Reports

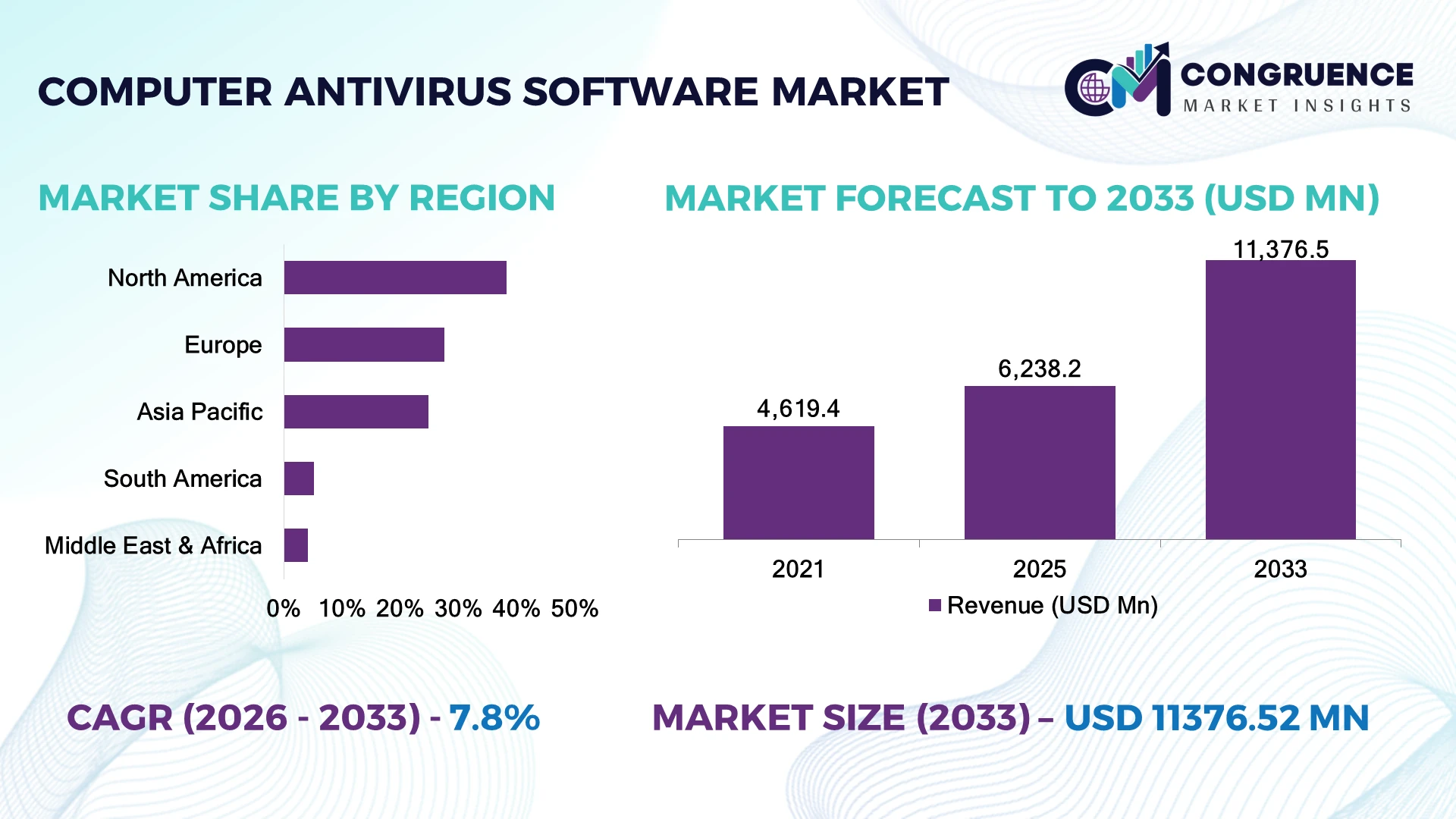

The Global Computer Antivirus Software Market was valued at USD 6,238.2 Million in 2025 and is anticipated to reach a value of USD 11,376.5 Million by 2033 expanding at a CAGR of 7.8% between 2026 and 2033. Growth is primarily driven by AI-powered threat detection, expanding hybrid work environments, stricter cybersecurity compliance requirements, and rising enterprise investment in endpoint protection platforms.

The United States dominates the global computer antivirus software market with an estimated 36% share, supported by advanced cybersecurity infrastructure, strong enterprise software spending, and rapid AI-driven security adoption across finance, healthcare, government, and technology sectors. More than 72% of large enterprises have deployed AI-assisted endpoint protection platforms, compared with approximately 61% in Germany, where regulatory compliance remains a stronger purchasing driver. Continued geopolitical cyber threats and ransomware campaigns across critical infrastructure are accelerating enterprise cybersecurity modernization and investment.

Organizations prioritizing intelligent, cloud-native endpoint security and automated threat response will strengthen cyber resilience while reducing operational risk and long-term security costs.

Market Size & Growth: Valued at USD 6,238.2 million in 2025 and projected to reach USD 11,376.5 million by 2033, driven by enterprise cybersecurity modernization and cloud endpoint protection.

Top Growth Drivers: AI-based threat detection contributes 42% of new deployments, ransomware protection 34%, and hybrid workforce security requirements 29%.

Short-Term Forecast: By 2028, automated malware detection is expected to improve incident response efficiency by 38% while reducing manual investigation workloads by 31%.

Emerging Technologies: AI-driven behavioral analytics, Extended Detection and Response (XDR), and Zero Trust integration are reshaping advanced antivirus software platforms.

Regional Leaders: North America exceeds USD 2.3 billion, Europe approaches USD 1.7 billion, and Asia-Pacific surpasses USD 1.8 billion, supported by enterprise digital transformation.

Consumer/End-User Trends: Nearly 68% of businesses now prioritize cloud-managed endpoint security over traditional standalone antivirus software.

Pilot/Case Example: In 2025, AI-assisted malware detection deployments reduced false-positive alerts by approximately 41% across enterprise security operations.

Competitive Landscape: The top five vendors collectively control nearly 57% of the global market, led by Microsoft, Broadcom, Gen Digital, Trend Micro, and ESET.

Regulatory & ESG Impact: More than 63% of regulated enterprises increased cybersecurity compliance spending following strengthened digital security regulations.

Investment & Funding: Over USD 4.5 billion in cybersecurity investments supported AI security platforms, cloud-native protection, and strategic technology acquisitions during the latest investment cycle.

Innovation & Future Outlook: Autonomous threat hunting, generative AI security assistants, and unified endpoint security platforms are becoming primary competitive differentiators across the global market.

Computer antivirus software has evolved from signature-based malware detection into intelligent endpoint security platforms supporting cloud workloads, hybrid workforces, and AI-assisted threat analysis. Approximately 64% of enterprise security teams now prioritize behavioral detection over traditional file scanning as ransomware and zero-day attacks become more sophisticated. Increasing regulatory compliance requirements and expanding managed security services are accelerating demand for integrated protection platforms, setting the foundation for broader strategic transformation.

The computer antivirus software market has become strategically important as cyber resilience increasingly influences enterprise competitiveness, operational continuity, and regulatory compliance. Organizations are shifting from isolated endpoint protection toward integrated cybersecurity ecosystems that combine antivirus software, endpoint detection, identity protection, and automated incident response. Rising cyberattacks targeting healthcare, manufacturing, financial services, and government infrastructure are accelerating investment in intelligent security platforms, while stricter digital security regulations continue reshaping enterprise procurement priorities.

AI-powered antivirus platforms now detect advanced threats approximately 47% faster than conventional signature-based solutions while reducing false-positive alerts by nearly 39%, allowing security teams to focus on higher-risk incidents. The United States leads adoption through large-scale enterprise cybersecurity investment and cloud infrastructure maturity, whereas Japan emphasizes secure industrial systems and manufacturing cybersecurity. During the next two to three years, more organizations are expected to consolidate multiple endpoint security tools into unified protection platforms supporting centralized threat management.

A practical example is multinational enterprises deploying cloud-managed endpoint protection across geographically distributed workforces, reducing security administration complexity while improving policy consistency. Vendors are responding through AI innovation, managed security partnerships, regional cloud infrastructure expansion, and integrated XDR capabilities. Companies that combine intelligent automation, rapid threat intelligence, and scalable cloud-native security architectures will establish stronger competitive positioning and deliver measurable operational advantages in an increasingly sophisticated cyber threat environment.

The rapid evolution of AI-powered cyber threats is driving enterprises to replace conventional antivirus software with intelligent endpoint protection platforms. Approximately 69% of large organizations now prioritize behavior-based threat detection, while automated malware analysis reduces incident response time by nearly 43%. The implementation of stricter cybersecurity regulations across the United States and the European Union has accelerated enterprise-wide deployment of advanced antivirus solutions with integrated threat intelligence. This structural shift improves operational resilience and reduces security management complexity. Vendors are expanding AI research, integrating Extended Detection and Response (XDR) capabilities, and partnering with cloud service providers to strengthen platform interoperability. A notable competitive advantage now lies in continuous threat learning rather than periodic signature database updates.

Compatibility limitations across legacy operating systems and fragmented enterprise IT environments continue restricting antivirus software modernization. Nearly 38% of enterprise endpoints still operate on mixed-generation infrastructure, while approximately 26% of organizations report integration challenges between legacy applications and modern security platforms. Manufacturing companies in Germany and Japan frequently delay endpoint upgrades to avoid disrupting operational technology environments. These constraints increase deployment costs, prolong implementation timelines, and reduce centralized security visibility. Software vendors are minimizing operational risks by offering hybrid deployment models, backward-compatible agents, and flexible licensing agreements while expanding partnerships with managed security service providers to simplify migration without interrupting business operations.

Autonomous cybersecurity powered by generative AI, predictive analytics, and cloud-native security orchestration is creating new growth opportunities beyond traditional malware protection. Approximately 47% of enterprise security teams are evaluating AI-assisted threat investigation, while security automation lowers manual alert processing by nearly 36%. Singapore continues investing in digital infrastructure and cybersecurity innovation, creating demand for intelligent endpoint protection across financial services and smart city ecosystems. Vendors are expanding AI research centers, integrating Security Operations Center automation, and developing ecosystem partnerships with cloud infrastructure providers. An emerging opportunity lies in adaptive security platforms capable of continuously modifying protection policies based on real-time enterprise risk profiles rather than predefined security rules.

Protecting endpoints across cloud environments, mobile devices, remote workforces, and operational technology networks has significantly increased execution complexity. Approximately 44% of enterprise security teams manage five or more endpoint operating environments, while unified policy enforcement improves security consistency by only around 29% without platform standardization. The United States continues experiencing growing pressure to secure AI-enabled workloads alongside conventional enterprise infrastructure, increasing operational demands on security teams. These complexities affect deployment consistency, compliance management, and long-term cybersecurity effectiveness. Software providers must invest in unified management consoles, cross-platform security frameworks, AI-assisted administration, and strategic cloud partnerships to maintain scalable and resilient enterprise protection.

AI Threat Detection Expands Nearly 63% of newly deployed enterprise antivirus platforms now incorporate behavioral AI analytics, reducing malware detection time by approximately 41%. Growing ransomware sophistication and expanding hybrid workforces are encouraging vendors to automate threat classification while increasing investment in machine learning-driven security operations.

Cloud Security Consolidates Approximately 58% of enterprise customers now prefer cloud-managed endpoint protection, reducing administrative workloads by nearly 34%. Organizations in the United Kingdom are consolidating standalone security tools into unified platforms, prompting vendors to expand cloud infrastructure, subscription services, and integrated policy management capabilities.

Zero Trust Integration Grows Around 49% of enterprise antivirus deployments are now integrated with Zero Trust security frameworks, improving access verification efficiency by approximately 27%. Regulatory compliance requirements and increasing identity-based attacks are accelerating partnerships between endpoint security providers and identity management platform vendors.

Security Automation Becomes Standard Automated remediation capabilities are now available in approximately 54% of premium antivirus platforms, reducing manual investigation efforts by nearly 32%. Enterprises increasingly prioritize platforms combining endpoint protection, XDR, and centralized threat intelligence, leading software vendors to strengthen AI development, platform integration, and enterprise-focused cybersecurity ecosystems.

Cloud-based antivirus software accounted for approximately 58% of the global computer antivirus software market in 2025, establishing itself as the dominant deployment model due to centralized management, real-time threat intelligence, lower maintenance requirements, and seamless scalability across distributed enterprise environments. Organizations increasingly prefer cloud-native platforms because they eliminate frequent signature updates while enabling continuous security monitoring. On-premise antivirus solutions remain strategically relevant for government agencies, defense organizations, and highly regulated industries requiring complete control over sensitive data and isolated network environments.

Cloud-native platforms are also the fastest-growing segment as hybrid workforces and multi-cloud infrastructures continue expanding. Nearly 66% of new enterprise endpoint security deployments now favor cloud-managed protection, while automated cloud policy enforcement improves administrative efficiency by approximately 34%. Vendors are investing in AI-enabled cloud security platforms, expanding regional data centers, and partnering with managed security providers to strengthen service delivery. Investment priorities continue shifting toward subscription-based security ecosystems that combine endpoint protection, threat intelligence, and centralized policy management.

According to a 2026 enterprise cybersecurity assessment by the Cloud Security Alliance, most large organizations now prioritize cloud-delivered endpoint protection to improve security visibility and simplify management across distributed enterprise environments.

Enterprise endpoint protection represented approximately 46% of the global computer antivirus software market in 2025, reflecting sustained investment in securing employee devices, servers, and corporate networks against ransomware, phishing, and advanced persistent threats. Financial institutions, healthcare providers, manufacturing companies, and government agencies continue concentrating cybersecurity spending on endpoint protection because compromised endpoints remain one of the most common attack vectors. Individual consumer protection remains a mature segment, while small business deployments continue expanding through simplified subscription-based security services.

Cloud workload protection has emerged as the fastest-growing application as organizations migrate business-critical operations to public and private cloud environments. Approximately 41% of enterprise security investments now include integrated cloud endpoint security, while AI-assisted threat response improves detection accuracy by nearly 37%. Vendors are expanding unified security platforms, integrating endpoint detection with identity management, and strengthening automation capabilities to support increasingly complex enterprise environments. Demand is shifting toward platforms capable of protecting users, workloads, and connected devices through a single security framework.

A 2025 enterprise security survey by the Information Systems Security Association reported that endpoint protection remains among the highest cybersecurity investment priorities as organizations expand cloud operations and hybrid work environments.

Large enterprises accounted for approximately 61% of the global computer antivirus software market in 2025 due to extensive endpoint footprints, stringent compliance obligations, and continuous exposure to sophisticated cyber threats. These organizations require centralized security management, AI-driven threat detection, and integrated security operations across geographically distributed infrastructure. Government agencies and critical infrastructure operators maintain stable demand because uninterrupted cybersecurity protection is essential for operational continuity, while educational institutions and healthcare organizations continue increasing endpoint security investments.

Small and medium-sized enterprises represent the fastest-growing end-user segment as cloud-based security platforms reduce implementation complexity and subscription pricing improves accessibility. Nearly 52% of SMEs now prefer managed antivirus services, while automated security administration reduces routine IT workloads by approximately 29%. Vendors are responding through scalable licensing models, managed detection partnerships, and industry-specific security packages designed for healthcare, retail, financial services, and manufacturing. Competitive positioning increasingly depends on delivering enterprise-grade protection through simplified deployment and predictable operating costs.

According to a 2026 enterprise cybersecurity study by the International Data Corporation (IDC), small and medium-sized businesses accelerated adoption of cloud-managed endpoint security platforms as cyber risk and compliance requirements continued increasing.

North America accounted for the largest market share at 38.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Enterprise AI Security Platforms Drive Market Leadership

North America accounted for approximately 38.2% of the global computer antivirus software market in 2025, supported by advanced cybersecurity infrastructure, widespread cloud adoption, and continuous enterprise investment in endpoint protection. Financial services, healthcare, government, and technology enterprises continue deploying AI-enabled antivirus platforms integrated with XDR and Zero Trust architectures to improve cyber resilience. Nearly 71% of large enterprises in the region have adopted centralized cloud-managed endpoint security, while managed security services continue expanding across mid-sized businesses. Software vendors are strengthening regional cloud infrastructure, investing in AI-powered threat intelligence, and expanding strategic cybersecurity partnerships to improve automated detection and incident response capabilities across increasingly distributed enterprise environments.

United States Market Outlook: The United States leads the regional market through strong enterprise cybersecurity spending, mature cloud infrastructure, and rapid adoption of AI-enabled endpoint protection. Approximately 78% of Fortune 500 organizations deploy integrated endpoint security platforms supporting centralized threat management and automated remediation. Continued investment in federal cybersecurity modernization and critical infrastructure protection encourages vendors to expand security operations, AI research, and enterprise-focused security service portfolios.

Regulatory Compliance Strengthens Enterprise Security Modernization

Europe represented approximately 27.6% of the global computer antivirus software market in 2025, driven by strict cybersecurity regulations, expanding digital infrastructure, and enterprise migration toward cloud-managed endpoint security. Organizations are replacing legacy antivirus software with integrated security platforms capable of supporting compliance, identity protection, and automated threat response. Approximately 62% of medium and large enterprises have adopted centralized endpoint security management, improving policy consistency and operational visibility. Vendors continue expanding regional cloud hosting capabilities and compliance-focused security services while strengthening partnerships with enterprise technology providers.

Germany Market Outlook: Germany remains Europe's leading market owing to its strong industrial economy, advanced enterprise IT infrastructure, and rigorous cybersecurity compliance standards. Approximately 29% of enterprise cybersecurity deployments within Europe are concentrated in Germany. Manufacturing, automotive, and industrial enterprises continue investing in AI-assisted endpoint protection and operational technology security to strengthen production resilience while meeting increasingly stringent digital security requirements.

Digital Transformation Expands Enterprise Security Deployment

Asia-Pacific accounted for approximately 24.8% of the global computer antivirus software market, supported by accelerating digital transformation, expanding cloud infrastructure, and rapid enterprise technology adoption. Growing investments in banking, telecommunications, e-commerce, and manufacturing are increasing demand for scalable endpoint protection platforms capable of securing distributed workforces. Approximately 57% of newly deployed enterprise security platforms in the region now include AI-assisted threat detection capabilities. Software providers are expanding regional data centers, strengthening cloud partnerships, and developing localized cybersecurity services to support rapidly growing enterprise demand.

China Market Outlook: China leads the regional market through its large digital economy, expanding enterprise cloud adoption, and significant investment in cybersecurity infrastructure. More than 65% of large domestic enterprises have implemented centralized endpoint protection across business operations. Local software vendors continue enhancing AI-driven malware detection, cloud security integration, and enterprise cybersecurity platforms while supporting national digital security initiatives across critical industries.

Enterprise Digitalization Expands Security Investments

South America accounted for approximately 5.2% of the global computer antivirus software market, supported by increasing enterprise digitalization, cloud migration, and stronger cybersecurity awareness across financial services, retail, and public administration. Organizations are prioritizing endpoint protection to address rising ransomware incidents while modernizing legacy IT infrastructure. Approximately 43% of medium-sized enterprises have adopted cloud-managed antivirus platforms, improving centralized security management and operational efficiency. Software vendors are strengthening regional partner ecosystems, expanding managed security offerings, and introducing subscription-based security solutions tailored to cost-sensitive organizations.

Brazil Market Outlook: Brazil represents the largest market in South America due to its extensive enterprise base, expanding digital banking sector, and accelerating cloud adoption. Approximately 54% of enterprise endpoint security deployments within the region are concentrated in Brazil. Domestic organizations continue investing in AI-enabled antivirus platforms, security automation, and managed cybersecurity services to strengthen resilience against increasingly sophisticated cyber threats.

Critical Infrastructure Security Drives Market Expansion

The Middle East & Africa accounted for approximately 4.2% of the global computer antivirus software market, supported by government digital transformation initiatives, modernization of critical infrastructure, and increasing cybersecurity investment across financial services, energy, and telecommunications. Organizations are adopting integrated endpoint protection to secure expanding cloud environments and mission-critical operations. Approximately 39% of enterprise cybersecurity modernization projects now include AI-powered endpoint protection platforms. Vendors are expanding regional cybersecurity operations, strengthening local technology partnerships, and enhancing managed detection capabilities to support evolving enterprise security requirements.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through large-scale digital transformation programs, smart infrastructure investments, and strengthened national cybersecurity frameworks. Nearly 36% of enterprise cybersecurity projects across the Gulf Cooperation Council are concentrated in Saudi Arabia. Public sector organizations, energy companies, and financial institutions continue deploying advanced endpoint security platforms integrated with cloud infrastructure and centralized security operations to strengthen national cyber resilience.

Microsoft, Gen Digital, Bitdefender, ESET, and Trend Micro compete aggressively through AI-powered detection, cloud-native security, and integrated endpoint platforms, while regional vendors emphasize affordability and localized compliance. The top five companies collectively hold approximately 57% of the global market. Competition centers on detection accuracy, automation, and ecosystem integration, with AI-assisted threat analysis improving detection efficiency by nearly 43% and automated response reducing incident handling time by approximately 35%. Cloud-managed deployments influence over 64% of enterprise purchasing decisions, accelerating platform consolidation. Vendors are expanding security operations, acquiring AI capabilities, forming cloud partnerships, and integrating XDR, identity protection, and Zero Trust frameworks into unified offerings. The competitive shift has moved decisively from signature-based antivirus toward intelligent cybersecurity platforms delivering continuous threat intelligence. High research investment, global threat intelligence networks, regulatory certifications, and enterprise integration capabilities remain significant entry barriers. Winning requires superior AI-driven protection, scalable cloud architecture, rapid threat response, and trusted enterprise ecosystems.

Microsoft

Gen Digital

Bitdefender

ESET

Trend Micro

McAfee

Malwarebytes

F-Secure

Sophos

Kaspersky

WatchGuard Technologies

VIPRE Security Group

G DATA CyberDefense

K7 Computing

Artificial intelligence, behavioral analytics, cloud-native endpoint protection, and Extended Detection and Response (XDR) are redefining computer antivirus software. Approximately 68% of enterprise deployments now incorporate AI-assisted malware detection, reducing threat investigation time by nearly 41%. Cloud-managed endpoint security has reached approximately 61% enterprise adoption, enabling centralized policy enforcement, continuous updates, and faster incident response. Integration with identity security, email protection, and security operations platforms creates measurable operational advantages through unified visibility and automated remediation.

Behavior-based detection significantly outperforms traditional signature-based antivirus by identifying previously unknown threats approximately 46% faster while reducing false-positive alerts by nearly 32%. Vendors with advanced AI models and global threat intelligence networks gain a competitive advantage through faster protection updates and more accurate risk prioritization. Cloud-native architectures also reduce endpoint management effort by approximately 28%, making them increasingly attractive for enterprises managing hybrid workforces and distributed infrastructure.

Between 2026 and 2028, autonomous threat hunting, generative AI security assistants, and predictive cyber risk analytics will become mainstream across enterprise security platforms. Nearly 72% of large organizations are expected to prioritize unified endpoint protection integrated with identity, cloud workload, and network security. Organizations investing today in AI-native security architecture, automation, and interoperable cybersecurity ecosystems will improve operational resilience, accelerate incident containment, and strengthen long-term competitive positioning.

April 2025 Bitdefender globally launched GravityZone PHASR, introducing user-tailored endpoint hardening to combat living-off-the-land attacks responsible for over 70% of major security incidents, strengthening enterprise attack surface reduction capabilities. Source: bitdefender.com (Bitdefender)

April 2025 Microsoft expanded Microsoft Defender XDR with new AI-powered security operations capabilities, enhanced endpoint protection tools, and improved security content management, strengthening automated enterprise threat detection and operational efficiency. Source: techcommunity.microsoft.com (TECHCOMMUNITY.MICROSOFT.COM)

April 2025 AV-TEST certified multiple enterprise antivirus platforms after achieving the maximum 18-point rating across protection, performance, and usability, reinforcing competitive differentiation through independently validated endpoint security effectiveness. Source: av-test.org (AV-TEST)

June 2025 Microsoft announced a new Windows security platform that moves antivirus and endpoint detection software outside the Windows kernel following the CrowdStrike disruption affecting 8.5 million devices, improving long-term platform resilience through industry collaboration. Source: theverge.com (The Verge)

The report provides comprehensive coverage of the computer antivirus software market across deployment types, including cloud-based and on-premise solutions, while evaluating applications such as enterprise endpoint protection, consumer security, server protection, and cloud workload security. End-user analysis spans large enterprises, small and medium-sized businesses, government organizations, healthcare, financial services, education, and industrial sectors. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by country-level deployment trends, enterprise adoption patterns, and competitive benchmarking. More than 60% of enterprise security assessments emphasize cloud-native and AI-enabled endpoint protection strategies.

The study evaluates emerging technologies including behavioral analytics, artificial intelligence, XDR, Zero Trust integration, automated threat response, and cloud-managed endpoint security. It benchmarks leading cybersecurity vendors, technology innovation, deployment strategies, and ecosystem partnerships while assessing enterprise purchasing priorities, platform adoption, and competitive positioning. The report supports investment planning, product development, market expansion, cybersecurity strategy, and long-term decision-making across the global computer antivirus software market between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6,238.2 Million |

|

Market Revenue in 2033 |

USD 11,376.5 Million |

|

CAGR (2026 - 2033) |

7.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft, Gen Digital, Bitdefender, ESET, Trend Micro, McAfee, Malwarebytes, F-Secure, Sophos, Kaspersky, WatchGuard Technologies, VIPRE Security Group, G DATA CyberDefense, K7 Computing |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |