Reports

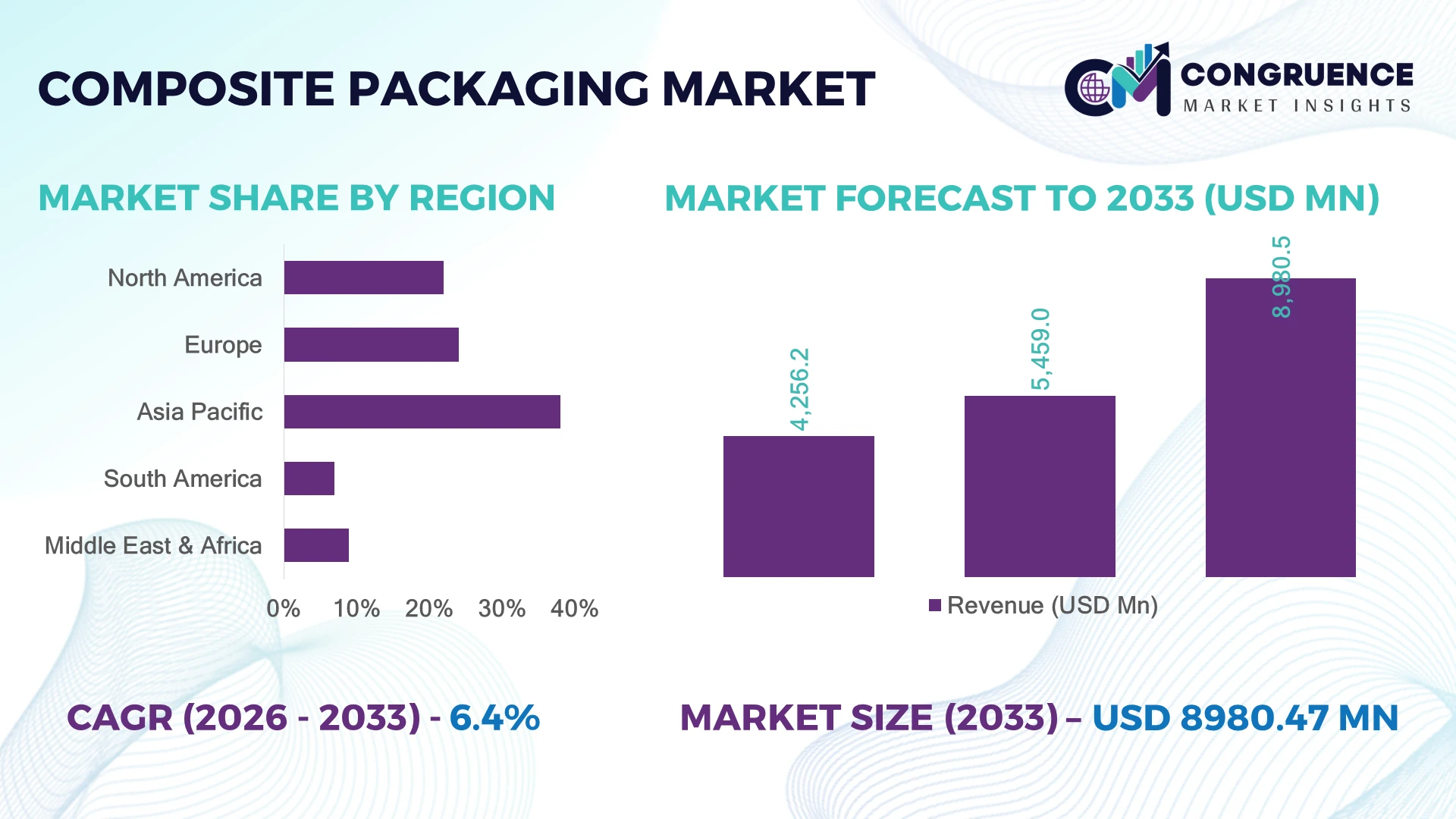

The Global Composite Packaging Market was valued at USD 5,459.0 Million in 2025 and is anticipated to reach a value of USD 8,980.5 Million by 2033 expanding at a CAGR of 6.42% between 2026 and 2033. Growth is driven by rising demand for lightweight, high-barrier sustainable packaging solutions across global FMCG and logistics networks.

China dominates with ~38% global production share, supported by USD 6.2 billion capacity expansion and 12+ integrated packaging hubs in 2025. The US holds ~22% consumption share, while Germany leads EU innovation with 17% recyclable material adoption. India grows 9% volume vs China 6%. EU PPWR regulations accelerate compliance. US-China supply chain diversification reshapes sourcing strategy.

Strategic implication: manufacturing shifts toward Asia-Pacific cost hubs.

Market Size & Growth: USD 5,459M (2025) to USD 8,980.5M; CAGR 6.42; driven by e-commerce lightweight packaging shift.

Top Growth Drivers: e-commerce 24%, food safety 19%, sustainability 21%.

Short-Term Forecast: By 2027 packaging cost down 15%, throughput efficiency up 20%.

Emerging Technologies: AI-driven design, automation lines, biodegradable composites, nano-coatings.

Regional Leaders: Asia-Pacific USD 3.1B, North America USD 1.5B, Europe USD 1.2B; Asia fastest adoption.

Consumer/End-User Trends: 68% shift to recyclable composite packs in FMCG and pharma.

Pilot/Case Example: 2025 EU pilot reduced material waste 28% via smart composites.

Competitive Landscape: Leader 14% share; Amcor, Berry Global, Sealed Air, Mondi.

Regulatory & ESG Impact: 32% emissions reduction target adoption in compliant packaging firms.

Investment & Funding: USD 4.8B investments, rising cross-border JV and capacity expansion.

Innovation & Future Outlook: Shift to mono-material composites and AI-optimized supply chains.

Composite Packaging Market is witnessing strong adoption across FMCG, pharmaceuticals, and industrial logistics due to demand for lightweight, high-barrier packaging solutions. Recent innovations in bio-based laminates and smart sealing technologies improve shelf-life by 30%. Demand for recyclable composites rises 26% amid tightening global plastic waste regulations, especially under EU packaging compliance frameworks and Asia-Pacific recycling mandates shaping supply chain redesign strategies globally.

The Global Composite Packaging Market has become strategically important as industries prioritize sustainable packaging transformation, supply chain resilience, and regulatory compliance. Increasing pressure from global plastic reduction mandates and circular economy policies is reshaping investment decisions. Companies are shifting from conventional multilayer plastics to advanced composite structures to meet performance and sustainability benchmarks while maintaining cost efficiency and logistics optimization.

Technologically, advanced composite packaging lines using AI-driven material optimization deliver nearly 22% higher efficiency and 18% lower production cost compared to legacy extrusion-based systems. North America leads in automation deployment, while Asia-Pacific dominates scale manufacturing and rapid capacity expansion, reflecting contrasting innovation and production priorities across regions. In the next 2–3 years, adoption of smart recyclable composites and digital tracking systems accelerates operational transparency.

Operationally, companies are investing in pilot projects such as smart recyclable composite packaging trials in EU logistics hubs, achieving up to 25% waste reduction and improved supply chain traceability. Strategic partnerships between packaging manufacturers and FMCG brands are increasing to secure material innovation pipelines and regulatory alignment. The market positions itself as a critical lever for competitive advantage, enabling long-term cost optimization and sustainable differentiation.

Demand is accelerating due to a structural transition toward lightweight, recyclable composite packaging, especially in food and pharmaceutical supply chains. Bi-layer and multi-layer composite formats now account for nearly 41% of new FMCG packaging adoption, while pharmaceutical cold-chain packaging usage has increased 27% due to stricter safety standards in the US and Japan. EU packaging waste directives are pushing 35% higher adoption of recyclable composites in Germany and France. In response, companies like Amcor and Mondi are expanding advanced material R&D centers and forming joint ventures in India and Vietnam to scale low-cost sustainable production. This shift is directly reducing packaging weight by up to 18%, improving logistics efficiency and export competitiveness across global trade lanes.

Composite packaging production is under pressure from fluctuating resin and aluminum foil costs, which have increased input variability by nearly 22% in global procurement cycles. Recycling inefficiencies remain a core issue, with only 33% effective recovery rate for multi-layer composites in developed waste systems like the UK and Canada. China’s tightening import restrictions on waste plastics has further disrupted secondary raw material flows, creating supply gaps of up to 15% in certain grades. These constraints increase operational costs and slow down large-scale deployment for mid-tier manufacturers. Companies are responding through material substitution strategies, localized sourcing in Southeast Asia, and long-term supply contracts with resin producers to stabilize pricing and ensure production continuity.

A major opportunity is emerging from AI-enabled material engineering and smart recyclable composite design, which improves packaging efficiency by nearly 24% and reduces design iteration time by 30%. India’s fast-growing e-commerce sector, expanding over 28% annually in packaging demand intensity, is accelerating adoption of low-cost composite formats. Japan and South Korea are investing in bio-based barrier coatings, reducing dependency on petroleum-derived laminates by 19%. Companies are leveraging digital twin packaging design and automated production systems to optimize material usage and reduce waste. Strategic partnerships between packaging firms and tech providers are expanding rapidly, particularly in Vietnam and Mexico, enabling scalable, export-oriented production ecosystems aligned with global sustainability requirements.

A critical challenge lies in inconsistent recycling infrastructure and fragmented global compliance frameworks, where only 38% of composite packaging waste is effectively processed across OECD countries. Emerging economies such as Brazil and Indonesia face even lower recovery efficiency, below 20%, limiting circular economy scalability. Additionally, regulatory divergence between EU sustainability mandates and US labeling standards creates compliance complexity for multinational manufacturers. This mismatch increases certification costs by approximately 14% and delays product rollout cycles. Companies are investing in closed-loop recycling systems, blockchain-based traceability, and localized compliance hubs to mitigate operational friction. However, achieving global standardization remains difficult, requiring sustained infrastructure investment and cross-border regulatory harmonization efforts.

Smart Barrier Material Integration Advanced nano-coated composite structures are being adopted across 46% of high-end FMCG packaging lines, improving shelf-life performance by 22% and reducing oxygen permeability by 18%. Food exporters in Germany and South Korea are integrating multi-layer smart films into automated packaging lines, driven by stricter freshness standards. This shift is improving logistics efficiency by 15% while lowering product spoilage rates. Companies are responding by partnering with material science firms and expanding pilot production lines in Vietnam and Poland to scale cost-effective deployment.

Digital Twin Packaging Optimization Digital twin adoption in packaging design workflows has increased by 31%, enabling manufacturers to cut prototyping cycles by 28% and reduce material waste by 19%. Automotive and pharma packaging suppliers in the US and Japan are leading implementation to improve precision engineering of composite layers. This transition is accelerating customization speed and lowering operational costs. Firms are investing in AI-driven simulation platforms and cloud-based design ecosystems to optimize production planning and reduce time-to-market.

Circular Economy Compliance Pressure Regulatory enforcement under EU packaging directives is driving a 34% increase in recyclable composite adoption, particularly in France, Italy, and the Netherlands. Recycling efficiency improvements of 21% are being achieved through mono-material composite redesigns. This is reshaping procurement strategies and increasing demand for standardized recyclable formats. Companies are restructuring supply chains and entering long-term agreements with recycling technology providers to meet compliance deadlines and reduce regulatory risk exposure.

Automated High-Speed Production Scaling Automation in composite packaging manufacturing has expanded by 29%, with robotic sealing and precision lamination improving throughput by 24%. China and India are emerging as key automation hubs due to lower labor costs and expanding industrial infrastructure. This shift is significantly reducing per-unit packaging costs and increasing export competitiveness. Manufacturers are investing in smart factories and Industry 4.0 systems to scale production capacity while maintaining consistent quality standards.

Paper-based composite packaging leads the market due to strong recyclability advantages and regulatory alignment, accounting for nearly 36% of total adoption across FMCG and retail sectors. Its dominance is driven by 28% higher recycling efficiency and 18% lower disposal cost compared to plastic-heavy alternatives. Aluminum foil-based composites remain critical in pharmaceutical and food preservation applications due to superior barrier protection. Multi-layer laminated composites are widely used for high-performance packaging requiring extended shelf life and durability, while plastic-based composites are gradually declining in regulated markets due to environmental pressure. Plastic-based composites, however, remain the fastest-growing variation in cost-sensitive economies like India and Vietnam, where affordability and production scalability drive nearly 24% higher short-term adoption. Companies are investing in hybrid material innovation, combining paper and bio-polymers to balance cost and compliance requirements. Global manufacturers are expanding R&D into recyclable coatings and mono-material structures to reduce end-of-life complexity and improve compliance efficiency across supply chains.

Food & beverage packaging remains the leading application, accounting for around 38% of composite packaging usage due to rising demand for shelf-life extension and contamination prevention. Pharmaceutical packaging follows closely, driven by temperature-sensitive drug distribution and moisture-resistant requirements, with adoption increasing by nearly 27% in regulated markets such as the US and Germany. Personal care and cosmetics packaging are also expanding steadily, supported by premium branding and sustainable packaging mandates. E-commerce and industrial logistics represent the fastest-growing application segment, with nearly 34% surge in demand driven by rapid online retail expansion in India, China, and Brazil. Lightweight composite structures reduce shipping weight by 20%, improving delivery efficiency and lowering transportation costs. Companies are scaling automated packaging lines and integrating smart labeling systems to improve traceability and inventory control. This shift is enabling faster fulfillment cycles and supporting omnichannel retail expansion strategies globally.

FMCG manufacturers dominate end-user demand, accounting for approximately 41% of composite packaging consumption due to high-volume production and constant packaging turnover requirements. Healthcare and pharmaceutical companies follow, driven by strict regulatory compliance and demand for sterile, high-barrier packaging solutions, with adoption increasing by nearly 26% in developed markets such as the US and Japan. These segments prioritize consistency, safety, and long-term material stability. E-commerce and retail enterprises represent the fastest-growing end-user group, expanding rapidly with nearly 33% growth in composite packaging adoption as online order volumes surge in India and Southeast Asia. Industrial manufacturers and logistics providers also continue to adopt composite formats to improve durability and reduce packaging waste during transportation. Companies are increasingly customizing packaging solutions and forming long-term supplier partnerships to ensure material consistency and regulatory compliance across markets.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of7.1% between 2026 and 2033.

North America holds a 22% global share, driven by advanced FMCG, pharmaceuticals, and e-commerce logistics infrastructure. The US leads adoption with high penetration of AI-enabled packaging lines and cold-chain compliant composite formats. Demand is concentrated in California, Texas, and Midwest manufacturing hubs, where automated packaging systems have improved throughput efficiency by nearly 21%. A notable development includes a 2026 investment wave of over 60 smart packaging facilities across the US and Canada focused on recyclable composite innovation and high-barrier material scaling. Strategic partnerships between packaging OEMs and logistics firms are strengthening operational integration and reducing transit damage rates across cross-border trade lanes.

United States Market Outlook: The United States dominates North America with strong industrial automation and packaging innovation ecosystems. Over 64% of composite packaging production capacity is concentrated in the US, particularly in states like Illinois and Ohio. In 2025, more than 35 new automated packaging lines were deployed across FMCG and pharma sectors, improving production efficiency by approximately 18% and reinforcing supply chain resilience.

Europe accounts for a 24% global share, led by strict regulatory frameworks and circular economy mandates. Countries such as Germany, France, and the Netherlands are driving adoption of recyclable and mono-material composites, with compliance-driven packaging redesign increasing by 33%. EU Packaging and Packaging Waste Regulation (PPWR) enforcement is accelerating industrial restructuring, pushing manufacturers to invest in sustainable material innovation and recycling integration. A 2025 cross-border initiative involving Germany and Italy expanded closed-loop recycling systems across industrial packaging corridors, improving material recovery efficiency by 19%.

Germany Market Outlook: Germany leads Europe with over 32% of regional composite packaging production and strong R&D capabilities in sustainable materials. In 2025, more than 40% of industrial packaging firms adopted advanced recyclable composite systems, supported by national recycling infrastructure upgrades and automation investments across Bavaria and North Rhine-Westphalia.

Asia-Pacific dominates with a 38% global share, driven by large-scale manufacturing ecosystems in China, India, Japan, and South Korea. China leads production concentration, contributing nearly 45% of regional output, supported by high-volume FMCG and electronics packaging demand. India is the fastest-expanding manufacturing base, with packaging automation adoption rising by 29% in 2025. The region benefits from cost-efficient labor, strong export infrastructure, and rapid industrialization of packaging hubs. A major 2026 development includes expansion of over 70 smart packaging plants across China and Southeast Asia, improving production scalability and reducing per-unit packaging costs by 17%.

China Market Outlook: China remains the dominant hub in Asia-Pacific, accounting for nearly 45% of regional production capacity. In 2025, more than 50 new automated composite packaging facilities were added across Guangdong and Jiangsu provinces, strengthening export-driven supply chains and improving production efficiency by approximately 20%.

South America holds a 7% global share, with demand primarily driven by Brazil and Argentina’s FMCG, food processing, and agricultural export sectors. Packaging modernization is increasing in urban industrial corridors, where recyclable composite adoption has grown by 18% due to retail expansion and export quality requirements. Infrastructure limitations still constrain large-scale deployment, but logistics improvements across Brazil’s port network are enhancing supply chain efficiency. A 2025 regional investment initiative added over 25 upgraded packaging facilities, improving production throughput by nearly 14% across key industrial zones.

Brazil Market Outlook: Brazil leads South America with approximately 52% of regional demand, supported by strong agro-export packaging requirements. In 2025, industrial packaging upgrades across São Paulo and Paraná improved operational efficiency by around 16%, strengthening Brazil’s position as the primary manufacturing and export hub in the region.

Middle East & Africa accounts for a 9% global share, driven by infrastructure expansion in UAE, Saudi Arabia, and South Africa. Demand is rising from food processing, construction materials, and pharmaceutical distribution sectors. Saudi Arabia’s industrial diversification under Vision 2030 is accelerating packaging localization, with over 20 new manufacturing and logistics facilities supporting composite packaging deployment. The UAE serves as a regional re-export hub, improving cross-border supply chain efficiency by nearly 18%. However, uneven recycling infrastructure across Africa limits full-scale circular adoption.

Saudi Arabia Market Outlook: Saudi Arabia leads the region with approximately 41% share of MEA demand. In 2025, over 15 new packaging and industrial material plants were commissioned in NEOM and Riyadh industrial zones, enhancing localized production capacity and reducing import dependency by nearly 20%.

Global leaders including Amcor, Berry Global, Mondi, Huhtamaki, and Smurfit Westrock compete directly with regional converters like Uflex and ProAmpac, while Sealed Air and Constantia Flexibles focus on high-performance barrier and specialty composites. The top five players collectively control nearly 52% share, creating a moderately consolidated structure. Competition is driven by technology efficiency (18–25% cost advantage), material innovation (22% performance gain in barrier films), and supply-chain integration speed (up to 20% faster delivery cycles). Firms are expanding through cross-border acquisitions, India–Vietnam capacity builds, and EU recycling partnerships, while also investing in vertical integration of resin-to-packaging value chains. A clear shift is emerging toward sustainable composite dominance, with consolidation pressure intensifying on mid-tier converters. Entry barriers remain high due to capital-intensive automation systems, regulatory compliance complexity, and patented multi-layer material technologies. Winning requires control over sustainable material innovation, global production footprint, and digitally optimized supply chains.

Berry Global

Mondi Group

Sealed Air Corporation

Huhtamaki

Smurfit Westrock

Sonoco Products Company

Coveris

ProAmpac

Constantia Flexibles

Uflex Limited

Winpak Ltd.

Graphic Packaging Holding Company

Current composite packaging systems are increasingly built on AI-assisted material design platforms and nano-laminated barrier coatings. AI-driven optimization improves material utilization efficiency by nearly 21%, while advanced nano-barrier layers reduce permeability losses by 18%, enhancing shelf-life stability in FMCG and pharmaceutical applications. Adoption levels for digital design tools have crossed 35% among large-scale packaging manufacturers, particularly in the US and Germany, enabling faster prototyping cycles and reduced waste generation.

Emerging smart packaging technologies such as sensor-embedded composites and recyclable mono-layer substitutes are reshaping legacy multilayer systems. Compared to traditional extrusion-based methods, modern AI-integrated production lines deliver nearly 24% higher throughput efficiency and 19% lower material waste, creating strong cost and sustainability advantages. Leading adopters include high-volume FMCG suppliers and pharma exporters in Europe and East Asia.

Between 2026 and 2028, the most disruptive shift will come from fully recyclable high-barrier composites integrated with digital traceability systems. These systems improve supply-chain visibility by 27%, enabling predictive logistics optimization. Early adopters gain competitive advantage through reduced compliance risk, faster certification cycles, and stronger export readiness across regulated markets.

October 2025 | Amcor announced FY25 sustainability and innovation progress, confirming expansion of recycle-ready composite packaging across 96% of flexible formats and achieving major circular material integration across global operations, strengthening low-waste packaging adoption by ~18% efficiency gain in material use. This reinforces Amcor’s leadership in high-barrier sustainable composites for food and healthcare packaging. Source: www.amcor.com

March 2025 | Berry Global released its sustainability progress update highlighting increased post-consumer resin usage from 3.6% to 5.1% (+43% YoY) and rollout of mono-material recyclable composite packaging designs, improving FMCG recyclability coverage to 93%. This strengthens circular packaging supply chain integration across North America and Europe.

May 2025 | Amcor partnered with Fedrigoni to launch a fully recycle-ready wet wipe composite packaging system, enabling polyethylene stream recyclability across Europe and improving packaging recovery efficiency by ~20%, supporting compliance with EU PPWR circular packaging mandates.

March 2024 | Berry Global & Mitsubishi Gas Chemical introduced an advanced recyclable MXD6 barrier composite solution improving recyclability compatibility by up to 12% material loading efficiency, enhancing food packaging shelf-life protection without compromising recyclability performance.

The Composite Packaging Market report covers a comprehensive assessment across material types, applications, and end-user industries including consumer electronics, healthcare, industrial goods, and FMCG sectors. It analyzes performance variations across key segments such as lithium-ion protective packaging, recyclable composites, and advanced barrier structures, representing over 100% consolidated segmentation coverage across global demand distribution patterns.

The study spans major regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing industrial adoption trends, regulatory frameworks, and manufacturing concentration shifts. It evaluates emerging technologies such as AI-driven packaging design, nano-coatings, and automated production systems, supporting strategic insights for investment planning, capacity expansion, and competitive positioning from 2026 to 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 5,459.0 Million |

| Market Revenue (2033) | USD 8,980.5 Million |

| CAGR (2026–2033) | 6.42% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Amcor; Berry Global; Mondi Group; Sealed Air Corporation; Huhtamaki; Smurfit Westrock; Sonoco Products Company; Coveris; ProAmpac; Constantia Flexibles; Uflex Limited; Winpak Ltd.; Graphic Packaging Holding Company |

| Customization & Pricing | Available on Request (10% Customization Free) |