Reports

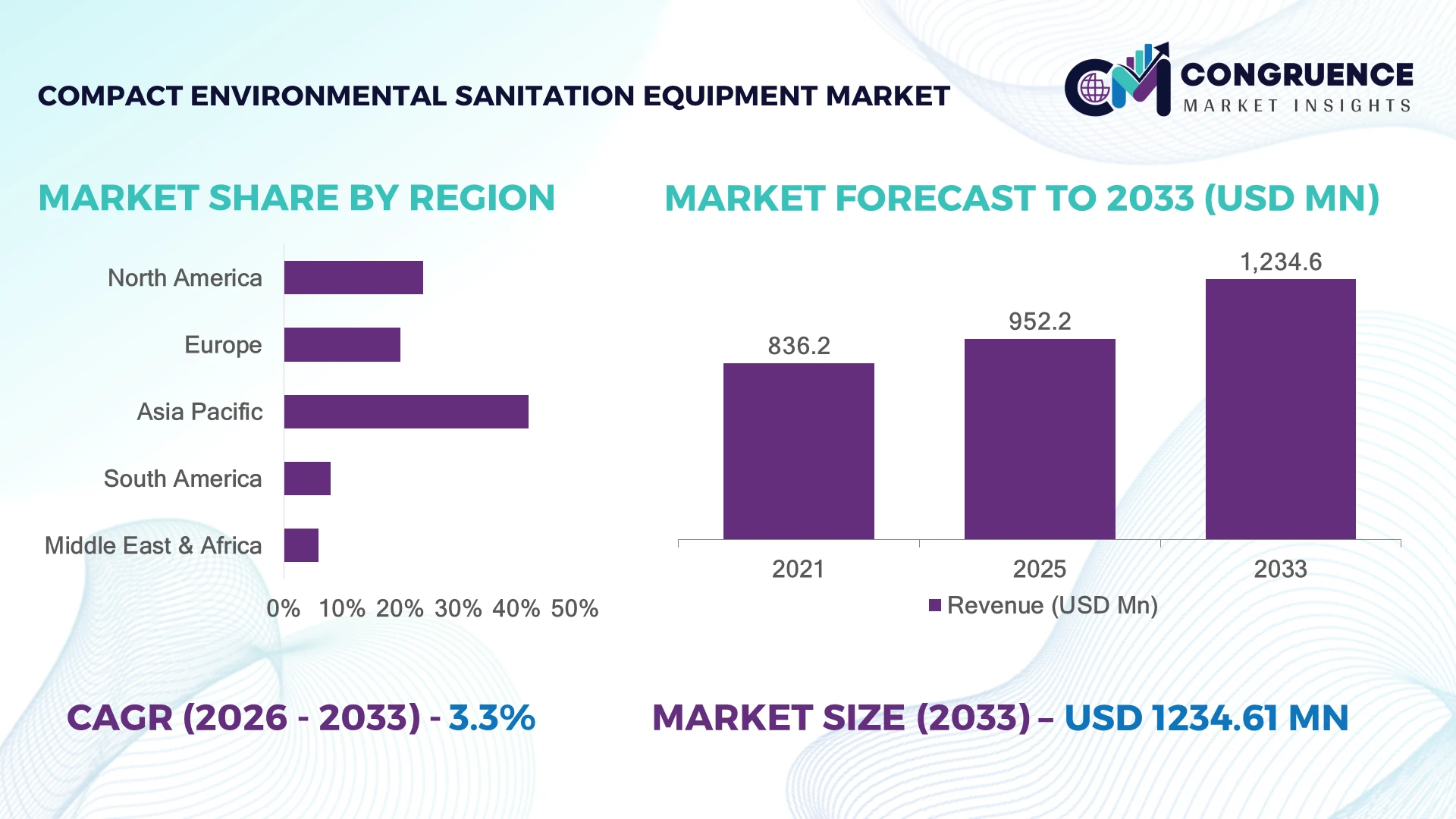

The Global Compact Environmental Sanitation Equipment Market was valued at USD 952.2 Million in 2025 and is anticipated to reach a value of USD 1,234.6 Million by 2033 expanding at a CAGR of 3.3% between 2026 and 2033. Growth is driven by decentralized wastewater treatment adoption, compact modular sanitation systems, and stricter urban environmental compliance requirements.

China dominates the market with nearly 34% share, supported by municipal sanitation upgrades, rural wastewater programs, and investments in smart environmental infrastructure. India accounts for around 15% adoption, driven by sanitation modernization initiatives and decentralized treatment deployment across industrial clusters. China’s installed compact treatment capacity exceeds India’s by over 40%, while Japan leads in automation integration with more than 60% of advanced sanitation facilities using digital monitoring systems.

Strategic focus on scalable sanitation technologies will define competitive positioning as cities prioritize efficient environmental infrastructure.

Market Size & Growth: USD 952.2 Million in 2025 to USD 1,234.6 Million by 2033 at 3.3% CAGR, driven by modular sanitation technology adoption and urban infrastructure modernization.

Top Growth Drivers: Decentralized wastewater treatment (34%), smart monitoring adoption (28%), and regulatory sanitation upgrades (22%) are accelerating market expansion.

Short-Term Forecast: By 2028, automated sanitation systems are expected to reduce operational costs by 15% and improve treatment efficiency by 20%.

Emerging Technologies: AI-based monitoring, IoT-enabled sanitation equipment, and advanced membrane filtration systems are reshaping compact treatment solutions.

Regional Leaders: Asia Pacific reaches USD 620 Million by 2033 with rural sanitation expansion; North America reaches USD 310 Million with smart infrastructure adoption; Europe reaches USD 250 Million with ESG-driven upgrades.

Consumer/End-User Trends: Over 45% of municipal and industrial users are adopting compact systems for space-efficient sanitation operations.

Pilot/Case Example: In 2024, decentralized sanitation projects in China achieved nearly 25% energy reduction through automated treatment optimization.

Competitive Landscape: Leading players hold approximately 35% combined share, including Xylem, Veolia, SUEZ, Evoqua Water Technologies, and Trojan Technologies.

Regulatory & ESG Impact: New environmental compliance programs are driving over 30% improvement targets in wastewater efficiency and resource recovery.

Investment & Funding: More than USD 1.5 Billion is directed toward water infrastructure modernization, partnerships, and sustainable sanitation expansion.

Innovation & Future Outlook: Next-generation compact systems integrating AI, renewable energy, and circular water management are becoming strategic priorities.

Compact Environmental Sanitation Equipment Market solutions are gaining importance across municipalities, industrial facilities, and remote communities due to increasing pressure for efficient sanitation infrastructure. Advanced filtration, automated monitoring, and modular treatment units are improving operational reliability, with more than 40% of new installations incorporating digital control features. Global supply-chain localization and stricter environmental standards are accelerating adoption of compact sanitation technologies across emerging economies, creating a stronger foundation for strategic market expansion.

The Compact Environmental Sanitation Equipment Market is becoming strategically important as governments, industries, and municipalities seek efficient solutions for wastewater management, environmental compliance, and infrastructure modernization. Rising urban density, limited land availability, and stricter discharge regulations are shifting investment toward modular and decentralized sanitation systems.

A major market shift is the transition from conventional centralized treatment facilities toward smart compact units with automated monitoring. Compared with legacy systems, advanced compact equipment using membrane filtration and digital controls improves operational efficiency by approximately 20% while reducing maintenance requirements by nearly 15%. Europe emphasizes regulatory-driven upgrades, while Asia Pacific focuses on large-scale deployment for rapidly expanding urban and industrial zones.

Over the next 2–3 years, companies are prioritizing partnerships, localized manufacturing, and technology integration to strengthen deployment capabilities. Municipal wastewater projects, industrial parks, and remote infrastructure developments are adopting compact systems to achieve faster installation and improved resource management. Strategic investments in automation, energy-efficient designs, and sustainable treatment processes will determine long-term competitive advantage and market leadership.

The shift toward decentralized sanitation infrastructure is a major growth driver as municipalities and industries seek space-efficient treatment solutions. China’s rural wastewater programs have increased adoption of compact systems, with decentralized projects representing over 35% of new small-scale treatment deployments. Smart monitoring integration has improved operational efficiency by nearly 25%, encouraging companies to invest in IoT-enabled equipment and automated controls. India’s industrial clusters are increasingly deploying modular sanitation units to meet stricter discharge requirements. Manufacturers are responding through technology partnerships, local production expansion, and advanced membrane filtration innovation to capture demand for flexible environmental solutions.

Compact environmental sanitation equipment faces scalability constraints due to installation costs, infrastructure readiness, and component supply dependencies. Imported filtration membranes and specialized control systems contribute nearly 20–30% of equipment costs in several developing markets, affecting project economics. In countries such as India and Brazil, limited wastewater networks restrict rapid deployment despite rising sanitation requirements. Regulatory variations across municipalities create additional compliance complexity, increasing project timelines by approximately 15%. Companies are reducing these pressures through localized manufacturing, supplier diversification, and standardized modular designs. The key operational challenge remains balancing affordability with advanced treatment performance.

The integration of digital technologies is creating opportunities for smarter sanitation management and predictive operations. AI-based monitoring and remote diagnostics can reduce maintenance requirements by around 20% while improving equipment uptime by nearly 30%. Japan’s advanced water management ecosystem demonstrates how automation and sensor-based systems can optimize compact treatment performance. Emerging markets including Indonesia and Vietnam are adopting modular sanitation solutions for industrial parks and urban expansion zones. Companies are increasing R&D investments, forming technology partnerships, and developing cloud-connected platforms to unlock recurring service models. The strongest opportunity lies in combining compact hardware with data-driven environmental management solutions.

Long-term market expansion faces challenges related to technology integration, skilled workforce availability, and operational consistency across diverse environments. Approximately 40% of sanitation operators in developing economies still rely on manual monitoring practices, creating barriers to advanced equipment adoption. Cybersecurity concerns are increasing as connected sanitation systems incorporate remote controls and cloud-based analytics, with industrial operators prioritizing stronger protection frameworks. In countries such as Mexico and South Africa, inconsistent infrastructure conditions affect deployment reliability and maintenance schedules. Companies must address these challenges through workforce training, resilient system design, cybersecurity investment, and strategic partnerships that ensure reliable sanitation operations.

Smart Monitoring Expansion IoT-enabled sanitation equipment adoption is accelerating as operators prioritize remote supervision and predictive maintenance. Over 40% of newly deployed compact systems now integrate digital monitoring capabilities, while automated controls improve operational visibility by nearly 25%. China’s municipal projects are increasingly using connected treatment units to manage dispersed wastewater assets. Companies are responding by scaling sensor integration, developing cloud-based platforms, and forming technology partnerships to improve lifecycle performance and reduce service costs.

Modular Design Shift Compact sanitation manufacturers are shifting toward modular and prefabricated designs to shorten installation timelines and address infrastructure limitations. Modular systems can reduce deployment time by approximately 30% compared with conventional treatment setups, while standardized components lower maintenance complexity by nearly 20%. Industrial parks in India and Southeast Asia are adopting flexible units for faster capacity expansion. Companies are restructuring production networks and expanding local assembly capabilities to improve supply-chain resilience.

Energy Efficiency Focus Energy optimization is becoming a key purchasing factor as operators face rising utility costs and sustainability requirements. Advanced compact treatment technologies using improved filtration and automation reduce energy consumption by around 15–25% compared with older systems. European environmental regulations are accelerating demand for low-energy sanitation solutions, pushing manufacturers toward efficient pumps, recovery systems, and optimized operating models. Companies are investing in greener designs and performance-based service agreements.

Decentralized Deployment Growth Decentralized sanitation adoption is increasing due to urban expansion, rural infrastructure needs, and stricter wastewater regulations. Small-scale treatment installations account for more than 35% of new sanitation projects in several developing markets, creating demand for portable and scalable solutions. Vietnam and Brazil are expanding decentralized wastewater programs to support underserved communities. Companies are responding through regional partnerships, customized solutions, and application-specific equipment development.

Modular compact sanitation equipment represents the leading type due to its flexibility, faster installation, and suitability for decentralized infrastructure projects. These systems account for nearly 45% of new deployments as municipalities and industries prioritize scalable wastewater treatment solutions. Traditional compact treatment units remain widely used because of established operating experience and lower maintenance requirements, while advanced integrated systems are gaining attention for automation and higher treatment efficiency. Companies are expanding modular product portfolios and investing in standardized designs to reduce deployment complexity. Advanced smart-enabled sanitation equipment is the fastest-growing type, supported by increasing adoption of remote monitoring, AI-based diagnostics, and automated process control. Adoption of digitally integrated systems has increased by approximately 30% in industrial applications, creating new investment priorities around connected infrastructure. Manufacturers are focusing on partnerships with technology providers to combine treatment hardware with analytics platforms.

Municipal wastewater treatment is the leading application segment due to large-scale sanitation requirements, urban expansion, and government-led infrastructure modernization programs. Municipal projects contribute nearly 50% of compact sanitation equipment demand as cities seek efficient solutions for limited-space environments. Industrial wastewater management is also expanding as manufacturing facilities face stricter discharge standards and require localized treatment capabilities. Companies are responding by developing application-specific systems with improved automation and compliance features. Remote community sanitation and emergency treatment applications represent the fastest-growing use cases, driven by infrastructure gaps and rapid deployment requirements. Adoption in these applications has increased by around 25% as governments and organizations prioritize flexible sanitation solutions. China and India are expanding compact systems for rural and semi-urban areas, while industrial users are integrating compact units into distributed facilities. Manufacturers are strengthening partnerships with infrastructure developers to improve project execution.

Municipalities represent the leading end-user group due to extensive sanitation infrastructure requirements and government investment programs. Public-sector projects account for approximately 55% of compact sanitation equipment deployments, supported by wastewater compliance initiatives and urban infrastructure upgrades. Industrial facilities are becoming increasingly important buyers as sectors such as food processing, manufacturing, and chemicals require efficient onsite treatment solutions. Companies are targeting municipalities through long-term service contracts and customized infrastructure partnerships. Industrial users are the fastest-growing end-user segment as businesses prioritize water reuse, regulatory compliance, and operational efficiency. Industrial adoption has increased by nearly 30% in facilities implementing sustainability-focused water management strategies. Commercial establishments and residential communities are also adopting compact systems where centralized networks are limited. Manufacturers are responding through flexible pricing models, customized equipment packages, and ecosystem partnerships.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

North America holds approximately 24% of the global compact environmental sanitation equipment market, supported by wastewater modernization programs, industrial compliance requirements, and increasing adoption of decentralized treatment systems. The United States represents the largest deployment base, with municipal and industrial facilities accounting for over 60% of regional installations. Advanced monitoring, automated controls, and energy-efficient treatment technologies are reshaping operational strategies. Infrastructure investment programs are encouraging partnerships between technology providers and water management companies, with several operators integrating remote diagnostics to improve system efficiency by nearly 20%. Companies are expanding service networks and developing smart sanitation platforms to strengthen long-term maintenance capabilities.

United States Market Outlook: The United States remains the regional technology leader due to strong municipal infrastructure and industrial wastewater demand. More than 50% of newly developed compact sanitation projects incorporate automation features, particularly across manufacturing, commercial facilities, and decentralized community systems. Companies are increasing investment in digital treatment solutions and localized service capabilities to support regulatory compliance.

Europe contributes nearly 20% of global compact environmental sanitation equipment demand, driven by strict wastewater regulations, sustainability targets, and modernization of aging infrastructure. Germany, France, and the United Kingdom represent major deployment markets where industrial facilities and municipalities are upgrading treatment capabilities. More than 45% of new sanitation installations incorporate energy-saving components and automated monitoring systems to improve environmental performance. The European Union’s circular water management initiatives are encouraging adoption of compact systems that support resource recovery and efficient operation. Companies are strengthening partnerships with engineering firms and expanding sustainable product portfolios to meet evolving compliance requirements.

Germany Market Outlook: Germany leads European adoption through advanced industrial infrastructure and strong environmental engineering capabilities. Around 40% of industrial wastewater facilities are implementing digitally monitored treatment processes to improve operational control. Manufacturers are focusing on energy-efficient equipment, automation integration, and customized solutions for industrial clusters.

Asia-Pacific dominates the compact environmental sanitation equipment market with approximately 42% share, supported by rapid urbanization, industrial expansion, and government sanitation initiatives. China, India, Japan, and South Korea are major contributors due to large-scale infrastructure programs and manufacturing capabilities. China accounts for nearly 35% of regional demand, supported by rural wastewater treatment upgrades and smart sanitation deployment. India is increasing adoption across industrial zones and developing communities, while Japan focuses on automation-driven treatment systems. Companies are expanding local manufacturing facilities and forming infrastructure partnerships to improve supply availability and reduce installation timelines by nearly 25%.

China Market Outlook: China remains the largest country-level market due to extensive municipal sanitation modernization and domestic equipment production strength. Over 50% of newly commissioned decentralized treatment projects include compact modular systems. Manufacturers are investing in smart monitoring technologies and regional production capacity to support nationwide environmental infrastructure development.

South America represents nearly 8% of global compact environmental sanitation equipment demand, with adoption concentrated in Brazil, Argentina, and Chile. Limited centralized wastewater infrastructure and increasing environmental compliance requirements are encouraging decentralized treatment deployment. Brazil accounts for more than 45% of regional demand due to industrial wastewater applications and municipal sanitation initiatives. Mining, food processing, and agricultural industries are adopting compact systems to improve water management efficiency. Companies are expanding partnerships with local engineering providers and developing affordable modular solutions. However, infrastructure limitations continue to influence project timelines, requiring manufacturers to focus on flexible installation models.

Brazil Market Outlook: Brazil leads regional adoption through industrial activity, water management requirements, and expanding sanitation investment. Approximately 30% of industrial facilities implementing wastewater upgrades are considering compact treatment technologies. Companies are targeting agricultural and industrial clusters with customized systems designed for operational efficiency and regulatory alignment.

Middle East & Africa is emerging as a high-potential market, supported by water scarcity challenges, infrastructure modernization programs, and government-led sustainability initiatives. The region accounts for approximately 6% of global demand, with adoption concentrated in the United Arab Emirates, Saudi Arabia, and South Africa. Desalination-linked water management projects and industrial developments are increasing demand for compact treatment solutions. Saudi Arabia’s water infrastructure transformation programs are accelerating investment in efficient sanitation technologies, while African markets are adopting decentralized systems for underserved communities. Companies are forming public-private partnerships and expanding regional service capabilities to address deployment challenges and operational requirements.

Saudi Arabia Market Outlook: Saudi Arabia is a strategic market due to large-scale water infrastructure investments and industrial diversification programs. More than 35% of new water management projects incorporate advanced monitoring and efficiency-focused technologies. Companies are prioritizing local partnerships and customized sanitation solutions to support long-term infrastructure transformation.

The compact environmental sanitation equipment market features global technology leaders competing with regional manufacturers and specialized OEM suppliers. Veolia, SUEZ, Xylem, and Pentair compete through advanced treatment technologies, service networks, and integrated water solutions, while regional players focus on cost efficiency and customized deployments. The top five companies collectively account for approximately 35% of market share, reflecting a moderately fragmented structure. Competition is centered on automation, lifecycle costs, modular design, and supply-chain reliability, with digital systems improving operational efficiency by 20–30%. Global players are expanding through partnerships, localized manufacturing, and technology acquisitions, while cost-focused manufacturers strengthen regional penetration. The market is shifting toward smart sanitation platforms and vertically integrated solutions as operators demand faster installation and lower maintenance. High technical expertise, regulatory compliance, and infrastructure partnerships create entry barriers. Winning players must combine innovation, scalable production, and localized service capabilities.

SUEZ

Xylem Inc.

Pentair plc

Ecolab Inc.

Kurita Water Industries Ltd.

Aquatech International LLC

Fluence Corporation Limited

Trojan Technologies

Organica Water

Bio-Microbics Inc.

Kubota Corporation

Compact environmental sanitation equipment is increasingly integrating smart monitoring, membrane filtration, and automated process controls to improve treatment reliability. IoT-enabled systems allow real-time performance tracking and reduce operational intervention by nearly 25%, while advanced membrane technologies improve contaminant removal efficiency by approximately 20% compared with conventional biological systems. Companies such as Veolia and Xylem are prioritizing connected solutions to strengthen service models and lifecycle management.

Emerging technologies include AI-driven analytics, digital twins, and energy-efficient treatment modules that optimize chemical usage, maintenance schedules, and resource recovery. AI-based monitoring platforms are gaining adoption across more than 30% of newly developed advanced wastewater projects, enabling predictive maintenance and reducing downtime. Compared with older manual systems, automated compact units deliver nearly 15–20% higher operational efficiency.

Between 2026 and 2028, competitive advantage will increasingly depend on integrated technology ecosystems combining hardware, software, and remote management capabilities. Manufacturers investing in automation, decentralized treatment designs, and data-driven services will benefit from faster deployment cycles and stronger customer retention.

May 2024 Veolia Water Technologies introduced its Cella™ biofilm technology at Denmark’s Svinninge wastewater facility, creating a compact treatment solution that increased plant capacity by 40% to 6,300 population equivalents. The project strengthened decentralized wastewater capabilities and demonstrated energy-efficient treatment deployment. Source: www.veoliawatertechnologies.com

May 2025 Xylem launched its Partnerships Accelerator program, selecting 13 startups from nine countries focused on water security technologies, including AI leak detection and wastewater resource recovery. The initiative expanded innovation collaboration and accelerated digital water technology adoption. Source: www.xylem.com

June 2025 SUEZ inaugurated the Eaux Blanches wastewater treatment plant in France, integrating advanced environmental technologies for climate-resilient water management. The facility supported regional modernization efforts and improved sustainable wastewater operations in a sensitive coastal area. Source: www.suez.com

2024 Veolia expanded ultra-compact wastewater solutions through automated treatment technologies capable of processing up to 3,000 liters per hour while achieving up to 99.9% hydrocarbon removal efficiency. The innovation supports industrial customers requiring smaller treatment footprints.

The report covers the global compact environmental sanitation equipment landscape across major types, applications, end-users, and geographic markets. The analysis evaluates modular systems, integrated treatment technologies, municipal wastewater applications, industrial deployments, and emerging decentralized sanitation solutions. It examines adoption patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa with emphasis on infrastructure development and technology integration.

The study provides strategic insights into automation adoption, digital monitoring, membrane technologies, competitive positioning, and evolving sanitation business models. With more than 10 major companies analyzed, the report supports investment decisions, expansion planning, partnership strategies, and competitive benchmarking. It highlights deployment trends, operational improvements, and future technology directions shaping market opportunities between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 952.2 Million |

| Market Revenue (2033) | USD 1,234.6 Million |

| CAGR (2026–2033) | 3.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Veolia Water Technologies; SUEZ; Xylem Inc.; Pentair plc; Ecolab Inc.; Kurita Water Industries Ltd.; Aquatech International LLC; Fluence Corporation Limited; Trojan Technologies; Organica Water; Bio-Microbics Inc.; Kubota Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |