Reports

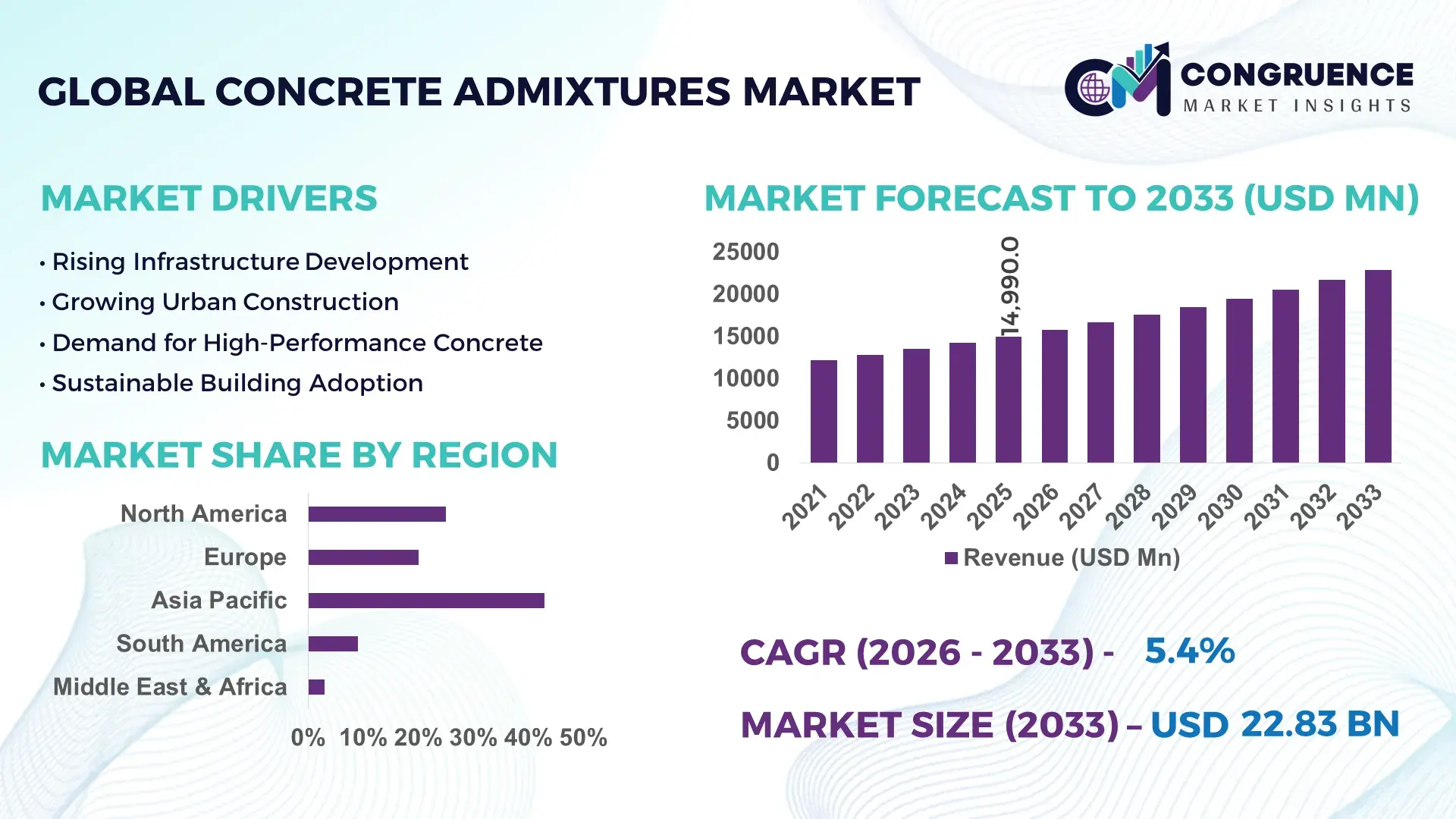

The Global Concrete Admixtures Market was valued at USD 14990 Million in 2025 and is anticipated to reach a value of USD 22831.08 Million by 2033 expanding at a CAGR of 5.4% between 2026 and 2033. Growth is being driven by accelerated adoption of high-performance concrete in transportation infrastructure, urban redevelopment projects, low-carbon construction programs, and increasing use of water-reducing and durability-enhancing admixture technologies across commercial and industrial building applications.

China remains the dominant country, accounting for approximately 31% of global concrete consumption, supported by large-scale rail, energy, and urban infrastructure investments exceeding USD 500 billion in active project pipelines during 2026. Compared with India, where advanced admixture penetration is nearing 38% in organized construction projects, China exceeds 55% adoption in major infrastructure works, while domestic production capacity utilization remains above 80%. Ongoing supply-chain diversification following global trade realignments continues to reinforce regional manufacturing competitiveness.

For industry participants, expanding localized production, performance-focused product portfolios, and infrastructure-linked partnerships remain critical to securing long-term market positioning.

Market Size & Growth: USD 14,990 million in 2025 rising to USD 22,831.08 million by 2033 at 5.4% CAGR, supported by advanced concrete technologies and infrastructure modernization.

Top Growth Drivers: Water reduction efficiency gains of 15%, construction productivity improvements of 12%, and durability enhancement exceeding 20% drive adoption.

Short-Term Forecast: By 2028, project cycle times are projected to decline by 8% while concrete performance consistency improves by 10%.

Emerging Technologies: AI-enabled mix optimization, smart dosing systems, and next-generation polycarboxylate admixtures improve material efficiency by 5–12%.

Regional Leaders: Asia-Pacific surpasses USD 9 billion, Europe exceeds USD 5 billion, and North America approaches USD 4 billion, supported by sustainable construction adoption.

Consumer/End-User Trends: More than 60% of large infrastructure projects specify performance-enhancing admixtures for durability and lifecycle cost reduction.

Pilot/Case Example: A 2026 transportation corridor project achieved 18% lower water usage and 14% faster placement through advanced admixture integration.

Competitive Landscape: Top manufacturers collectively control roughly 40% of global demand, with leading multinational suppliers maintaining extensive regional production networks.

Regulatory & ESG Impact: Low-carbon construction initiatives reduce cement-related emissions by up to 12% through optimized admixture-enabled concrete formulations.

Investment & Funding: Industry expansion and capacity investments exceed USD 2 billion globally, emphasizing regional manufacturing and supply-chain resilience.

Innovation & Future Outlook: High-performance sustainable admixtures, digital quality control, and carbon-reduction solutions are reshaping competitive differentiation across global markets.

Concrete admixtures play an increasingly important role in enhancing concrete performance, durability, and sustainability across infrastructure, commercial, and industrial construction. Demand is particularly strong in transportation networks, data centers, and energy projects where lifecycle performance requirements are rising. Advanced polycarboxylate-based products now deliver over 20% water reduction efficiency, while stricter carbon-management regulations and evolving supply-chain localization strategies are accelerating adoption of high-performance formulations, setting the stage for broader strategic market developments.

The concrete admixtures market has become strategically important as construction firms, infrastructure developers, and material suppliers prioritize durability, resource efficiency, and lifecycle performance. Infrastructure modernization programs, stricter carbon-intensity requirements, and supply-chain restructuring are accelerating the shift toward performance-engineered concrete solutions. Admixtures are increasingly viewed as a productivity tool rather than a material additive, helping contractors reduce cement consumption while maintaining structural specifications and project timelines.

Technology adoption is creating measurable operational advantages. Advanced polycarboxylate ether-based admixtures deliver up to 20% higher water-reduction efficiency compared with conventional lignosulfonate formulations, while reducing concrete placement variability by approximately 15%. China continues to lead large-scale deployment through infrastructure and industrial construction programs, whereas Germany and Japan focus on precision-engineered admixture systems for high-performance and sustainable building applications. Across major construction markets, digital concrete quality monitoring adoption has surpassed 35% among large contractors, improving batch consistency and reducing rework costs.

A practical example is the integration of admixture optimization platforms in transportation and data-center projects, where project teams have achieved 10–12% reductions in material waste. Manufacturers are responding through localized production investments, technical-service partnerships, and low-carbon product development. Over the next two to three years, adoption of performance-enhancing admixtures is expected to expand steadily across infrastructure and industrial projects, strengthening competitive differentiation through efficiency, compliance, and long-term asset performance.

Large-scale infrastructure modernization and stricter construction performance standards are accelerating demand for advanced concrete admixtures. In India, infrastructure spending allocations continue to support transportation, logistics, and urban development projects, while admixture penetration in organized construction has exceeded 40%. Modern water-reducing technologies lower water consumption by 15–25% and improve compressive strength by approximately 10–15%, enabling contractors to meet tighter engineering specifications. Simultaneously, carbon-reduction targets are encouraging cement optimization strategies that rely on admixture-enhanced concrete formulations. The result is improved durability, lower maintenance requirements, and faster project execution. Manufacturers are expanding production capacity, investing in application laboratories, and forming partnerships with ready-mix concrete suppliers. A key strategic insight is that admixtures are increasingly being specified during project design stages rather than procurement stages, strengthening long-term supplier influence.

Volatility in petrochemical-derived raw materials remains a significant structural limitation for admixture manufacturers. Input cost fluctuations of 10–18% can materially affect formulation economics, particularly for high-performance products dependent on specialty polymers. China continues to influence global chemical supply availability, while logistics disruptions and energy-price variability create procurement uncertainty for producers operating in multiple markets. These pressures reduce pricing flexibility and compress margins, especially in competitive public infrastructure contracts. In several developing economies, advanced admixture utilization remains below 35% because cost-sensitive projects prioritize upfront material expenditure over lifecycle performance benefits. Companies are mitigating risk through localized sourcing, long-term supplier agreements, and formulation optimization programs. An important operational insight is that procurement resilience is becoming as critical as product innovation in maintaining profitability and market access.

The transition toward low-carbon construction presents a substantial opportunity for admixture suppliers. Advanced formulations enabling cement reduction of 8–15% without compromising performance are gaining traction across commercial and infrastructure projects. In India and the United Arab Emirates, green-building adoption rates continue to rise, creating demand for admixtures that improve durability while supporting environmental compliance objectives. Digital concrete optimization tools are also expanding, with adoption among large ready-mix operators approaching 30%, enabling more precise material utilization. Companies are increasing R&D investment in carbon-efficient formulations, recycled-material compatibility, and smart dosing technologies. A less obvious opportunity lies in supporting supplementary cementitious material integration, where admixtures improve consistency and workability. Firms building technical ecosystems around sustainability, testing services, and performance validation are strengthening long-term customer retention and differentiation.

As admixture technologies become more sophisticated, execution complexity is emerging as a long-term challenge. Advanced formulations often require precise dosage control, quality monitoring, and site-specific calibration, yet skilled concrete technology professionals remain in limited supply across several construction markets. Field performance variations can reach 12–20% when batching practices are inconsistent or workforce training is inadequate. In rapidly urbanizing countries, project schedules are tightening while quality requirements continue to increase, placing additional pressure on deployment consistency. Manufacturers must invest in technical support teams, contractor education programs, and digital monitoring platforms to maintain performance reliability. A critical strategic challenge is ensuring uniform results across diverse climatic and operational environments. Companies that combine product innovation with strong technical-service infrastructure will be better positioned to sustain competitiveness and large-scale project participation.

Digital Mix Design Expansion: Concrete producers are increasingly deploying AI-assisted mix optimization and automated dosing platforms, with adoption among large ready-mix operators exceeding 35% and batching accuracy improving by nearly 15%. Labor shortages and tighter project schedules are accelerating deployment across India and China. The shift is reducing material waste by 8–12% while improving quality consistency. Manufacturers are expanding digital service offerings and partnering with software providers to strengthen customer retention beyond product sales.

Low-Carbon Formulation Acceleration: Cement reduction strategies have become a core operational trend, with advanced admixtures enabling 8–15% lower cement usage and supporting carbon-reduction targets. Regulatory pressure on embodied emissions and procurement requirements for sustainable infrastructure projects are reshaping product portfolios. Suppliers are increasing investment in admixtures compatible with supplementary cementitious materials, while contractors prioritize formulations that improve durability and reduce lifecycle maintenance costs.

Localized Manufacturing Networks: Supply-chain resilience has emerged as a major operational focus, prompting producers to localize production and raw-material sourcing. In several markets, regional procurement of key inputs has increased by over 20%, reducing logistics exposure and delivery variability. Companies are restructuring distribution networks, expanding technical-service centers, and forming local partnerships to improve responsiveness and secure infrastructure project participation.

Performance-Specific Product Demand: Demand is shifting from standard admixtures toward application-specific formulations engineered for precast, transportation, and industrial projects. High-performance product penetration has increased by approximately 18% in large construction programs where speed and durability are critical. A less obvious trend is the growing use of customized admixture packages tied to project specifications, encouraging suppliers to integrate testing, technical consulting, and performance validation into commercial agreements.

Superplasticizers represent the leading type segment, accounting for the largest share of advanced concrete applications due to superior workability, water reduction, and compatibility with modern construction requirements. These formulations can reduce water demand by 20–30% while maintaining structural performance, making them indispensable for infrastructure and high-rise developments. Their scalability and ability to support high-strength concrete continue to strengthen market dominance. Companies are expanding polycarboxylate-based product portfolios and investing in application-specific formulations to meet evolving project specifications.

Accelerating admixtures are emerging as the fastest-growing segment, supported by demand for shorter construction cycles and improved productivity. Usage has increased by nearly 12% in precast and transportation projects where rapid strength development is operationally valuable. Water-reducing admixtures remain widely adopted for cost-efficient concrete production, while retarding admixtures retain importance in hot-climate construction environments. Air-entraining products continue to support freeze-thaw durability requirements in developed construction markets. Investment priorities are increasingly shifting toward multifunctional admixtures that combine workability, strength enhancement, and sustainability benefits within a single formulation.

Infrastructure Projects represent the leading application segment, supported by transportation corridors, urban transit systems, bridges, tunnels, and utility upgrades. Large-scale public works increasingly require durability-enhancing and water-reducing admixtures to improve lifecycle performance. Advanced admixture utilization in infrastructure applications exceeds 55% in many large projects, while performance specifications have become more stringent. Suppliers are strengthening relationships with engineering firms and contractors to secure long-term participation in strategic infrastructure programs.

Precast Concrete is the fastest-growing application due to increasing emphasis on construction speed, labor efficiency, and quality consistency. Adoption of advanced admixtures in precast manufacturing has improved production throughput by approximately 15% while reducing curing-related delays. Commercial Construction remains a significant consumer as developers prioritize high-performance building materials. Residential Construction continues to generate stable volume demand, particularly in urban housing developments, while Industrial Construction is expanding through logistics facilities, manufacturing plants, and data-center projects. Companies are responding through automation integration, dedicated technical support, and tailored admixture systems designed for specific construction workflows.

Construction remains the dominant end-user group, driven by continuous demand from residential, commercial, and mixed-use developments. This segment accounts for the highest deployment volume because admixtures directly improve workability, durability, and project execution efficiency. Adoption of performance-enhancing formulations has surpassed 45% in large organized construction projects, reflecting increasing specification requirements. Manufacturers are targeting this segment through product customization, contractor engagement programs, and technical support networks that strengthen long-term customer relationships.

Utilities & Energy is emerging as the fastest-growing end-user segment, supported by investments in renewable energy facilities, transmission infrastructure, and energy storage projects. Admixture usage within energy-related construction has increased by approximately 12–14% as operators prioritize long-life concrete performance under demanding environmental conditions. Infrastructure & Transportation continues to generate substantial demand through road, rail, and airport projects, while Government Projects remain important due to public investment programs. Industrial Facilities and Real Estate Development segments are increasingly adopting specialized formulations to improve project efficiency and structural durability. Companies are expanding ecosystem partnerships, refining pricing strategies, and developing sector-specific solutions to capture evolving procurement requirements.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

Infrastructure Renewal and Performance-Driven Specifications

North America maintains a strong position in the concrete admixtures market, supported by transportation upgrades, industrial construction, logistics facilities, and data center expansion. The region accounts for approximately 24% of global demand, with advanced admixture penetration exceeding 60% in large infrastructure projects. Contractors increasingly specify high-performance formulations to improve durability and reduce lifecycle maintenance costs. Adoption of automated batching systems has improved mix consistency by nearly 12%, supporting tighter engineering requirements. Manufacturers continue expanding technical service capabilities and localized production networks to strengthen supply reliability and project support.

United States Market Outlook: The United States remains the regional leader due to extensive infrastructure modernization programs, advanced ready-mix concrete operations, and strong industrial construction activity. More than 65% of major transportation and commercial projects utilize performance-enhancing admixtures to improve durability and placement efficiency. Growing investment in manufacturing facilities, logistics hubs, and data centers is increasing demand for specialized admixture formulations. Suppliers are prioritizing technical partnerships, digital quality-control solutions, and regional distribution expansion to strengthen competitive positioning.

Sustainability-Led Material Optimization

Europe's market is shaped by strict environmental standards, modernization of aging infrastructure, and growing emphasis on low-carbon construction practices. The region contributes approximately 22% of global demand and demonstrates high adoption of admixtures designed to reduce cement consumption and improve durability. Advanced concrete technologies are increasingly integrated into commercial and infrastructure developments, with sustainable formulations improving material efficiency by 10–15%. Companies are investing in product innovation and collaboration with construction firms to support evolving environmental compliance requirements and performance specifications.

Germany Market Outlook: Germany serves as the region's most influential market due to its engineering-intensive construction sector, industrial manufacturing base, and leadership in sustainable building technologies. Adoption of advanced concrete additives in major infrastructure and industrial projects exceeds 55%, reflecting strong demand for quality and durability. Domestic manufacturers emphasize low-carbon product development, precision formulation technologies, and technical support services. Continued modernization of transportation and industrial assets reinforces demand for high-performance admixture solutions across the country.

Large-Scale Infrastructure Deployment Advantage

Asia-Pacific leads the global market with approximately 43% share, driven by extensive infrastructure construction, urbanization programs, industrial expansion, and manufacturing capacity growth. The region represents the largest deployment base for concrete admixtures, supported by transportation networks, smart-city projects, and energy infrastructure investments. Advanced admixture utilization has increased by more than 18% in major infrastructure developments as project owners prioritize durability and operational efficiency. Suppliers are expanding production facilities and technical-service networks to support growing project pipelines and localized demand requirements.

China Market Outlook: China remains the dominant country due to its scale of infrastructure development, industrial construction activity, and domestic manufacturing ecosystem. Advanced admixture penetration exceeds 55% across large infrastructure projects, supported by continuous investment in transportation, utilities, and urban redevelopment programs. Local producers are increasing research activity around high-performance and sustainable formulations while expanding production capacity. Strong integration between construction enterprises, material suppliers, and infrastructure developers continues to reinforce China's leadership position within the market.

Urban Infrastructure Expansion Momentum

South America is experiencing steady demand growth supported by transportation improvements, residential development, and industrial facility construction. The region contributes approximately 6% of global consumption, with infrastructure modernization projects driving increasing use of performance-enhancing concrete technologies. Admixture adoption has risen by nearly 10% in large public works projects where durability and maintenance reduction are critical objectives. However, project financing variability and construction-cycle fluctuations continue to influence deployment rates. Manufacturers are addressing these challenges through localized distribution partnerships and targeted technical support programs.

Brazil Market Outlook: Brazil represents the largest market in South America due to its construction scale, urban development activity, and infrastructure investment pipeline. Demand is particularly strong across transportation corridors, industrial facilities, and commercial developments. Advanced admixture utilization has expanded by approximately 12% in large-scale projects as contractors focus on performance optimization and operational efficiency. Suppliers are strengthening regional manufacturing, technical training, and contractor engagement strategies to support long-term market penetration and project execution consistency.

Mega-Project Investment Transformation

Middle East & Africa is emerging as the fastest-expanding regional market, supported by large-scale infrastructure projects, urban development initiatives, industrial diversification programs, and energy-sector construction. The region accounts for roughly 5% of global demand but demonstrates some of the highest deployment growth rates for advanced concrete technologies. High-performance admixture adoption has increased by approximately 15% in major development projects where durability and environmental resilience are essential. Companies are investing in local production, technical partnerships, and project-specific formulation capabilities to support evolving construction requirements.

Saudi Arabia Market Outlook: Saudi Arabia is the region's most strategically significant market, driven by large infrastructure developments, industrial diversification initiatives, and extensive urban construction activity. Advanced admixture deployment continues to accelerate across transportation, tourism, and mixed-use development projects. More than 50% of major construction programs now specify high-performance concrete solutions to address durability and environmental performance requirements. Manufacturers are expanding local operations, technical-service resources, and collaborative project-development efforts to capitalize on sustained construction activity and modernization objectives.

The competitive landscape is led by global formulation specialists including Sika, Master Builders Solutions, Fosroc, Mapei, and GCP Applied Technologies competing against regional manufacturers and cost-focused local suppliers. The top five players collectively account for approximately 42% of global market activity, creating a moderately consolidated structure. Competition centers on performance enhancement, technical support, supply reliability, and customized formulations rather than price alone. Advanced admixture technologies deliver 15–30% water reduction benefits, while premium formulations improve durability by more than 20%, making innovation a decisive differentiator. Global leaders are expanding production facilities, strengthening contractor partnerships, and integrating technical consulting services into commercial offerings. Regional competitors focus on localized sourcing, faster delivery cycles, and project-specific pricing strategies. The competitive shift is moving toward sustainable formulations, digital quality-control integration, and supply-chain resilience. Key barriers include formulation expertise, certification requirements, technical-service capabilities, and established contractor relationships. Winning requires superior performance validation, localized execution, and continuous product innovation.

Sika AG

Master Builders Solutions

Fosroc International

Mapei S.p.A.

GCP Applied Technologies

CHRYSO

RPM International

Arkema Group

Kao Corporation

CICO Technologies

MUHU (China) Construction Materials

Cemex

Cormix International

Thermax Limited

Advanced polycarboxylate ether (PCE) superplasticizers remain the core technology shaping the concrete admixtures market. By 2026, more than 55% of large infrastructure and commercial projects utilize PCE-based formulations because they improve water reduction by 20–30% compared with conventional lignosulfonate admixtures while increasing compressive strength by 10–15%. Automated dosing systems are also gaining traction, improving batching accuracy by approximately 12% and reducing material wastage by 8%. These technologies provide contractors with better consistency, lower cement consumption, and improved project execution efficiency.

Emerging technologies are focused on digital concrete optimization and intelligent quality-control systems. AI-enabled mix design platforms are now deployed by over 35% of large ready-mix producers, helping optimize admixture dosage and reduce production variability by nearly 10%. Integration between admixture chemistry, IoT sensors, and plant automation enables real-time monitoring of concrete performance. Companies adopting these solutions achieve faster project turnaround, stronger specification compliance, and reduced operational costs, creating a clear competitive advantage in infrastructure and industrial construction projects.

Between 2026 and 2028, innovation will increasingly center on low-carbon admixtures, nano-engineered additives, and formulations optimized for supplementary cementitious materials. These technologies support cement reduction of 8–15% while maintaining structural performance and durability. Compared with traditional concrete systems, next-generation solutions deliver superior sustainability and lifecycle efficiency. Global technology leaders and innovation-focused manufacturers are accelerating investment in digital platforms, advanced chemistry, and performance validation because early adoption strengthens market differentiation, improves customer retention, and secures participation in high-value construction programs.

September 2024 – Sika AG commenced construction of a new concrete admixtures manufacturing facility in Florida, USA, expanding regional production capacity and supporting infrastructure demand. The project is designed to reduce approximately 7,800 tonnes of CO₂ emissions by 2032 through improved operational efficiency and logistics optimization. Source: usa.sika.com

January 2025 – Master Builders Solutions expanded operations in India through MBT Construction Chemicals, strengthening access to transportation, industrial, and commercial construction sectors. The initiative enhances local market coverage and technical service capabilities for advanced admixture deployment. Source: master-builders-solutions.com

June 2025 – Sika AG invested in Giatec Scientific Inc. to integrate AI-driven concrete optimization technologies with admixture solutions, enabling measurable reductions in cement consumption and improved material performance through digital concrete analytics. Source: sika.com

December 2025 – Sika AG inaugurated a highly automated admixture production facility in Florida dedicated to advanced superplasticizers. The plant incorporates end-to-end digitalized production processes, improving manufacturing efficiency and strengthening supply responsiveness for major construction projects.

The report provides comprehensive analysis of the concrete admixtures market across water-reducing, superplasticizers, accelerating, retarding, and air-entraining product categories. It evaluates demand patterns across residential construction, commercial construction, infrastructure projects, industrial construction, and precast concrete applications while assessing procurement behavior among construction companies, infrastructure developers, government agencies, utilities, and industrial operators. Infrastructure-related applications account for more than 40% of advanced admixture deployment, reflecting the increasing importance of durability and performance-driven construction practices.

The study covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, supported by detailed country-level assessments and competitive benchmarking. It analyzes technology adoption trends including AI-assisted mix optimization, automated dosing systems, low-carbon admixture formulations, and advanced polycarboxylate technologies. The report also examines deployment patterns, innovation strategies, manufacturing expansion initiatives, and evolving customer requirements. Strategic insights support investment planning, market-entry assessment, partnership development, competitive positioning, and long-term business decision-making across the 2026–2033 outlook period.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14990 Million |

|

Market Revenue in 2033 |

USD 22831.08 Million |

|

CAGR (2026 - 2033) |

5.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sika AG, Master Builders Solutions, Fosroc International, Mapei S.p.A., GCP Applied Technologies, CHRYSO, RPM International, Arkema Group, Kao Corporation, CICO Technologies, MUHU (China) Construction Materials, Cemex, Cormix International, Thermax Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |