Reports

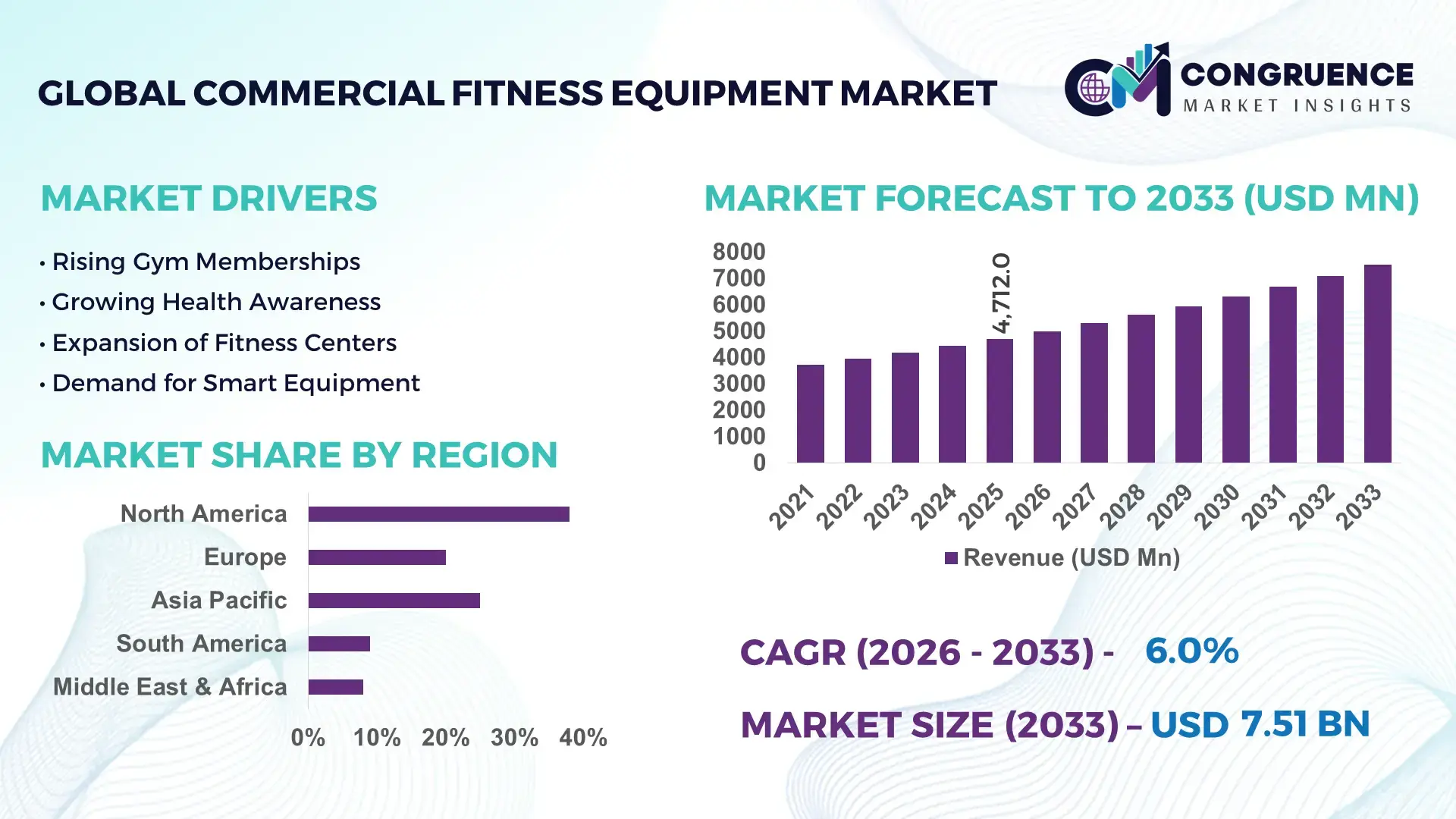

The Global Commercial Fitness Equipment Market was valued at USD 4712 Million in 2025 and is anticipated to reach a value of USD 7510.21 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033. Growth is being driven by accelerated gym chain expansion, AI-enabled connected fitness equipment deployment, corporate wellness investments, and rising refurbishment cycles across health clubs, hotels, and institutional fitness facilities.

The United States remains the dominant country, accounting for approximately 32% of global commercial fitness equipment installations in 2026, supported by large fitness franchise networks, corporate wellness programs, and connected equipment penetration exceeding 45% across premium facilities. In comparison, China represents nearly 22% of new equipment manufacturing capacity, backed by industrial investments and smart manufacturing initiatives. Ongoing supply-chain diversification following global trade realignments has increased regional sourcing activity, while digitally integrated strength and cardio equipment adoption has expanded by more than 18% year over year in major commercial facilities.

For market participants, prioritizing smart equipment portfolios, localized manufacturing strategies, and service-based recurring revenue models remains critical for sustaining competitive positioning and operational scalability.

Market Size & Growth: USD 4712 Million in 2025, reaching USD 7510.21 Million by 2033 at 6% CAGR, supported by connected fitness platforms and commercial facility modernization.

Top Growth Drivers: AI-enabled equipment adoption (+18%), fitness franchise expansion (+14%), and corporate wellness spending growth (+11%).

Short-Term Forecast: By 2028, predictive maintenance tools reduce equipment downtime by approximately 20% and improve asset utilization by 15%.

Emerging Technologies: AI coaching, IoT-connected machines, and advanced lightweight materials improve equipment efficiency by 12–18%.

Regional Leaders: North America exceeds USD 2.5 Billion, Asia-Pacific approaches USD 2.1 Billion, and Europe surpasses USD 1.7 Billion, driven by digital fitness integration.

Consumer/End-User Trends: More than 48% of premium commercial facilities deploy app-connected equipment for personalized training experiences.

Pilot/Case Example: In 2026, large fitness network upgrades improved member engagement by 22% and reduced maintenance costs by 16%.

Competitive Landscape: Top manufacturers collectively control approximately 38% market share, with strong positions across cardio, strength, and connected equipment segments.

Regulatory & ESG Impact: Energy-efficient equipment designs lower facility power consumption by 10–15% while supporting sustainability targets.

Investment & Funding: Industry investments exceed USD 1.2 Billion, focused on digital ecosystems, manufacturing expansion, and strategic partnerships amid supply-chain shifts.

Innovation & Future Outlook: AI-driven analytics, biometric integration, and subscription-based service models are reshaping long-term competitive strategies.

Commercial fitness equipment demand is increasingly concentrated in health clubs, boutique fitness studios, hospitality facilities, educational institutions, and corporate wellness centers. Recent innovation focuses on AI-powered coaching systems, cloud-connected equipment management, and integrated performance analytics. More than 40% of newly installed premium machines now feature digital connectivity. As operators seek greater equipment utilization and maintenance efficiency amid evolving procurement strategies, the market is transitioning toward data-driven fitness ecosystems, setting the stage for broader strategic evaluation.

Commercial fitness equipment is becoming a strategic investment category as operators compete through digital member engagement, equipment utilization efficiency, and data-driven facility management. The market is shifting beyond hardware sales toward connected fitness ecosystems that integrate analytics, maintenance monitoring, and personalized training. Supply-chain restructuring across manufacturing hubs in China, Vietnam, and Mexico is reducing procurement risk while enabling faster delivery cycles for large fitness chains, hospitality groups, and institutional buyers seeking scalable deployment models.

Technology differentiation is reshaping purchasing decisions. AI-enabled connected equipment can reduce maintenance-related downtime by nearly 20% and improve asset utilization by approximately 15% compared with legacy standalone systems. The United States leads in premium connected equipment deployment, with digital integration present in more than 45% of commercial facilities, while China maintains strong manufacturing scale and expanding smart-fitness production capabilities. A practical example is the deployment of predictive maintenance platforms across multi-location gym networks, allowing operators to optimize equipment availability and reduce service interventions.

Over the next two to three years, connected equipment penetration is expected to exceed 55% among newly equipped premium facilities, supported by strategic partnerships between manufacturers, software providers, and fitness operators. Companies are increasing investment in subscription-based services, digital platforms, and localized production networks. Organizations that combine equipment innovation, operational intelligence, and service-driven business models will secure stronger competitive positioning and long-term market relevance.

The primary growth driver is the rapid integration of connected fitness technologies across commercial facilities. More than 45% of premium fitness centers now utilize digitally connected equipment, while AI-enabled monitoring systems improve equipment utilization by approximately 15% and reduce maintenance downtime by nearly 20%. Corporate wellness participation has expanded by over 12% in major business hubs, increasing demand for advanced fitness installations. A notable industry shift involves equipment manufacturers integrating software platforms and performance analytics into traditional hardware offerings. This transition is creating recurring service opportunities and strengthening customer retention. Companies are responding through technology partnerships, digital ecosystem development, and expansion of smart equipment portfolios. A key strategic insight is that operators increasingly prioritize lifecycle performance data over upfront equipment cost, reshaping procurement and vendor selection criteria.

High acquisition costs and supply-chain dependencies continue to constrain market expansion, particularly among independent fitness operators. Connected commercial equipment typically carries acquisition costs 20–30% higher than conventional systems, while imported components account for nearly 40% of production inputs for several manufacturers. Logistics expenses remain elevated compared with pre-disruption levels, creating margin pressure across distribution networks. China-based component concentration continues to expose procurement cycles to trade policy changes and transportation bottlenecks. These constraints directly affect facility modernization timelines and return-on-investment calculations. Companies are mitigating risk through supplier diversification, regional assembly operations, and long-term procurement contracts. An important operational insight is that localization strategies are increasingly being pursued not only for cost control but also to improve inventory responsiveness and project delivery reliability.

A major opportunity lies in the transition from equipment sales to integrated digital fitness ecosystems. More than 50% of large fitness chains are evaluating connected platforms that combine performance analytics, remote management, and personalized training capabilities. Smart equipment deployments can improve member engagement metrics by 20% while reducing operational service requirements by approximately 15%. In countries such as India and Saudi Arabia, new wellness infrastructure investments are creating demand for advanced commercial installations. Emerging innovations including biometric integration, AI-based coaching engines, and cloud-managed fitness platforms are expanding value creation beyond physical equipment. Companies are increasing R&D spending, forming software alliances, and building subscription-driven ecosystems. A non-obvious strategic advantage is the ability to monetize operational data streams, creating additional revenue channels and stronger customer retention.

Long-term market expansion depends on successfully managing technology integration and operational complexity. More than 35% of commercial facilities operate mixed equipment environments, creating interoperability challenges between legacy machines and modern digital platforms. Connected systems can increase cybersecurity monitoring requirements by approximately 25%, while skilled technical workforce availability remains constrained in several deployment markets. As fitness operators expand multi-site networks, maintaining consistent software performance, data accuracy, and equipment connectivity becomes increasingly difficult. These challenges affect deployment scalability, customer experience consistency, and long-term competitiveness. Companies must invest in cybersecurity frameworks, workforce training programs, and standardized technology architectures. A critical strategic insight is that future competitive advantage will depend not only on equipment innovation but also on the ability to manage integrated digital infrastructure efficiently across distributed facility networks.

Connected Equipment Standardization Expands: Commercial operators are rapidly replacing isolated machines with integrated equipment ecosystems. Connected equipment deployment has exceeded 45% in premium facilities, while centralized monitoring reduces service response times by nearly 20% and improves asset utilization by 15%. Multi-site fitness chains in the United States are standardizing software platforms across locations to simplify maintenance workflows. Equipment suppliers are responding through software partnerships, cloud-enabled platforms, and bundled service contracts that increase operational visibility and reduce lifecycle management costs.

Strength Training Gains Priority: Strength-focused equipment installations have increased by approximately 18%, outpacing traditional cardio-focused procurement cycles. Operators report member retention improvements of nearly 12% in facilities expanding strength and functional training zones. Labor constraints affecting personal training availability are encouraging investments in guided digital strength systems. Manufacturers are scaling modular product lines and launching sensor-enabled resistance equipment to support higher utilization rates and more efficient floor-space allocation.

Localized Manufacturing Networks Accelerate: Supply-chain diversification remains a major operational trend as manufacturers reduce dependency on single-country sourcing models. Regional assembly strategies have shortened equipment lead times by nearly 15%, while inventory availability has improved by approximately 12%. Mexico, Vietnam, and India continue attracting production expansion initiatives. Companies are restructuring supplier networks, increasing component localization, and establishing strategic logistics partnerships to improve delivery consistency and reduce procurement disruptions.

Data Monetization Models Emerge: Fitness operators are increasingly treating equipment-generated data as a business asset rather than a maintenance tool. Facilities utilizing performance analytics report engagement increases exceeding 20% and programming efficiency gains of nearly 10%. A non-obvious shift is the use of aggregated equipment data to optimize membership offerings and staffing schedules. Equipment providers are expanding analytics capabilities, investing in AI-driven reporting tools, and forming ecosystem partnerships that transform operational intelligence into competitive differentiation.

Cardio Equipment remains the leading type segment due to its broad deployment across health clubs, hotels, corporate fitness centers, and institutional facilities. The segment accounts for an estimated 38% of commercial installations, supported by high utilization rates, digital connectivity integration, and established replacement cycles. Connected treadmills, ellipticals, and rowing systems continue benefiting from performance-tracking capabilities and centralized fleet management. Strength Equipment follows closely as operators rebalance floor space toward resistance-based training programs. Manufacturers are enhancing both categories through AI-enabled coaching functions, touchscreen interfaces, and predictive maintenance features that improve operational efficiency.

Functional Equipment represents the fastest-growing type segment, with deployment growth exceeding 16% as facilities prioritize flexible training environments and space optimization. Functional systems provide lower space requirements while supporting diverse workout formats, creating strong appeal for boutique operators. Cycling Equipment maintains relevance through immersive digital training experiences and group fitness integration, while Training Accessories benefit from relatively low capital requirements and frequent replacement cycles. Companies are directing investment toward modular equipment ecosystems, product innovation, and strategic partnerships to address evolving operator preferences and maximize facility utilization.

Cardio Equipment represents the leading application segment, driven by its central role in member onboarding, endurance training, and general fitness programs. Approximately 40% of equipment usage hours in large commercial facilities are linked to cardio-focused activities, reflecting broad accessibility across user demographics. Connected cardio platforms further strengthen demand by integrating performance tracking and personalized workout recommendations. Strength Equipment applications continue expanding as facilities respond to increasing demand for resistance training and performance-focused fitness programs. Operators are investing in digital coaching tools and analytics systems to improve engagement and optimize equipment utilization.

Functional Equipment applications are emerging as the fastest-growing area, supported by rising adoption of group training formats and hybrid fitness programming. Utilization rates for multifunctional training zones have increased by nearly 18% in newly renovated facilities. Cycling Equipment applications remain important within premium clubs emphasizing immersive experiences, while Training Accessories support rehabilitation, mobility, and supplemental conditioning programs. Companies are expanding deployment footprints, integrating digital monitoring technologies, and redesigning facility layouts to accommodate changing workout preferences and maximize operational efficiency.

Health Clubs remain the dominant end-user segment due to large-scale equipment deployment requirements, continuous replacement cycles, and high utilization intensity. This segment accounts for an estimated 45% of commercial equipment demand, supported by franchise expansion and premium facility modernization initiatives. Large operators increasingly deploy connected equipment platforms capable of reducing maintenance downtime by approximately 20%. Hotels represent a stable secondary buyer group, focusing on guest experience enhancement through compact, technology-enabled fitness installations. Equipment manufacturers continue prioritizing customization programs and service agreements tailored to high-volume operators.

Corporates are the fastest-growing end-user segment, with workplace wellness investments increasing by nearly 14% as organizations seek productivity and employee engagement benefits. Educational Institutions are expanding fitness infrastructure to support student wellness initiatives, while Hospitals increasingly incorporate specialized equipment into rehabilitation and preventive health programs. Sports Organizations remain important buyers of advanced performance-training systems requiring high durability and analytics integration. Companies are targeting these segments through flexible financing models, strategic partnerships, and ecosystem-based offerings that combine equipment, software, and service support into long-term customer relationships.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Connected Infrastructure Drives Premium Facility Upgrades

North America maintains the largest position in the commercial fitness equipment market, supported by extensive health club networks, corporate wellness deployments, and rapid adoption of connected fitness technologies. The region represents approximately 36% of global demand, with the United States accounting for the majority of commercial installations. More than 45% of premium facilities have integrated cloud-connected equipment and digital performance monitoring platforms. Strategic partnerships between equipment manufacturers and fitness operators continue accelerating equipment replacement cycles. Enterprise wellness investments and hotel fitness modernization programs are also strengthening demand. Operators increasingly prioritize predictive maintenance, centralized fleet management, and integrated member engagement technologies to improve facility performance and operational efficiency.

United States Market Outlook: The United States remains the primary demand center due to its large fitness club infrastructure, advanced technology adoption, and strong corporate wellness ecosystem. National fitness chains continue investing in connected strength and cardio platforms to improve member retention and operational visibility. More than 50% of newly commissioned premium fitness facilities now deploy integrated digital equipment ecosystems. Equipment suppliers are expanding software capabilities, service contracts, and data analytics offerings to strengthen long-term customer relationships and support large-scale enterprise deployments.

Sustainability and Facility Modernization Reshape Procurement

Europe represents a mature commercial fitness equipment market characterized by sustainability-focused procurement and facility modernization initiatives. The region accounts for approximately 28% of global installations, supported by strong health club penetration and increasing adoption of energy-efficient equipment systems. Operators are prioritizing low-energy machines, digital monitoring tools, and lifecycle management solutions. Equipment refurbishment programs have expanded by nearly 14% across major markets as operators seek cost-efficient modernization strategies. Fitness chains and hospitality providers continue investing in connected equipment deployments that improve utilization tracking and maintenance efficiency while aligning with environmental performance objectives.

Germany Market Outlook: Germany leads the European market through its strong commercial fitness infrastructure, manufacturing capabilities, and technology-focused deployment strategies. Large fitness operators increasingly adopt connected equipment platforms capable of supporting centralized performance monitoring across multiple facilities. Digital equipment penetration has expanded significantly among premium fitness chains, while wellness-focused corporate programs continue supporting procurement activity. Manufacturers benefit from established engineering expertise and strong enterprise demand for durable, technology-integrated equipment systems.

Manufacturing Scale and Smart Fitness Adoption Accelerate

Asia-Pacific is emerging as the fastest-expanding regional market due to large-scale fitness infrastructure development, rising commercial facility investments, and strong manufacturing capacity. The region contributes approximately 31% of global market activity and remains a major production hub for commercial fitness equipment. Smart equipment adoption has increased by nearly 18% annually in leading metropolitan markets. Fitness franchise expansion, wellness-oriented urban development, and increasing digital fitness integration continue strengthening demand. Manufacturers are expanding regional production facilities and supply networks to support growing domestic and export requirements while improving procurement responsiveness.

China Market Outlook: China combines manufacturing leadership with rapidly growing commercial fitness deployment activity. The country accounts for roughly 22% of global commercial fitness equipment production capacity and continues investing in smart manufacturing technologies. Large urban fitness operators increasingly deploy AI-enabled training systems and connected equipment platforms. Domestic manufacturers are strengthening international competitiveness through automation investments, product innovation, and supply-chain integration, creating advantages in production efficiency and large-volume equipment deployment.

Health Club Expansion Supports Market Development

South America continues to strengthen its position through expanding health club networks, rising wellness awareness, and increasing investment in urban fitness infrastructure. The region contributes approximately 6% of global demand and remains concentrated in major metropolitan centers. Commercial operators are modernizing facilities through digital equipment upgrades and flexible training environments. Equipment deployment across organized fitness chains has increased by nearly 12% over recent years. While infrastructure disparities and import dependencies remain operational constraints, growing franchise activity and premium facility development continue supporting long-term market expansion.

Brazil Market Outlook: Brazil serves as the largest commercial fitness equipment market in South America due to its extensive fitness club network and growing wellness economy. Major urban centers continue attracting investments in premium fitness facilities equipped with connected cardio and strength systems. Equipment modernization initiatives have increased significantly among large operators seeking improved member engagement and operational efficiency. Suppliers are expanding regional distribution networks and service capabilities to support growing deployment requirements and reduce equipment delivery timelines.

Wellness Infrastructure Investment Gains Momentum

The Middle East & Africa market is being shaped by large-scale wellness infrastructure projects, hospitality expansion, and government-supported health initiatives. The region accounts for approximately 5% of global demand but demonstrates strong deployment momentum in premium commercial facilities. New fitness and wellness developments integrated into mixed-use infrastructure projects are driving procurement activity. Commercial installations linked to hospitality and lifestyle developments have increased by nearly 15% in key markets. Operators are adopting connected equipment technologies to differentiate customer experiences and improve facility management efficiency.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant market due to substantial investments in wellness infrastructure, hospitality development, and lifestyle transformation programs. Fitness facility construction and modernization activity continue expanding across major cities, creating demand for advanced commercial equipment solutions. Connected equipment adoption is increasing rapidly within premium facilities, while international fitness brands are strengthening their local presence through partnerships and expansion strategies. These developments position the country as a leading deployment and investment hub within the region.

The commercial fitness equipment market is led by Life Fitness, Technogym, Precor, Matrix Fitness, and Johnson Health Tech, which collectively control approximately 42% of global market activity. Competition occurs between global technology-focused leaders and regional cost-competitive manufacturers, while connected-fitness innovators increasingly challenge traditional equipment suppliers. Technology integration, customization capabilities, and supply-chain responsiveness have become primary differentiators. AI-enabled equipment ecosystems improve operator utilization rates by nearly 15%, while predictive maintenance solutions reduce service downtime by approximately 20%. Premium brands compete through digital platforms, software subscriptions, and enterprise partnerships, whereas regional manufacturers emphasize cost efficiency and faster delivery cycles. Vertical integration strategies are expanding as companies seek greater control over components, software, and after-sales services. Consolidation and digital transformation continue shifting competitive dynamics toward ecosystem-based offerings. High capital requirements, service network expectations, and technology development costs remain significant entry barriers. Winning requires integrated hardware, software, analytics, and lifecycle service capabilities rather than equipment performance alone.

Life Fitness

Technogym

Johnson Health Tech

Matrix Fitness

Precor

Nautilus Commercial

Core Health & Fitness

TRUE Fitness

SportsArt

Torque Fitness

Cybex International

Shua Fitness

Impulse Health Tech

Panatta Sport International

Commercial fitness equipment technology is increasingly centered on connected ecosystems, IoT-enabled monitoring, and AI-driven performance analytics. In 2026, more than 45% of premium commercial facilities deploy connected cardio and strength equipment capable of tracking utilization, maintenance status, and user engagement. Predictive maintenance platforms reduce unplanned downtime by approximately 20%, while centralized equipment management improves asset utilization by nearly 15%. Operators benefit through lower service costs, improved equipment availability, and stronger member retention, making digital integration a core procurement requirement rather than an optional feature.

Emerging technologies include biometric tracking, AI coaching engines, and cloud-based fitness management platforms. Facilities implementing AI-assisted training systems report engagement improvements of 12–18%, while cloud-connected equipment networks reduce administrative workload by nearly 10%. Compared with legacy standalone machines, connected equipment ecosystems deliver approximately 25% greater operational visibility and faster maintenance response times. Large health club chains and hospitality operators are accelerating deployment through software partnerships and subscription-based service models that create recurring operational value beyond hardware ownership.

Disruptive innovation between 2026 and 2028 will focus on digital twins, adaptive resistance systems, and real-time performance optimization. Adoption of intelligent training platforms is expected to exceed 55% among newly equipped premium facilities. Technology leaders with integrated hardware, analytics, and software capabilities gain competitive advantages, while manufacturers relying solely on traditional equipment face increasing pressure from ecosystem-driven competitors.

February 2024 – Matrix Fitness launched the ultra-premium Onyx Collection featuring five commercial cardio machines including treadmills, cycles, and ClimbMill systems. The launch expanded its premium portfolio by 5 new products, strengthening positioning in luxury fitness facilities and high-end hospitality projects. Source: athleticbusiness.com

September 2025 – Technogym completed a wellness infrastructure partnership with Formula 1, equipping its Media & Technology Centre with connected fitness systems and activating a digital wellness platform for employees. The deployment supports 100% personalized training access, strengthening Technogym’s enterprise wellness footprint. Source: healthclubmanagement.co.uk

October 2025 – Peloton introduced the Peloton Pro Series, including its first commercial treadmill through its commercial business expansion strategy. The launch expanded Peloton’s commercial equipment portfolio with an integrated hardware-software ecosystem, enabling operators to deliver multi-modal training within a compact facility footprint. Source: onepeloton.com

May 2026 – Matrix Fitness expanded its Florida commercial operations by adding three senior industry professionals with nearly 70 years of combined experience. The expansion increased local market coverage capacity and strengthened customer support capabilities across commercial, hospitality, community, and multi-housing fitness segments. Source: athleticbusiness.com

This report provides comprehensive analysis of the commercial fitness equipment market across equipment categories, deployment environments, technology trends, and competitive positioning. The study evaluates Cardio Equipment, Strength Equipment, Functional Equipment, Cycling Equipment, and Training Accessories while assessing adoption patterns across Health Clubs, Hotels, Corporates, Educational Institutions, Hospitals, and Sports Organizations. The report examines deployment trends, equipment modernization strategies, connected fitness integration, and procurement priorities influencing industry development between 2026 and 2033. More than 45% of premium facilities now utilize connected equipment platforms, making technology adoption a central evaluation parameter.

The analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional deployment concentration, manufacturing activity, infrastructure investments, and enterprise adoption trends. Strategic insights include supply-chain restructuring, smart equipment deployment, predictive maintenance adoption, AI-enabled training technologies, and evolving operator business models. The report supports investment planning, expansion prioritization, partnership evaluation, competitive benchmarking, and technology roadmap development by identifying high-impact segments, emerging demand clusters, and operational shifts shaping future market direction.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 4712 Million |

|

Market Revenue in 2033 |

USD 7510.21 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Life Fitness, Technogym, Johnson Health Tech, Matrix Fitness, Precor, Nautilus Commercial, Core Health & Fitness, TRUE Fitness, SportsArt, Torque Fitness, Cybex International, Shua Fitness, Impulse Health Tech, Panatta Sport International |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |