Reports

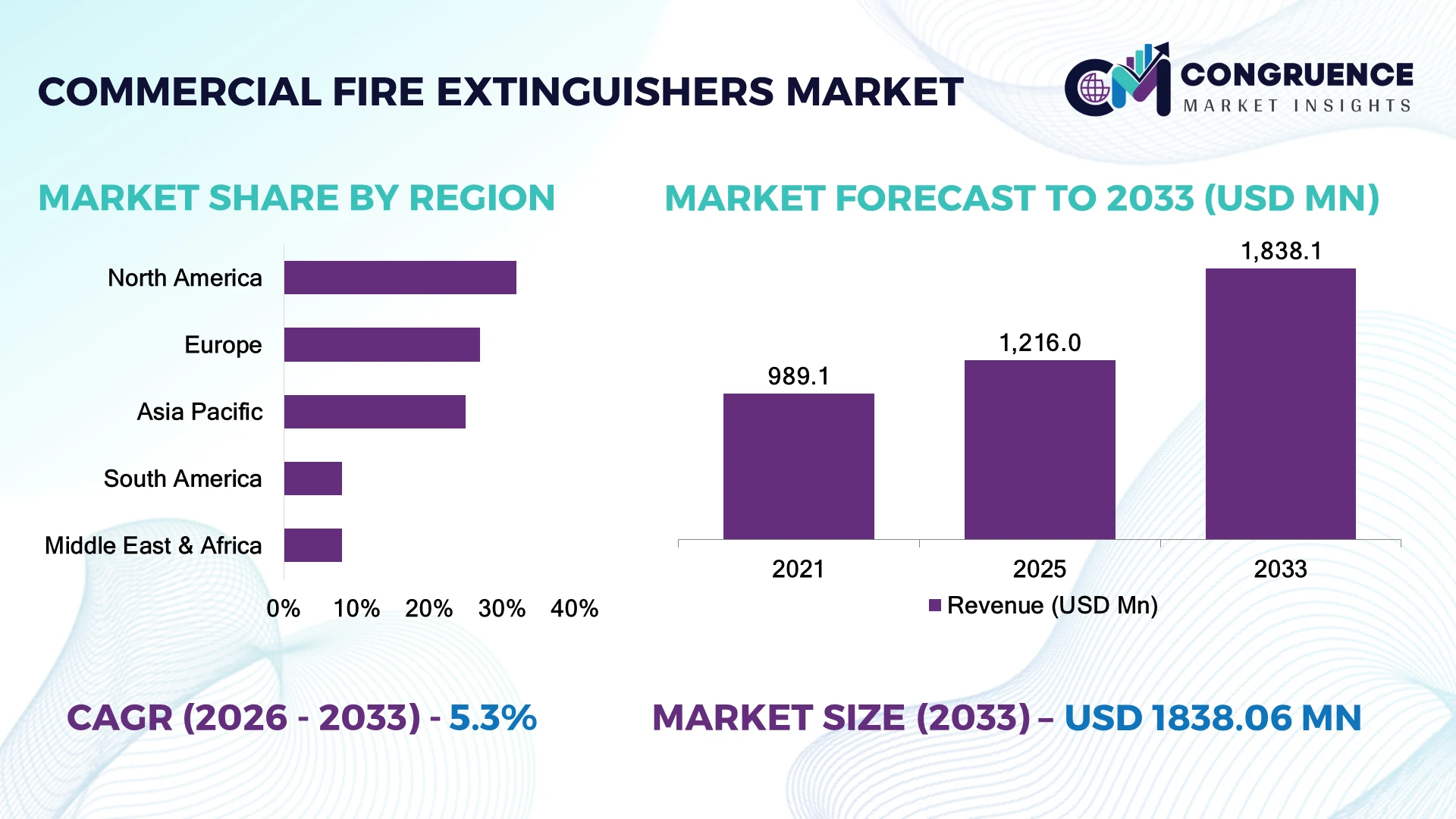

The Global Commercial Fire Extinguishers Market was valued at USD 1,216.0 Million in 2025 and is anticipated to reach a value of USD 1,838.1 Million by 2033 expanding at a CAGR of 5.3% between 2026 and 2033. Growth is driven by stricter fire safety enforcement, smart detection integration, replacement of aging suppression equipment, and rising installation across commercial buildings, industrial facilities, and data centers.

The United States dominates the market with nearly 30% share, supported by NFPA compliance upgrades, commercial infrastructure investments, and more than 40 million commercial buildings requiring safety systems. China follows with over 20% share, driven by industrial expansion and urban development programs. The U.S. records higher smart extinguisher adoption, while China leads manufacturing capacity with over 60% of global fire equipment production.

Strategic investments are shifting toward connected, automated, and regulation-ready fire protection solutions.

Market Size & Growth: USD 1.22 billion market in 2025 projected toward USD 1.84 billion by 2033, supported by stricter fire codes and smart safety upgrades.

Top Growth Drivers: Industrial safety compliance (35%), infrastructure modernization (30%), commercial automation adoption (25%).

Short-Term Forecast: By 2028, smart-enabled extinguishers improve inspection efficiency by 25% and reduce manual monitoring costs by 20%.

Emerging Technologies: AI-based monitoring, IoT-connected extinguishers, and advanced eco-friendly suppression materials are reshaping fire safety systems.

Regional Leaders: North America reaches USD 650 million with digital compliance adoption; Asia Pacific reaches USD 720 million through industrial expansion; Europe reaches USD 400 million via sustainability-focused upgrades.

Consumer/End-User Trends: Over 45% of commercial facility operators prioritize automated inspection and connected safety equipment.

Pilot/Case Example: 2024 smart fire safety deployments in large commercial facilities reduced inspection response time by 30%.

Competitive Landscape: Global leaders hold approximately 40% combined share, including Johnson Controls, Siemens, Honeywell, Amerex Corporation, and Minimax.

Regulatory & ESG Impact: Updated fire safety standards improve compliance rates by 20% while encouraging lower-toxicity extinguishing agents.

Investment & Funding: Over USD 5 billion invested globally in fire protection modernization, with partnerships expanding smart building safety networks.

Innovation & Future Outlook: Next-generation systems combine AI analytics, remote diagnostics, and sustainable agents, shifting competition toward intelligent fire prevention ecosystems.

Commercial fire extinguishers are increasingly deployed across offices, manufacturing plants, warehouses, hospitality facilities, and transportation hubs due to rising safety requirements and technology upgrades. Advanced products now integrate pressure monitoring, digital alerts, and environmentally safer agents, with connected systems improving maintenance accuracy by nearly 30%. Global regulatory tightening, including post-fire safety reforms in major economies, is accelerating adoption of smarter protection solutions and creating opportunities for manufacturers focused on automation and reliability.

The Commercial Fire Extinguishers Market is becoming strategically important as businesses prioritize operational resilience, regulatory compliance, and protection of high-value assets. Commercial infrastructure expansion, stricter workplace safety regulations, and modernization of aging fire protection networks are reshaping investment priorities across industries.

A major market shift is the transition from traditional manual inspection models toward connected fire safety ecosystems. IoT-enabled extinguishers with remote monitoring capabilities reduce inspection workloads by around 25% compared with conventional systems, while advanced suppression materials improve environmental performance and reduce maintenance requirements. Europe emphasizes sustainability-driven upgrades, whereas North America leads digital integration and Asia Pacific focuses on large-scale industrial deployment.

Over the next 2–3 years, adoption of smart monitoring platforms, automated compliance tracking, and integrated building management systems will accelerate. Large facilities, including warehouses and data centers, are deploying connected extinguishing solutions to minimize downtime and improve emergency response. Companies are expanding through technology partnerships, regional manufacturing investments, and product innovation strategies. Competitive advantage will increasingly depend on delivering intelligent, compliant, and scalable fire protection systems that support long-term infrastructure safety.

The adoption of connected fire protection systems is becoming a primary growth catalyst as commercial facilities upgrade from manual inspection models to intelligent monitoring platforms. Over 45% of large enterprises are prioritizing automated safety solutions, while IoT-enabled extinguishers improve inspection efficiency by nearly 25% and reduce response delays by around 30%. Regulatory enforcement in countries such as the United States and Germany is accelerating replacement cycles across offices, warehouses, and industrial sites. Companies are responding through investments in digital fire safety platforms, sensor integration, and strategic partnerships to deliver predictive maintenance capabilities and improve compliance performance.

High component costs, raw material volatility, and dependency on specialized manufacturing networks remain key limitations for commercial fire extinguisher deployment. Metal, valve assemblies, and environmentally compliant extinguishing agents account for significant production expenses, with equipment prices increasing by approximately 10–15% in recent supply cycles. Small and medium businesses in countries such as India and Brazil face affordability barriers due to limited safety budgets and uneven enforcement infrastructure. Manufacturers are reducing exposure through localized production, multi-year supplier agreements, and diversified sourcing strategies. The major operational challenge is maintaining competitive pricing while meeting stricter performance and environmental requirements.

The integration of AI analytics, remote monitoring, and smart building platforms creates significant opportunities for next-generation commercial fire extinguishers. Connected safety systems are gaining traction, with digital monitoring adoption increasing by more than 30% across advanced commercial facilities. Countries such as Japan and South Korea are expanding automated building safety infrastructure, creating demand for intelligent extinguishing solutions. Manufacturers are developing cloud-based inspection tools, subscription-based maintenance models, and integrated safety ecosystems to capture recurring revenue opportunities. A key strategic opportunity lies in combining extinguishers with broader building management platforms, enabling predictive risk detection and reducing operational downtime.

The transition toward intelligent fire protection systems introduces execution challenges related to interoperability, cybersecurity, and workforce readiness. Nearly 35% of commercial facilities operate mixed-age safety infrastructure, creating integration barriers for connected extinguisher technologies. Data protection requirements are becoming more stringent in countries such as the United States and European markets, increasing compliance complexity for digital safety providers. Companies must address installation consistency, technician training gaps, and compatibility issues across diverse building systems. Leading manufacturers are investing in cybersecurity frameworks, technical training programs, and standardized communication protocols to ensure reliable deployment and maintain long-term competitiveness.

Smart Monitoring Integration Growth: Commercial facilities are rapidly adopting IoT-enabled extinguishers and remote inspection platforms, with connected safety deployments increasing by nearly 30% and inspection automation improving workflow efficiency by 25%. Large enterprises in the United States and Japan are integrating fire systems with building management platforms, prompting manufacturers to expand sensor-based product portfolios and cloud monitoring partnerships.

Eco-Friendly Agent Transition: Environmental regulations are accelerating the replacement of traditional suppression chemicals, with more than 35% of new commercial installations shifting toward lower-impact extinguishing agents. European compliance initiatives and sustainability targets are influencing procurement decisions, while manufacturers are restructuring supply chains to increase production of recyclable cylinders and advanced chemical formulations.

Automated Compliance Expansion: Digital compliance tracking is transforming safety audits, reducing documentation workload by approximately 20% and improving inspection accuracy by over 30% in large commercial properties. Following stricter workplace safety enforcement in countries such as the United States, companies are investing in automated reporting tools and maintenance management systems.

Enterprise Safety Platform Convergence: Fire extinguishers are increasingly becoming part of integrated risk management ecosystems, with around 40% of newly designed smart buildings connecting safety equipment with centralized platforms. Companies are forming technology partnerships to combine fire protection, analytics, and emergency response systems, creating a shift from standalone equipment toward predictive safety operations.

Portable fire extinguishers represent the leading type segment, accounting for approximately 55% of commercial deployments due to their affordability, regulatory acceptance, and suitability across offices, retail facilities, and industrial locations. Their easy installation and replacement cycles support widespread adoption, particularly among small and medium enterprises. Wheeled extinguishers hold around 20% share and remain important for heavy-duty industrial environments requiring higher discharge capacity. Automatic and smart-enabled extinguishing systems are the fastest-growing category, expanding as enterprises adopt connected safety infrastructure and automated response technologies. This segment is gaining momentum with adoption rates rising by nearly 35% in advanced commercial buildings. Companies are increasing investment in sensor integration, remote monitoring capabilities, and hybrid protection solutions. Emerging smart systems are reshaping purchasing decisions by shifting focus from basic compliance toward operational intelligence and predictive maintenance.

Industrial facilities represent the leading application segment, contributing approximately 45% of commercial fire extinguisher demand due to high-risk operations, machinery exposure, and strict workplace safety requirements. Manufacturing hubs in the United States, China, and Germany continue upgrading fire protection infrastructure as automation increases operational complexity. Commercial offices and retail spaces collectively account for nearly 35% of demand, supported by compliance-driven installations and employee safety requirements. Data centers and specialized facilities are emerging as the fastest-growing application areas, with adoption increasing by around 30% as businesses prioritize protection of high-value digital infrastructure. Rising cloud computing capacity and stricter uptime requirements are accelerating deployment of advanced extinguishing systems. Companies are adapting through customized solutions, integrated monitoring platforms, and partnerships with facility management providers to address evolving operational risks.

Commercial enterprises are the dominant end-user segment, representing nearly 50% of market demand due to extensive deployment across offices, retail chains, hospitality properties, and mixed-use buildings. Large organizations prioritize standardized fire safety systems across multiple locations, driving bulk procurement and long-term maintenance agreements. Industrial operators account for approximately 30% share, supported by manufacturing expansion and stricter occupational safety requirements. Data centers and infrastructure operators are the fastest-growing end-user group, with adoption rising by nearly 35% as digital assets become increasingly critical to business continuity. These users demand advanced monitoring, rapid response capabilities, and integration with facility automation systems. Manufacturers are targeting this segment through specialized product development, technology partnerships, and lifecycle service models. Smaller enterprises are increasingly adopting modular solutions due to improved affordability and simplified compliance management.

North America accounted for the largest market share at 32% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America holds the leading position in the commercial fire extinguishers market, supported by strict workplace safety regulations, advanced building infrastructure, and high replacement activity across commercial facilities. The region contributes approximately 32% of global demand, with the United States representing the largest deployment base across offices, industrial plants, healthcare facilities, and data centers. More than 50% of large commercial buildings are integrating digital inspection and monitoring tools to improve compliance efficiency. Manufacturers are expanding connected product portfolios, partnering with building automation providers, and investing in advanced suppression technologies to support automated safety management.

United States Market Outlook: The United States remains the regional powerhouse due to strong NFPA-driven compliance requirements and extensive commercial infrastructure. Over 40 million commercial buildings require fire safety equipment upgrades and periodic replacements. Growing data center construction, industrial automation, and smart building investments are increasing demand for intelligent extinguishing solutions with remote monitoring capabilities.

Europe maintains a strong market position due to stringent fire safety standards, sustainability initiatives, and modernization of aging commercial infrastructure. Countries including Germany, France, and the United Kingdom are accelerating adoption of environmentally responsible extinguishing agents and digitally managed safety systems. The region represents nearly 27% of global demand, with industrial facilities and commercial complexes accounting for major deployments. More than 35% of new installations incorporate lower-impact suppression materials aligned with environmental regulations. Companies are strengthening regional manufacturing networks, developing recyclable equipment designs, and forming partnerships with facility management firms to address compliance and sustainability requirements.

Germany Market Outlook: Germany leads European adoption through its advanced industrial base, engineering capabilities, and emphasis on workplace safety standards. The country’s manufacturing sector represents a significant demand center, with more than 30% of industrial facilities upgrading fire protection systems through automation and digital monitoring technologies. Strong automotive, chemical, and machinery industries continue supporting specialized extinguisher deployments.

Asia-Pacific is the fastest-expanding market, driven by manufacturing growth, urban infrastructure development, and increasing commercial construction activity. The region contributes approximately 25% of global demand while accounting for more than 60% of fire equipment manufacturing capacity, led by China. Industrial parks, logistics hubs, and high-rise commercial developments are creating large-scale deployment opportunities. China, India, and South Korea are increasing investments in automated safety systems, with smart fire monitoring adoption rising by nearly 30% in advanced facilities. Companies are expanding production capacity, establishing local partnerships, and optimizing supply chains to meet growing demand from industrial and commercial users.

China Market Outlook: China dominates regional production and commercial deployment due to its extensive manufacturing ecosystem and infrastructure expansion programs. The country supplies over 60% of global fire equipment output and continues upgrading industrial safety systems across factories, warehouses, and commercial complexes. Government-led urban modernization initiatives are supporting adoption of advanced fire protection technologies.

South America is experiencing steady demand growth as commercial infrastructure upgrades and industrial safety improvements accelerate across major economies. Brazil and Argentina represent key demand centers, supported by manufacturing, mining, logistics, and commercial construction activities. The region contributes around 8% of global demand, with industrial facilities accounting for a significant portion of installations. Safety modernization programs are increasing replacement activity, while approximately 25% of large enterprises are adopting improved inspection and maintenance systems. Companies are addressing market limitations through local distribution partnerships, regional service networks, and cost-efficient product offerings tailored to emerging commercial users.

Brazil Market Outlook: Brazil represents the largest market in South America due to its industrial scale, commercial infrastructure base, and mining operations. The country’s manufacturing and logistics sectors drive significant extinguisher demand, with more than 20% of large industrial facilities undergoing safety equipment modernization programs. Local partnerships are becoming essential for improving distribution efficiency and maintenance coverage.

The Middle East & Africa market is being shaped by large-scale infrastructure projects, hospitality expansion, energy investments, and commercial property development. The region contributes approximately 8% of global demand, with the Gulf countries representing major adoption centers due to advanced construction activity and safety regulations. Saudi Arabia and the United Arab Emirates are increasing investments in smart buildings, airports, and industrial zones, where automated fire protection systems are becoming standard requirements. More than 30% of newly developed commercial projects incorporate advanced monitoring solutions. Companies are expanding through regional partnerships, project-based contracts, and localized service capabilities.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the key regional market due to large infrastructure programs, industrial diversification, and commercial construction growth. Projects linked to Vision 2030 are increasing demand for advanced fire safety systems across airports, hotels, industrial zones, and mixed-use developments. Over 25% of major new facilities are integrating modern fire protection technologies during initial construction phases.

The Commercial Fire Extinguishers Market features competition between global safety technology leaders, regional manufacturers, and specialized fire protection suppliers. Major players such as Johnson Controls, Siemens, Honeywell, and Minimax compete with cost-focused manufacturers and customized solution providers. The top five companies collectively account for approximately 40% of market share, creating a moderately consolidated structure. Competition is driven by smart monitoring capabilities, product reliability, pricing efficiency, and service networks, with technology-focused players gaining advantage through connected solutions adopted in over 30% of advanced facilities. Companies are expanding through acquisitions, regional manufacturing, digital partnerships, and integrated building safety platforms. The market is shifting from traditional equipment supply toward intelligent fire management ecosystems, increasing pressure on low-cost manufacturers. High certification requirements, compliance expertise, and distribution infrastructure remain key entry barriers. Winning players will require scalable technology, strong service capabilities, and localized solutions.

Honeywell

Siemens

Minimax

Amerex Corporation

Kidde

UTC Fire & Security

NAFFCO

Safex Fire Services

BAVARIA Brandschutz Industrie

Desautel

FlameStop Australia

Smart monitoring technologies are transforming commercial fire extinguishers by integrating IoT sensors, cloud platforms, and real-time diagnostics. Connected extinguishers improve inspection efficiency by nearly 25% compared with manual systems and are being deployed in more than 30% of newly developed smart commercial facilities. Companies benefit through predictive maintenance, reduced downtime, and improved compliance visibility.

Artificial intelligence, automated inspection tools, and advanced suppression materials represent emerging technology shifts. AI-enabled safety platforms improve fault detection accuracy by approximately 30%, while environmentally safer extinguishing agents reduce maintenance complexity by around 15%. Compared with traditional manual equipment, intelligent systems deliver faster monitoring response and operational efficiency improvements exceeding 20%, creating advantages for technology-focused manufacturers.

Between 2026 and 2028, integration with building management systems, digital compliance platforms, and remote service networks will become a competitive requirement. Global leaders and specialized technology providers are positioned to benefit through partnerships and ecosystem development, while conventional equipment suppliers face pressure to modernize product portfolios and service models.

June 2025 Johnson Controls relaunched its Connected Sprinkler service, expanding digital fire protection capabilities with real-time insights and predictive maintenance features. The solution supports data-driven facility management by reducing reactive maintenance needs and improving lifecycle efficiency across commercial buildings. Source: www.johnsoncontrols.com

July 2025 Honeywell acquired Li-ion Tamer from Nexceris to strengthen its fire life safety portfolio, adding early thermal runaway detection technology for lithium-ion battery applications. The acquisition expanded Honeywell’s capabilities for energy storage and data center safety markets through technology integration and portfolio expansion. Source: www.honeywell.com

July 2025 Honeywell was selected to upgrade the fire alarm system at Phoenix Sky Harbor International Airport Terminal 4. The project involves replacing thousands of devices with modern automated systems across a terminal serving more than 80 airline gates, improving emergency response visibility and operational management. Source: www.honeywell.com

March 2026 Siemens introduced its Sinteso Nova and Cerberus Nova fire detector portfolio, integrating cloud connectivity, IoT capabilities, remote diagnostics, and predictive maintenance functions. The launch supports healthcare, education, data center, and commercial real estate applications by enabling continuous system monitoring and smarter safety operations.

The Commercial Fire Extinguishers Market Report provides comprehensive coverage of market segmentation by type, application, and end-user, including portable systems, wheeled units, smart extinguishing technologies, industrial facilities, commercial buildings, data centers, and infrastructure operators. The study analyzes major markets across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with focus on deployment patterns, regulatory influences, and technology adoption.

The report evaluates competitive positioning, product innovation, supply-chain strategies, digital transformation, and emerging opportunities in intelligent fire protection systems. It highlights adoption trends such as connected monitoring, sustainable extinguishing agents, and automated compliance solutions. The analysis supports investment decisions, expansion planning, partnership evaluation, and competitive strategy development from 2026 onward.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,216.0 Million |

| Market Revenue (2033) | USD 1,838.1 Million |

| CAGR (2026–2033) | 5.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Johnson Controls; Honeywell; Siemens; Minimax; Amerex Corporation; Kidde; UTC Fire & Security; NAFFCO; Safex Fire Services; BAVARIA Brandschutz Industrie; Desautel; FlameStop Australia |

| Customization & Pricing | Available on Request (10% Customization Free) |