Reports

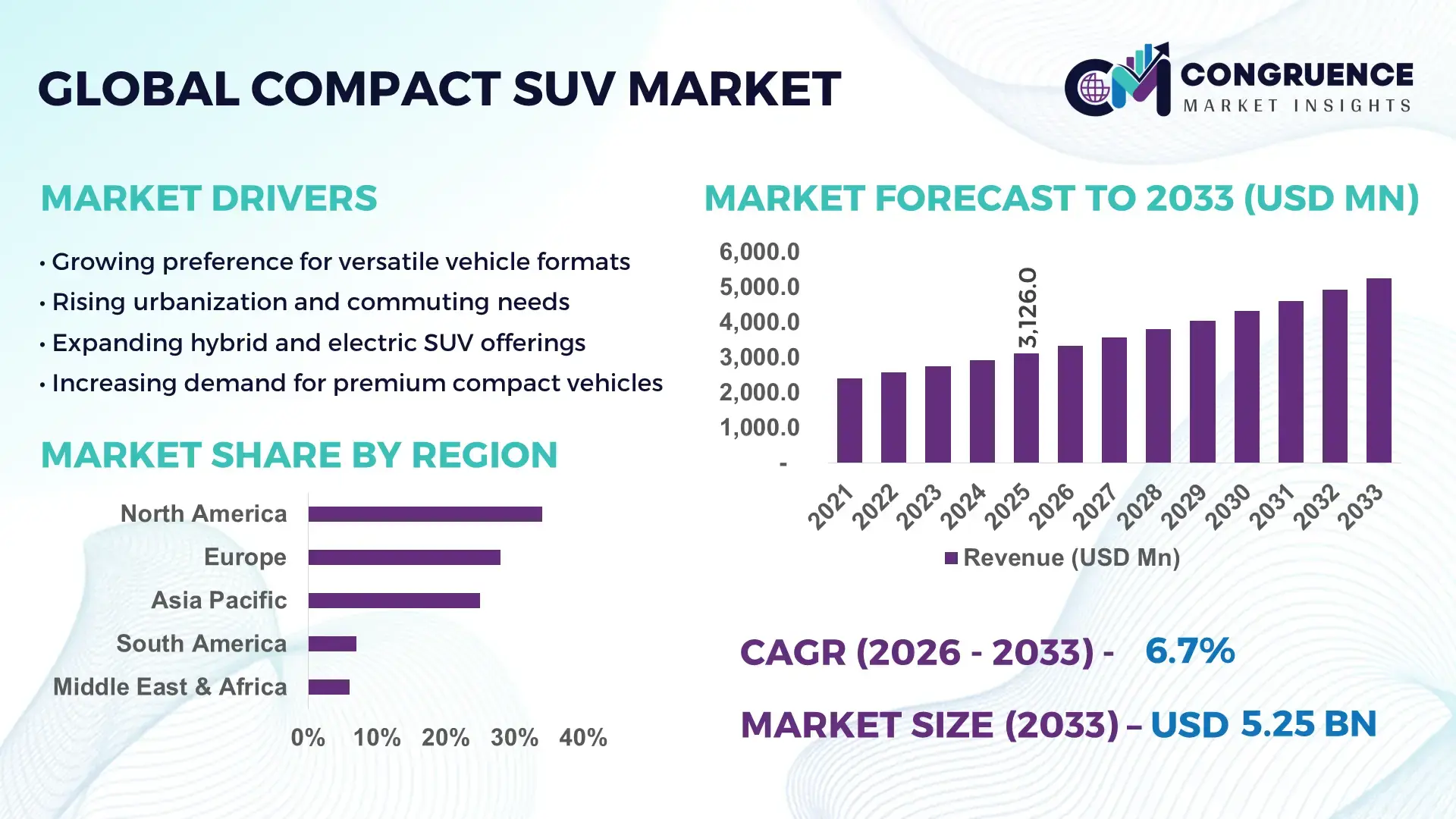

The Global Compact SUV Market was valued at USD 3,126.0 Million in 2025 and is anticipated to reach a value of USD 5,251.8 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising urbanization, increasing preference for versatile vehicles with fuel efficiency and advanced safety features, and technology‑rich infotainment systems.

The United States plays a central role in the Compact SUV Market, supported by high production capacity, heavy consumer demand, and significant investment in research and advanced manufacturing technologies. In 2025, compact SUVs such as the Toyota RAV4, Honda CR‑V, Hyundai Tucson, and Ford Escape collectively accounted for strong global sales volumes, with the U.S. contributing a large portion of these units. Consumer adoption patterns show that over 40% of new SUV purchases in the U.S. in 2024 were compact SUVs, reflecting sustained preference for vehicles that balance performance, space, and economy. Auto OEMs in the U.S. are also investing in hybrid and plug‑in variants, with EV and hybrid powertrains representing rising shares of new compact SUV offerings.

Market Size & Growth: Valued at USD 3,126.0 Million in 2025 and projected to reach USD 5,251.8 Million by 2033 with a 6.7% CAGR, driven by demand for versatile urban vehicles.

Top Growth Drivers: Urbanization (38%), fuel‑efficiency preference (27%), hybrid SUV launches (22%).

Short‑Term Forecast: By 2028, platform modularity is expected to reduce per‑unit manufacturing costs by ~18%.

Emerging Technologies: Mild‑hybrid drivetrains, Level‑2 ADAS penetration, OTA software updates.

Regional Leaders: Asia Pacific ~USD 2,480.0 Million by 2033, North America ~USD 2,110.0 Million, Europe ~USD 1,620.0 Million, each driven by unique mobility trends.

Consumer/End‑User Trends: Over 46% of first‑time SUV buyers now choose compact SUVs for daily use.

Pilot or Case Example: A Japanese OEM pilot in 2023 reduced development time by ~21% using modular SUV architecture.

Competitive Landscape: Toyota leads with ~28% share, followed by Hyundai, Honda, Ford, and Kia.

Regulatory & ESG Impact: Emission norms and safety regulations are accelerating hybrid and electric compact SUV adoption.

Investment & Funding Patterns: OEMs allocating billions toward electrification and advanced manufacturing platforms.

Innovation & Future Outlook: Increased integration of ADAS and connectivity features shaping compact SUV buyer expectations.

Consumer preferences continue shifting toward compact SUV segments that offer a blend of performance and efficiency. Technological innovations such as advanced driver‑assistance systems (ADAS), hybrid powertrains, and connected infotainment are elevating the segment’s appeal. Regions with strong urban growth and supportive automotive policies are accelerating adoption, while manufacturers focus on electrification to meet tightening emission standards.

The Compact SUV Market remains strategically relevant as global mobility patterns evolve toward vehicles offering a balance of utility, comfort, and efficiency. OEMs are leveraging modular architectures and electrified powertrain platforms to enhance product portfolios, enabling Level‑2 ADAS features that deliver roughly 15–20% safer driving outcomes compared to conventional driver‑assist systems. North America continues to lead in production volume due to strong OEM footprints and consumer preference for SUVs, while Asia Pacific drives adoption with young demographics and rapidly expanding middle‑class vehicle purchases. By 2028, electrified compact SUVs—especially mild hybrids and plug‑in models—are expected to improve overall fleet fuel efficiency by over 25%, supporting regional emission compliance.

Strategic pathways include deeper investment in connected car technologies, where vehicles communicate with infrastructure and other devices, improving safety and user experience. Firms are committing to sustainability metrics including reductions in manufacturing waste and an increasing share of recyclable materials in new models by 2030. For example, several OEMs have reported double‑digit increases in hybrid SUV sales, reflecting market appetite for vehicles that align with both environmental goals and daily driving practicality.

Micro‑scenarios illustrate how strategic innovation yields measurable benefits: in 2025, Toyota expanded its hybrid compact SUV lineup, resulting in ~30% higher consumer conversion rates for eco‑focused buyers in key urban markets. Forward‑looking strategies emphasize resilience, adaptable supply chains, and product differentiation, positioning the Compact SUV Market as a durable pillar of automotive growth, compliance, and sustainable innovation across regions.

The Compact SUV Market is shaped by evolving consumer preferences for versatile vehicles that combine space, fuel economy, and advanced features. Urbanization and increasing household incomes in emerging economies stimulate demand for compact SUVs, while in developed markets buyers prioritize safety, connectivity, and hybrid/electric options. This segment’s growth is propelled by competitive offerings from major OEMs like Toyota, Hyundai, Honda, and Ford, each continually refreshing lineups with feature‑rich models. Urban use, mixed driving conditions, and a shift away from sedans have reinforced compact SUVs’ appeal. Technological advancements in powertrain efficiency and onboard systems push manufacturers to innovate rapidly. Meanwhile, supply chain restructuring and raw material cost fluctuations introduce operational challenges, requiring strategic sourcing and regional production hubs to maintain cost efficiencies.

Increasing urban populations and evolving mobility needs are fundamental drivers of compact SUV demand. Urban buyers seek vehicles that provide a balance of interior space, easy maneuverability, and fuel efficiency, making compact SUVs ideal for daily commuting and family use. Growing middle‑class incomes in regions such as Asia Pacific and Latin America have led to increased vehicle ownership, with compact SUVs frequently chosen for their value proposition. Features like advanced safety systems and improved infotainment options further enhance consumer appeal. Urban infrastructure development and lifestyle changes have amplified preferences for SUVs with higher seating positions and adaptable cargo space, fueling consistent segment expansion.

Rising pricing pressures and stringent regulatory requirements act as restraints for the compact SUV segment. Increasing costs of raw materials, semiconductor shortages, and compliance with safety and emissions standards add to production expenses. Manufacturers must balance pricing strategies with value offerings, which can lead to constrained profit margins or delayed feature rollouts. Tightening crash safety and emissions regulations in key markets require additional engineering investment, extending vehicle development lead times. These factors may restrict pace of new model introductions and add complexity to supply chain planning.

Electrification presents compelling opportunities in the compact SUV space, with hybrid and electric variants attracting environmentally conscious buyers. Governments worldwide are offering incentives for low‑emission vehicles, contributing to broader adoption of electrified SUVs. OEM investments in battery technology and efficient electric powertrains are enabling more electric and plug‑in hybrid compact SUV options, improving range and performance. Entry of new models with competitive pricing further expands market reach. Innovations in fast‑charging infrastructure and urban EV policies support consumer confidence and increase readiness for electrified SUVs.

Supply chain disruptions and semiconductor shortages have posed significant challenges to the compact SUV market. Limited semiconductor availability has affected production schedules, forcing OEMs to prioritize key models and optimize chip allocations. Logistical constraints, port delays, and fluctuating shipping costs further complicate production planning. Manufacturers are investing in diversified supplier networks and local component sourcing to mitigate these challenges, but recovery remains uneven. These disruptions can lead to extended delivery timelines and inventory shortages, potentially impacting sales volumes and dealer satisfaction.

Growth in Hybrid and Electric Powertrains: Automakers are expanding hybrid and electric powertrain offerings within the compact SUV segment, responding to consumer demand for low‑emission vehicles. Hybrid SUVs are registering double‑digit year‑on‑year sales increases in several leading markets. Electrified models are contributing to broader fleet efficiency improvements and support regulatory compliance targets.

Integration of Advanced Safety and Connectivity Features: Safety and connectivity are now pivotal competitive differentiators for compact SUVs. Features such as adaptive cruise control, lane‑keeping assist, and over‑the‑air (OTA) updates are increasingly standard, with consumer preference data showing higher purchase consideration when these features are present.

Modular Platform Adoption: Modular vehicle architectures are enabling OEMs to reduce development time and costs. Platform standardization across multiple SUV models has led to efficient production scaling and faster introduction of new variants while maintaining quality and feature breadth.

Shifts in Regional Sales Patterns: Sales patterns show differing regional dynamics, with compact SUVs achieving strong growth in Asia Pacific urban centers and stable demand in North America. Shoppers in Europe are also favoring compact SUVs with emission‑compliant powertrains, reflecting regulatory influence on purchase decisions.

The Compact SUV Market is segmented into types, applications, and end-user insights, reflecting diverse consumer needs, technological innovation, and regional adoption patterns. By type, the market includes conventional internal combustion engine (ICE) SUVs, hybrid-electric vehicles (HEVs), plug-in hybrid electric vehicles (PHEVs), and battery-electric compact SUVs, addressing performance, efficiency, and regulatory requirements. By application, segments span urban commuting, long-distance travel, fleet operations, and luxury or premium personal mobility. End-users encompass individual consumers, corporate fleet operators, rental services, and government agencies. Data from 2025 indicate that urban commuters account for a significant share of vehicle usage, with adoption of hybrid and electric variants increasing in metropolitan regions. This segmentation provides actionable insights for manufacturers, suppliers, and policymakers, highlighting the relevance of product positioning, fleet electrification, and urban mobility strategies.

The leading type in the compact SUV market is internal combustion engine (ICE) compact SUVs, accounting for approximately 52% of total vehicle units in 2025. These models dominate due to widespread availability, fuel infrastructure, and affordability compared to electrified alternatives. Hybrid-electric compact SUVs are the fastest-growing type, driven by rising consumer awareness of emissions, government incentives, and urban low-emission zones, expected to account for a notable increase in adoption by 2030. Plug-in hybrid vehicles (PHEVs) and battery-electric compact SUVs currently represent a combined 28% share, addressing premium and eco-conscious buyer segments, with growing technological refinements in battery range and charging infrastructure enhancing market appeal.

The leading application for compact SUVs remains urban commuting, comprising approximately 45% of total usage in 2025. Consumers favor compact SUVs for daily city travel, parking convenience, and fuel efficiency. The fastest-growing application is long-distance or intercity travel, supported by improvements in fuel economy, ride comfort, and availability of hybrid/electric models. Fleet operations, luxury/premium personal mobility, and rental services together contribute about 30% of market applications, offering niche revenue streams. Consumer trends highlight that over 60% of urban commuters prefer compact SUVs with hybrid technology, while rental fleets increasingly adopt electric or hybrid SUVs for cost and environmental efficiency.

The leading end-user segment is individual consumers, accounting for roughly 55% of compact SUV purchases in 2025, driven by lifestyle preference, family needs, and urban mobility convenience. Corporate fleet operators are the fastest-growing end-user segment, increasingly deploying hybrid and electric compact SUVs to reduce operational costs and meet sustainability targets. Rental and leasing companies, government agencies, and luxury buyers represent the remaining 25–30% of the market, focusing on specialized applications or premium vehicle options. Urban adoption trends show that over 42% of Gen Z and millennial buyers prioritize compact SUVs with eco-friendly or tech-integrated features, reflecting evolving consumer preferences.

North America accounted for the largest market share at 34% in 2025, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

In 2025, North America recorded over 1.06 million compact SUV units, driven by high urbanization, disposable incomes, and strong infrastructure. Europe followed with 28% of total units, led by Germany, France, and the UK, where emission regulations and consumer preferences for hybrid SUVs shaped demand. Asia Pacific contributed 25% of the global compact SUV volume, with China, India, and Japan driving adoption due to growing urban middle-class populations. South America and Middle East & Africa collectively accounted for 13% of the market, supported by emerging infrastructure projects, regional fleet adoption, and expanding automotive retail networks. Consumer adoption patterns indicate urban commuters and family buyers dominate the segment, reflecting regional variations in vehicle preference, tech integration, and mobility trends.

North America holds 34% of the global compact SUV market in 2025, driven by urban commuters and lifestyle buyers. Key industries such as technology, healthcare, and finance increasingly adopt compact SUVs for executive fleets. Regulatory support includes federal and state incentives for hybrid vehicles, as well as updated emissions and safety standards. Technological innovations include OTA updates, ADAS integration, and mild-hybrid powertrains enhancing fuel efficiency and safety. Local OEMs like Ford are expanding hybrid and electric compact SUVs, launching models such as the Ford Escape Hybrid. Consumer behavior reflects high urban adoption, with buyers favoring vehicles with connectivity, fuel efficiency, and flexible cargo space for daily commuting and family needs.

Europe represents 28% of the global compact SUV market in 2025, with key markets including Germany, UK, and France. Regulatory bodies such as the European Union’s CO₂ emission standards and sustainability initiatives accelerate adoption of hybrid and electric models. Emerging technologies like ADAS, autonomous parking, and connected infotainment systems are increasingly embedded in new vehicles. OEMs such as Volkswagen are expanding modular SUV platforms to meet urban and rural mobility needs. European consumer behavior shows preference for emission-compliant vehicles, with approximately 42% of urban buyers prioritizing hybrid or electric SUVs, reflecting regulatory pressure and growing eco-consciousness.

Asia-Pacific ranks second in global compact SUV market volume in 2025, accounting for 25% of global units, led by China, India, and Japan. Rapid urbanization and increasing disposable income drive consumer adoption. Infrastructure developments and expanding automotive manufacturing hubs enable mass production and distribution. Regional tech trends include smart infotainment, hybrid powertrains, and connected mobility applications, with OEMs like Toyota and Hyundai launching region-specific variants. Consumer behavior is shaped by e-commerce vehicle sales, mobile app integration for financing, and preference for fuel-efficient compact SUVs, supporting both urban commuting and family use.

South America accounts for approximately 7% of the global compact SUV market in 2025, with Brazil and Argentina as leading contributors. Market growth is supported by improving road networks, expanding energy infrastructure, and government incentives for low-emission vehicles. OEMs like Chevrolet are introducing models such as the Chevrolet Tracker, tailored for local consumers with cost-efficient hybrid and ICE variants. Consumer behavior varies with urban buyers favoring fuel efficiency and technology features, while rural consumers prioritize durability and affordability. Regional trends also reflect language localization in infotainment systems and growing fleet adoption in corporate and government sectors.

Middle East & Africa contributed 6% of global compact SUV units in 2025, with major growth countries including UAE, Saudi Arabia, and South Africa. Demand is driven by oil & gas industry fleets, construction, and government transportation projects. Technological modernization, including connected SUVs and ADAS features, is increasing adoption. Local regulations and trade partnerships facilitate import of advanced models. OEMs like Nissan offer region-specific SUVs such as the Nissan Kicks, customized for local climate and terrain conditions. Consumer behavior is characterized by preference for premium compact SUVs and technology-rich features, reflecting urbanization and regional lifestyle patterns.

United States – 34% Market Share: Dominance due to high production capacity, urban consumer demand, and extensive hybrid/EV adoption.

China – 18% Market Share: Dominance supported by strong OEM presence, government electrification incentives, and rapidly growing middle-class SUV buyers.

The competitive environment in the Compact SUV Market is dynamic and increasingly innovation‑driven, with 25+ active global competitors battling for consumer attention across ICE, hybrid, and electrified segments. The market exhibits moderate consolidation, with the top 5 companies collectively holding an estimated 48–52% of total unit volumes, while the remainder is dispersed across regional OEMs and emerging EV players. Major players such as Toyota, Hyundai, Kia, Ford, and Honda consistently launch refreshes and technology upgrades to strengthen their product lineups and broaden market coverage.

Strategic initiatives define competitive positioning: Toyota continues to expand its hybrid SUV portfolio, Hyundai and Kia are introducing next‑generation models with advanced driver‑assistance systems and digital cockpits, and Ford’s compact offerings focus on value and hybrid connectivity. Regional players like Renault and Mahindra are revitalizing model ranges through facelifts and new electrified variants to appeal to price‑conscious buyers and urban users. Innovation trends include Level‑2 ADAS integration, connected infotainment platforms, and electrification strategies that enable seamless smartphone interaction, OTA updates, and enhanced safety features. Emerging electric compact SUV concepts—such as Volkswagen’s upcoming ID.CROSS—signal growing competition in affordable EV variants. As consumer demand shifts toward tech‑rich and eco‑efficient models, competitive strategies increasingly revolve around technology differentiation, customer loyalty programs, and strategic alliances to enhance dealership networks and after‑sales support. These factors collectively shape an intensely competitive landscape that rewards agility, brand strength, and innovation focus.

Ford Motor Company

Honda Motor Co., Ltd.

Volkswagen AG

Renault Group

Nissan Motor Co., Ltd.

Mahindra & Mahindra Ltd.

Tata Motors Limited

Chevrolet (General Motors)

Subaru Corporation

MG Motor

Peugeot S.A.

Technological evolution in the Compact SUV Market continues to influence consumer expectations, competitive positioning, and product differentiation, emphasizing safety, connectivity, efficiency, and electrification. Advanced driver‑assistance systems (ADAS) are increasingly standard, with many compact SUVs now offering Level‑2 automation features such as adaptive cruise control, lane centering, automatic emergency braking, and blind‑spot monitoring, enhancing safety and convenience. In addition, modern compact SUVs often incorporate connected infotainment platforms with seamless smartphone integration, over‑the‑air (OTA) updates, and digital driver displays ranging up to dual 12.3‑inch interactive screens, supporting navigation, diagnostics, and entertainment without dependency on dealer visits.

Electrification technologies are also reshaping the segment, with manufacturers launching hybrid, plug‑in hybrid, and full‑electric compact SUVs that leverage high‑efficiency powertrains, battery energy storage systems, and regenerative braking to reduce overall emissions and operating costs. The adoption of high voltage battery packs offering real‑world driving ranges exceeding 400 km is gaining traction among urban buyers. Manufacturers are optimizing power electronics, thermal management, and electric motor technologies to enhance reliability and performance in diverse climatic conditions.

Chassis and platform technologies continue to evolve, with modular designs allowing multiple powertrain configurations on shared architectures, enabling economies of scale while reducing development timelines. Lightweight materials such as high‑strength steel and aluminum alloys are employed to improve fuel economy without compromising structural integrity. Connectivity ecosystems are increasingly tied to cloud‑based services, allowing real‑time data analytics, remote diagnostics, and personalized driving profiles. Together, these technologies reflect a shift toward intelligent, energy‑efficient, and user‑centric compact SUV offerings that align with modern mobility demands.

• In 2025, the Ford Puma remained the UK’s best‑selling car for the third consecutive year, with 55,488 registrations, highlighting sustained consumer preference for compact SUVs, especially petrol and hybrid variants even as EV adoption remains gradual. Source: www.thescottishsun.co.uk

• In August 2025, Renault India launched the facelifted 2025 Renault Kiger, expanding its variant lineup between ₹6.29 lakh and ₹11.29 lakh, enhancing interior and technology features to strengthen competitiveness in the compact SUV segment. Source: www.timesofindia.indiatimes.com

• In September 2025, Volkswagen unveiled the new compact electric SUV concept, ID.CROSS, with an anticipated 2026 premiere and an expected price range of €28,000–€30,000, underlining the shift toward electrified compact SUV models. Source: www.reuters.com

• In January 2025, Tata Motors announced the launch of the Tata Punch Facelift, scheduled for release on January 13, 2025, with updated styling and features to enhance its position within the compact SUV market. Source: www.economictimes.com

The scope of the Compact SUV Market Report encompasses a thorough assessment of product types, key applications, geographic regions, end‑user behaviors, technology landscapes, and competitive dynamics within the global automotive ecosystem. It examines the range of compact SUV types, including conventional internal combustion engine (ICE) vehicles, hybrid electric vehicles (HEVs), plug‑in hybrids (PHEVs), and fully electric compact SUVs, detailing their features, positioning, and consumer appeal. Each type is analyzed for segmentation attributes such as powertrain configuration, feature differentiation, and usage scenarios.

The report also analyzes key applications of compact SUVs, spanning urban commuting, family mobility, fleet utilization, long‑distance travel, and premium lifestyle mobility. These application contexts reflect diverse usage patterns among demographics and underline strategic positioning for OEMs targeting specific end‑user groups. End‑user insights cover individual consumers, corporate fleets, rental and leasing providers, and government/public sector acquisitions, highlighting purchasing drivers, adoption trends, and regional behavior patterns.

Geographically, the scope includes a comprehensive review of North America, Europe, Asia Pacific, South America, and Middle East & Africa, each evaluated for infrastructure readiness, regulatory environments, consumer preferences, and automotive retail ecosystems. Regulatory and sustainability landscapes—including emissions norms, safety mandates, and electrification incentives—are integrated into regional analysis to illustrate how policy influences market trajectories.

The report’s technology segment covers ADAS, connectivity platforms, electrification technologies, modular chassis platforms, battery innovations, and digital cockpits, providing actionable insights for decision‑makers assessing future product roadmaps. Additionally, it includes competitive benchmarking, strategic initiatives by leading OEMs, and emerging market opportunities, giving stakeholders a full summary of current status and future directions in the compact SUV arena.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,126.0 Million |

| Market Revenue (2033) | USD 5,251.8 Million |

| CAGR (2026–2033) | 6.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Toyota Motor Corporation, Hyundai Motor Company, Kia Corporation, Ford Motor Company, Honda Motor Co., Ltd., Volkswagen AG, Renault Group, Nissan Motor Co., Ltd., Mahindra & Mahindra Ltd., Tata Motors Limited, Chevrolet (General Motors), Subaru Corporation, MG Motor, Peugeot S.A. |

| Customization & Pricing | Available on Request (10% Customization Free) |