Reports

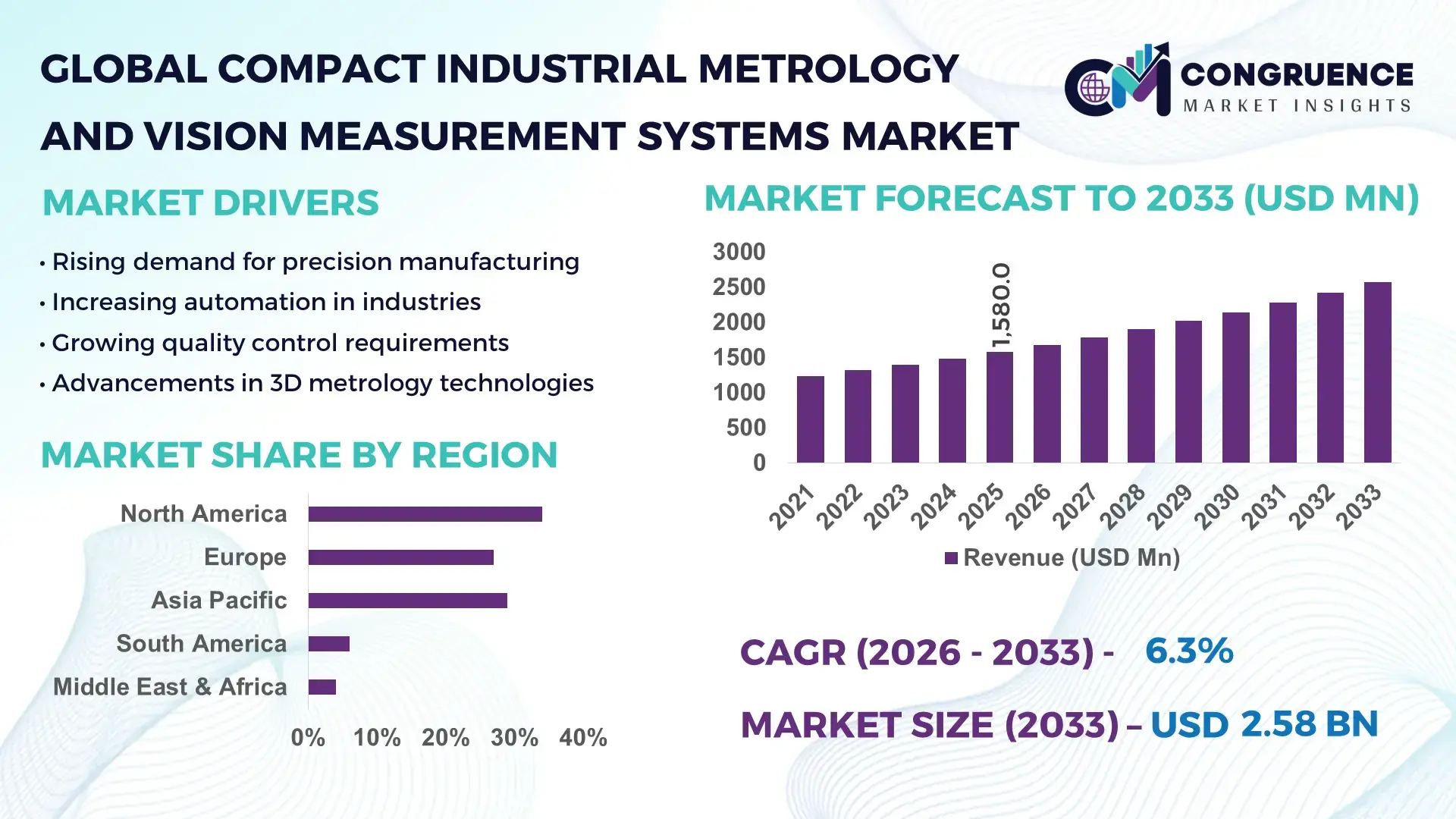

The Global Compact Industrial Metrology and Vision Measurement Systems Market was valued at USD 1,580.0 Million in 2025 and is anticipated to reach a value of USD 2,575.9 Million by 2033 expanding at a CAGR of 6.3% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by increasing adoption of automated quality inspection and precision manufacturing across industries such as automotive, electronics, and aerospace.

The United States dominates the Compact Industrial Metrology and Vision Measurement Systems Market with strong industrial infrastructure and high technology adoption. The country accounts for over 35% of global precision manufacturing output, with more than 70% of large-scale manufacturers integrating automated inspection systems into production lines. Investment in advanced manufacturing technologies exceeded USD 220 billion in 2025, with over 60% directed toward automation and quality control systems. Key industries such as aerospace and automotive contribute significantly, with aerospace manufacturers utilizing high-precision metrology systems in over 80% of component validation processes. Additionally, more than 65% of semiconductor fabrication facilities in the U.S. deploy vision-based measurement systems for defect detection and process optimization.

Market Size & Growth: USD 1,580.0 Million in 2025, projected to reach USD 2,575.9 Million by 2033, growing at 6.3% CAGR driven by rising automation in precision manufacturing.

Top Growth Drivers: Automation adoption at 68%, inspection accuracy improvement demand at 55%, and manufacturing efficiency gains of 40%.

Short-Term Forecast: By 2028, automated inspection systems are expected to reduce production defects by 30% and improve throughput by 25%.

Emerging Technologies: AI-powered vision systems, 3D optical metrology, and edge-based real-time inspection analytics.

Regional Leaders: North America projected at USD 900 Million by 2033 with high aerospace adoption; Asia-Pacific at USD 1,050 Million driven by electronics manufacturing; Europe at USD 625 Million with strong automotive integration.

Consumer/End-User Trends: Over 72% of large manufacturers prioritize inline inspection systems to enhance productivity and reduce manual errors.

Pilot or Case Example: In 2025, a semiconductor facility implemented AI vision systems achieving 35% defect reduction and 20% faster inspection cycles.

Competitive Landscape: Market leader holds ~18% share, followed by 4–5 major players focusing on innovation and product differentiation.

Regulatory & ESG Impact: Compliance with ISO quality standards has increased adoption by 50%, while energy-efficient systems reduce operational energy use by 15%.

Investment & Funding Patterns: Over USD 3 billion invested globally in industrial automation and metrology technologies during 2024–2025.

Innovation & Future Outlook: Integration of AI, IoT, and cloud-based analytics is driving predictive quality control and real-time decision-making.

The Compact Industrial Metrology and Vision Measurement Systems Market is driven by automotive (32%), electronics (28%), and aerospace (18%) sectors, with rapid integration of AI-enabled inspection tools. Increasing regulatory focus on product quality and sustainability is influencing adoption. Asia-Pacific leads consumption growth, while North America drives innovation. Future trends include smart factories, digital twins, and autonomous quality control systems.

The Compact Industrial Metrology and Vision Measurement Systems Market plays a strategic role in enabling precision manufacturing, quality assurance, and digital transformation across industrial ecosystems. As industries transition toward smart factories, the demand for compact, high-accuracy measurement systems is rising significantly. AI-enabled vision systems now deliver up to 45% improvement in defect detection accuracy compared to traditional manual inspection methods, positioning them as critical tools in modern production environments.

From a regional perspective, Asia-Pacific dominates in production volume due to its large-scale manufacturing base, while North America leads in adoption, with over 70% of enterprises integrating advanced metrology systems into automated workflows. The increasing focus on zero-defect manufacturing and real-time quality monitoring is driving continuous innovation in compact systems.

By 2028, AI-driven predictive inspection technologies are expected to reduce production downtime by 30% while improving operational efficiency by 25%. Companies are also aligning with ESG goals, committing to reducing material waste by up to 20% through enhanced quality control and precision measurement technologies.

In 2025, a leading U.S.-based semiconductor manufacturer achieved a 35% reduction in defect rates through the implementation of AI-powered vision inspection systems, demonstrating measurable performance gains. As industries continue to prioritize automation, compliance, and sustainability, the Compact Industrial Metrology and Vision Measurement Systems Market is set to emerge as a critical pillar supporting resilient and efficient industrial operations globally.

The Compact Industrial Metrology and Vision Measurement Systems Market is influenced by rapid advancements in automation, increasing demand for high-precision manufacturing, and the expansion of Industry 4.0 initiatives. The shift toward digital manufacturing environments has significantly increased the need for real-time quality inspection systems capable of delivering accurate and consistent measurements. Industries such as automotive, aerospace, and electronics are adopting compact metrology solutions to enhance production efficiency and minimize defects.

Technological advancements, including AI-based vision systems and 3D optical measurement tools, are transforming traditional inspection processes. Over 65% of manufacturers are now investing in automated inspection solutions to improve accuracy and reduce operational costs. Additionally, the growing trend of miniaturization in electronics and precision engineering is driving demand for compact and portable metrology systems. However, factors such as high initial investment costs and integration challenges continue to influence market dynamics.

The increasing demand for automated quality inspection is a primary driver of the Compact Industrial Metrology and Vision Measurement Systems Market. With over 70% of manufacturers adopting automation technologies, there is a strong need for systems that can deliver precise and consistent measurements in real-time. Automated vision systems reduce human error by up to 40% and improve inspection speed by nearly 30%, enabling manufacturers to maintain high production standards. Industries such as automotive and electronics rely heavily on high-precision measurement systems to ensure product quality and compliance with regulatory standards. The adoption of inline inspection systems has increased by more than 60% in the past five years, highlighting the growing importance of automation. Additionally, the integration of AI and machine learning algorithms enhances defect detection capabilities, further driving market demand.

High implementation and integration costs remain a significant restraint for the Compact Industrial Metrology and Vision Measurement Systems Market. Advanced metrology systems require substantial capital investment, with initial setup costs often exceeding traditional inspection methods by 30–50%. This creates a barrier for small and medium-sized enterprises with limited budgets. Additionally, the complexity of integrating these systems into existing production lines poses operational challenges. Nearly 45% of manufacturers report difficulties in aligning new metrology solutions with legacy systems. Training requirements for skilled personnel further add to the overall cost, with companies spending up to 20% more on workforce training and system maintenance. These factors collectively slow down adoption, particularly in developing regions.

The rapid adoption of Industry 4.0 presents significant opportunities for the Compact Industrial Metrology and Vision Measurement Systems Market. With over 65% of global manufacturers investing in smart factory initiatives, there is a growing demand for integrated measurement systems that support real-time data analysis and predictive maintenance. Compact metrology systems enable seamless integration with IoT platforms, allowing manufacturers to monitor production processes and detect anomalies in real-time. The use of digital twins and cloud-based analytics is expected to enhance decision-making and improve operational efficiency by up to 25%. Furthermore, the increasing adoption of robotics and automation in manufacturing creates new opportunities for advanced vision measurement systems, particularly in high-precision industries such as semiconductors and aerospace.

Integration complexities pose a major challenge for the Compact Industrial Metrology and Vision Measurement Systems Market. Many manufacturing facilities operate with legacy systems that are not compatible with advanced metrology technologies, making integration a complex and time-consuming process. Approximately 50% of manufacturers face challenges in aligning new systems with existing workflows, leading to delays in implementation. Data interoperability is another critical issue, as different systems often use incompatible data formats, limiting seamless communication. Additionally, cybersecurity concerns are increasing, with over 35% of manufacturers reporting vulnerabilities in connected systems. These challenges require significant investment in system upgrades and IT infrastructure, which can hinder market growth.

AI-powered defect detection improving accuracy by 45%: Advanced AI-based vision systems are being widely adopted, enabling real-time defect detection with up to 45% higher accuracy compared to traditional inspection methods. Over 70% of large manufacturers have integrated AI-driven inspection systems to reduce errors and enhance product quality.

Growth in 3D optical metrology adoption by 60%: The use of 3D optical measurement systems has increased significantly, with adoption rates rising by nearly 60% in precision manufacturing sectors. These systems provide high-resolution measurements and are particularly востребованы in aerospace and automotive industries for complex component analysis.

Expansion of inline inspection systems by 50%: Inline inspection systems are gaining traction, with over 50% of manufacturers implementing them to improve production efficiency. These systems reduce inspection time by up to 30% and enable continuous monitoring of production processes.

Increasing demand for portable metrology solutions by 35%: Portable and compact metrology systems are becoming more popular, with demand increasing by approximately 35%. These systems offer flexibility and ease of use, making them suitable for on-site inspections and remote applications.

The Compact Industrial Metrology and Vision Measurement Systems Market is segmented based on type, application, and end-user industries, reflecting diverse industrial requirements and technological advancements. Different types of systems cater to varying levels of precision, portability, and automation needs. Applications span across inspection, quality control, reverse engineering, and process optimization, highlighting the versatility of these systems. End-user industries such as automotive, aerospace, electronics, and healthcare drive demand, each requiring specific measurement capabilities.

The segmentation highlights a strong shift toward automated and AI-enabled systems, particularly in high-precision industries. Automotive and electronics sectors collectively account for a significant portion of demand due to their reliance on high-quality manufacturing processes. Meanwhile, emerging applications in healthcare and additive manufacturing are expanding the market scope, driven by the need for precision and compliance with stringent standards.

The Compact Industrial Metrology and Vision Measurement Systems Market includes coordinate measuring machines (CMM), optical digitizers and scanners, vision measuring systems, and portable metrology devices. Vision measuring systems currently lead with approximately 38% share due to their high-speed, non-contact inspection capabilities widely used in electronics and semiconductor manufacturing. Optical digitizers and scanners account for around 27%, driven by demand in reverse engineering and 3D modeling. Portable metrology devices represent the fastest-growing segment, expanding at an estimated CAGR of 8.5% due to their flexibility and suitability for on-site inspections. CMM systems maintain relevance with a combined share of nearly 20%, especially in high-precision industrial environments. Other niche systems contribute approximately 15% collectively, serving specialized applications.

• In 2025, a leading aerospace manufacturer deployed portable 3D scanning systems across 12 facilities, improving inspection efficiency by 28% and reducing measurement errors by 18%.

Key applications include quality control and inspection, reverse engineering, virtual simulation, and process optimization. Quality control and inspection dominate with approximately 45% share, driven by the need for defect-free production in automotive and electronics industries. Reverse engineering accounts for around 25%, supporting product design and innovation. Process optimization is the fastest-growing application, with an estimated CAGR of 8.2%, as manufacturers increasingly rely on real-time data analytics. Other applications collectively contribute nearly 30% of the market. In 2025, over 68% of enterprises globally reported adopting automated inspection systems for production lines, highlighting strong demand.

• In 2025, over 150 manufacturing plants implemented AI-based inspection systems, achieving up to 30% improvement in defect detection and operational efficiency.

The primary end-users include automotive, aerospace, electronics, healthcare, and industrial manufacturing sectors. Automotive leads with approximately 32% share, driven by stringent quality standards and high production volumes. Electronics follows with 28%, supported by the miniaturization of components and high precision requirements. Healthcare is the fastest-growing segment, expanding at an estimated CAGR of 9%, driven by increasing adoption of precision measurement in medical device manufacturing. Aerospace and other industries collectively contribute around 40%. In 2025, over 65% of manufacturers in advanced industries adopted automated metrology systems to enhance production quality.

• In 2025, a global automotive manufacturer implemented advanced vision systems across its production lines, reducing inspection errors by 25% and improving overall product quality.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

The global market demonstrates strong regional variations driven by industrial development and technological adoption. Europe holds approximately 27% share, supported by automotive and aerospace industries, while Asia-Pacific accounts for nearly 29% due to rapid industrialization and electronics manufacturing growth. South America and the Middle East & Africa collectively contribute around 10%, with increasing investments in manufacturing infrastructure. Over 70% of advanced manufacturing facilities in North America and Europe have adopted automated metrology systems, while Asia-Pacific is witnessing adoption rates exceeding 60% in electronics manufacturing hubs.

North America holds approximately 34% market share, driven by strong adoption in aerospace, automotive, and semiconductor industries. The U.S. leads regional demand with over 70% of large enterprises deploying automated inspection systems. Government initiatives supporting advanced manufacturing and quality standards have increased adoption by 40%. Technological advancements such as AI-driven inspection and digital twins are widely implemented. A key player in the region has expanded its AI-based vision systems, improving inspection efficiency by 30%. Consumer behavior reflects high enterprise adoption, particularly in healthcare and finance sectors, where precision and compliance are critical.

Europe accounts for around 27% market share, with Germany, the UK, and France leading adoption. Strong regulatory frameworks and sustainability initiatives drive demand for high-precision systems. Over 65% of manufacturers in Europe have integrated automated inspection solutions to comply with quality standards. The region is also witnessing increased adoption of 3D optical metrology systems. A local player has introduced advanced scanning solutions, enhancing measurement accuracy by 25%. Consumer behavior shows strong preference for explainable and compliant technologies due to regulatory pressure.

Asia-Pacific ranks second in market share and leads in growth volume, driven by China, Japan, and India. The region accounts for nearly 29% of global demand, supported by large-scale electronics and automotive manufacturing. Over 60% of manufacturers are adopting automated inspection systems. Rapid industrialization and smart factory initiatives are key growth drivers. A regional player has expanded production capacity, increasing system deployment by 35%. Consumer behavior indicates strong demand driven by e-commerce and mobile-enabled industrial applications.

South America holds approximately 6% market share, with Brazil and Argentina leading adoption. Infrastructure development and energy sector investments are key drivers. Government incentives for industrial automation have increased adoption by 20%. A local manufacturer has introduced cost-effective metrology solutions, improving accessibility for SMEs. Consumer behavior shows demand linked to industrial modernization and localization needs.

The Middle East & Africa region accounts for around 4% market share, driven by oil & gas and construction sectors. Countries such as the UAE and South Africa are leading adoption. Technological modernization initiatives have increased demand for advanced inspection systems by 18%. Trade partnerships and government policies support industrial growth. A regional player has implemented advanced vision systems in energy projects, improving inspection accuracy by 22%. Consumer behavior reflects growing adoption in infrastructure and industrial sectors.

United States – 34% Market share: Strong advanced manufacturing base and high adoption of automation technologies.

China – 22% Market share: Large-scale electronics and industrial production driving demand for precision systems.

The Compact Industrial Metrology and Vision Measurement Systems Market is moderately fragmented, with over 50 active global and regional players competing across various segments. The top five companies collectively hold approximately 45% of the market, indicating a competitive yet consolidated structure at the top tier. Key players focus on product innovation, strategic partnerships, and acquisitions to strengthen their market positions.

Technological differentiation is a major competitive factor, with companies investing heavily in AI-powered vision systems, 3D scanning technologies, and cloud-based analytics platforms. Over 60% of leading companies have introduced new products with enhanced automation capabilities in the past two years. Strategic collaborations between metrology solution providers and manufacturing companies have increased by 35%, enabling customized solutions for industry-specific applications.

Additionally, companies are expanding their global footprint through regional partnerships and distribution networks. Innovation trends such as real-time inspection, predictive analytics, and digital twin integration are shaping the competitive landscape, with firms aiming to enhance efficiency and reduce operational costs for end-users.

Hexagon AB

Nikon Metrology

FARO Technologies, Inc.

Keyence Corporation

Mitutoyo Corporation

Renishaw plc

KLA Corporation

Cognex Corporation

Jenoptik AG

Perceptron, Inc.

GOM GmbH

Wenzel Group GmbH

Vision Engineering Ltd.

The Compact Industrial Metrology and Vision Measurement Systems Market is undergoing rapid technological transformation driven by advancements in artificial intelligence, machine vision, and 3D optical measurement technologies. AI-powered vision systems are now capable of detecting defects with up to 45% higher accuracy compared to traditional inspection methods, significantly improving quality control processes.

The adoption of 3D optical metrology systems has increased by over 60%, enabling high-resolution measurements for complex components in industries such as aerospace and automotive. These systems utilize structured light and laser scanning technologies to deliver precise measurements in real-time. Additionally, edge computing is gaining traction, allowing real-time data processing and reducing latency by nearly 30%.

Integration with IoT platforms is another key trend, with over 65% of manufacturers implementing connected inspection systems for real-time monitoring and predictive maintenance. Digital twin technology is also being widely adopted, enabling simulation and optimization of production processes.

Cloud-based analytics platforms are enhancing data-driven decision-making, with companies reporting up to 25% improvement in operational efficiency. Furthermore, portable metrology systems are becoming increasingly popular, offering flexibility and ease of use for on-site inspections. These technological advancements are reshaping the market, enabling more efficient, accurate, and scalable measurement solutions.

• In May 2025, Carl Zeiss AGannounced the release of its ZEISS CALYPSO 2025 and PiWeb software upgrades, enhancing measurement efficiency and collaboration. The new SoftTouch Mode reduces measurement time by up to 40% while maintaining accuracy, significantly improving industrial inspection workflows. Source: www.zeiss.com

• In February 2025, Carl Zeiss AGunveiled seven new metrology innovations during its ZEISS Live Tech Reveal event, including AI-driven inspection systems, automated 3D scanning solutions, and advanced vision measuring machines designed to improve defect detection and streamline manufacturing quality processes.

• In November 2025, Carl Zeiss AGintroduced ZEISS INSPECT 2026 and updated PiWeb solutions, enabling end-to-end inspection workflows with improved data analytics and compliance capabilities, supporting faster and more efficient quality control in complex manufacturing environments.

• In 2024, Hexagon ABexpanded its industrial automation portfolio through acquisitions such as indurad and Voyansi, strengthening capabilities in autonomous solutions, digital reality, and smart manufacturing, thereby enhancing its positioning in advanced metrology and industrial intelligence systems.

The Compact Industrial Metrology and Vision Measurement Systems Market Report provides a comprehensive analysis of the global market, covering key segments including type, application, end-user industries, and regional markets. The report examines various product types such as coordinate measuring machines, optical digitizers, vision measuring systems, and portable metrology devices, highlighting their adoption across different industrial applications.

From an application perspective, the report covers quality control and inspection, reverse engineering, process optimization, and virtual simulation, providing insights into their role in enhancing manufacturing efficiency and precision. End-user analysis includes automotive, aerospace, electronics, healthcare, and industrial manufacturing sectors, each contributing significantly to market demand.

Geographically, the report analyzes key regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, offering insights into regional adoption patterns, technological advancements, and industrial growth trends. The report also explores emerging technologies such as AI-driven vision systems, 3D optical metrology, and IoT-enabled inspection platforms.

Additionally, the scope includes analysis of regulatory frameworks, ESG initiatives, and investment trends shaping the market landscape. It provides detailed insights into competitive dynamics, innovation strategies, and future growth opportunities, enabling decision-makers to make informed business decisions and strategic investments in the Compact Industrial Metrology and Vision Measurement Systems Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,580.0 Million |

| Market Revenue (2033) | USD 2,575.9 Million |

| CAGR (2026–2033) | 6.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Carl Zeiss AG; Hexagon AB; Nikon Metrology; FARO Technologies, Inc.; Keyence Corporation; Mitutoyo Corporation; Renishaw plc; KLA Corporation; Cognex Corporation; Jenoptik AG; Perceptron, Inc.; GOM GmbH; Wenzel Group GmbH; Vision Engineering Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |