Reports

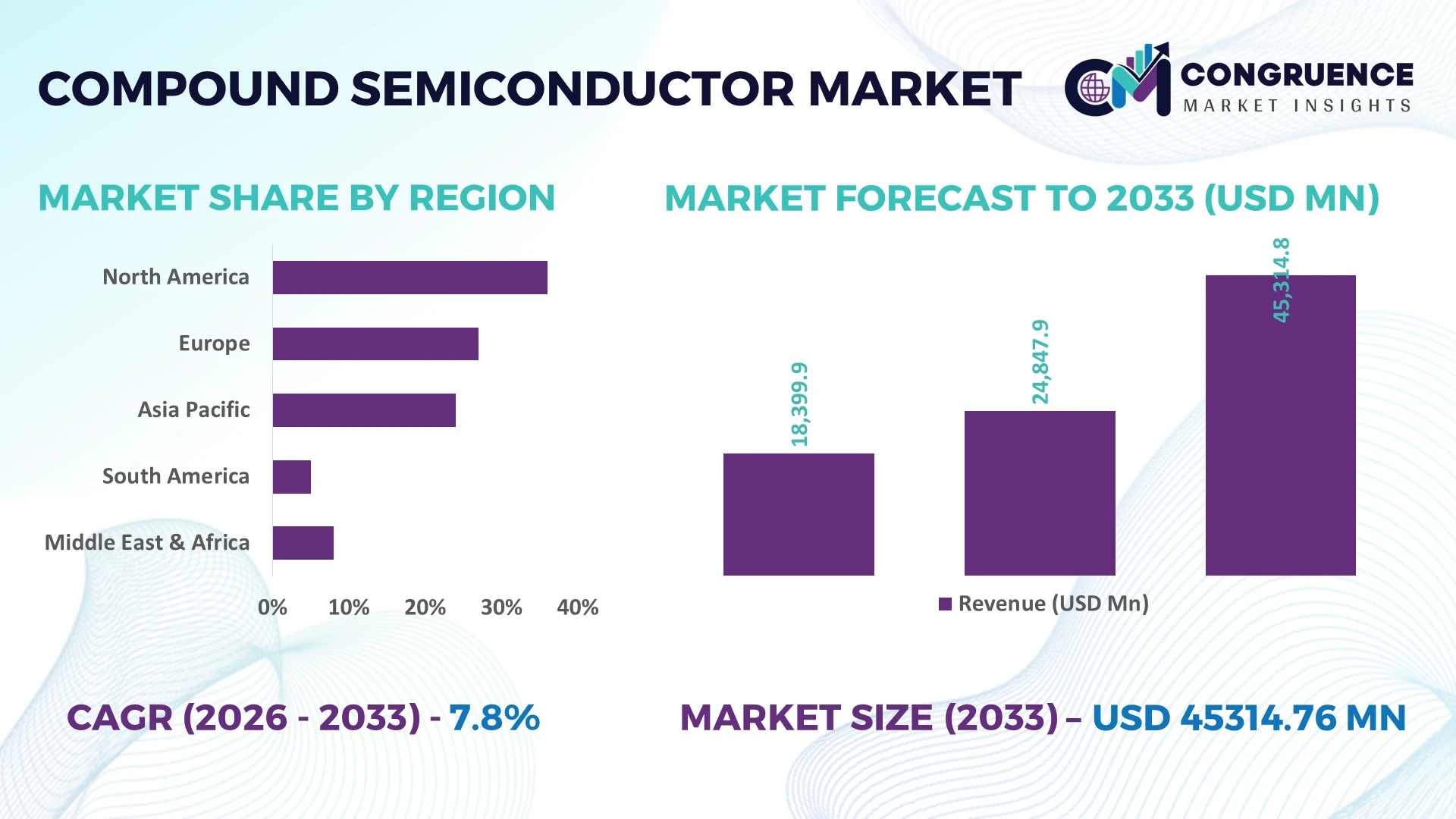

The Global Compound Semiconductor Market was valued at USD 24847.9 Million in 2025 and is anticipated to reach a value of USD 45314.76 Million by 2033 expanding at a CAGR of 7.8% between 2026 and 2033. Rising deployment of gallium nitride (GaN) and silicon carbide (SiC) devices across electric vehicles, 5G infrastructure, AI data centers, renewable energy systems, and advanced defense electronics is accelerating high-performance compound semiconductor production and capacity expansion.

China remains the dominant country, accounting for approximately 36% of global manufacturing capacity, supported by multi-billion-dollar investments in power electronics, EV supply chains, and telecom infrastructure. Japan retains leadership in advanced semiconductor materials, while the United States strengthens domestic fabrication through strategic industrial policies following global supply chain realignment. More than 55% of next-generation power devices are now concentrated across East Asia, reinforcing regional manufacturing leadership.

Strategic investment in resilient supply chains, advanced wafer production, and material innovation remains essential for sustaining long-term competitive advantage.

Market Size & Growth: USD 24,847.9 million (2025) to USD 45,314.76 million (2033) at 7.8% CAGR, driven by expanding GaN and SiC power electronics adoption.

Top Growth Drivers: EV semiconductor demand +28%, AI infrastructure deployment +24%, renewable power electronics expansion +21%.

Short-Term Forecast: By 2028, device efficiency improves 18% while manufacturing costs decline nearly 12% through larger wafer production.

Emerging Technologies: AI-enabled fabrication, 200mm SiC wafers, advanced GaN-on-silicon processes accelerate high-growth semiconductor manufacturing.

Regional Leaders: Asia-Pacific exceeds USD 22 billion, North America approaches USD 10 billion, Europe surpasses USD 7 billion through industrial electrification.

Consumer/End-User Trends: Over 48% of demand originates from EVs, telecom infrastructure, and industrial automation applications.

Pilot/Case Example: 2026 manufacturing expansion improved wafer throughput by 20% while reducing production cycle time by 15%.

Competitive Landscape: Top manufacturers control nearly 46% market share, led by Infineon, Wolfspeed, STMicroelectronics, onsemi, and ROHM.

Regulatory & ESG Impact: Energy-efficient semiconductor policies reduce power losses by nearly 30% across high-voltage applications amid regional supply-chain diversification.

Investment & Funding: More than USD 15 billion supports fab expansion, strategic partnerships, and advanced material production worldwide.

Innovation & Future Outlook: Vertical integration, heterogeneous integration, and next-generation wide-bandgap materials strengthen global competitiveness and long-term technology leadership.

Growing demand from electric mobility, renewable energy conversion, aerospace electronics, AI computing infrastructure, and high-frequency communications continues to reshape the Compound Semiconductor Market. Innovations in 200mm silicon carbide wafers and advanced gallium nitride devices improve manufacturing scalability, while over 40% of new capacity targets automotive applications. Ongoing supply-chain localization and industrial policy initiatives further strengthen long-term strategic positioning across major manufacturing regions.

Compound semiconductors have become a strategic technology foundation for electrification, AI computing, high-frequency communications, and advanced industrial systems, making them central to global manufacturing competitiveness. Supply-chain restructuring since 2023 has accelerated domestic fabrication programs in the United States, Japan, and Europe, while governments prioritize resilient semiconductor ecosystems over import dependence. This shift is reshaping investment priorities as manufacturers expand wafer production, secure critical materials, and strengthen technology partnerships to support long-term industrial resilience.

Compared with conventional silicon devices, silicon carbide power semiconductors reduce switching losses by nearly 50% and improve power conversion efficiency by approximately 10% in high-voltage applications, lowering cooling requirements and system operating costs. China leads manufacturing scale through integrated supply chains, while Japan maintains technological leadership in substrate quality and material processing. Over the next two to three years, 200mm silicon carbide wafer production is expected to exceed 30% of total industry output, improving manufacturing efficiency and supporting broader commercial deployment.

Electric vehicle manufacturers are increasingly integrating gallium nitride and silicon carbide components into onboard charging and traction inverter platforms to enhance energy efficiency and system reliability. In response, semiconductor companies are expanding fabrication capacity, forming long-term supply agreements, and investing in advanced packaging technologies. Organizations that combine material innovation, manufacturing scale, and diversified supply networks will strengthen competitive positioning while securing sustained operational advantages across high-value electronics markets.

Rapid electrification across automotive, renewable energy, and industrial automation is accelerating demand for compound semiconductors capable of operating under higher voltages and temperatures. Silicon carbide devices improve inverter efficiency by nearly 10%, while gallium nitride components reduce power losses by approximately 30% in high-frequency applications. China continues expanding domestic power semiconductor production, while the United States supports fabrication through industrial policy and advanced manufacturing incentives. These structural shifts are prompting companies to invest in larger wafer production, advanced packaging, and strategic partnerships with automotive OEMs. A notable operational trend is the integration of semiconductor suppliers into vehicle development cycles, enabling faster product qualification and improving long-term supply security for critical electronic systems.

High substrate costs and concentrated raw material processing continue to constrain large-scale deployment of compound semiconductors. Silicon carbide wafer prices remain approximately 35% higher than comparable silicon alternatives, while substrate defect rates still exceed 8% for some production grades, limiting manufacturing yields. Dependence on specialized material suppliers in China creates procurement uncertainty for global manufacturers during trade or export policy adjustments. These constraints increase production costs, extend qualification timelines, and reduce pricing flexibility. Companies are responding by localizing substrate production, securing long-term procurement agreements, and qualifying multiple material suppliers to improve resilience. Investment in higher-yield crystal growth technologies also supports better operational efficiency and manufacturing consistency.

Expansion of AI infrastructure, smart grids, fast-charging networks, and industrial electrification is creating new commercial opportunities beyond traditional automotive demand. More than 40% of new high-power semiconductor design activity targets energy-efficient infrastructure, while automated manufacturing can improve production throughput by approximately 20%. Japan and Germany are strengthening collaborative research programs focused on next-generation gallium oxide and advanced compound materials capable of higher voltage performance. Companies are increasing investment in R&D, pilot production lines, and ecosystem partnerships to commercialize emerging technologies. A significant strategic opportunity lies in integrated power modules combining advanced materials with intelligent control systems, enabling greater efficiency across industrial and utility-scale applications.

Expanding compound semiconductor manufacturing requires highly specialized process expertise, advanced equipment, and rigorous quality control that remain difficult to scale consistently. Qualification cycles for automotive-grade components frequently exceed 18 months, while fabrication facilities require equipment utilization above 85% to maintain operational efficiency. The United States and several European manufacturing hubs continue facing shortages of experienced semiconductor process engineers, slowing technology deployment. Companies must also address increasingly complex packaging, thermal management, and reliability validation requirements as device performance advances. Strategic investment in workforce development, digital manufacturing platforms, collaborative research, and automated quality inspection will be essential for maintaining production consistency and long-term global competitiveness.

Advanced Wafer Scaling Accelerates Production is shifting toward 200mm silicon carbide wafers, with output capacity increasing by nearly 30% and wafer utilization improving around 18%. Equipment suppliers are automating crystal growth and inspection processes to improve yield consistency. Expansion incentives in the United States and Japan, combined with supply-chain diversification, are encouraging manufacturers to establish localized production and reduce dependence on single-country sourcing.

AI Manufacturing Improves Yield Semiconductor manufacturers are integrating AI-driven process control and predictive maintenance, reducing defect rates by approximately 15% while increasing production throughput by nearly 20%. Automated optical inspection now shortens quality verification cycles by over 25%. Companies are expanding digital manufacturing platforms and collaborating with equipment vendors to improve operational efficiency amid growing demand for high-performance power devices.

Automotive Platform Integration Expands Electric vehicle manufacturers are standardizing silicon carbide power modules across multiple vehicle platforms, lowering inverter size by about 20% and improving energy efficiency by nearly 8%. Tighter emissions regulations and battery performance targets are accelerating design transitions. Semiconductor suppliers are responding through long-term automotive partnerships, dedicated packaging facilities, and vertically integrated manufacturing strategies to secure qualified component supply.

Advanced Packaging Gains Priority Demand for high-density packaging and heterogeneous integration is increasing as thermal performance and power density become critical differentiators. Advanced packaging adoption has risen by roughly 22%, while module assembly cycle times have declined by nearly 12% through automation. Companies are restructuring production workflows and investing in co-development partnerships, recognizing packaging innovation as a competitive advantage rather than a downstream manufacturing function.

Silicon Carbide (SiC) remains the leading segment because of its superior efficiency, thermal conductivity, and suitability for high-voltage power conversion across electric vehicles, renewable energy systems, and industrial drives. Nearly 48% of newly designed high-power semiconductor platforms now incorporate SiC devices due to lower switching losses and improved operating temperatures. Gallium Nitride (GaN) is the fastest-growing type as demand expands across fast chargers, AI servers, and telecom infrastructure, where compact size and high-frequency performance provide measurable system advantages. Manufacturers are increasing investment in larger wafer production and advanced epitaxy to improve yields and reduce manufacturing costs.

Gallium Arsenide (GaAs) maintains strategic importance in RF communications and satellite systems, while Indium Phosphide (InP) supports high-speed optical communication and photonic integration. Gallium Phosphide (GaP) continues serving specialized optoelectronic applications despite its comparatively smaller deployment scale. Companies are balancing mature product portfolios with next-generation material investments, strengthening long-term competitiveness through technology diversification and collaborative material development.

Power Electronics represents the dominant application due to extensive deployment in electric mobility, renewable energy conversion, industrial automation, and grid infrastructure. Approximately 46% of compound semiconductor demand is linked to high-efficiency power conversion systems requiring lower energy losses and higher thermal stability. Electric Vehicles constitute the fastest-growing application as manufacturers integrate silicon carbide traction inverters and onboard charging systems to improve driving range and charging performance. Companies are expanding production capacity, qualifying automotive-grade components, and strengthening partnerships with vehicle manufacturers to support increasing platform standardization.

RF Devices continue supporting advanced wireless communication, while 5G Infrastructure expands demand for gallium nitride-based high-frequency amplifiers with greater power efficiency. Optoelectronics remains strategically important for optical networking, sensing, and laser technologies. Suppliers are increasingly integrating application-specific product development with customer engineering programs, enabling faster deployment and improving long-term commercial relationships across multiple industrial sectors.

Automotive remains the largest end-user segment as electric vehicle production, charging infrastructure, and advanced powertrain systems increasingly rely on compound semiconductors for higher efficiency and thermal performance. Around 44% of industry demand originates from automotive manufacturing, where silicon carbide devices enhance inverter performance and improve energy utilization. Telecommunications is the fastest-growing end-user as network modernization and AI-enabled data traffic accelerate deployment of gallium nitride components in high-frequency communication equipment. Companies are responding through dedicated automotive qualification programs, long-term supply agreements, and application-specific product customization.

Industrial manufacturers continue expanding adoption across motor drives, robotics, and renewable energy systems, while Aerospace & Defense prioritizes high-reliability electronic systems capable of operating in demanding environments. Consumer Electronics increasingly integrates gallium nitride solutions into compact fast-charging products, improving efficiency while reducing device size. Suppliers are strengthening ecosystem partnerships and differentiated product portfolios to address varying operational requirements across these established and emerging customer groups.

Asia-Pacific accounted for the largest market share at 58.4% in 2025 however, North America is expected to register the fastest growth, expanding at a 9.1% CAGR between 2026 and 2033.

Advanced Domestic Manufacturing and AI Infrastructure Expansion

North America is strengthening its position through domestic semiconductor manufacturing, AI infrastructure expansion, and increasing adoption of wide-bandgap power devices across electric vehicles and defense electronics. The region contributes approximately 22% of global compound semiconductor production, supported by integrated research ecosystems and advanced fabrication facilities. More than 35% of newly announced semiconductor capacity additions target power electronics and high-performance computing applications. Manufacturers continue expanding wafer processing, advanced packaging, and strategic partnerships with automotive and cloud infrastructure companies, improving supply resilience while accelerating commercialization of next-generation compound semiconductor technologies.

United States Market Outlook: The United States leads regional deployment through advanced semiconductor fabrication, federal manufacturing incentives, and strong collaboration between technology companies, automotive manufacturers, and research institutions. More than 40% of domestic investment in new semiconductor facilities targets advanced materials and power devices. Companies are expanding silicon carbide and gallium nitride production while strengthening local supply chains, enabling greater manufacturing independence and supporting rapid deployment across AI infrastructure, aerospace, industrial automation, and electrified transportation systems.

Industrial Electrification and Technology Sovereignty

Europe continues advancing compound semiconductor deployment through industrial electrification, automotive innovation, and semiconductor manufacturing resilience. The region accounts for nearly 18% of global market activity, supported by advanced automotive supply chains and coordinated industrial policies. More than 30% of recent manufacturing investments focus on silicon carbide production for electric mobility and renewable energy applications. Companies are increasing collaboration between material suppliers, equipment manufacturers, and automotive OEMs to improve production efficiency while strengthening regional technology independence and reducing strategic supply-chain exposure.

Germany Market Outlook: Germany remains Europe's industrial center for compound semiconductor adoption due to its strong automotive manufacturing base, precision engineering capabilities, and expanding semiconductor ecosystem. Approximately 45% of regional automotive semiconductor development projects involve German manufacturers and suppliers. Continued investment in electric mobility, industrial automation, and advanced power electronics enables companies to commercialize higher-efficiency semiconductor solutions while supporting long-term manufacturing competitiveness across strategic export industries.

Manufacturing Scale and Supply Chain Leadership

Asia-Pacific dominates the global market through integrated manufacturing ecosystems, extensive electronics production, and vertically coordinated supply chains. The region represents approximately 58.4% of worldwide market activity, supported by large-scale wafer fabrication and advanced material processing capabilities. More than 55% of global silicon carbide substrate production is concentrated across key manufacturing hubs, enabling efficient supply for automotive, telecommunications, and industrial applications. Enterprises continue expanding production capacity, automation, and export capabilities while investing in next-generation materials to reinforce long-term technological leadership.

China Market Outlook: China maintains the strongest competitive position through extensive manufacturing capacity, vertically integrated semiconductor supply chains, and sustained industrial investment. Nearly 36% of global compound semiconductor manufacturing capacity is located within China, supported by expanding electric vehicle production and telecommunications infrastructure. Domestic companies continue investing in substrate manufacturing, epitaxy, and device fabrication while accelerating technology localization to strengthen industrial self-sufficiency and improve resilience against external supply disruptions.

Industrial Modernization Drives Emerging Demand

South America is gradually increasing compound semiconductor adoption through renewable energy projects, industrial automation, and expanding electric mobility initiatives. The region contributes a relatively modest share of global deployment but continues improving technology adoption within power electronics and telecommunications infrastructure. Approximately 18% of new industrial modernization projects incorporate advanced power management technologies requiring higher-efficiency semiconductor components. Companies are entering strategic partnerships with international suppliers while balancing infrastructure expansion with manufacturing limitations and import dependency.

Brazil Market Outlook: Brazil represents the region's largest opportunity through expanding industrial manufacturing, renewable energy investments, and growing electric mobility adoption. National infrastructure modernization programs continue increasing demand for efficient power conversion technologies across utilities and industrial facilities. Semiconductor distributors and technology providers are strengthening local engineering support, application development, and supply partnerships to improve deployment efficiency while supporting the country's long-term industrial digitalization objectives.

Infrastructure Investment Supports Technology Adoption

The Middle East & Africa market is expanding through digital infrastructure investment, smart city development, renewable energy integration, and industrial diversification strategies. Although representing a smaller share of global demand, deployment of advanced power electronics continues increasing across utilities, transportation, and telecommunications. More than 20% of recently announced smart infrastructure projects include advanced energy management systems utilizing high-efficiency semiconductor technologies. International technology partnerships and localized engineering initiatives are improving technical capabilities while supporting long-term infrastructure modernization objectives.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market development through ambitious industrial diversification, renewable energy deployment, and digital infrastructure investment. Large-scale smart city and utility modernization programs are increasing demand for advanced power electronics capable of improving operational efficiency and energy reliability. Technology companies are expanding regional partnerships, engineering services, and solution integration capabilities while supporting local manufacturing initiatives that strengthen national technology capacity and long-term industrial competitiveness.

Global leaders including Wolfspeed, Infineon Technologies, STMicroelectronics, onsemi, and ROHM compete directly in high-performance power semiconductors, while Asian material specialists challenge established suppliers through manufacturing scale and cost efficiency. Technology innovators focus on silicon carbide and gallium nitride advancement, whereas cost-driven manufacturers emphasize substrate availability and production economics. The top five players collectively control approximately 46% of the market, creating intense competition across automotive, industrial, and telecommunications applications. Performance leadership increasingly outweighs price alone, with manufacturers achieving nearly 20% faster product qualification and around 15% higher production yields through advanced process optimization. Vertical integration improves supply reliability by approximately 25%, encouraging strategic investment in substrate production, epitaxy, and packaging. Competition is shifting toward long-term supply agreements, joint development partnerships, and localized manufacturing as customers prioritize resilient sourcing. High capital requirements, complex qualification standards, and specialized material expertise remain significant entry barriers. Success depends on combining manufacturing scale, technology leadership, dependable supply chains, and application-specific engineering capabilities.

Wolfspeed, Inc.

Infineon Technologies AG

STMicroelectronics N.V.

onsemi

ROHM Co., Ltd.

Qorvo, Inc.

Skyworks Solutions, Inc.

Sumitomo Electric Industries, Ltd.

Coherent Corp.

NXP Semiconductors N.V.

Mitsubishi Electric Corporation

MACOM Technology Solutions Holdings, Inc.

Wide-bandgap semiconductor technologies remain the primary innovation driver, with silicon carbide and gallium nitride replacing conventional silicon in demanding power applications. Silicon carbide devices improve power conversion efficiency by approximately 10% while reducing switching losses by nearly 50% compared with legacy silicon components. Around 45% of new electric vehicle powertrain platforms now integrate wide-bandgap devices, enabling higher operating temperatures, compact system designs, and lower cooling requirements. Automotive manufacturers, industrial equipment suppliers, and renewable energy developers benefit through improved operational efficiency and reduced lifecycle costs.

Emerging technologies include 200mm silicon carbide wafers, AI-enabled semiconductor manufacturing, heterogeneous integration, and advanced packaging. Automated process control improves production yields by nearly 15%, while digital inspection reduces manufacturing defects by approximately 20%. Adoption of advanced packaging continues expanding as power density and thermal management become critical design priorities. Companies investing in vertically integrated manufacturing, intelligent production systems, and advanced substrate engineering gain stronger competitive differentiation through faster commercialization and improved manufacturing consistency.

Between 2026 and 2028, photonic integration, gallium oxide research, and intelligent power modules will reshape high-performance electronics. Integrated semiconductor platforms are expected to improve overall system efficiency by approximately 12% compared with current architectures while reducing assembly complexity. Companies that accelerate deployment of advanced materials, automation, and collaborative technology ecosystems will secure stronger positions in automotive electrification, AI infrastructure, industrial automation, and next-generation communication networks before industry standards mature.

January 2024: Infineon Technologies and Wolfspeed expanded their long-term 150 mm silicon carbide wafer supply agreement by adding a multi-year capacity reservation covering both 150 mm and future 200 mm wafers, strengthening supply-chain resilience for automotive and energy applications. s

March 2024: Wolfspeed completed the structural topping-out of its John Palmour Silicon Carbide Manufacturing Center, designed for 200 mm wafer production with an approximately USD 5 billion planned investment, significantly increasing future manufacturing capability for advanced power semiconductors.

January 2025: Wolfspeed launched its Gen 4 silicon carbide MOSFET technology platform, delivering up to 21% lower on-resistance and 15% lower switching losses, enabling higher power density while reducing system development time and improving efficiency for industrial and automotive applications.

September 2025: Infineon Technologies and ROHM signed a memorandum of understanding to develop compatible silicon carbide power packages, with ROHM's DOT-247 package reducing thermal resistance by 15% and inductance by 50%, improving sourcing flexibility and accelerating customer adoption.

This report provides comprehensive analysis of the global Compound Semiconductor Market across Gallium Nitride (GaN), Silicon Carbide (SiC), Gallium Arsenide (GaAs), Indium Phosphide (InP), and Gallium Phosphide (GaP). It evaluates demand across power electronics, RF devices, optoelectronics, electric vehicles, and 5G infrastructure while assessing adoption patterns within automotive, telecommunications, consumer electronics, aerospace & defense, and industrial sectors. The assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing more than 95% of global industry activity.

The report analyzes technology evolution, manufacturing capacity expansion, supply-chain localization, advanced packaging, and wide-bandgap semiconductor deployment trends shaping the market between 2026 and 2033. It examines competitive positioning of leading manufacturers, strategic partnerships, production investments, and operational benchmarks while identifying emerging application opportunities, deployment priorities, and enterprise adoption trends. Business stakeholders gain actionable insights supporting investment decisions, product development strategies, regional expansion planning, supply-chain optimization, and long-term competitive positioning in the rapidly evolving compound semiconductor industry.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 24847.9 Million |

Market Revenue in 2033 | USD 45314.76 Million |

CAGR (2026 - 2033) | 7.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Wolfspeed, Inc., Infineon Technologies AG, STMicroelectronics N.V., onsemi, ROHM Co., Ltd., Qorvo, Inc., Skyworks Solutions, Inc., Sumitomo Electric Industries, Ltd., Coherent Corp., NXP Semiconductors N.V., Mitsubishi Electric Corporation, MACOM Technology Solutions Holdings, Inc. |

Customization & Pricing | Available on Request (10% Customization is Free) |