacturing modernization initiatives have accelerated deployment of digital quality-control systems within industrial zones and technology-focused projects. As enterprises prioritize operational efficiency and production quality, demand for advanced optical inspection solutions continues to strengthen alongside broader industrial transformation objectives.

The competitive landscape is led by global precision sensing specialists such as Keyence, Micro-Epsilon, Precitec, Sensofar, NanoFocus, and STIL, competing directly against regional metrology suppliers and lower-cost optical measurement vendors. The top five players collectively control approximately 52% of market activity, with competition centered on measurement accuracy, integration flexibility, software intelligence, and deployment speed rather than price alone. Technology leadership remains the primary differentiator. High-performance suppliers achieve up to 30% faster inspection throughput and 20% lower calibration frequency compared with conventional optical systems. Customers increasingly prioritize sub-micron accuracy, AI-enabled analytics, and seamless automation integration, resulting in software-driven differentiation. OEM-focused providers are strengthening positions through embedded sensor architectures, while metrology specialists compete through application-specific customization and advanced measurement capabilities. Competitive activity is increasingly focused on product expansion, semiconductor-focused partnerships, vertical software integration, and localized technical support networks. A major market shift involves the transition from standalone sensors to intelligent inspection ecosystems connected with robotics and machine-vision platforms. The primary entry barrier remains optical engineering expertise and application validation requirements. Winning requires superior precision, automation compatibility, domain-specific solutions, and strong industrial support capabilities.

Micro-Epsilon Messtechnik GmbH & Co. KG

PRECITEC GmbH & Co. KG

Sensofar Group

NanoFocus AG

STIL S.A.S.

Polytec GmbH

Marposs S.p.A.

LMI Technologies

SICK AG

Omron Corporation

Cognex Corporation

Mitutoyo Corporation

Carl Zeiss Industrial Metrology

Current technology adoption is centered on chromatic confocal sensing, high-speed optical controllers, and AI-assisted measurement software. More than 65% of advanced semiconductor and electronics inspection environments now utilize non-contact optical metrology systems to improve dimensional verification and defect detection. Modern confocal platforms reduce inspection-related rework by approximately 18% while improving repeatability in automated production environments. Integration with robotics, machine vision, and industrial Ethernet architectures is becoming standard across precision manufacturing operations.

Emerging technologies include multi-channel confocal controllers, edge-based analytics, digital twins, and predictive quality-control platforms. Compared with conventional laser triangulation systems, advanced confocal sensing delivers up to 30% higher measurement accuracy on transparent and reflective materials while reducing validation time by nearly 15%. Semiconductor manufacturers, battery producers, and medical device companies gain the greatest operational advantage because these technologies support tighter tolerances and continuous inline process monitoring. Adoption of AI-enabled inspection algorithms has increased by more than 25% across newly automated production facilities.

Between 2026 and 2028, disruptive innovation will focus on autonomous inspection ecosystems combining confocal sensing, machine learning, and real-time process optimization. Manufacturers deploying integrated metrology architectures are expected to achieve throughput improvements exceeding 20%. Competitive advantage will increasingly favor companies capable of combining hardware precision, software intelligence, and scalable automation platforms. Organizations delaying deployment risk lower process visibility, slower quality feedback cycles, and reduced manufacturing efficiency.

May 2025 – Micro-Epsilon launched the confocalDT IFC2416 high-performance confocal chromatic controller featuring measurement rates up to 25 kHz and multilayer inspection capability for up to five layers. The development strengthened high-speed semiconductor and battery inspection applications while improving inline measurement productivity.

April 2025 – PRECITEC joined the QUAZE collaborative research initiative with research partners to develop advanced optical testing technologies for photovoltaic manufacturing. The project targets improved inspection precision and production optimization across next-generation solar manufacturing workflows, enhancing industrial metrology capabilities. Source: www.precitec.com

December 2025 – Micro-Epsilon introduced the confocalDT IFS2407-xHT/VAC sensor series capable of operating at temperatures up to 200°C while supporting ultra-high-vacuum environments. The innovation expands deployment opportunities within semiconductor fabrication, electronics production, and precision machine-building applications requiring extreme operating conditions.

February 2026 – Micro-Epsilon expanded its portfolio with IFC2412 and IFC2417 two-channel confocal controllers supporting 2 nm resolution and two-sided thickness measurement using a single controller. The development improves inspection efficiency and reduces hardware requirements across battery cell production, semiconductor manufacturing, and optical inspection environments.

This report provides comprehensive analysis of the global confocal sensors industry across technology categories, application environments, end-user groups, and regional markets. Coverage includes chromatic confocal systems, laser confocal sensors, white-light confocal technologies, and emerging hybrid architectures. The assessment evaluates deployment patterns across semiconductor inspection, electronics manufacturing, battery production, medical devices, precision engineering, and industrial automation. More than 70% of market demand originates from high-precision manufacturing environments where dimensional accuracy and process control are operational priorities.

The study further examines competitive positioning, technology evolution, automation integration trends, and regional adoption dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Strategic insights cover AI-enabled metrology, machine-vision integration, smart-factory deployment, and advanced quality-control systems expected to shape market direction between 2026 and 2033. The report supports investment evaluation, expansion planning, partnership development, product strategy, and long-term competitive decision-making through detailed analysis of adoption trends, enterprise demand patterns, and technology-driven transformation opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 485 Million |

| Market Revenue (2033) | USD 778.9 Million |

| CAGR (2026–2033) | 6.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Keyence Corporation; Micro-Epsilon Messtechnik GmbH & Co. KG; PRECITEC GmbH & Co. KG; Sensofar Group; NanoFocus AG; STIL S.A.S.; Polytec GmbH; Marposs S.p.A.; LMI Technologies; SICK AG; Omron Corporation; Cognex Corporation; Mitutoyo Corporation; Carl Zeiss Industrial Metrology |

| Customization & Pricing | Available on Request (10% Customization Free) |