Reports

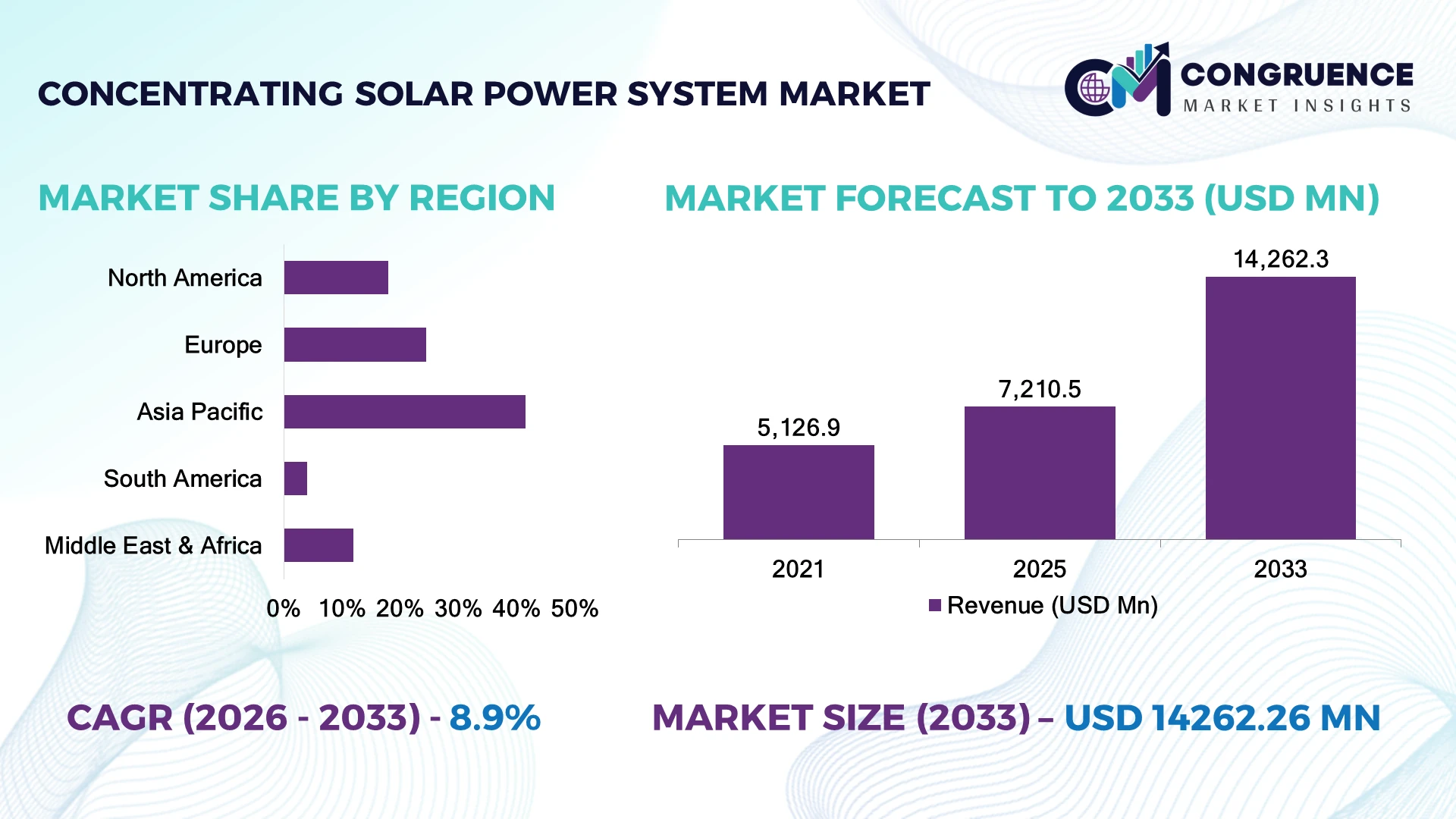

The Global Concentrating Solar Power System Market was valued at USD 7,210.5 Million in 2025 and is anticipated to reach a value of USD 14,262.3 Million by 2033 expanding at a CAGR of 8.9% between 2026 and 2033. Growth is being driven by utility-scale renewable energy deployment, long-duration thermal energy storage integration, and increasing investments in dispatchable low-carbon power infrastructure.

China accounts for approximately 31% of global installed concentrating solar power capacity, supported by large-scale renewable energy investments, molten salt storage deployment, and grid modernization initiatives, while Spain remains Europe's technology leader through advanced commercial CSP operations. Following global energy security priorities reinforced after the Russia-Ukraine conflict, thermal storage utilization has improved plant dispatchability by nearly 40%, strengthening CSP's role in balancing renewable electricity generation.

Utilities and developers investing in high-efficiency thermal storage, localized supply chains, and next-generation CSP technologies are positioned to strengthen long-term energy resilience and competitive advantage.

Market Size & Growth: USD 7,210.5 Million in 2025, projected to reach USD 14,262.3 Million by 2033 at a CAGR of 8.9%, supported by utility-scale renewable energy expansion.

Top Growth Drivers: Thermal energy storage (44%), grid decarbonization (38%), and utility-scale renewable projects (34%) continue driving investment.

Short-Term Forecast: By 2028, advanced thermal storage is expected to improve plant utilization by nearly 18%.

Emerging Technologies: AI-powered plant optimization, molten salt storage, and high-efficiency heliostat automation are improving operational performance.

Regional Leaders: Asia-Pacific exceeds USD 5.8 Billion, Europe approaches USD 3.9 Billion, and the Middle East surpasses USD 2.6 Billion through utility-scale deployment.

Consumer/End-User Trends: More than 62% of new CSP investments now prioritize integrated thermal energy storage.

Pilot/Case Example: A 2026 CSP modernization project improved thermal efficiency by 16% while reducing operating costs by 12%.

Competitive Landscape: The leading developer controls approximately 14% market share alongside ACWA Power, BrightSource Energy, Abengoa, and SEPCOIII.

Regulatory & ESG Impact: Renewable energy mandates increased dispatchable solar project approvals by over 27% across key markets.

Investment & Funding: More than USD 8.5 Billion has been allocated to CSP projects, storage integration, and grid modernization initiatives.

Innovation & Future Outlook: Supercritical CO₂ cycles, advanced receivers, and digital asset optimization are strengthening long-term plant competitiveness.

Concentrating Solar Power System Market deployment continues expanding across utility-scale electricity generation, industrial heat production, and hybrid renewable energy projects. Advanced molten salt storage, AI-assisted performance optimization, and high-efficiency receiver technologies are improving dispatchable clean energy generation. Nearly 58% of newly announced CSP projects now integrate long-duration thermal storage, supported by grid reliability initiatives and energy security strategies, establishing a strong foundation for long-term strategic investment.

Concentrating Solar Power Systems are becoming strategically important as power utilities seek dispatchable renewable generation capable of supporting grid stability alongside intermittent solar and wind resources. Energy security priorities, grid modernization programs, and expanding renewable integration targets are accelerating investment in thermal energy storage and utility-scale CSP infrastructure.

Modern molten salt storage systems extend electricity generation for more than eight hours after sunset while improving dispatch flexibility by approximately 35% compared with conventional solar photovoltaic facilities without storage. China leads global capacity expansion through large-scale renewable energy investments, whereas Spain continues advancing high-efficiency CSP technologies and operational optimization. Over the next two to three years, integrated thermal storage, digital plant monitoring, and automated heliostat control are expected to improve operational efficiency and strengthen grid reliability across utility-scale projects.

Utilities are increasingly deploying CSP facilities alongside photovoltaic plants and battery storage to create diversified renewable energy portfolios with greater operational flexibility. Technology providers are expanding strategic partnerships, investing in advanced receiver materials, and strengthening local manufacturing capabilities to improve project economics. Organizations combining thermal storage innovation, digital plant optimization, and efficient project execution will secure stronger competitive positioning while supporting long-term decarbonization and resilient electricity infrastructure.

The ability to deliver dispatchable renewable electricity through integrated thermal energy storage is accelerating Concentrating Solar Power System deployment across utility-scale projects. More than 64% of newly announced CSP developments now incorporate molten salt storage, while advanced receiver technologies improve thermal conversion efficiency by approximately 17% and increase evening power availability by nearly 35%. China's renewable energy expansion and long-duration storage programs continue strengthening CSP deployment alongside large transmission investments. The combination of storage capability and predictable power generation enables utilities to reduce dependence on fossil-fuel peaking plants while improving grid stability. Developers are responding through larger integrated projects, strategic technology partnerships, localized manufacturing, and investment in high-efficiency heliostat systems to improve project economics and operational flexibility.

High upfront investment requirements and specialized component availability continue limiting the pace of CSP deployment. Engineering, procurement, and construction costs remain approximately 28% higher than conventional utility-scale photovoltaic projects, while specialized receiver tubes and molten salt materials account for nearly 22% of total project expenditure. Spain and several Middle Eastern markets continue facing procurement challenges linked to specialized thermal equipment manufacturing and long project development cycles. These constraints affect financing timelines, contractor availability, and project scalability. Developers are mitigating risk through long-term supplier agreements, localized manufacturing initiatives, standardized plant designs, and hybrid renewable configurations that improve financial viability while reducing dependence on imported high-value components.

Hybrid renewable power plants combining Concentrating Solar Power, photovoltaic generation, battery storage, and intelligent energy management systems are creating significant long-term opportunities. Integrated renewable configurations improve renewable energy utilization by approximately 26%, while digital plant optimization reduces operational losses by nearly 14%. Saudi Arabia and the United Arab Emirates are expanding utility-scale hybrid energy developments to strengthen energy diversification and improve electricity reliability. Technology providers are investing in AI-driven plant control, supercritical CO₂ power cycles, and advanced thermal storage solutions through strategic partnerships and collaborative research. An emerging opportunity lies in supplying high-temperature industrial process heat, enabling CSP operators to diversify revenue beyond electricity generation while supporting industrial decarbonization initiatives.

Delivering large-scale CSP facilities requires coordinated engineering, transmission infrastructure, and long-term operational expertise, making execution significantly more complex than conventional renewable projects. Construction schedules can extend by approximately 30% because of specialized engineering requirements, while grid interconnection processes increase commissioning timelines by nearly 18% for utility-scale developments. South Africa and Australia continue strengthening transmission infrastructure to accommodate dispatchable renewable generation, yet project execution remains dependent on skilled engineering resources and robust grid planning. Developers must invest in digital asset management, predictive maintenance platforms, workforce development, and advanced project delivery capabilities. Successfully scaling technically complex projects while maintaining operational reliability will determine long-term competitiveness in the global CSP industry.

Advanced Thermal Storage Expansion Integrated molten salt storage is becoming standard across new CSP developments, with more than 62% of announced projects incorporating long-duration storage and improving dispatchable generation by approximately 34%. Energy security priorities and grid modernization programs are encouraging developers to expand storage capacity, while utilities increasingly favor plants capable of supplying electricity beyond daylight hours.

Digital Plant Performance Optimization AI-enabled monitoring, predictive maintenance, and automated heliostat calibration are improving plant availability by nearly 16% while reducing maintenance downtime by approximately 19%. Operators are integrating digital twins and advanced analytics into daily operations, enabling faster performance optimization and lower lifecycle operating costs across utility-scale facilities.

Hybrid Renewable Project Development Utilities are increasingly combining CSP with photovoltaic systems and battery storage to improve renewable energy utilization and operational flexibility. Hybrid configurations increase energy delivery efficiency by approximately 24% while reducing renewable curtailment by nearly 18%. Project developers are strengthening technology partnerships and integrated engineering capabilities to deliver diversified renewable power assets with enhanced grid reliability.

Localized Manufacturing Initiatives Governments and developers are expanding domestic manufacturing of heliostats, receiver components, and thermal storage systems to strengthen supply resilience. Local sourcing strategies have reduced equipment lead times by approximately 21% while lowering logistics exposure by nearly 15%. Companies are investing in regional production facilities, supplier collaborations, and standardized component designs to improve project execution and long-term supply-chain stability.

Parabolic trough systems account for approximately 52% of the Concentrating Solar Power System Market, supported by their proven commercial performance, lower operational risk, and compatibility with large-scale molten salt thermal storage. Their mature engineering ecosystem, established supply chain, and reliable dispatchable electricity generation continue making them the preferred technology for utility-scale projects. Solar tower systems represent the fastest-growing segment as higher operating temperatures and improved thermal efficiency increase adoption for next-generation renewable energy facilities. Linear Fresnel and dish Stirling technologies retain strategic relevance in niche industrial and distributed energy applications where land availability, modular deployment, or process heat requirements influence technology selection.

Developers are expanding investments in high-temperature receiver technologies and automated heliostat control systems to improve plant performance. More than 61% of newly announced CSP facilities now incorporate advanced thermal storage with tower-based designs, while digital optimization improves solar field efficiency by approximately 15%. Investment priorities are gradually shifting toward higher-efficiency configurations capable of delivering longer dispatchable generation and stronger project economics.

According to 2026 deployment assessments released by the International Renewable Energy Agency (IRENA), utility-scale CSP expansion increasingly favors solar tower technology with integrated thermal storage for large renewable energy projects seeking higher operational flexibility and dispatchable power generation.

Utility-scale electricity generation represents approximately 71% of Concentrating Solar Power System deployment, reflecting the technology's strategic role in delivering dispatchable renewable energy for national grids. Long-duration thermal storage, stable power output, and compatibility with grid balancing requirements continue driving investment from utilities and independent power producers. Industrial process heat is the fastest-growing application as mining, chemicals, cement, and food processing industries increasingly adopt CSP to reduce fossil fuel consumption and improve energy security. Desalination, district heating, and hybrid renewable energy applications continue expanding as operators diversify plant utilization beyond conventional electricity production.

Developers are integrating CSP with photovoltaic systems, battery storage, and digital energy management platforms to maximize asset utilization. More than 57% of newly planned CSP facilities now incorporate hybrid renewable configurations, while intelligent plant controls improve operational efficiency by approximately 18%. Companies are expanding engineering partnerships and project portfolios to capture emerging industrial decarbonization opportunities alongside conventional utility markets.

According to 2025 findings published by the International Energy Agency (IEA), industrial heat applications are emerging as one of the strongest deployment areas for concentrating solar technologies because of growing demand for carbon-free high-temperature process energy.

Utilities account for approximately 67% of total Concentrating Solar Power System demand, supported by large-scale renewable generation programs, national grid modernization initiatives, and growing investment in dispatchable clean energy infrastructure. Their purchasing concentration reflects the need for reliable renewable electricity capable of supporting peak demand and grid stability. Industrial energy producers represent the fastest-growing end-user segment as manufacturers increasingly invest in CSP for high-temperature process heat, energy diversification, and emissions reduction. Independent power producers, government agencies, and commercial energy developers continue strengthening adoption through hybrid renewable projects and long-term infrastructure investments.

Technology providers are responding through customized engineering solutions, strategic EPC partnerships, and advanced thermal storage integration. Nearly 54% of new CSP procurement programs now prioritize storage-enabled configurations, while digital asset management improves operational availability by approximately 14%. Companies are strengthening regional manufacturing capabilities and long-term service agreements to improve project performance and reinforce customer relationships across utility and industrial sectors.

According to a 2026 global renewable infrastructure assessment published by the International Energy Agency (IEA), electric utilities remain the largest investors in dispatchable solar technologies, while industrial energy users are accelerating adoption of concentrating solar systems for continuous high-temperature thermal applications.

Asia-Pacific accounted for the largest market share at 41.5% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

Grid Reliability Investments Revitalize Dispatchable Solar Projects

North America continues strengthening its Concentrating Solar Power System market through grid modernization, long-duration energy storage deployment, and utility-scale renewable diversification. The region contributes approximately 18% of global market demand, supported by investments in dispatchable clean energy, transmission upgrades, and advanced thermal storage integration. More than 60% of proposed CSP developments now evaluate hybrid configurations combining thermal storage with photovoltaic generation to improve grid flexibility. Utilities are increasingly deploying digital asset management platforms and predictive maintenance systems, improving plant availability by nearly 15% while reducing operational interruptions. Strategic collaboration between developers, EPC contractors, and technology providers continues accelerating modernization of renewable generation infrastructure.

United States Market Outlook: The United States remains the region's largest market through its advanced renewable energy ecosystem, established CSP operating experience, and strong investment in grid modernization. Southwestern states continue supporting utility-scale renewable developments requiring dispatchable electricity generation. More than 70% of the country's installed CSP capacity incorporates thermal storage, enabling utilities to improve evening peak supply while strengthening renewable energy reliability through advanced operational optimization.

Technology Innovation Supports Renewable Grid Stability

Europe maintains a technology-driven CSP market through advanced engineering capabilities, renewable energy integration, and industrial decarbonization strategies. The region represents approximately 30% of global market activity, supported by established commercial facilities and continuous investment in high-efficiency thermal storage technologies. More than 58% of modernization projects now focus on digital plant optimization and improved receiver performance to increase operational efficiency. Technology developers continue strengthening research partnerships and advanced component manufacturing, supporting long-term competitiveness in dispatchable renewable electricity generation.

Spain Market Outlook: Spain leads the European market with the world's most mature commercial CSP operating base and extensive expertise in thermal storage integration. Utilities and technology providers continue upgrading existing facilities through digital monitoring, heliostat optimization, and advanced control systems. High operational experience and established engineering capabilities position Spain as a global technology leader supporting new international CSP developments and engineering services.

Large-Scale Renewable Deployment Drives Regional Leadership

Asia-Pacific dominates the global Concentrating Solar Power System market through extensive renewable energy investments, expanding domestic manufacturing, and integrated power infrastructure development. The region accounts for approximately 41.5% of global demand, supported by large utility-scale projects and national energy transition strategies. More than 65% of newly commissioned CSP capacity includes advanced molten salt thermal storage, improving dispatchable renewable generation and grid reliability. Project developers continue expanding local supply chains, automated heliostat manufacturing, and digital plant management capabilities to strengthen operational performance and project execution.

China Market Outlook: China remains the world's largest CSP market through sustained renewable infrastructure investment, vertically integrated manufacturing, and government-supported demonstration programs. Utility developers continue expanding solar tower and parabolic trough installations with high-capacity thermal storage systems. Nearly 31% of global installed CSP capacity is concentrated in China, encouraging continuous investment in next-generation receiver technologies, intelligent plant automation, and localized equipment manufacturing.

Mining Sector Expands Renewable Heat Adoption

South America is steadily increasing CSP deployment as mining operations, industrial facilities, and utilities seek reliable renewable energy for electricity and high-temperature process heat. The region contributes approximately 4% of global market demand, supported by excellent solar irradiation and expanding renewable infrastructure investment. Hybrid renewable projects improve operational flexibility while reducing dependence on conventional fuels. Developers are strengthening engineering partnerships and localized project execution capabilities, although transmission expansion and financing availability remain important considerations for accelerating commercial deployment.

Chile Market Outlook: Chile leads the regional market through exceptional solar resources, strong mining activity, and national decarbonization objectives. Mining companies increasingly evaluate CSP with thermal storage to provide continuous electricity and industrial heat in remote operations. Continued transmission investment and renewable energy expansion strengthen Chile's position as the region's most advanced market for utility-scale concentrating solar technology.

Mega Renewable Projects Accelerate Thermal Storage Deployment

The Middle East & Africa represents the fastest-expanding regional market, supported by large-scale renewable energy programs, economic diversification strategies, and rising investment in dispatchable clean power infrastructure. The region accounts for approximately 15% of global market activity, with CSP increasingly integrated into national energy transition plans. More than 63% of recently announced utility-scale renewable projects evaluate thermal storage as a strategic grid-balancing solution. Developers are expanding regional manufacturing partnerships, engineering capabilities, and digital plant technologies to improve project efficiency and long-term operational resilience.

United Arab Emirates Market Outlook: The United Arab Emirates has established itself as a regional technology leader through large-scale CSP deployment, advanced thermal storage implementation, and integrated renewable energy infrastructure. Utility-scale projects increasingly combine photovoltaic generation with concentrating solar technology to maximize dispatchable clean electricity. Continued investment in innovation, high-capacity storage systems, and smart grid integration is strengthening the country's role as a benchmark for utility-scale renewable energy development across the Middle East.

Competition is led by ACWA Power, BrightSource Energy, Abengoa, SolarReserve technologies, and SEPCOIII, with integrated project developers competing against EPC contractors, thermal storage innovators, and engineering specialists for utility-scale renewable infrastructure contracts. The top five participants collectively account for approximately 54% of the market. Competition depends on thermal storage efficiency, project execution capability, localized supply chains, and levelized electricity costs rather than equipment pricing alone. Advanced receiver technologies improve thermal efficiency by nearly 16%, digital plant optimization reduces operating costs by approximately 13%, and localized manufacturing shortens procurement timelines by almost 20%. Companies are expanding through strategic utility partnerships, EPC collaborations, vertical integration, and investment in next-generation solar tower technologies. Competitive momentum is shifting toward storage-integrated CSP projects with higher dispatchability and digital asset optimization. High capital intensity, lengthy permitting, and specialized engineering expertise remain the principal entry barriers. Market leadership depends on delivering reliable dispatchable power, efficient thermal storage, strong execution capability, and localized manufacturing partnerships.

ACWA Power

BrightSource Energy

Abengoa

SEPCOIII Electric Power Construction Co., Ltd.

Aalborg CSP A/S

Synhelion SA

Heliogen, Inc.

SENER Grupo de Ingeniería

TSK Electrónica y Electricidad S.A.

ENGIE

GlassPoint Solar

China Energy Engineering Corporation (Energy China)

Torresol Energy

Concentrating Solar Power Systems are advancing through high-temperature solar towers, molten salt thermal storage, AI-enabled heliostat control, and digital twin technologies integrated with utility-scale renewable infrastructure. More than 62% of newly commissioned CSP facilities now incorporate long-duration thermal storage, while AI-based heliostat optimization improves solar field efficiency by approximately 15%. Automated receiver monitoring and predictive maintenance reduce operational downtime, enabling more reliable dispatchable renewable electricity for modern power grids.

Compared with conventional parabolic trough configurations, advanced solar tower systems operating with next-generation receiver materials improve thermal efficiency by nearly 18% and extend storage-supported electricity delivery by approximately 35%. Utilities integrating CSP with photovoltaic plants and battery systems achieve greater operational flexibility and improved grid stability. Large energy developers and vertically integrated EPC companies gain the strongest competitive advantage because advanced thermal storage enables continuous renewable generation during peak demand periods.

Between 2026 and 2028, supercritical CO₂ power cycles, particle-based thermal storage, autonomous heliostat calibration, and AI-driven plant optimization will reshape project economics. Companies investing in advanced receiver technologies, digital plant intelligence, and localized manufacturing will improve operational reliability and strengthen competitiveness. Early technology adoption enables developers to increase dispatchability, reduce lifecycle costs, and secure stronger positions in long-duration renewable energy markets.

January 2025 – Heliogen concluded its Capella Generation 3 concentrating solar power demonstration project, validating technologies designed for a planned 5-MWe commercial-scale CSP plant and advancing next-generation high-temperature solar thermal commercialization. Source: Heliogen

May 2025 – Heliogen agreed to be acquired by Zeo Energy, combining advanced concentrating solar technology with distributed clean energy solutions to create an integrated residential, commercial, and utility-scale platform. Source: Heliogen

Q1 2024 – ACWA Power confirmed commercial operation of the 950 MW Noor Energy 1 hybrid CSP and photovoltaic project in Dubai, featuring the world's largest thermal energy storage facility and strengthening dispatchable renewable electricity generation. Source: ACWA Power

March 2024 – ACWA Power reported technical repairs at the 150 MW Noor Ouarzazate III CSP plant in Morocco following a molten salt storage system issue, reinforcing industry focus on long-term thermal storage reliability. Source: Reuters

This report provides comprehensive analysis of the Concentrating Solar Power System Market across parabolic trough, solar tower, linear Fresnel, and dish Stirling technologies. It evaluates deployment across utility-scale power generation, industrial process heat, desalination, district heating, and hybrid renewable energy applications while assessing demand from utilities, independent power producers, industrial energy users, government agencies, and commercial developers. Regional coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 20 strategically significant country markets and profiling leading technology developers and EPC providers.

The study examines molten salt thermal storage, AI-enabled plant optimization, advanced heliostat systems, digital twins, supercritical CO₂ cycles, and hybrid renewable integration shaping the market between 2026 and 2033. It highlights technology adoption, deployment patterns, project execution strategies, competitive positioning, and infrastructure investment trends that support investment planning, expansion strategy, technology selection, and long-term competitive decision-making across the evolving global renewable energy sector.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 7,210.5 Million |

|

Market Revenue in 2033 |

USD 14,262.3 Million |

|

CAGR (2026 - 2033) |

8.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ACWA Power, BrightSource Energy, Abengoa, SEPCOIII Electric Power Construction Co., Ltd., Aalborg CSP A/S, Synhelion SA, Heliogen, Inc., SENER Grupo de Ingeniería, TSK Electrónica y Electricidad S.A., ENGIE, GlassPoint Solar, China Energy Engineering Corporation (Energy China), Torresol Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |