Reports

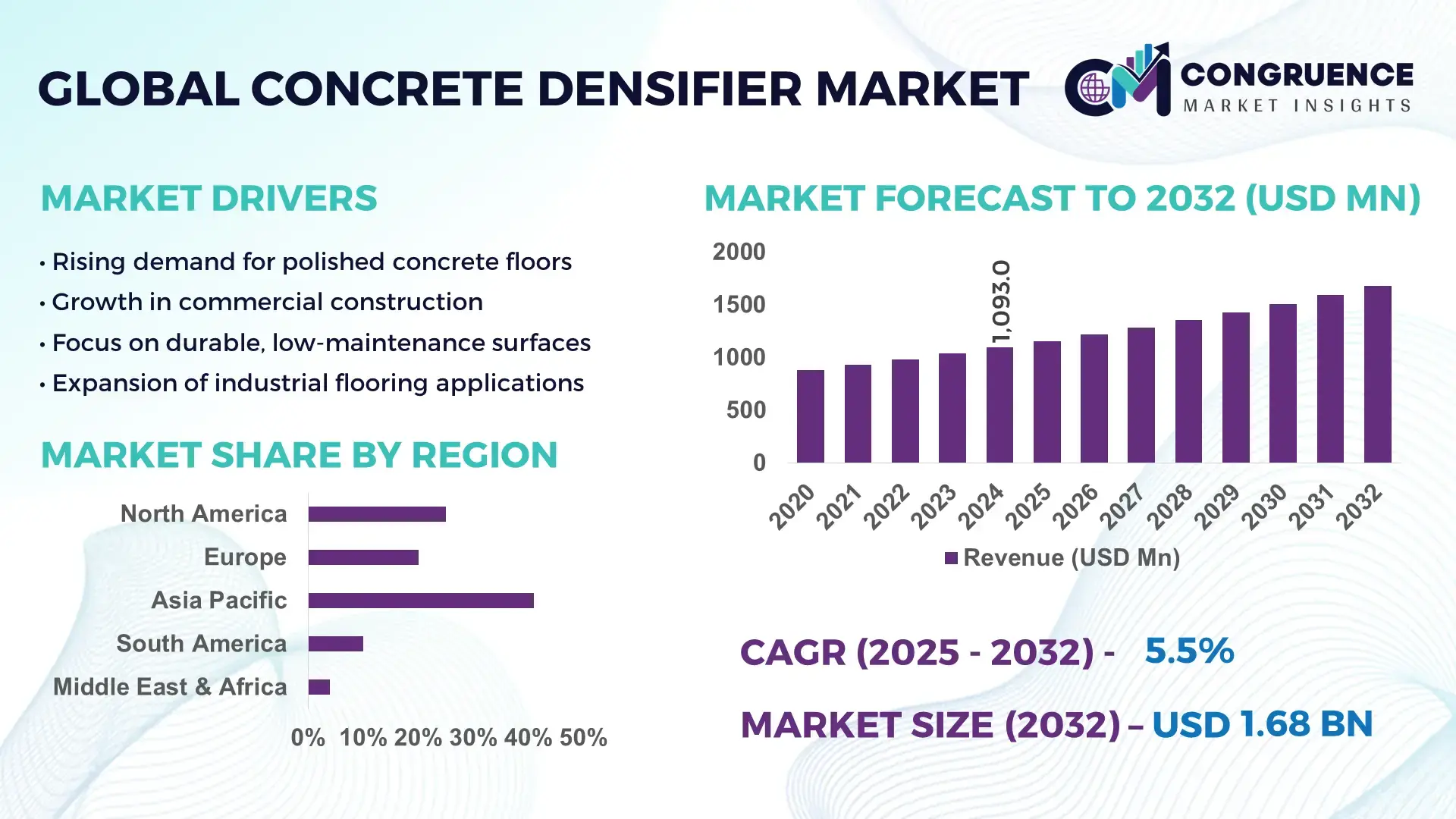

The Global Concrete Densifier Market was valued at USD 1092.98 Million in 2024 and is anticipated to reach a value of USD 1677.38 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032. Growth is supported by rising demand for durable, low-maintenance industrial flooring and increased adoption of sustainable construction materials.

China represents the dominant national market for concrete densifiers, supported by large-scale domestic production capacity and sustained infrastructure investment. The country produced over 2.6 billion metric tons of cement in 2024, enabling extensive downstream consumption of concrete treatment solutions across logistics hubs, manufacturing parks, airports, and urban transit projects. Annual infrastructure investment exceeded USD 1.6 trillion, with densifier-treated floors increasingly specified in industrial zones and data centers. Technological advancements include widespread use of lithium- and nano-silicate densifiers, automation-enabled polishing systems, and smart curing controls, improving abrasion resistance by over 30% and extending floor service life beyond 20 years in high-load applications.

Market Size & Growth: Valued at USD 1092.98 Million in 2024, projected to reach USD 1677.38 Million by 2032, growing at a CAGR of 5.5%, driven by increased industrial flooring upgrades and lifecycle cost optimization.

Top Growth Drivers: Industrial flooring adoption growth at 42%, surface durability improvement of 35%, maintenance cost reduction of 28%.

Short-Term Forecast: By 2028, industrial facility flooring costs are expected to decline by 18% due to extended resurfacing cycles and reduced downtime.

Emerging Technologies: Lithium-silicate densifiers, nano-silica penetration technology, and automated floor polishing systems.

Regional Leaders: Asia Pacific projected at USD 720 Million by 2032 with logistics park adoption; North America at USD 430 Million driven by warehouse retrofits; Europe at USD 310 Million supported by green building compliance.

Consumer/End-User Trends: High adoption among logistics operators, automotive plants, data centers, and food processing facilities prioritizing dust-proof and chemical-resistant floors.

Pilot or Case Example: In 2024, a large logistics hub retrofit project achieved a 25% reduction in floor maintenance downtime using lithium-based densifiers.

Competitive Landscape: Market leader holds approximately 18% share, followed by 3–5 established multinational and regional specialty chemical manufacturers.

Regulatory & ESG Impact: Green building certifications and low-VOC material mandates accelerating adoption in commercial and public infrastructure projects.

Investment & Funding Patterns: Over USD 480 Million invested recently in industrial flooring upgrades, with increased use of long-term facility performance contracts.

Innovation & Future Outlook: Integration of densifiers with polished concrete systems, smart surface monitoring, and low-carbon formulations shaping future demand.

The concrete densifier market serves key industry sectors including industrial manufacturing, warehousing and logistics, commercial real estate, transportation infrastructure, and institutional buildings, with industrial and logistics facilities contributing over half of total consumption. Recent innovations focus on lithium- and nano-silicate formulations that enhance penetration depth, reduce curing time by up to 40%, and improve surface hardness. Regulatory emphasis on sustainable construction and reduced particulate emissions supports adoption, while economic growth in Asia Pacific drives volume demand. Consumption patterns show higher per-square-meter usage in heavy-load facilities, with future outlook centered on smart flooring systems, carbon-efficient materials, and increased specification in large-scale infrastructure projects.

The strategic relevance of the Concrete Densifier Market lies in its direct contribution to extending concrete lifecycle performance, lowering operational expenditure, and supporting compliance with sustainability-led construction mandates. Concrete densifiers are increasingly positioned as a value-added surface engineering solution rather than a post-construction add-on, with measurable impacts on abrasion resistance, dust suppression, and load-bearing efficiency. Lithium-silicate densifier technology delivers approximately 30% higher surface hardness improvement compared to traditional sodium-silicate standards, enabling faster curing cycles and reduced floor downtime in industrial settings. Asia Pacific dominates in volume consumption due to extensive industrial and logistics infrastructure, while North America leads in adoption intensity, with nearly 62% of large warehouse operators integrating densifier-treated flooring into facility standards. By 2028, AI-enabled surface assessment and automated polishing technologies are expected to cut floor maintenance downtime by 20% through predictive wear monitoring and optimized reapplication cycles. From an ESG perspective, firms are committing to embodied carbon and waste reduction targets, with concrete floor retrofitting programs supporting up to 25% material reuse and lower demolition waste by 2030. In 2024, a major industrial facility operator in the United States achieved a 22% reduction in annual floor maintenance costs through the deployment of lithium-based densifiers combined with automated polishing systems. Looking ahead, the Concrete Densifier Market is positioned as a pillar of operational resilience, regulatory alignment, and sustainable growth, supporting long-term infrastructure performance across industrial, commercial, and institutional assets.

The rising demand for durable industrial flooring is a primary driver of growth in the Concrete Densifier Market, particularly across logistics, manufacturing, and warehousing sectors. Modern industrial facilities experience continuous forklift movement, heavy static loads, and chemical exposure, conditions that accelerate untreated concrete wear. Concrete densifiers improve surface hardness by 20–35%, significantly reducing dusting and surface spalling. Large distribution centers increasingly specify densifier-treated floors to minimize maintenance shutdowns and enhance workplace safety. In high-throughput logistics facilities, treated concrete floors have demonstrated service life extensions exceeding 15 years. As industrial floor areas continue to expand globally, densifiers are being adopted as a standard performance-enhancing solution rather than a discretionary upgrade.

Application complexity and performance variability act as notable restraints on the Concrete Densifier Market. Densifier effectiveness depends heavily on concrete composition, surface porosity, curing conditions, and installer expertise. Improper application can reduce penetration efficiency by more than 25%, leading to inconsistent results and client dissatisfaction. In regions with limited access to skilled applicators or standardized surface preparation practices, adoption remains uneven. Additionally, older sodium- and potassium-based densifiers may require multiple applications and extended curing times, increasing labor requirements. These factors can deter small and mid-sized contractors from specifying densifiers, particularly in cost-sensitive construction projects.

Infrastructure retrofitting and sustainability-driven construction present substantial opportunities for the Concrete Densifier Market. Aging industrial floors in warehouses, factories, and public buildings are increasingly refurbished rather than replaced, creating demand for surface-hardening solutions that extend usable life. Concrete densifiers support sustainability goals by reducing the need for new concrete pours, lowering material consumption, and minimizing demolition waste. In green building projects, densifier-treated polished concrete floors are favored for their low VOC emissions and reduced maintenance inputs. Emerging opportunities also exist in transportation infrastructure, where densifiers improve abrasion resistance in terminals and parking structures exposed to high mechanical stress.

Cost pressures and regulatory compliance complexities represent ongoing challenges for the Concrete Densifier Market. Advanced lithium- and nano-silicate formulations carry higher upfront material costs, which can discourage adoption in price-sensitive projects despite long-term savings. Additionally, varying regional regulations related to chemical composition, worker safety, and environmental impact increase compliance complexity for manufacturers and applicators. Meeting low-VOC and environmental labeling requirements often necessitates reformulation and additional testing, raising development costs. These challenges require suppliers to balance performance innovation with affordability and regulatory alignment to sustain long-term market momentum.

• Expansion of Modular and Prefabricated Construction Driving Standardized Densifier Use: The rapid shift toward modular and prefabricated construction is reshaping demand dynamics in the Concrete Densifier market, as factory-controlled environments require uniform surface performance. Around 55% of new commercial and industrial projects using modular practices reported measurable cost efficiencies and schedule compression. Pre-cast slabs treated with densifiers before installation demonstrate up to 30% higher surface hardness consistency compared to on-site applications. Europe and North America together account for nearly 60% of modular floor deployments, where densifier-treated panels reduce post-installation polishing time by approximately 25%.

• Rising Adoption of Lithium- and Nano-Silicate Formulations in Industrial Flooring: Advanced lithium- and nano-silicate densifiers are increasingly replacing older sodium-based products due to superior penetration and faster reaction times. These formulations improve abrasion resistance by 28–35% and reduce curing windows by nearly 40%, enabling faster commissioning of facilities. In high-load environments such as logistics hubs and manufacturing plants, over 65% of newly specified densifiers now fall under lithium-based categories. The trend is particularly visible in large-scale warehouses exceeding 50,000 square meters, where performance uniformity is critical.

• Integration of Automated Polishing and Smart Application Technologies: Automation is becoming a defining trend in the Concrete Densifier market, with robotic polishing and sensor-assisted application systems gaining traction. Automated systems can improve application uniformity by 20% and reduce labor dependency by nearly 30%. In technologically advanced construction markets, roughly 45% of large flooring contractors have adopted semi-automated densifier application workflows. Smart monitoring tools also enable predictive maintenance scheduling, lowering unexpected surface repairs by approximately 18% over a three-year operational period.

• Increased Specification of Densifier-Treated Floors in Sustainability-Oriented Projects: Sustainability-focused construction is accelerating the specification of densifier-treated polished concrete floors as alternatives to coatings and coverings. Densifier-treated surfaces can reduce lifecycle maintenance material use by up to 32% and lower dust-related particulate emissions by nearly 40%. In institutional and commercial buildings targeting green certifications, polished concrete with densifiers is now selected in over 50% of large-floor-area projects. This trend supports long-term durability goals while aligning with stricter low-VOC and waste-reduction requirements.

The Concrete Densifier market segmentation reflects varied performance requirements, usage intensity, and procurement behavior across construction ecosystems. Segmentation by type highlights the dominance of advanced silicate chemistries designed for high-load and long-life concrete surfaces. Application-based segmentation shows strong concentration in industrial and logistics flooring, followed by commercial and institutional infrastructure where durability and dust suppression are operational priorities. End-user segmentation further clarifies demand concentration among industrial facility operators and large contractors, while public infrastructure agencies and commercial property owners represent steady secondary demand. Across all segments, adoption is influenced by surface lifecycle expectations, compliance with low-dust and low-maintenance standards, and increasing preference for retrofit solutions over replacement. Segmentation insights indicate a shift from traditional, commodity-grade treatments toward performance-driven densifiers aligned with automation, sustainability, and long-term asset management strategies.

Lithium silicate densifiers represent the leading product type in the Concrete Densifier market, accounting for approximately 48% of total adoption due to superior penetration, rapid reaction with calcium hydroxide, and reduced efflorescence risk. Sodium silicate densifiers currently hold around 22% adoption, while potassium silicate products account for nearly 15%. However, nano-silicate densifiers are emerging as the fastest-growing type, expanding at an estimated CAGR of 7.8%, driven by their ability to enhance micro-surface density and improve abrasion resistance by over 35% in high-traffic environments. These advanced formulations are increasingly specified in data centers, automated warehouses, and clean manufacturing units. The remaining product types, including blended and hybrid silicate formulations, together contribute roughly 15% of the market, serving niche retrofit and cost-sensitive projects.

Industrial flooring is the leading application segment in the Concrete Densifier market, accounting for nearly 46% of total usage, supported by extensive deployment in warehouses, factories, and logistics hubs where surface wear directly affects operational uptime. Commercial buildings follow with approximately 24% adoption, while institutional and infrastructure applications together represent around 18%. Parking structures and transportation facilities make up the remaining 12%. Although industrial flooring dominates overall use, transportation infrastructure applications are expanding at the fastest pace, with an estimated CAGR of 6.9%, driven by high abrasion loads and extended operating hours in airports and transit terminals. Other applications collectively contribute 30% of demand, reflecting diversified usage across retail, healthcare, and public buildings.

Industrial facility operators constitute the largest end-user segment, representing approximately 44% of total Concrete Densifier consumption, reflecting their focus on minimizing dust, improving safety, and extending floor service life. Commercial property owners account for around 26%, while public infrastructure agencies contribute nearly 17%. Contractors and flooring service providers together represent the remaining 13%. Among these, data center operators and large logistics providers are the fastest-growing end-user group, with adoption increasing at an estimated CAGR of 7.2%, driven by high floor load density and zero-downtime requirements. Other end-users collectively maintain steady demand, with adoption rates exceeding 55% in new-build industrial projects and nearly 40% in large-scale renovation programs.

Asia-Pacific accounted for the largest market share at 41.6% in 2024 however, the Region Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2025 and 2032.

Asia-Pacific is followed by North America with a 27.4% share and Europe at 21.1%, while South America and the Middle East & Africa together account for nearly 9.9% of global demand. Growth patterns vary significantly by region, driven by infrastructure spending, industrial floor area expansion, sustainability mandates, and retrofitting intensity. Asia-Pacific leads in absolute consumption volume due to large-scale industrial and logistics construction exceeding 1.2 billion square meters annually. North America shows higher densifier penetration per square meter, with adoption rates above 65% in new industrial flooring projects. Europe demonstrates strong specification-driven demand linked to regulatory and ESG compliance, while emerging regions show increasing uptake tied to transport infrastructure and energy projects.

How is performance-driven flooring reshaping industrial surface treatment adoption?

The market holds approximately 27.4% share of global Concrete Densifier demand, supported by extensive warehousing, data center expansion, and manufacturing modernization. Logistics, automotive, food processing, and healthcare facilities are primary demand generators, with over 70% of newly built warehouses specifying densifier-treated floors. Regulatory focus on low-dust workplaces and low-VOC construction materials is strengthening adoption. Digital transformation is evident through automated polishing, laser-guided surface leveling, and smart maintenance planning, improving floor lifecycle efficiency by nearly 20%. A leading regional flooring solutions provider expanded lithium-silicate densifier production capacity by over 15% in 2024 to meet retrofit demand. Consumer behavior shows higher enterprise adoption in logistics and healthcare facilities, where uptime and hygiene compliance are critical.

How are sustainability mandates accelerating advanced surface treatment adoption?

Europe accounts for around 21.1% of the Concrete Densifier market, with Germany, the UK, and France contributing more than 60% of regional demand. Strict sustainability frameworks, green building certifications, and circular construction initiatives are central growth enablers. Over 55% of large commercial flooring projects now specify polished concrete with densifiers to meet environmental compliance benchmarks. Emerging technologies such as nano-silicate formulations and low-alkali products are gaining traction to align with worker safety and emissions standards. A major European construction materials company introduced next-generation densifiers aimed at reducing curing time by 35%. Consumer behavior reflects strong regulatory-driven purchasing, with buyers prioritizing compliance, transparency, and long-term performance validation.

Why is large-scale infrastructure development transforming surface hardening demand?

This region leads the market in volume, representing 41.6% of global Concrete Densifier consumption. China, India, and Japan are the top consuming countries, together accounting for over 70% of regional usage. Massive investments in industrial parks, logistics corridors, airports, and metro systems are driving demand, with annual new industrial floor construction exceeding 700 million square meters. Manufacturing automation and e-commerce fulfillment centers are accelerating densifier adoption. Regional innovation hubs are promoting lithium- and hybrid-silicate technologies tailored for high-humidity and high-load environments. A prominent Asian construction chemical manufacturer expanded its densifier portfolio to serve smart factory projects. Consumer behavior is driven by cost efficiency, scale, and rapid project execution.

How are infrastructure renewal and industrial upgrades shaping surface treatment needs?

South America holds nearly 5.2% of global Concrete Densifier demand, led by Brazil and Argentina. Infrastructure rehabilitation, port modernization, and industrial facility upgrades are key demand drivers. Brazil alone accounts for over 45% of regional consumption due to large logistics and agribusiness storage facilities. Government-backed infrastructure programs and favorable trade policies are supporting industrial construction activity. Local producers are increasingly focusing on potassium- and blended-silicate densifiers to balance performance and affordability. Consumer behavior in the region is highly price-sensitive, with demand linked closely to infrastructure funding cycles and export-oriented industrial growth.

How is mega construction and energy-sector investment influencing surface durability requirements?

The Middle East & Africa region represents approximately 4.7% of the Concrete Densifier market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Large-scale commercial developments, logistics hubs, airports, and oil & gas facilities are major demand centers. Over 60% of densifier usage in the region is tied to new-build projects rather than retrofits. Technological modernization includes adoption of high-penetration lithium densifiers to withstand extreme temperatures and heavy loads. Regional regulations emphasize durability and lifecycle performance for public infrastructure. Consumer behavior favors premium, long-life solutions that reduce maintenance under harsh operating conditions.

China – 24.8% share: Dominance supported by extensive industrial floor construction volume and large-scale infrastructure deployment.

United States – 19.6% share: Leadership driven by high densifier penetration in logistics, manufacturing, and data center flooring projects.

The Concrete Densifier market exhibits a moderately fragmented competitive structure, with an estimated 60–70 active manufacturers and specialty chemical suppliers operating globally. The top five companies together account for approximately 38% of total market presence, indicating room for both multinational leaders and regional specialists. Competition is primarily shaped by product performance differentiation, formulation innovation, geographic reach, and contractor network strength. Leading players focus on lithium- and nano-silicate technologies, which now represent over 60% of newly launched products, reflecting a shift away from legacy sodium- and potassium-based solutions. Strategic initiatives include capacity expansions of 10–20% in high-growth regions, cross-border distribution partnerships, and targeted acquisitions of regional flooring solution providers to strengthen local market access. Product launches increasingly emphasize low-alkali content, faster curing cycles reduced by up to 40%, and enhanced abrasion resistance exceeding 30%. Digital engagement with contractors, including application training platforms and performance monitoring tools, is also emerging as a competitive lever. Overall, competition is driven by technical credibility, application reliability, and the ability to align with sustainability and lifecycle cost expectations of industrial and commercial end users.

Sika AG

BASF SE

Mapei S.p.A.

RPM International Inc.

Euclid Chemical Company

Ashford Formula

Prosoco Inc.

LATICRETE International

W. R. Meadows

Solomon Colors Inc.

CTS Cement Manufacturing Corp.

Sika AG

BASF SE

Mapei S.p.A.

The Concrete Densifier market is witnessing significant technological evolution, driven by the need for higher performance, faster installation, and extended service life of concrete surfaces. Lithium-silicate densifiers have emerged as the dominant technology, accounting for approximately 48% of adoption due to their superior penetration and chemical reaction with calcium hydroxide, which increases surface hardness by up to 30% compared to traditional sodium-silicate formulations. Nano-silicate densifiers are rapidly gaining attention, currently representing around 15% of total installations, offering enhanced micro-structural densification, improved abrasion resistance, and reduced curing time by nearly 35%. Hybrid formulations combining lithium and nano-silicate compounds are also being introduced, capturing an additional 12% of market uptake, particularly for industrial floors exposed to high mechanical stress.

Automation and digitalization are reshaping application techniques. Robotic polishing and sensor-assisted application systems now cover approximately 25% of new industrial and commercial floor projects, improving surface uniformity by 20% while reducing labor intensity by 30%. Predictive monitoring technologies, including IoT-based surface condition sensors, are being integrated into maintenance programs, helping facility managers anticipate wear patterns and reduce unplanned downtime by up to 18%. Emerging innovations also focus on environmentally optimized densifiers with low-alkali content and reduced VOC emissions, currently specified in over 40% of green building and sustainability-compliant projects. The integration of smart surface analytics and advanced chemical formulations positions the Concrete Densifier market for continued technological leadership, enabling industrial, commercial, and institutional facilities to achieve long-lasting, high-performance flooring solutions.

• In 2024, Prosoco introduced a VOC‑free nano‑lithium densifier formulation that has been adopted in over 3,700 commercial and industrial projects across North America, enhancing surface hardness and compliance with stringent indoor air quality regulations, and improving application efficiency on polished concrete floors.

• Curecrete Distribution unveiled a comprehensive Environmental Product Declaration (EPD) for densified and polished concrete products in 2024, underscoring measurable reductions in embodied carbon and lifecycle environmental impact for concrete surface treatments used in industrial flooring applications.

• Evonik launched a bio‑based concrete densifier in 2024, derived from agricultural silica waste and scaled to 8,000 metric tons of production for use across Asia, supporting sustainable construction practices while enhancing surface durability.

• AmeriPolish introduced a high‑gloss densifier designed for UV‑exposed environments in 2024, with adoption across 14 major international airport terminals, delivering improved scratch resistance and long‑term aesthetic performance for heavy‑traffic public flooring.

The scope of the Concrete Densifier Market Report encompasses a comprehensive review of product categories, surface treatment formulations, application methodologies, and geographic demand patterns that define the global industry landscape. The report details segmentation across types such as lithium‑silicate, sodium‑silicate, potassium‑silicate, hybrid, and eco‑friendly water‑based densifiers, capturing performance characteristics, penetration behavior, and usage preferences across diverse floor use cases. Volume and adoption metrics are assessed by application environments including industrial warehouse flooring, commercial retail and hospitality spaces, institutional facilities such as hospitals and airports, transportation infrastructure surfaces, and decorative concrete finishes where densifier integration with polishing systems is increasingly specified.

Geographically, the analysis covers major regions—North America, Europe, Asia‑Pacific, South America, and Middle East & Africa—highlighting regional volume metrics and distinct procurement behavior. Technology focus areas include advanced chemical formulations with nano‑enhancement, dual‑function densifier/cure systems, static‑dissipative surface solutions for technical infrastructure, and automated application tools that advance coverage uniformity and project turnaround. The report also explores niche segments such as moisture‑tolerant densifiers for green concrete applications, high‑gloss decorative densifiers for architectural exposure, and static‑controlled treatments for sensitive environments like data centers. Through an industry‑centric lens, the report synthesizes market breadth across end‑user adoption trends, performance specification drivers, regulatory alignment, and innovation pathways, enabling decision‑makers to evaluate current and emerging opportunities in surface hardening technologies that improve durability, reduce lifecycle maintenance, and support sustainability objectives.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 1092.98 Million |

|

Market Revenue in 2032 |

USD 1677.38 Million |

|

CAGR (2025 - 2032) |

5.5% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sika AG, BASF SE, Mapei S.p.A., RPM International Inc., Euclid Chemical Company, Ashford Formula, Prosoco Inc., LATICRETE International, W. R. Meadows, Solomon Colors Inc., CTS Cement Manufacturing Corp., Sika AG, BASF SE, Mapei S.p.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |