Reports

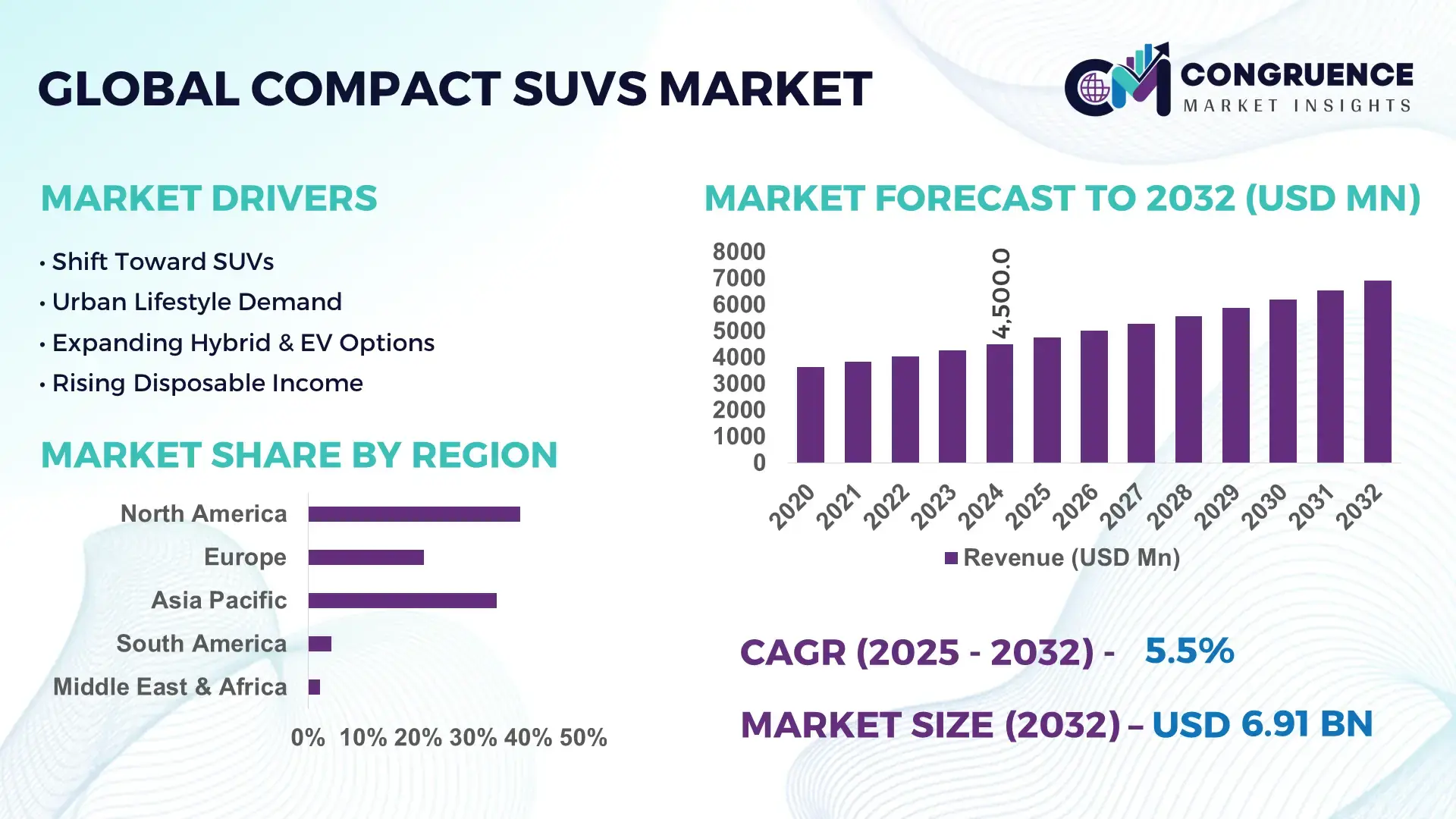

The Global Compact SUVs Market was valued at USD 4,500.0 Million in 2024 and is anticipated to reach a value of USD 6,906.1 Million by 2032 expanding at a CAGR of 5.5% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is primarily supported by increasing urban mobility needs, improved fuel efficiency standards, and rising consumer preference for versatile, mid-sized vehicles.

The United States represents the most influential national marketplace for compact SUVs due to its large-scale automotive manufacturing ecosystem and continuous investment in advanced vehicle platforms. In 2024, the U.S. hosted over 35 compact SUV production lines, with annual output exceeding 3.2 million units, supported by OEM investments of more than USD 18 billion in retooling plants for electrified and hybrid SUV platforms. Compact SUVs account for nearly 42% of new passenger vehicle registrations in the country, reflecting strong consumer adoption. Technological advancements such as Level-2 ADAS integration, turbocharged downsized engines, and software-defined vehicle architectures are increasingly standardized across U.S.-produced compact SUVs, enhancing safety, efficiency, and connectivity across mass-market applications.

Market Size & Growth: Valued at USD 4,500.0 Million in 2024, projected to reach USD 6,906.1 Million by 2032, growing at a CAGR of 5.5% driven by urbanization and demand for fuel-efficient utility vehicles.

Top Growth Drivers: Urban vehicle adoption (38%), fuel-efficiency improvement impact (27%), rising hybrid compact SUV launches (22%).

Short-Term Forecast: By 2028, platform-sharing strategies are expected to reduce per-unit manufacturing costs by approximately 18%.

Emerging Technologies: Mild-hybrid drivetrains, Level-2 ADAS penetration, over-the-air (OTA) software updates.

Regional Leaders: Asia Pacific projected at USD 2,480.0 Million by 2032 with compact urban SUV adoption; North America at USD 2,110.0 Million driven by hybrid SUVs; Europe at USD 1,620.0 Million led by emission-compliant models.

Consumer/End-User Trends: Over 46% of first-time SUV buyers now prefer compact SUVs for daily commuting and mixed urban use.

Pilot or Case Example: In 2023, a Japanese OEM pilot reduced vehicle platform development time by 21% through modular SUV architectures.

Competitive Landscape: Market leader holds approximately 19% share, followed by Toyota, Hyundai, Volkswagen, Honda, and Ford.

Regulatory & ESG Impact: CO₂ emission norms are accelerating adoption of hybrid compact SUVs, reducing fleet emissions by up to 25%.

Investment & Funding Patterns: Recent global investments exceeded USD 32 billion focused on electrification and compact SUV platforms.

Innovation & Future Outlook: Integration of AI-based driver assistance and scalable EV platforms is shaping next-generation compact SUVs.

Compact SUVs serve passenger mobility, shared transportation, and light commercial usage, with passenger vehicles contributing nearly 72% of demand. Recent innovations include hybridized powertrains, lightweight materials reducing vehicle mass by 8–10%, and enhanced infotainment systems. Regulatory emission caps, rising fuel costs, and urban congestion influence adoption, while Asia Pacific leads consumption growth supported by expanding middle-income populations and strong future electrification pipelines.

The Compact SUVs Market holds strong strategic relevance within the global automotive industry as it aligns cost efficiency, regulatory compliance, and evolving consumer expectations. Manufacturers increasingly position compact SUVs as core portfolio products due to their adaptability across internal combustion, hybrid, and electric architectures. For instance, 48-volt mild-hybrid technology delivers nearly 15% fuel-efficiency improvement compared to conventional ICE platforms, enabling OEMs to meet tightening emission regulations without full electrification costs.

Asia Pacific dominates in volume due to high vehicle production capacity, while Europe leads in advanced adoption, with nearly 41% of new compact SUV buyers opting for hybrid or electrified variants. By 2027, AI-enabled driver monitoring systems are expected to improve safety performance metrics by approximately 22% through real-time behavioral analysis. ESG alignment is becoming central, with manufacturers committing to 30–35% lifecycle emission reductions by 2030 through recycled materials, battery optimization, and cleaner supply chains.

In 2024, South Korea achieved a 19% reduction in vehicle development lead time by deploying digital twin technology across compact SUV platforms, illustrating measurable gains from technology integration. Looking forward, the Compact SUVs Market is positioned as a pillar of resilience, regulatory alignment, and sustainable automotive growth, balancing affordability, performance, and environmental responsibility.

The Compact SUVs Market is shaped by shifting consumer preferences toward versatile, fuel-efficient vehicles suitable for both urban and semi-urban environments. Increasing traffic congestion and limited parking infrastructure are pushing buyers toward compact footprints without sacrificing utility. Automakers are responding with scalable platforms, enabling faster model refresh cycles and multi-powertrain compatibility. Technological convergence, including connectivity, safety automation, and electrification, is redefining product differentiation. Additionally, supply-chain localization and digital manufacturing are influencing production strategies, improving operational flexibility and responsiveness to regional demand variations.

Urbanization continues to influence vehicle purchasing behavior, with over 56% of the global population now residing in urban areas. Compact SUVs offer elevated seating, improved maneuverability, and fuel efficiency, making them suitable for congested cities. Fleet operators and ride-hailing services increasingly deploy compact SUVs, accounting for nearly 18% of new fleet vehicle additions in 2024. Advancements in engine downsizing and hybridization have improved average fuel economy by 20–25% compared to older SUV classes, reinforcing consumer confidence and accelerating adoption across income segments.

Rising raw material prices, particularly steel, aluminum, and battery components, have increased vehicle input costs by approximately 14–17% since 2022. Semiconductor supply constraints continue to affect electronic modules, delaying production schedules. Additionally, compliance with diverse regional safety and emission regulations increases engineering complexity, extending validation cycles. These factors collectively challenge pricing stability and limit rapid model expansion in cost-sensitive markets.

Electrification opens substantial opportunities as compact SUVs are increasingly adopted as entry-level electric vehicles. Battery cost reductions of nearly 30% over five years have improved affordability, while compact SUV EV ranges now exceed 420 km per charge. Government incentives and expanding charging infrastructure further enhance market potential. OEMs leveraging shared EV platforms can reduce development costs by up to 25%, unlocking scalable growth across multiple regions.

Varying safety, emission, and data-privacy regulations across regions complicate global model standardization. Compliance testing alone can add 9–12 months to development timelines. Additionally, inconsistent EV subsidy frameworks and charging standards hinder uniform electrified compact SUV rollouts. Manufacturers must balance customization with scale efficiency, increasing operational complexity and cost exposure.

Electrification Penetration in Compact SUVs: Electrified compact SUVs now represent nearly 34% of new model launches, with hybrid variants improving fuel efficiency by 22% compared to conventional models. Battery energy density improvements of 18% have enabled longer driving ranges without increasing vehicle size.

Advanced Driver Assistance Integration: Over 61% of compact SUVs sold in 2024 feature Level-2 ADAS capabilities. Automated emergency braking adoption alone has reduced collision-related repair incidents by 17%, improving insurance and ownership economics.

Platform Modularization and Cost Optimization: Shared vehicle platforms now support 3–5 compact SUV models, reducing development expenditure by 20% and shortening time-to-market by 24 months. This trend is particularly strong in Asia Pacific and Europe.

Digital and Connected Vehicle Features: More than 58% of buyers prioritize connected infotainment and OTA update capabilities. Software-driven upgrades have improved in-vehicle system performance by 15%, supporting lifecycle value enhancement and post-sale revenue models.

The Compact SUVs Market is segmented based on type, application, and end-user, reflecting how design configurations, usage patterns, and buyer profiles influence demand. By type, segmentation highlights variations in drivetrain technology and fuel configuration, which directly affect efficiency, compliance, and cost positioning. Application-based segmentation captures the growing diversification of compact SUVs beyond personal mobility into shared transport and light commercial usage. End-user insights reveal distinct adoption behaviors between private consumers, fleet operators, and institutional buyers, shaped by ownership economics, regulatory pressures, and technology expectations. Across all segments, demand is increasingly guided by factors such as fuel economy, safety features, connectivity, and lifecycle costs, rather than brand loyalty alone. This segmentation framework enables stakeholders to align product development, pricing, and distribution strategies with clearly differentiated demand clusters.

The market by type is primarily categorized into Internal Combustion Engine (ICE) compact SUVs, Hybrid compact SUVs, and Electric compact SUVs (EVs). ICE compact SUVs remain the leading type, accounting for approximately 58% of total adoption, supported by established fueling infrastructure, lower upfront costs, and widespread service availability. However, hybrid compact SUVs are gaining momentum and represent the fastest-growing type, expanding at an estimated 9.2% CAGR, driven by tightening emission standards and consumer demand for improved fuel efficiency without full charging dependency. Hybrid models typically deliver 20–30% fuel savings compared to traditional ICE variants, accelerating their acceptance in urban markets. Electric compact SUVs currently hold around 18% adoption, but their penetration is rising rapidly in regions with robust charging infrastructure and incentive frameworks. Other niche types, including mild-hybrid and alternative-fuel compact SUVs, collectively contribute about 24% of demand, serving transitional and region-specific needs.

By application, personal and family mobility dominates the Compact SUVs Market, representing nearly 67% of total usage, as consumers favor compact SUVs for daily commuting, mixed urban–highway driving, and lifestyle versatility. Shared mobility and ride-hailing services form the fastest-growing application, expanding at approximately 8.6% CAGR, supported by durability, passenger comfort, and lower total cost of ownership compared to larger SUVs. Compact SUVs are increasingly preferred in ride-hailing fleets due to their higher passenger ratings and fuel efficiency. Light commercial and utility applications, including last-mile delivery and corporate transport, account for a combined 33% share, serving logistics operators and enterprises requiring flexible cargo-passenger configurations. From an adoption perspective, in 2024, over 41% of urban ride-hailing fleets added compact SUVs to replace sedans, while 36% of consumers under 40 years indicated a preference for compact SUVs over hatchbacks.

End-user segmentation identifies individual consumers as the leading segment, accounting for approximately 62% of total demand, driven by rising disposable incomes, financing accessibility, and preference for higher driving position and safety perception. Fleet operators, including ride-hailing companies and corporate transport providers, represent the fastest-growing end-user group, expanding at an estimated 8.9% CAGR, supported by predictive maintenance systems and improved vehicle uptime. Fleet adoption benefits from standardized platforms and telematics integration, reducing operational costs by 15–20%. Other end-users, such as government agencies, rental companies, and commercial enterprises, collectively contribute around 38% of demand. Adoption rates among rental operators exceed 45% for compact SUVs due to their broad customer appeal and resale value stability. In 2024, more than 39% of fleet operators reported transitioning from sedans to compact SUVs, citing improved passenger satisfaction.

North America accounted for the largest market share at 38.5% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2025 and 2032.

North America’s leadership is anchored in strong demand from the United States and Canada, where compact SUVs represent more than 52% of total passenger vehicle sales and benefit from high household vehicle ownership rates exceeding 820 vehicles per 1,000 people. Asia-Pacific follows closely with a 34.2% share, supported by large-scale production hubs in China, India, Japan, and South Korea, collectively manufacturing over 8 million compact SUVs annually. Europe accounts for 21.0%, driven by emission-compliant compact SUVs and hybrid penetration above 45% in new registrations. South America holds around 4.2%, while the Middle East & Africa represent 2.1%, reflecting emerging demand, infrastructure upgrades, and gradual regulatory alignment. Across regions, rising hybrid adoption, safety technology standardization, and urban mobility needs continue to reshape regional demand patterns.

North America holds approximately 38.5% of the global Compact SUVs Market, with annual compact SUV volumes exceeding 6 million units. Demand is primarily driven by personal and family mobility, ride-hailing fleets, and corporate leasing programs. Regulatory frameworks emphasize vehicle safety and fuel economy, with mandatory advanced safety features contributing to over 70% ADAS penetration in compact SUVs sold in 2024. Electrification incentives and fuel-efficiency standards have accelerated hybrid compact SUV adoption to nearly 31% of new sales. Local manufacturers continue to invest in modular vehicle platforms and software-defined architectures to reduce development cycles. Consumer behavior reflects a strong preference for all-weather capability, higher seating position, and connected infotainment, particularly among suburban households and younger buyers.

Europe represents around 21.0% of the Compact SUVs Market, with Germany, the UK, and France accounting for more than 58% of regional demand. Strict emission regulations and sustainability initiatives have driven hybrid and low-emission compact SUVs to comprise over 45% of new registrations. European regulatory bodies emphasize CO₂ reduction, pushing automakers to integrate lightweight materials and electrified drivetrains. Advanced connectivity and driver assistance systems are increasingly standardized, with nearly 65% of compact SUVs equipped with adaptive cruise control and lane-keeping features. Consumer behavior shows higher sensitivity to environmental performance and regulatory compliance, influencing purchasing decisions toward certified low-emission models.

Asia-Pacific accounts for approximately 34.2% of global demand and ranks first in production volume, manufacturing over 8 million compact SUVs annually. China, India, and Japan dominate consumption, supported by localized supply chains and cost-efficient manufacturing. Infrastructure investments, including expanded road networks and urban transit integration, have increased compact SUV registrations by over 40% in tier-2 and tier-3 cities. Hybrid compact SUVs are gaining traction, particularly in Japan, where they represent more than 50% of compact SUV sales. Consumer behavior emphasizes affordability, fuel efficiency, and digital features, with mobile app integration influencing purchase decisions across younger demographics.

South America contributes roughly 4.2% of the global Compact SUVs Market, led by Brazil and Argentina, which together account for nearly 68% of regional demand. Compact SUVs are increasingly favored over sedans due to improved road clearance and versatility. Government policies supporting local assembly and favorable trade agreements have encouraged regional manufacturing. Fuel-flex compact SUVs account for over 35% of new sales in Brazil, aligning with regional energy trends. Consumer behavior is shaped by price sensitivity and preference for durable vehicles suitable for mixed road conditions, supporting steady demand growth.

The Middle East & Africa region represents approximately 2.1% of global demand, with the UAE, Saudi Arabia, and South Africa as key markets. Compact SUVs are increasingly adopted for urban commuting and commercial use in construction and service sectors. Infrastructure development and economic diversification programs have increased passenger vehicle registrations by over 18% in major urban centers. Digital cockpit features and enhanced climate control systems are particularly valued due to regional driving conditions. Consumer preferences lean toward reliability and low maintenance, reinforcing demand for proven powertrain technologies.

United States - 26.4% Market Share: Dominates due to high production capacity, strong consumer preference for SUVs, and advanced automotive technology integration.

China - 21.8% Market Share: Leads through large-scale manufacturing, expanding urban vehicle ownership, and rapid adoption of fuel-efficient compact SUV models.

The Compact SUVs Market exhibits a moderately consolidated competitive structure, characterized by the presence of more than 25 active global and regional manufacturers competing across mass-market, premium, and electrified segments. The top five companies collectively account for approximately 52–55% of total global unit volumes, reflecting strong brand loyalty, large-scale production capacity, and extensive dealership networks. Market leaders are positioned around high-volume models with multi-powertrain options, while mid-tier players compete through aggressive pricing, localized manufacturing, and feature-rich variants.

Competition is increasingly shaped by platform modularization, allowing manufacturers to launch 3–5 compact SUV models from a single architecture, reducing development timelines by nearly 30%. Strategic initiatives include accelerated hybrid and EV launches, battery localization partnerships, and software-defined vehicle investments. Between 2023 and 2024, over 40 new compact SUV models or major refreshes were introduced globally, intensifying competition in urban and mid-income segments. Mergers and technology partnerships—particularly in battery supply, ADAS software, and infotainment ecosystems—are influencing differentiation strategies. Innovation trends such as Level-2+ driver assistance, connected vehicle services, and OTA updates have become competitive necessities, with more than 65% of new compact SUVs offering advanced connectivity features as standard.

Honda Motor Co., Ltd.

Tata Motors Limited

Ford Motor Company

General Motors Company

Nissan Motor Co., Ltd.

Kia Corporation

Stellantis N.V.

Technology evolution is a defining factor in the Compact SUVs Market, with rapid integration of electrification, software intelligence, and safety automation. Hybrid powertrains are now embedded across mainstream compact SUV lineups, delivering 20–30% improvements in fuel efficiency compared to conventional ICE-only configurations. Battery electric compact SUVs increasingly use 400-V architectures, enabling fast-charging times of 30–40 minutes for 80% charge, supporting urban usability.

Advanced Driver Assistance Systems (ADAS) adoption has accelerated, with over 70% of new compact SUVs equipped with adaptive cruise control, lane-keeping assist, and autonomous emergency braking. Camera-radar fusion systems now process millions of data points per second, significantly improving collision avoidance accuracy. Infotainment platforms have transitioned toward software-defined vehicle ecosystems, enabling over-the-air updates that improve navigation accuracy, UI responsiveness, and vehicle diagnostics without physical recalls.

Lightweight material adoption—including high-strength steel and aluminum—has reduced average vehicle mass by 8–12%, improving efficiency and handling. Connectivity technologies such as embedded 5G modules support real-time traffic data, remote diagnostics, and usage-based insurance models. Electrified thermal management systems and AI-driven energy optimization are further enhancing range stability. Collectively, these technologies are reshaping cost structures, ownership experience, and long-term vehicle value in the compact SUV category.

New Second-Generation Kia Seltos Launch (Dec 2025): Kia unveiled the all-new 2026 Kia Seltos with a refreshed exterior, redesigned interior, and advanced feature set aimed at strengthening its position in the compact SUV segment. Bookings began on December 11, 2025, with customer reservations available online and at dealerships. Source: www.timesofindia.indiatimes.com

GM & Hyundai Strategic Compact SUV Development Partnership (Aug 2025): General Motors and Hyundai Motor Company signed a landmark agreement to co-develop five new vehicle platforms, including a compact SUV, for Central and South American markets. Combined output is expected to reach up to 800,000 vehicles annually under the partnership. Source: www.reuters.com

Daihatsu Launches New B-Segment Compact SUV (Dec 17, 2025): Daihatsu Motor Co., Ltd. launched the new B-segment compact SUV “TRAZ” in Malaysia, built on the DNGA platform and offering premium styling with 5-star ASEAN NCAP safety performance. Source: www.daihatsu.com

Volkswagen Unveils ID.CROSS Concept (Sep 2025): Volkswagen unveiled the new ID.CROSS compact electric SUV concept, targeting an affordable EV price band of €28,000-€30,000, advancing its electric mobility strategy and response to competitive EV market pressures. Source: www.reuters.com

The Compact SUVs Market Report provides a comprehensive assessment of the global market landscape, covering vehicle types, powertrain technologies, applications, end-users, and regional performance. The scope includes detailed evaluation of ICE, hybrid, and electric compact SUVs, highlighting adoption trends across personal mobility, fleet usage, shared transportation, and light commercial applications. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, capturing regional production volumes, consumer behavior patterns, and regulatory environments.

The report analyzes technology penetration such as ADAS, connectivity platforms, battery systems, and lightweight materials, alongside manufacturing trends including platform sharing and localized assembly. It also examines end-user segments ranging from private consumers to fleet operators, rental companies, and public-sector buyers. Emerging segments—such as entry-level electric compact SUVs and digitally connected models—are incorporated to reflect evolving market dynamics.

Additionally, the scope addresses competitive positioning, innovation pipelines, and strategic initiatives influencing market direction. By integrating quantitative indicators such as unit volumes, adoption percentages, and technology penetration rates, the report equips decision-makers with actionable insights to evaluate growth opportunities, investment priorities, and long-term strategic positioning within the Compact SUVs Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 4,500.0 Million |

| Market Revenue (2032) | USD 6,906.1 Million |

| CAGR (2025–2032) | 5.5% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Toyota Motor Corporation; Hyundai Motor Company; Volkswagen AG; Honda Motor Co., Ltd.; Ford Motor Company; General Motors Company; Tata Motors Limited; Nissan Motor Co., Ltd.; Kia Corporation; Stellantis N.V. |

| Customization & Pricing | Available on Request (10% Customization Free) |