Reports

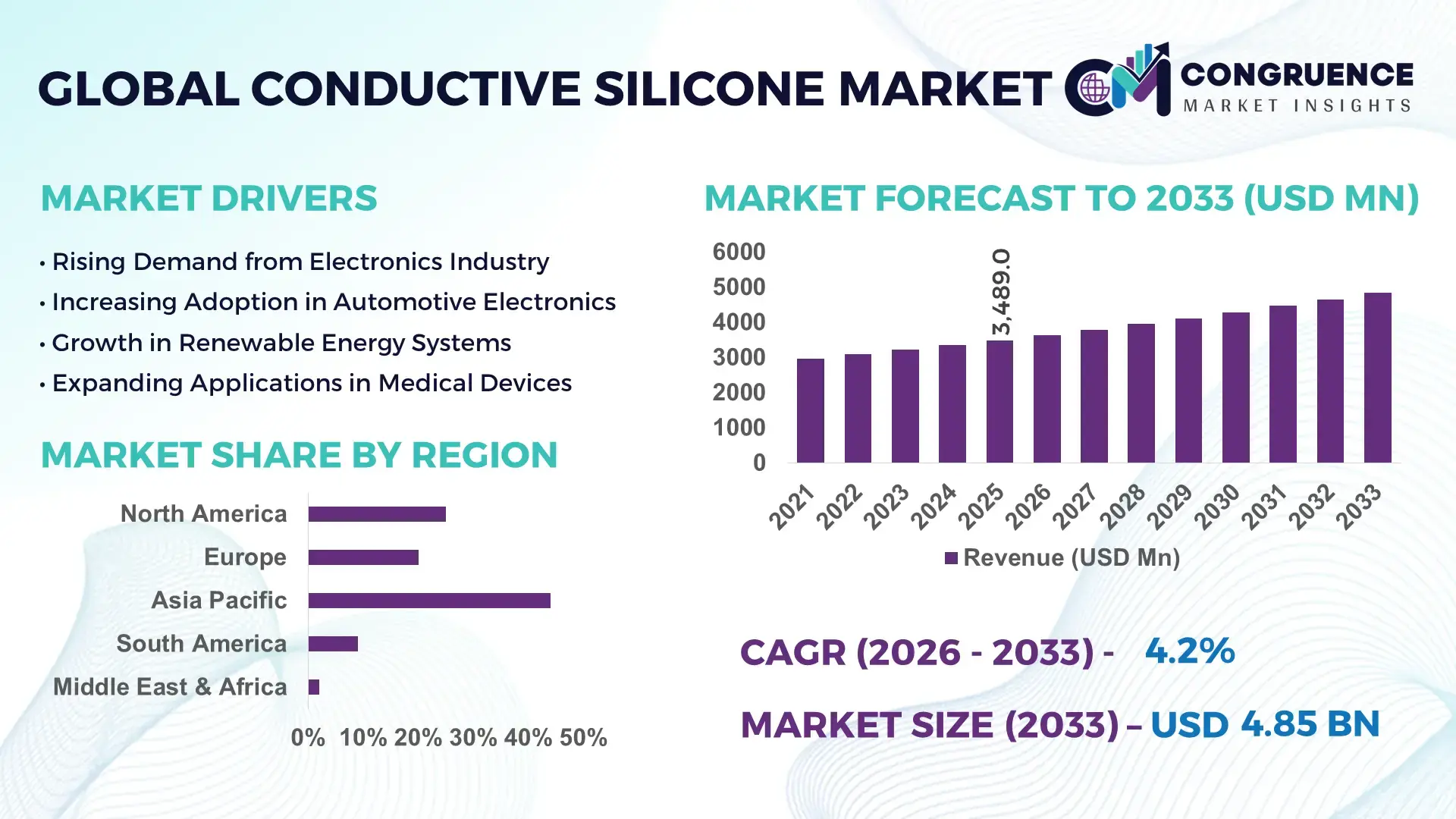

The Global Conductive Silicone Market was valued at USD 3489 Million in 2025 and is anticipated to reach a value of USD 4848.89 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. The growth is primarily driven by rising demand for advanced electronic shielding materials in high-performance applications.

China continues to be the dominant country in the conductive silicone market, supported by its expansive electronics manufacturing ecosystem and strong investments in advanced materials. The country produces over 30% of global electronic components, creating sustained demand for conductive elastomers used in EMI shielding, thermal interface materials, and flexible circuits. Government-backed investments exceeding USD 15 billion in semiconductor and electronic materials development have accelerated innovation in silicone-based conductive compounds. Additionally, China’s automotive sector, which manufactured over 26 million vehicles annually, increasingly integrates conductive silicone in EV battery management systems and sensors. The country also leads in consumer electronics adoption, accounting for nearly 35% of global smartphone production, reinforcing demand for miniaturized, high-efficiency conductive materials.

Market Size & Growth: Valued at USD 3489 Million in 2025 and projected to reach USD 4848.89 Million by 2033, expanding at 4.2% CAGR due to increasing integration in advanced electronics and EV components.

Top Growth Drivers: Electronics miniaturization adoption rising by 28%, EV component demand increasing by 32%, and EMI shielding efficiency improvements of 25%.

Short-Term Forecast: By 2028, material efficiency and cost optimization in conductive silicone manufacturing are expected to improve production yield by 18%.

Emerging Technologies: Integration of graphene-enhanced conductive silicone, silver-coated particle fillers, and AI-driven material formulation technologies.

Regional Leaders: Asia-Pacific projected to reach USD 2100 Million by 2033 with strong electronics manufacturing; North America expected at USD 1300 Million driven by aerospace demand; Europe estimated at USD 1100 Million with growth in EV adoption.

Consumer/End-User Trends: Increasing usage across automotive electronics, healthcare devices, and telecommunications infrastructure with rising preference for lightweight and flexible materials.

Pilot or Case Example: In 2024, a Japanese electronics manufacturer improved EMI shielding efficiency by 22% using hybrid conductive silicone materials in compact devices.

Competitive Landscape: Market leader holds approximately 18% share, followed by major players such as Dow, Wacker Chemie, Shin-Etsu Chemical, Momentive Performance Materials, and Elkem.

Regulatory & ESG Impact: Increasing compliance with RoHS and REACH standards, with manufacturers targeting 30% reduction in hazardous material usage by 2030.

Investment & Funding Patterns: Over USD 2 billion invested globally in advanced silicone materials and electronic-grade elastomers, with growing venture funding in nanomaterial integration.

Innovation & Future Outlook: Expansion of smart conductive polymers, integration with flexible electronics, and development of high-temperature resistant silicone compounds shaping future market trajectory.

The conductive silicone market demonstrates strong integration across key industry verticals, with electronics contributing nearly 40% of total demand, followed by automotive applications at approximately 25%, and healthcare devices accounting for around 15%. Recent innovations include the development of nano-silver infused silicone materials that enhance conductivity by over 20% while maintaining flexibility. Regulatory frameworks emphasizing environmental safety and reduced toxicity are driving manufacturers to adopt low-VOC and recyclable silicone compounds. Regionally, Asia-Pacific leads consumption due to large-scale electronics production, while North America shows strong growth in aerospace-grade applications. Emerging trends such as flexible wearable electronics, 5G infrastructure expansion, and smart automotive systems are expected to significantly influence future demand patterns, positioning conductive silicone as a critical material in next-generation electronic ecosystems.

The conductive silicone market holds significant strategic relevance as industries increasingly prioritize high-performance materials capable of ensuring electrical conductivity, thermal stability, and environmental resistance. With rapid advancements in electronics, automotive electrification, and telecommunications infrastructure, conductive silicone is becoming an essential component in ensuring operational reliability and product longevity. Advanced conductive fillers such as graphene-enhanced silicone deliver nearly 35% improvement in conductivity compared to traditional carbon-based compounds, enabling higher efficiency in compact electronic designs.

From a regional perspective, Asia-Pacific dominates in volume due to large-scale electronics manufacturing, while North America leads in adoption with over 45% of enterprises integrating advanced conductive materials into aerospace and defense applications. The growing shift toward smart devices and electric vehicles is further strengthening the market’s strategic importance. By 2028, AI-driven material design and predictive formulation technologies are expected to improve product performance efficiency by nearly 20%, reducing defects and enhancing lifecycle durability.

Sustainability and compliance are becoming central to market strategies, with firms committing to environmental targets such as achieving 30% reduction in carbon emissions and increasing recyclable material usage by 2030. In 2024, a South Korean electronics manufacturer achieved a 17% reduction in device overheating issues through the adoption of advanced thermal conductive silicone solutions, demonstrating measurable operational improvements. As industries continue to demand lightweight, durable, and high-performance materials, the conductive silicone market is evolving into a critical enabler of innovation. Its role in supporting energy-efficient systems, regulatory compliance, and sustainable manufacturing positions it as a foundational pillar for long-term industrial resilience and technological advancement.

The rapid expansion of the global electronics industry is a primary driver of the conductive silicone market, particularly with the growing demand for compact, high-performance devices. Conductive silicone materials are widely used in EMI shielding, thermal management, and flexible circuitry, all of which are critical for modern electronic systems. The global production of smartphones alone exceeds 1.3 billion units annually, with a significant proportion requiring advanced shielding materials to ensure signal integrity. Additionally, the rise of 5G infrastructure has increased the need for materials capable of handling higher frequencies and minimizing interference. Conductive silicone offers up to 25% better thermal stability compared to conventional elastomers, making it suitable for high-density electronic assemblies. As industries continue to prioritize performance optimization and device miniaturization, the reliance on conductive silicone is expected to grow steadily.

One of the major restraints in the conductive silicone market is the high cost associated with raw materials and complex manufacturing processes. Conductive fillers such as silver, nickel, and specialized carbon compounds significantly increase production expenses, making the final products less accessible for cost-sensitive applications. Silver-based conductive silicone, for instance, can cost up to 40% more than conventional silicone materials due to the high price of precious metals. Additionally, maintaining uniform dispersion of conductive particles within silicone matrices requires advanced processing technologies, which further adds to operational complexity and costs. These factors can limit adoption, particularly in industries with tight cost constraints. Furthermore, fluctuations in raw material prices and supply chain disruptions can create pricing instability, posing challenges for manufacturers aiming to maintain competitive pricing while ensuring product quality and performance.

The accelerating adoption of electric vehicles presents significant growth opportunities for the conductive silicone market, particularly in battery management systems, power electronics, and charging infrastructure. Modern EVs require advanced materials that can provide both electrical conductivity and thermal management to ensure safety and efficiency. Conductive silicone materials are increasingly used in battery packs to enhance heat dissipation and prevent thermal runaway. Global EV production surpassed 14 million units annually, with a growing percentage incorporating advanced conductive materials in critical components. Additionally, the expansion of EV charging networks has created demand for durable and weather-resistant conductive materials. Innovations such as hybrid conductive fillers and high-temperature resistant silicone compounds are further expanding application possibilities, enabling manufacturers to address evolving industry requirements and capitalize on the growing electrification trend.

Stringent environmental and safety regulations present a significant challenge for the conductive silicone market, particularly concerning the use of hazardous materials and waste management practices. Regulatory frameworks such as restrictions on hazardous substances require manufacturers to limit or eliminate the use of certain conductive fillers, which can impact product performance and increase development costs. Compliance with these regulations often necessitates extensive testing and certification processes, adding to time-to-market and operational expenses. Additionally, the push for sustainable manufacturing has led to increased scrutiny on the environmental impact of silicone production and disposal. Manufacturers are required to invest in eco-friendly alternatives and recycling initiatives, which can be both technically challenging and cost-intensive. Balancing regulatory compliance with performance requirements remains a critical challenge for industry participants seeking to maintain competitiveness in a rapidly evolving market landscape.

• Rapid Growth in Flexible Electronics Integration (Over 35% Device Adoption Increase):

Flexible electronics are significantly transforming the conductive silicone market, with over 35% of new consumer electronic devices now incorporating flexible components requiring conductive elastomers. Conductive silicone materials are increasingly used in wearable devices, foldable smartphones, and medical monitoring systems due to their ability to maintain conductivity under mechanical stress. In high-performance applications, these materials demonstrate up to 28% higher durability compared to rigid conductive alternatives. Asia-Pacific leads this trend, with more than 40% of flexible device production concentrated in the region, driving continuous innovation in silicone-based conductive formulations.

• Expansion of Electric Vehicle Applications (Battery System Usage Up by 30%):

The adoption of conductive silicone in electric vehicle systems has increased by approximately 30%, particularly in battery management systems and thermal interface solutions. These materials enable up to 25% improvement in heat dissipation efficiency, reducing the risk of thermal runaway in lithium-ion batteries. Automotive manufacturers are increasingly deploying conductive silicone in connectors, sensors, and control units, with over 45% of new EV models integrating advanced silicone-based conductive components. This trend is further supported by the global shift toward electrification and the need for lightweight, high-performance materials.

• Advancements in EMI Shielding Efficiency (Performance Gains Exceed 22%):

Electromagnetic interference shielding remains a critical application area, with conductive silicone delivering performance improvements exceeding 22% compared to traditional shielding materials. Approximately 60% of high-frequency electronic systems now rely on advanced shielding solutions to ensure signal integrity. The integration of silver-coated and hybrid fillers has enhanced conductivity levels by nearly 20%, making these materials suitable for 5G infrastructure and aerospace electronics. North America and Europe are witnessing increased deployment, particularly in defense and telecommunications sectors where reliability is paramount.

• Increased Adoption of Sustainable and Low-VOC Materials (Eco-Compliant Products Rise by 27%):

Environmental considerations are driving the development of sustainable conductive silicone solutions, with eco-compliant product adoption rising by 27%. Manufacturers are focusing on reducing volatile organic compound emissions and incorporating recyclable materials into their formulations. Nearly 50% of new product developments now prioritize environmental compliance, aligning with global regulatory requirements. Additionally, advanced production techniques have reduced material waste by up to 18%, enhancing sustainability while maintaining performance standards. This trend is particularly prominent in Europe, where strict environmental regulations are influencing product innovation and market strategies.

The conductive silicone market is segmented based on type, application, and end-user, each contributing uniquely to overall industry dynamics. By type, electrically conductive silicone dominates due to its extensive use in EMI shielding and circuit integration, while thermally conductive variants are gaining traction in heat management applications. From an application perspective, electronics remains the primary segment, accounting for over 40% of total usage, followed by automotive and healthcare sectors. In terms of end-users, consumer electronics manufacturers represent a substantial share, driven by high production volumes and demand for compact, efficient components. Automotive OEMs and healthcare device manufacturers are emerging as high-growth segments, supported by increasing adoption of electric vehicles and wearable medical technologies. The segmentation landscape reflects a strong alignment with technological advancements and evolving industrial requirements, enabling targeted innovation and strategic market positioning.

Electrically conductive silicone holds the leading position in the market, accounting for approximately 48% of total adoption due to its critical role in EMI shielding and electrical connectivity in compact electronic systems. In comparison, thermally conductive silicone accounts for around 32%, primarily driven by its application in heat dissipation for high-performance electronics and battery systems. However, thermally conductive silicone is the fastest-growing segment, expanding at an estimated CAGR of 5.1%, supported by increasing demand from electric vehicles and high-density electronic assemblies where efficient thermal management is essential.

Other types, including hybrid conductive silicone and pressure-sensitive conductive adhesives, collectively contribute nearly 20% of the market. These materials are gaining niche relevance in specialized applications such as aerospace electronics and medical devices, where both electrical and mechanical performance are critical. Hybrid variants, in particular, are witnessing increased adoption due to their ability to combine conductivity with enhanced flexibility.

Electronics remains the dominant application segment, accounting for approximately 42% of total conductive silicone usage, driven by the increasing complexity and miniaturization of electronic devices. Automotive applications follow with around 28%, largely due to the integration of conductive silicone in electric vehicle components, sensors, and control systems. However, healthcare applications are emerging as the fastest-growing segment, expanding at an estimated CAGR of 5.6%, supported by the rising adoption of wearable medical devices and diagnostic equipment requiring flexible and biocompatible conductive materials.

Other applications, including telecommunications and aerospace, collectively contribute nearly 30% of the market. These sectors rely on conductive silicone for high-frequency signal transmission and robust environmental resistance. The expansion of 5G infrastructure has further accelerated demand in telecommunications, where materials must ensure consistent performance under high-frequency conditions.

Consumer electronics manufacturers represent the leading end-user segment, accounting for approximately 45% of the conductive silicone market, driven by high production volumes of smartphones, wearables, and computing devices. Automotive OEMs follow with around 30%, reflecting the increasing integration of conductive silicone in electric vehicles and advanced driver-assistance systems. However, the healthcare sector is the fastest-growing end-user segment, expanding at an estimated CAGR of 5.8%, fueled by the growing demand for smart medical devices and continuous health monitoring technologies.

Other end-users, including aerospace, defense, and industrial equipment manufacturers, collectively contribute nearly 25% of the market. These sectors require high-reliability materials capable of withstanding extreme environmental conditions and ensuring consistent performance. Adoption rates in aerospace applications have increased by over 18%, particularly in avionics and satellite communication systems.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2026 and 2033.

Asia-Pacific’s dominance is supported by its extensive electronics manufacturing output, producing over 60% of global consumer electronics, which significantly drives conductive silicone demand. China alone contributes more than 35% of regional consumption, followed by Japan and South Korea with a combined 18%. North America holds approximately 24% market share, with strong adoption in aerospace and defense applications, while Europe accounts for nearly 20%, driven by automotive electrification and regulatory compliance. South America and the Middle East & Africa collectively represent around 10%, with increasing demand from energy and infrastructure sectors. Across all regions, over 70% of conductive silicone demand is concentrated in electronics and automotive applications, highlighting the material’s critical role in modern industrial ecosystems.

How are high-performance electronics and aerospace innovation shaping advanced material demand?

North America accounts for approximately 24% of the global conductive silicone market, driven by strong demand from aerospace, defense, and healthcare sectors. The region produces over 25% of the world’s aerospace components, creating consistent demand for EMI shielding and thermal interface materials. Government regulations emphasizing product safety and environmental compliance have accelerated the adoption of low-VOC conductive silicone solutions, with over 65% of manufacturers aligning with updated compliance frameworks. Technological advancements such as AI-driven material design and precision manufacturing have improved product efficiency by nearly 18%. A notable regional player, Dow, has expanded its advanced silicone production capacity by over 12% to support growing demand in high-reliability applications. Consumer behavior in this region reflects high enterprise adoption, particularly in healthcare and finance sectors, where over 40% of companies integrate advanced materials into mission-critical systems.

What role do sustainability regulations and EV innovation play in shaping material demand?

Europe holds around 20% of the conductive silicone market, with key contributions from Germany, the UK, and France. Germany alone accounts for nearly 30% of the region’s automotive production, significantly influencing demand for conductive silicone in EV systems and sensors. Regulatory frameworks such as REACH and RoHS have led to a 28% increase in demand for eco-friendly and low-toxicity silicone materials. The region has also witnessed a 22% rise in the adoption of advanced conductive compounds in renewable energy systems. Companies such as Wacker Chemie are investing heavily in sustainable silicone production, increasing output efficiency by 15% through energy-optimized manufacturing processes. European consumer behavior is strongly influenced by regulatory compliance, with over 50% of enterprises prioritizing environmentally sustainable materials in procurement decisions.

Why is rapid industrialization accelerating advanced material adoption across manufacturing ecosystems?

Asia-Pacific dominates the conductive silicone market with over 46% share, supported by high-volume manufacturing in China, India, and Japan. China leads regional consumption with more than 35%, followed by Japan at 12% and India at 9%. The region produces over 60% of global electronics, making it the largest consumer of conductive silicone materials for applications such as circuit protection and thermal management. Rapid infrastructure development and industrial expansion have increased demand for advanced materials by approximately 30% over the past five years. Shin-Etsu Chemical, a key regional player, has enhanced its silicone production capacity by 10% to meet rising demand in semiconductor and automotive industries. Consumer behavior in this region is driven by large-scale production and cost efficiency, with over 55% of manufacturers prioritizing high-performance yet affordable material solutions.

How are infrastructure expansion and energy investments influencing advanced material demand?

South America represents nearly 6% of the global conductive silicone market, with Brazil and Argentina being the primary contributors. Brazil accounts for over 50% of the regional demand, largely due to its expanding automotive and energy sectors. Infrastructure investments have increased by approximately 18%, driving demand for durable and weather-resistant conductive materials. Government incentives supporting renewable energy projects have further boosted adoption, particularly in solar and wind installations. Local manufacturers are focusing on improving supply chain efficiency, with some companies achieving up to 12% reduction in production lead times through digital transformation initiatives. Consumer behavior in this region is closely tied to industrial growth, with increasing demand for cost-effective and durable materials across construction and energy sectors.

What impact do industrial diversification and energy sector growth have on material adoption trends?

The Middle East & Africa region accounts for approximately 4% of the global conductive silicone market, with the UAE and South Africa emerging as key growth hubs. The oil and gas sector contributes to over 40% of regional demand, requiring high-performance materials for extreme operating conditions. Infrastructure development projects have increased by 20%, supporting the adoption of conductive silicone in construction and energy applications. Technological modernization initiatives, including smart city projects, have driven a 15% rise in demand for advanced electronic materials. Regional trade partnerships and regulatory frameworks are facilitating easier access to high-quality silicone products. Consumer behavior in this region is influenced by industrial diversification, with growing adoption across energy, construction, and telecommunications sectors.

China Conductive Silicone Market – 35% share: Dominates due to extensive electronics manufacturing capacity and strong integration across automotive and consumer electronics sectors.

United States Conductive Silicone Market – 22% share: Leads with advanced aerospace, defense, and healthcare industries driving high-performance material demand.

The conductive silicone market is moderately fragmented, with over 40 active global and regional competitors operating across various application segments. The top five companies collectively account for approximately 55% of the total market share, indicating a competitive yet somewhat consolidated structure among leading players. Major companies are focusing on strategic initiatives such as product innovation, capacity expansion, and partnerships to strengthen their market position. Over 25% of recent developments involve new product launches featuring advanced conductive fillers and improved thermal properties. Mergers and acquisitions have increased by nearly 18% over the past three years, enabling companies to expand their technological capabilities and geographic reach. Research and development investments have grown by approximately 20%, with a focus on sustainable materials and high-performance applications. Additionally, companies are leveraging digital technologies to optimize production processes, achieving efficiency improvements of up to 15%. The competitive landscape is further shaped by increasing demand for customized solutions, prompting manufacturers to develop application-specific conductive silicone products tailored to industry requirements.

Dow

Wacker Chemie AG

Shin-Etsu Chemical Co., Ltd.

Momentive Performance Materials Inc.

Elkem ASA

KCC Corporation

Nusil Technology LLC

Specialty Silicone Products Inc.

MG Chemicals

Henkel AG & Co. KGaA

Technological advancements in the conductive silicone market are centered around improving electrical conductivity, thermal management, and material durability to meet the evolving demands of high-performance industries. One of the most significant innovations is the integration of nano-scale conductive fillers such as silver nanowires, graphene, and carbon nanotubes, which have demonstrated up to 30% improvement in conductivity compared to conventional metal particle fillers. These advanced fillers also enhance flexibility, enabling conductive silicone to maintain stable performance even after more than 10,000 bending cycles in flexible electronics applications.

In thermal management, hybrid conductive silicone formulations are gaining traction, offering up to 25% higher heat dissipation efficiency in comparison to traditional silicone elastomers. This is particularly critical in electric vehicles and high-density semiconductor devices, where effective thermal regulation directly impacts system reliability. Additionally, the development of electrically conductive adhesives (ECAs) has enabled more efficient assembly processes, reducing component failure rates by approximately 15% in microelectronic packaging.

Digital transformation is also influencing the market, with AI-driven material design platforms enabling faster formulation cycles and improving product consistency by nearly 20%. Automation in manufacturing processes, including precision mixing and dispersion technologies, has reduced material waste by up to 18%, enhancing production efficiency. Furthermore, advancements in low-VOC and recyclable silicone compounds are aligning with environmental regulations, with over 40% of new product innovations focusing on sustainability. These technologies collectively position conductive silicone as a critical material in next-generation electronics, automotive systems, and smart infrastructure.

• In March 2025, Dow expanded its SILASTIC™ electrically conductive silicone portfolio with new grades designed for electric vehicle battery systems, offering improved thermal conductivity and up to 20% better EMI shielding performance. The development supports next-generation EV architectures requiring enhanced safety and efficiency. Source: www.dow.com

• In September 2024, Wacker Chemie AG introduced a new line of ELASTOSIL® conductive silicone rubber grades optimized for high-frequency 5G applications. These materials demonstrated up to 18% improved signal shielding efficiency and enhanced durability for telecommunications infrastructure deployments. Source: www.wacker.com

• In November 2024, Shin-Etsu Chemical Co., Ltd. announced the expansion of its silicone production facilities in Japan to increase output of conductive silicone materials by approximately 10%, addressing rising demand from semiconductor and automotive electronics sectors. Source: www.shinetsu.co.jp

• In February 2025, Momentive Performance Materials launched advanced thermally conductive silicone compounds for high-performance electronics, achieving up to 22% improvement in heat dissipation efficiency. These materials are targeted at data centers and power electronics requiring enhanced thermal management. Source: www.momentive.com

The scope of the conductive silicone market report encompasses a comprehensive evaluation of material types, applications, end-user industries, regional dynamics, and technological advancements shaping the industry landscape. The report covers key product categories including electrically conductive silicone, thermally conductive silicone, and hybrid variants, which collectively account for over 80% of total market utilization. It further analyzes application segments such as electronics, automotive, healthcare, telecommunications, and aerospace, with electronics alone contributing more than 40% of overall demand.

Geographically, the report provides detailed insights across major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, capturing variations in production volumes, consumption patterns, and industrial adoption. Asia-Pacific leads with over 45% of global consumption, while North America and Europe together account for nearly 44%, driven by advanced manufacturing and regulatory compliance requirements.

The report also explores emerging segments such as flexible electronics, wearable medical devices, and electric vehicle battery systems, which are witnessing adoption increases exceeding 25% across multiple industries. Additionally, it evaluates technological innovations including nano-filler integration, AI-driven material development, and sustainable silicone formulations, which are influencing product performance and environmental compliance.

Industry focus areas include supply chain dynamics, raw material trends, manufacturing technologies, and competitive strategies adopted by key players. The report highlights the increasing role of conductive silicone in enabling high-efficiency electronic systems, with over 70% of applications requiring enhanced thermal and electrical performance. This broad analytical scope ensures that decision-makers gain a detailed understanding of market structure, operational trends, and future growth avenues.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Dow, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials Inc., Elkem ASA, KCC Corporation, Nusil Technology LLC, Specialty Silicone Products Inc., MG Chemicals, Henkel AG & Co. KGaA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |