Reports

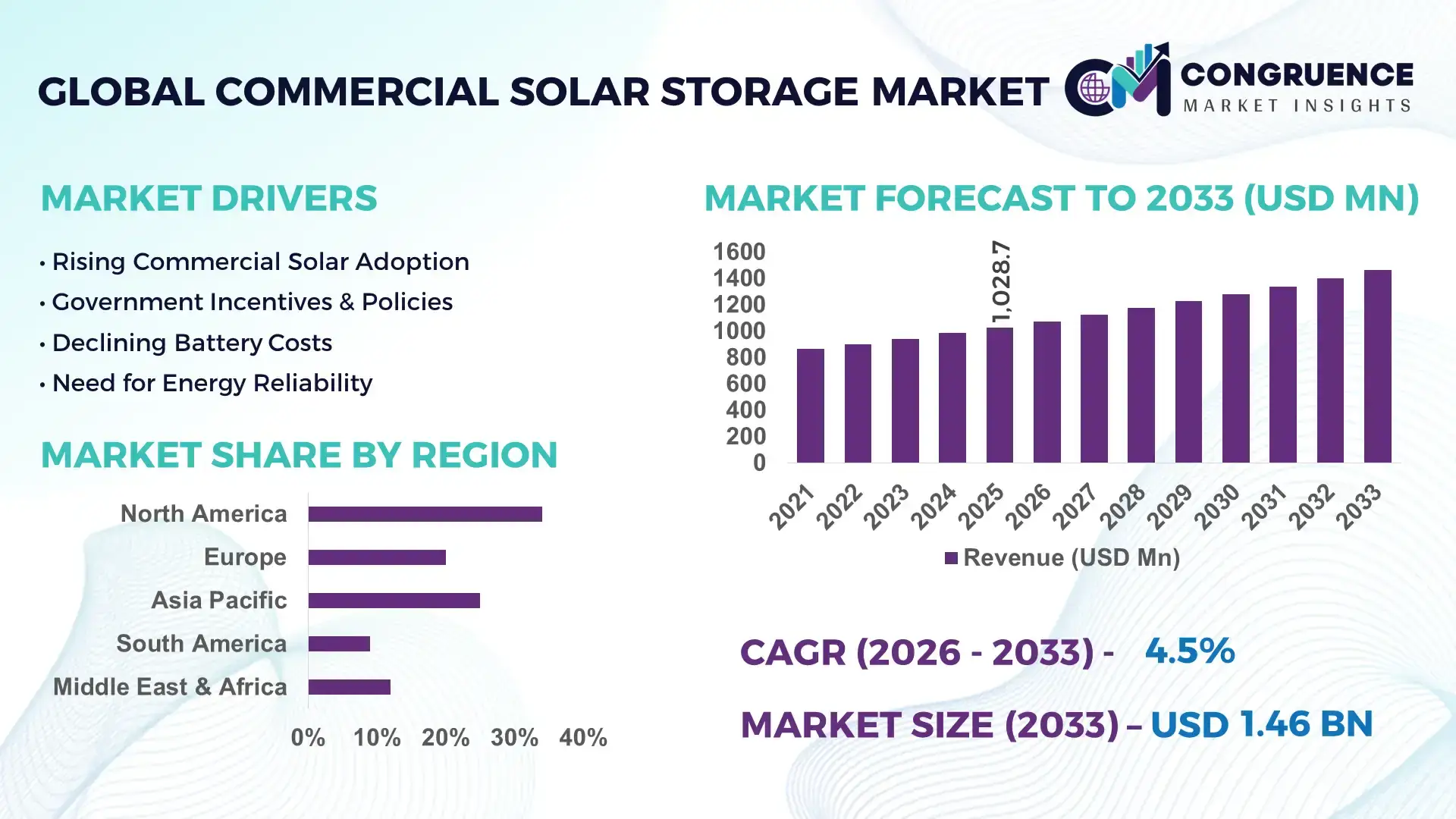

The Global Commercial Solar Storage Market was valued at USD 1028.68 Million in 2025 and is anticipated to reach a value of USD 1462.89 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. This growth is driven by increasing deployment of battery-backed solar systems to improve energy reliability and manage peak demand costs in commercial facilities.

The United States represents the most advanced commercial solar storage ecosystem, supported by large-scale battery manufacturing expansion and sustained investment in distributed energy resources. Commercial and industrial installations increasingly pair rooftop solar with lithium-ion and LFP battery systems exceeding 250 kWh capacity per site. More than 35 U.S. states have active energy storage incentives or resilience programs supporting commercial adoption. Key applications include data centers, cold storage logistics, retail chains, and healthcare campuses, where backup duration requirements range from 2–6 hours. Technological progress includes AI-driven energy management platforms, DC-coupled architectures, and integration with building automation systems, enabling load shifting and demand charge reduction across multi-facility portfolios.

• Market Size & Growth: USD 1028.68M (2025) to USD 1462.89M (2033), CAGR 4.5%, driven by commercial energy cost optimization and resilience demand.

• Top Growth Drivers: Solar-plus-storage adoption +18%, battery efficiency gains +22%, corporate clean-energy procurement +25%.

• Short-Term Forecast: By 2028, system costs decline 15% while usable storage performance improves 10%.

• Emerging Technologies: AI energy optimization, solid-state battery R&D, hybrid solar-storage microgrid architectures.

• Regional Leaders: North America ~USD 8.3B by 2033 (resilience focus); Europe ~USD 5.6B (grid flexibility demand); Asia Pacific ~USD 6.9B (industrial adoption growth).

• Consumer/End-User Trends: Retail, manufacturing, logistics, and commercial real estate adopt systems for peak shaving and backup continuity.

• Pilot or Case Example: 2025 multi-site commercial project achieved 12% peak load reduction and 9% improved energy continuity.

• Competitive Landscape: Market leader ~30% share; key players include Tesla, BYD, Sungrow, Schneider Electric, and SolarEdge.

• Regulatory & ESG Impact: Storage incentives, carbon reporting mandates, and demand charge reforms support deployment.

• Investment & Funding Patterns: Over USD 1.5B recent project finance, rise in storage-as-a-service and energy leasing models.

• Innovation & Future Outlook: Growth in modular systems, second-life EV battery use, and scalable commercial microgrids.

Commercial solar storage demand is strongest in manufacturing (≈28%), commercial real estate (≈24%), retail chains (≈18%), and logistics facilities (≈15%) where load variability and outage sensitivity are high. Advancements in modular battery racks, thermal management, and predictive analytics are improving lifecycle performance. Regulatory support for grid services participation and carbon reduction targets further stimulates adoption. North America and Europe remain mature consumption hubs, while Asia Pacific shows accelerated growth due to industrial electrification and energy security priorities. Long-term outlook centers on integrated energy management, hybrid microgrids, and higher-density storage chemistries enabling longer-duration commercial applications.

The Commercial Solar Storage Market holds strategic relevance as enterprises transition toward energy resilience, cost predictability, and decarbonization mandates. Commercial facilities with integrated solar-plus-storage systems reduce peak grid dependency by 15–30% while improving power continuity during outages. Lithium iron phosphate (LFP) battery systems are increasingly preferred, as advanced LFP chemistries deliver 18% longer cycle life improvement compared to conventional NMC battery standards used a decade earlier. This shift supports longer asset utilization and improved lifecycle economics for commercial portfolios.

Asia Pacific dominates in installation volume due to rapid industrial solar capacity expansion, while North America leads in adoption, with nearly 42% of medium-to-large enterprises integrating or planning onsite storage for operational resilience. By 2028, AI-driven energy optimization platforms are expected to improve battery dispatch efficiency by 20%, reducing unnecessary cycling and extending system lifespan. Firms are committing to ESG metrics including a 35% reduction in Scope 2 emissions and battery recycling rates exceeding 60% by 2030, aligning storage adoption with sustainability reporting frameworks.

In 2025, a large U.S. commercial real estate portfolio achieved a 14% reduction in demand charges through AI-enabled load forecasting and storage dispatch integration. These developments position the Commercial Solar Storage Market as a foundational pillar for grid resilience, regulatory compliance, and long-term sustainable growth across commercial infrastructure.

Frequent grid disturbances and extreme weather events are prompting commercial operators to invest in onsite energy resilience. Facilities such as hospitals, cold storage warehouses, and data centers require uptime reliability above 99.9%, making battery-backed solar systems essential. Demand charges can represent up to 40% of commercial electricity bills in urban markets, and storage-enabled peak shaving reduces peak load by 15–25%. Additionally, electrification of building systems, including HVAC and fleet charging, increases load volatility, strengthening the business case for integrated storage. Energy independence initiatives and corporate sustainability commitments further support adoption, with many enterprises targeting over 50% renewable electricity usage within operational portfolios. These combined factors are accelerating deployment of commercial-scale battery systems across multi-site property networks.

Despite long-term operational savings, initial capital expenditure for commercial storage systems remains substantial, especially for projects exceeding 500 kWh capacity. Balance-of-system components, fire safety compliance, thermal management, and advanced monitoring software add significant cost layers. Interconnection approval processes can extend beyond 9–12 months in certain regions due to grid capacity studies and safety regulations. Space constraints in urban commercial buildings further complicate installation, requiring structural assessments and ventilation modifications. Insurance requirements for battery systems have also tightened, increasing compliance expenses. These financial and logistical factors delay decision cycles and may discourage smaller commercial entities from adopting storage solutions without third-party financing or incentive support mechanisms.

The integration of AI-enabled energy management systems with commercial storage creates opportunities for optimized energy dispatch, predictive maintenance, and participation in grid services markets. Smart platforms can forecast load patterns with accuracy above 90%, enabling dynamic battery scheduling that enhances usable capacity by nearly 12%. Commercial operators can monetize storage assets through demand response participation, frequency regulation, and virtual power plant aggregation. Growing adoption of EV charging infrastructure in commercial complexes also increases demand for onsite buffering solutions to prevent grid overload. Modular battery designs allow scalable deployments aligned with facility expansion, while second-life EV batteries present cost-efficient storage alternatives. These developments open new revenue streams and improve total asset utilization for commercial energy portfolios.

Commercial battery installations must comply with stringent fire safety codes, electrical standards, and local permitting requirements that vary widely across jurisdictions. Compliance with updated building and fire codes often requires dedicated enclosures, monitoring systems, and thermal suppression technologies, increasing project timelines. Grid interconnection standards differ by utility, complicating system design and delaying commissioning. Recycling and end-of-life battery handling regulations are evolving, adding uncertainty around long-term compliance costs. Additionally, supply chain fluctuations for battery materials and power electronics can impact equipment availability and project scheduling. These factors collectively create operational and regulatory hurdles that require careful planning and specialized expertise for successful deployment.

• Rise in Modular and Prefabricated System Deployment: Commercial solar storage projects increasingly use modular battery enclosures and skid-mounted systems, reducing onsite installation time by nearly 30% and lowering labor requirements by 22%. Standardized containerized storage units between 250 kWh and 2 MWh now represent over 48% of new commercial deployments, enabling faster permitting and easier scalability for multi-facility operators.

• Expansion of AI-Driven Energy Optimization Platforms: More than 40% of newly commissioned commercial solar storage systems now incorporate AI-based energy management software capable of improving dispatch accuracy by 18–25%. Predictive load forecasting reduces battery degradation rates by approximately 12%, while automated peak shaving algorithms cut grid demand peaks by up to 20% in large commercial buildings.

• Increasing Adoption of Lithium Iron Phosphate (LFP) Chemistries: LFP batteries account for nearly 60% of new commercial storage installations due to higher thermal stability and cycle life exceeding 6,000 cycles, about 20% longer than earlier nickel-based chemistries. Safety incident rates have declined by 15% with improved battery management systems, strengthening acceptance in urban commercial infrastructure.

• Integration with EV Charging and Microgrid Infrastructure: Approximately 35% of commercial properties installing solar storage now pair systems with electric vehicle charging hubs. Onsite storage reduces charging-related peak loads by 25% and enables self-consumption of solar energy above 70% during daylight hours, supporting facility electrification and improving operational energy resilience.

The Commercial Solar Storage Market segmentation reflects diversified deployment patterns shaped by system configuration, operational objectives, and sector-specific energy requirements. By type, lithium-ion battery systems dominate installations due to energy density, modularity, and lifecycle performance advantages. Application segmentation shows peak shaving and load management as primary use cases, while backup power and microgrid integration gain traction in resilience-focused environments. From an end-user perspective, commercial real estate, manufacturing, and logistics facilities collectively represent the highest concentration of installations because of load variability and high demand charge exposure. System sizes most commonly range between 100 kWh and 2 MWh, covering over 65% of commercial projects, indicating strong demand for mid-scale distributed storage. Deployment strategies also differ regionally, with urban markets favoring compact indoor systems and industrial zones adopting containerized outdoor units for scalability. These segmentation patterns illustrate a shift from pilot installations toward standardized, performance-optimized commercial energy infrastructure.

Lithium-ion battery systems account for approximately 62% of commercial solar storage installations, leading due to high round-trip efficiency exceeding 90%, compact footprint, and declining degradation rates. Flow batteries represent about 18%, valued for long-duration discharge capability above 6 hours, though adoption remains limited to specialized industrial sites. Lead-acid and other chemistries collectively contribute nearly 20%, primarily in cost-sensitive or legacy system upgrades.

While lithium-ion remains dominant, flow battery adoption is rising fastest with an estimated 8.5% CAGR, driven by demand for extended-duration storage supporting critical loads and microgrid operations. Improvements in electrolyte stability and system lifespan beyond 10,000 cycles strengthen their industrial appeal. Advanced lithium iron phosphate variants continue expanding within the lithium-ion category due to improved thermal safety.

Peak shaving and demand charge management represent the leading application, accounting for about 44% of system usage, as commercial electricity tariffs often allocate up to 40% of costs to peak demand. Backup power applications hold 28%, especially in healthcare and data centers where continuity standards exceed 99.9%. Energy arbitrage and participation in grid services make up roughly 16%, while microgrid integration and renewable smoothing represent the remaining 12%.

Backup power is the fastest-growing application with an estimated 9% CAGR, fueled by grid reliability concerns and extreme weather events. Facilities increasingly require 2–4 hours of autonomous backup, expanding storage capacity requirements. EV charging support within commercial complexes also strengthens multi-use application models.

Commercial real estate leads adoption with around 38% of installations, as office parks and retail complexes manage variable loads and sustainability mandates. Manufacturing facilities account for 27%, driven by process stability requirements and high energy intensity. Logistics and cold storage contribute 19%, where temperature control reliability is critical. Healthcare, education, and other institutional users collectively hold 16%.

Logistics and warehousing represent the fastest-growing end-user segment, expanding at approximately 10% CAGR due to electrified material handling systems and 24/7 operational models. Cold storage sites increasingly deploy 500 kWh–1.5 MWh systems to protect temperature-sensitive inventory.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

Regional dynamics are shaped by infrastructure maturity, commercial electrification rates, and distributed energy policy frameworks. Europe follows with 28% share, driven by decarbonization mandates across commercial real estate and industrial sectors. Asia-Pacific holds 26% share, supported by rapid rooftop solar additions exceeding 18 GW annually in commercial and industrial segments. South America contributes 7%, where commercial storage is tied to grid reliability gaps and rising industrial solar adoption. Middle East & Africa represent 5%, with demand concentrated in commercial complexes, hospitality infrastructure, and industrial free zones. System sizes between 250 kWh and 1.5 MWh account for nearly 61% of regional installations, reflecting mid-scale commercial load balancing requirements. Over 45% of new commercial buildings in developed markets now integrate solar-ready electrical infrastructure, enabling smoother storage retrofits and multi-asset energy management deployment.

How is digital energy optimization reshaping commercial power reliability strategies?

North America represents approximately 34% of global Commercial Solar Storage installations, with strong demand from healthcare campuses, data centers, logistics hubs, and large retail chains. Demand charge management programs influence over 55% of commercial electricity tariffs, encouraging storage-backed peak shaving. Policy mechanisms such as investment tax credits, state storage incentives, and resilience grants support project viability. Digital transformation trends include AI-enabled building energy management systems, with over 40% of new systems integrating predictive dispatch software. A leading regional battery integrator expanded a 2 GWh domestic manufacturing facility in 2025 to serve commercial and industrial customers. Enterprise consumer behavior shows higher adoption among healthcare and finance facilities where uptime standards exceed 99.95%, making storage systems essential for operational continuity.

What role do decarbonization mandates play in accelerating behind-the-meter energy storage adoption?

Europe accounts for nearly 28% of the Commercial Solar Storage market, led by Germany, the UK, and France where commercial solar rooftops surpass 20 GW combined capacity. Sustainability frameworks require businesses to reduce operational emissions by over 30% before 2030, stimulating battery integration. Demand response participation and time-of-use pricing affect more than 50% of commercial consumers, increasing the value of storage assets. Emerging technologies include hybrid inverter architectures and grid-interactive smart meters. A regional power electronics manufacturer introduced modular commercial battery cabinets supporting 1 MWh scalable configurations in 2025. Consumer behavior reflects strong regulatory influence, with enterprises prioritizing energy transparency, carbon accounting, and compliance reporting alongside operational savings.

How is industrial electrification driving distributed storage expansion across high-growth economies?

Asia-Pacific holds roughly 26% of market volume and ranks as the fastest-expanding region. China, India, and Japan represent the top consuming countries, together accounting for over 70% of regional commercial solar installations. Manufacturing expansion, logistics infrastructure, and technology parks drive storage demand. Industrial rooftop solar additions exceed 10 GW annually in key economies, increasing the need for load balancing solutions. Regional innovation hubs focus on battery chemistry optimization and AI-integrated energy control platforms. A major regional battery producer commissioned a 3 GWh commercial storage production line to meet rising domestic demand. Consumer behavior trends show growth driven by energy security concerns and industrial load management priorities.

How are grid stability initiatives influencing commercial storage deployment patterns?

South America contributes about 7% of global installations, with Brazil and Argentina as leading adopters. Commercial solar additions above 3 GW annually in Brazil increase demand for battery-backed peak management. Energy sector reforms encourage distributed generation, while net billing policies stimulate storage integration. Infrastructure trends show rising deployment in agro-processing, mining support facilities, and commercial retail centers. A regional renewable energy developer launched a 500 kWh modular storage program serving mid-sized commercial clients. Consumer behavior reflects demand tied to power reliability gaps, with enterprises prioritizing backup capacity and cost stabilization in regions experiencing grid fluctuation challenges.

Why is commercial infrastructure modernization increasing demand for onsite energy storage?

Middle East & Africa represent nearly 5% of the Commercial Solar Storage Market, with growth concentrated in the UAE, Saudi Arabia, and South Africa. Demand is linked to commercial real estate, oil and gas support facilities, and hospitality infrastructure where energy reliability is essential. Solar deployment in commercial zones exceeds 2 GW annually across leading Gulf countries. Technological modernization includes smart grid pilots and AI-based facility energy management. A regional energy services firm deployed containerized 1 MWh storage systems across industrial free zones in 2025. Consumer behavior trends show preference for integrated solar-storage packages to ensure cooling load stability and reduce reliance on diesel backup systems.

United States Commercial Solar Storage Market – 29% share, supported by advanced distributed energy infrastructure and strong commercial resilience investments.

China Commercial Solar Storage Market – 24% share, driven by large-scale battery manufacturing capacity and rapid industrial solar deployment.

The Commercial Solar Storage market exhibits a moderately fragmented structure with over 45 active global and regional competitors participating across battery manufacturing, system integration, power electronics, and digital energy platforms. The top five companies collectively account for approximately 41% of total installed commercial storage capacity, reflecting a competitive yet innovation-driven landscape. Market leaders differentiate through vertically integrated supply chains, offering batteries, inverters, and software under unified platforms, reducing integration costs by nearly 15%.

Strategic initiatives include cross-sector partnerships between battery manufacturers and building energy management firms, with more than 30 notable collaborations formed during the past two years to enable AI-based optimization. Product innovation focuses on modular storage blocks ranging from 100 kWh to 2 MWh, now representing over 48% of new deployments. Mergers and acquisitions activity increased by about 18% year-over-year, primarily targeting software analytics and thermal management technologies. Competitive positioning also depends on warranty extensions beyond 10 years and performance guarantees exceeding 6,000 charge cycles. Digital differentiation is accelerating, with nearly 40% of vendors embedding predictive maintenance capabilities. Companies emphasizing fire safety engineering and compliance with updated building codes gain advantage in dense urban commercial markets where regulatory approval timelines influence procurement decisions.

Tesla

BYD

Sungrow

Schneider Electric

SolarEdge Technologies

LG Energy Solution

Fluence Energy

Enphase Energy

Eaton

Huawei Digital Power

Saft

Generac

Technology advancements are reshaping the Commercial Solar Storage market, with system performance and total cost of ownership increasingly defined by integrated hardware-software innovations. At the core, lithium-ion battery chemistries, particularly lithium iron phosphate (LFP), constitute roughly 60% of newly commissioned commercial systems due to high thermal stability and cycle life extending beyond 6,000 cycles in heavy duty use. Emerging solid-state battery research is advancing cell energy densities above 300 Wh/kg, potentially increasing usable storage capacity per cabinet by over 25% compared to current liquid electrolyte systems.

System architecture trends show a clear shift toward DC-coupled solar and storage configurations in nearly 45% of new commercial installations. These configurations reduce conversion steps, improving round-trip efficiency by up to 7 percentage points relative to AC-coupled equivalents. Modular battery units with standardized 250 kWh to 1 MWh blocks now constitute more than half of commercial deployments, enabling scalable energy storage that aligns with facility expansion plans and simplifies maintenance logistics.

Power conversion technology has also progressed, with bidirectional inverters capable of peak output variation control across broader voltage ranges. New inverter platforms support over 30% faster response times to grid frequency events, enhancing participation in demand response and grid support programs. The integration of AI-enabled energy management systems is now a commercial norm in nearly 40% of deployments, offering predictive load forecasting that reduces unnecessary cycling by approximately 12% and improves dispatch reliability for peak shaving and backup scenarios.

Thermal management systems are evolving with liquid cooling loops and phase-change materials integrated into rack designs to maintain optimal cell temperatures, reducing capacity fade rates by up to 15% under high load conditions. Safety instrumentation, including real-time cell monitoring networks across battery strings, has improved fault detection speeds by well over 20%, minimizing operational risk in dense urban facilities. These technological strides are enabling commercial operators to achieve higher uptime, improved lifecycle performance, and enhanced regulatory compliance, underscoring technology’s central role in strategic storage deployment decisions.

• In December 2024, SolarEdge expanded its commercial solar storage portfolio with the CSS-OD system tailored for indoor and outdoor commercial and industrial solar installations, featuring a 102.4 kWh battery and scalable inverter up to 1 MWh, enabling optimized self-consumption and peak shaving for business customers. (investors.solaredge.com)

• In early 2025, SolarEdge showcased its ‘ONE for C&I’ energy optimization platform and integrated solar-powered EV charging solutions for commercial customers at Intersolar 2025, enhancing real-time energy data analytics and tariff optimization for business energy managers. (corporate.solaredge.com)

• Throughout late 2025, SolarEdge completed first commercial battery installations of its CSS-OD system in Germany’s largest solar self-consumption market, with over 150 orders equating to more than 15 MWh of commercial storage capacity deployed across the country. (EveryTicker)

• In 2025, Enphase Energy launched its modular IQ Battery 5P with FlexPhase technology for single-phase and three-phase configurations, expanding its energy storage offerings to support higher load small commercial and mixed-use solar applications in new international markets. (Investing.com India)

The scope of the Commercial Solar Storage Market Report encompasses comprehensive analysis across product types, deployment applications, geographic regions, and end-user sectors relevant to commercial energy storage adoption. This includes segmentation by battery technology—such as lithium-ion architectures dominating mid-range commercial storage units between 100 kWh and 2 MWh—as well as emerging long-duration storage innovations and hybrid system configurations tailored to peak shaving, backup power, and microgrid integration. Geographic analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with regional insights into policy frameworks, incentive structures, and infrastructure investment trends shaping commercial procurement decisions.

The report further examines application areas ranging from demand charge management in high-consumption facilities to renewable self-consumption optimization and participation in ancillary service markets. Technology coverage includes bidirectional inverters, AI-enabled energy management software, and modular storage design trends that influence deployment speed, maintenance practices, and lifecycle performance. Industry focus also extends to verticals such as commercial real estate, manufacturing plants with critical uptime requirements, logistics centers with high load variability, and institutional campuses where resilience and sustainability metrics are prioritized. Comparative analysis of system configurations and energy software platforms offers decision-makers clarity on integration challenges, interoperability concerns, and long-term operational value. The report’s breadth includes emerging segments like integrated EV charging support and DC-coupled solar storage systems, addressing evolving energy strategies among commercial property owners and energy service providers. Targeted at strategic planners, investors, and industry professionals, the report synthesizes quantitative and qualitative insights to support technology evaluation, procurement planning, and competitive benchmarking within the commercial solar storage landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tesla, BYD, Sungrow, Schneider Electric, SolarEdge Technologies, LG Energy Solution, Fluence Energy, Enphase Energy, Eaton, Huawei Digital Power, Saft, Generac |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |