Reports

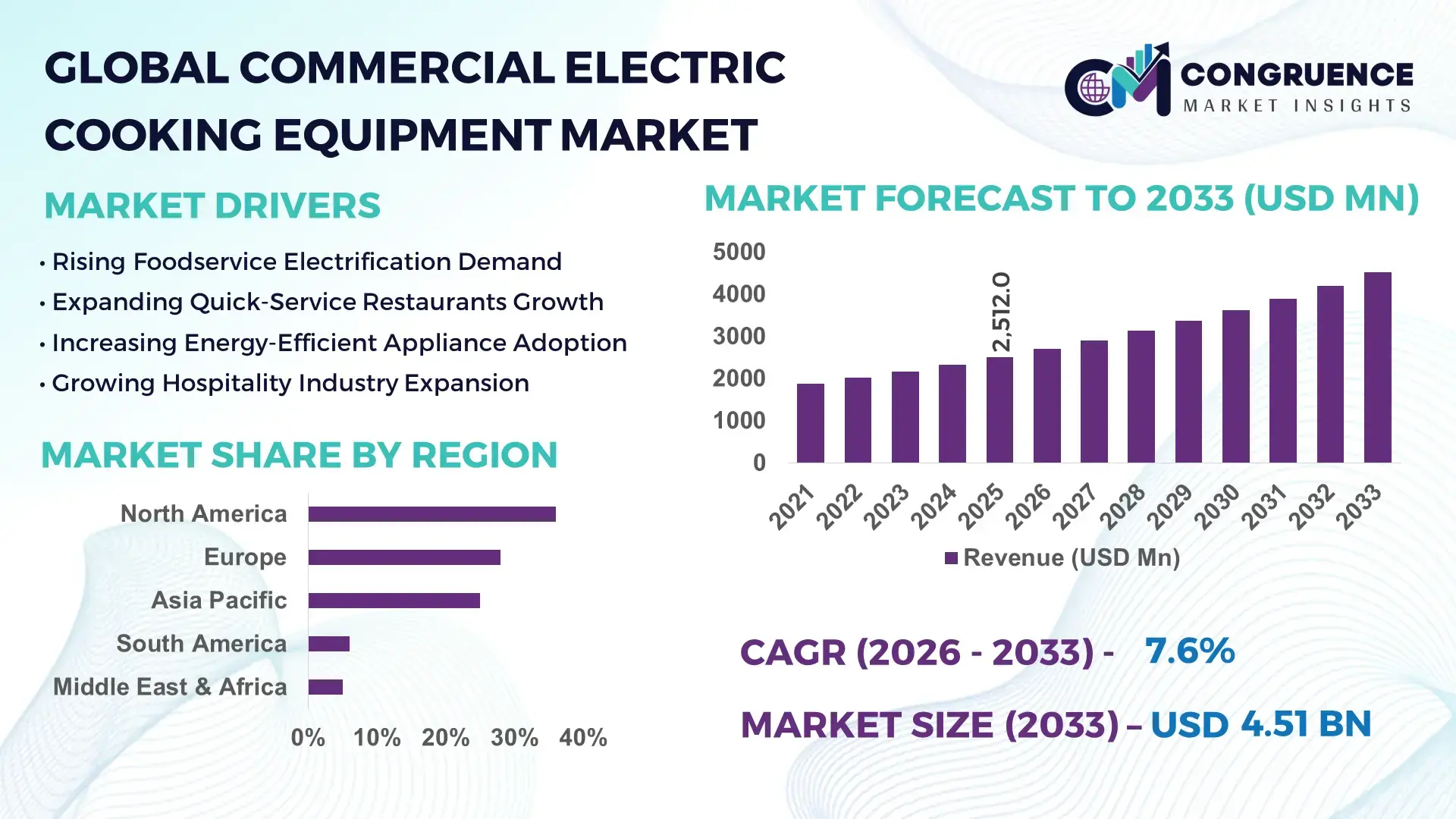

The Global Commercial Electric Cooking Equipment Market was valued at USD 2,512.0 Million in 2025 and is anticipated to reach a value of USD 4,513.5 Million by 2033 expanding at a CAGR of 7.6% between 2026 and 2033. The market is being propelled by the rapid transition toward energy-efficient induction cooking systems, smart kitchen automation, and electrification initiatives across restaurants, hotels, institutional kitchens, and quick-service restaurant chains seeking lower operating costs and improved food preparation consistency. Growing deployment of connected cooking platforms capable of real-time monitoring has increased kitchen productivity by over 20% while reducing energy consumption by nearly 15% compared to conventional cooking environments. Between 2024 and 2026, tightening energy-efficiency regulations, rising labor costs, and supply chain restructuring across foodservice equipment manufacturing hubs have accelerated investment in advanced electric cooking infrastructure. The ongoing geopolitical focus on energy security following disruptions in global fuel markets has further encouraged commercial operators to reduce dependence on gas-based cooking systems.

The United States remains the dominant country, accounting for approximately 31% of global market demand due to its extensive foodservice ecosystem, with more than 1 million restaurant establishments and large-scale adoption of smart commercial kitchens. Over USD 2.5 billion has been invested in commercial kitchen modernization projects across hospitality and institutional sectors over the last three years. Induction cooking penetration in newly installed commercial kitchens exceeds 35%, compared with less than 20% in several emerging markets. Strong adoption among quick-service restaurants, healthcare facilities, and educational institutions continues to reinforce the country's leadership in advanced electric cooking equipment deployment and operational innovation.

As commercial foodservice operators prioritize efficiency, electrification, and digital kitchen management, companies capable of delivering integrated, high-performance cooking solutions are positioned to secure long-term competitive advantage across global markets.

Market Size & Growth: USD 2,512.0 million in 2025 rising to USD 4,513.5 million by 2033, supported by smart kitchen adoption and electrification initiatives across foodservice operations.

Top Growth Drivers: Energy savings up to 15%, labor productivity gains above 20%, and induction cooking adoption exceeding 35% in modern commercial kitchens.

Short-Term Forecast: By 2028, kitchen energy consumption is projected to decline by 12% while cooking efficiency improves by nearly 18%.

Emerging Technologies: AI-enabled monitoring, IoT-connected appliances, and advanced induction systems are reducing downtime by over 25%.

Regional Leaders: North America USD 1.45 billion, Europe USD 1.12 billion, and Asia-Pacific USD 1.05 billion supported by digital kitchen transformation trends.

Consumer/End-User Trends: More than 42% of large foodservice operators are prioritizing electric cooking equipment upgrades over gas-based replacements.

Pilot/Case Example: In 2025, a multinational restaurant chain improved kitchen throughput by 22% and reduced energy use by 14% through induction deployment.

Competitive Landscape: Leading manufacturers collectively control approximately 38% market share, led by Welbilt, Electrolux Professional, Ali Group, Middleby, and Rational.

Regulatory & ESG Impact: Energy-efficiency standards are helping operators lower utility costs by 10–15% while strengthening sustainability compliance.

Investment & Funding: More than USD 1.8 billion has been directed toward kitchen modernization, manufacturing expansion, and strategic partnerships since 2024.

Innovation & Future Outlook: Autonomous cooking systems, predictive maintenance, and cloud-connected kitchens are redefining next-generation foodservice operations.

Commercial electric cooking equipment demand is concentrated within quick-service restaurants, full-service restaurants, hospitality facilities, healthcare institutions, and educational campuses, which collectively contribute nearly 70% of equipment deployment activity. Advanced induction technologies now represent over 35% of newly installed cooking systems, while smart connectivity features have expanded by approximately 28% across premium commercial kitchens. Demand growth remains strongest across Asia-Pacific and North America as operators respond to labor constraints, energy-efficiency targets, and supply chain optimization initiatives. Increasing integration of AI-enabled monitoring and predictive maintenance capabilities is reshaping procurement priorities, setting the stage for deeper strategic transformation and competitive differentiation.

Commercial electric cooking equipment has become a critical battleground for foodservice competitiveness as operators seek to simultaneously reduce operating expenses, improve kitchen productivity, strengthen sustainability performance, and address workforce shortages. The market is no longer centered solely on cooking hardware; it is increasingly transforming into a technology-driven ecosystem where automation, connectivity, energy management, and operational intelligence determine competitive success.

A significant industry shift is accelerating due to rising energy-efficiency regulations, labor constraints, and the restructuring of global foodservice supply chains. Commercial operators are optimizing kitchen layouts and replacing aging gas infrastructure with digitally connected electric cooking systems capable of delivering measurable operational gains. Modern induction cooking technology improves efficiency by 30% while reducing energy costs by 20% compared to legacy gas-based cooking systems. This performance advantage is reshaping capital allocation decisions among restaurant chains, institutional kitchens, and hospitality groups seeking long-term operating leverage.

North America leads in deployment volume, while Europe leads in sustainability-driven adoption and innovation with more than 40% of newly specified commercial kitchen projects incorporating advanced electric cooking technologies. Within the next two to three years, connected kitchen platforms are expected to reduce unplanned equipment downtime by approximately 25% while improving kitchen productivity by nearly 18%. ESG performance is emerging as a competitive advantage, enabling operators to lower energy consumption by up to 15%, strengthen regulatory compliance, and improve access to environmentally focused procurement programs. A notable example involves a multi-location hospitality operator that upgraded to smart induction systems and achieved a 22% improvement in kitchen throughput alongside a 14% reduction in utility consumption.

Manufacturers are shifting investment toward software-enabled equipment, predictive maintenance platforms, and regional manufacturing expansion strategies to capture high-growth opportunities. The organizations that integrate automation, electrification, and intelligent kitchen management fastest will secure stronger margins, operational resilience, and long-term market leadership as the industry continues accelerating toward digitally optimized foodservice environments.

The Commercial Electric Cooking Equipment Market is undergoing a significant transformation driven by electrification trends, operational efficiency requirements, and the modernization of commercial foodservice infrastructure. Restaurants, hotels, institutional kitchens, healthcare facilities, and catering operations are increasingly replacing conventional cooking systems with advanced electric alternatives capable of delivering greater precision, consistency, and energy performance. Growing labor shortages across foodservice operations are accelerating investments in automated cooking platforms and connected equipment ecosystems. At the same time, rising electricity grid modernization efforts and stricter sustainability requirements are influencing procurement decisions worldwide. Manufacturers are responding by expanding smart equipment portfolios, enhancing connectivity capabilities, and developing modular cooking platforms designed for scalability. Competitive dynamics are increasingly shaped by technological differentiation, energy optimization, and service-based business models, making innovation a critical factor for long-term market positioning.

Commercial kitchen electrification is emerging as the primary growth engine reshaping equipment procurement and operational strategies. Energy-efficient induction cooking systems can improve thermal efficiency by more than 30%, while reducing cooking-related energy consumption by approximately 15%. Simultaneously, connected cooking equipment has demonstrated productivity improvements exceeding 20% in high-volume foodservice environments. The global restructuring of energy markets following geopolitical fuel supply disruptions has further accelerated the shift away from gas-dependent operations. This cause-and-effect dynamic is driving restaurant chains, institutional kitchens, and hospitality operators to modernize kitchen infrastructure. In response, manufacturers are accelerating production capacity, expanding regional distribution networks, and investing heavily in smart cooking technologies. Strategic partnerships between equipment suppliers and foodservice operators are increasing as organizations seek faster deployment of advanced cooking ecosystems capable of supporting operational consistency, sustainability objectives, and long-term cost optimization.

Despite strong momentum, high capital expenditure requirements remain a structural constraint for many operators. Advanced induction and connected cooking systems typically carry acquisition costs that are 20–35% higher than conventional alternatives. In addition, key electronic components account for nearly 25% of total equipment manufacturing costs, exposing suppliers to semiconductor and component supply volatility. Infrastructure limitations represent another challenge, particularly in regions where commercial facilities require electrical upgrades exceeding 15% of existing power capacity. These factors can delay procurement cycles and extend return-on-investment timelines. To mitigate these risks, manufacturers are diversifying supplier networks, implementing long-term sourcing agreements, and introducing modular product architectures that reduce installation complexity. Leasing programs and equipment-as-a-service models are also emerging as practical solutions to overcome adoption barriers while preserving capital flexibility for foodservice operators.

The strongest opportunities are developing at the intersection of automation, connectivity, and predictive analytics. Smart kitchen systems have demonstrated equipment downtime reductions approaching 25%, while predictive maintenance capabilities can lower maintenance expenses by nearly 18%. AI-enabled cooking optimization platforms are improving food consistency metrics by more than 20% across high-volume operations. A particularly important future signal is the expansion of cloud-connected kitchen ecosystems that enable centralized monitoring of multi-location foodservice networks. Beyond traditional efficiency gains, these technologies unlock new business value through operational visibility, workforce optimization, and performance benchmarking. Companies are aggressively investing in software platforms, research initiatives, and integrated equipment ecosystems to establish competitive differentiation. Organizations building comprehensive technology-enabled cooking environments today are positioning themselves to capture disproportionate value as digital kitchen adoption accelerates globally.

Scaling advanced commercial electric cooking infrastructure presents significant execution challenges. Electrical infrastructure upgrades can increase project costs by 10–20% in older facilities, while skilled technician shortages have extended installation timelines by approximately 15% in several developed markets. Grid capacity limitations in certain urban regions also create operational constraints for high-power commercial kitchen deployments. These challenges directly impact scalability, deployment speed, and long-term operational consistency. The tension between rapid modernization and infrastructure readiness is becoming increasingly pronounced as adoption accelerates. Companies must therefore invest in equipment efficiency improvements, strategic utility partnerships, and workforce development initiatives to maintain momentum. Manufacturers that successfully address installation complexity, interoperability requirements, and infrastructure compatibility will be better positioned to sustain market leadership and support large-scale industry transformation.

Smart Kitchen Adoption Up 28% Across Large Foodservice Operations – Connected cooking equipment deployments have increased by 28%, while remote monitoring usage has expanded by 24%. Operators are integrating real-time performance dashboards to optimize workflow visibility and reduce equipment downtime by nearly 18%. Manufacturers are responding through cloud-enabled platforms and subscription-based service models, reshaping how commercial kitchens are managed and maintained.

Induction Cooking Installations Surpass 35% of New Commercial Kitchen Projects – New induction-based installations now exceed 35% of major kitchen renovation projects, while cooking efficiency improvements of 30% and energy savings approaching 15% are being consistently reported. Rising energy-security concerns and sustainability requirements are forcing operators to accelerate electrification strategies and reduce dependence on legacy fuel-based systems.

Labor Optimization Programs Reduce Kitchen Task Dependency by 20% – Automated cooking workflows have reduced manual intervention requirements by approximately 20%, while smart scheduling tools have improved labor utilization by nearly 16%. Foodservice operators are increasingly deploying semi-autonomous cooking systems to address workforce shortages and maintain service consistency. Equipment providers are expanding automation-focused product portfolios to capture this operational shift.

Regional Manufacturing Expansion Increasing Supply Resilience by 22% – Equipment manufacturers are restructuring production networks, increasing regional sourcing levels by roughly 22% to reduce supply-chain exposure. Component localization strategies have shortened lead times by nearly 12% while improving inventory responsiveness. This non-obvious shift is redefining competitive positioning as supply reliability becomes as important as product performance in procurement decisions.

The Commercial Electric Cooking Equipment Market is segmented across types, applications, and end-user categories, reflecting the operational diversity of the global foodservice industry. Demand remains concentrated in high-throughput cooking environments where energy efficiency, precision control, and labor optimization directly influence profitability. Electric ovens, induction cooktops, fryers, and specialized cooking systems collectively account for a substantial share of equipment deployment across commercial kitchens. Approximately 48% of procurement activity originates from restaurant-led operations, while institutional facilities and hospitality establishments contribute significantly to long-term equipment replacement cycles. Demand is increasingly shifting toward connected and energy-efficient solutions as operators seek to reduce utility consumption by 10–15% while improving kitchen productivity. Manufacturers are aligning product development strategies around automation, smart monitoring, and modular equipment platforms, making segment-specific positioning critical for capturing future growth opportunities.

Electric ovens dominate the Commercial Electric Cooking Equipment Market with an estimated 34% share, supported by their versatility, scalability, and widespread deployment across restaurants, hotels, and institutional kitchens. Their ability to support multiple cooking applications while maintaining consistent output makes them the preferred choice for high-volume operations. Induction cooktops represent the fastest-growing segment, recording adoption growth of approximately 11%, driven by superior energy efficiency, precise temperature control, and increasing electrification initiatives. Compared with traditional electric ranges, induction systems improve thermal efficiency by more than 30%, making them increasingly attractive for operators focused on reducing operational costs. Electric fryers, griddles, steamers, and specialty cooking systems collectively account for nearly 42% of market demand, serving niche requirements across quick-service restaurants, catering services, and institutional food preparation facilities. Demand is steadily shifting toward multifunctional equipment capable of integrating with smart kitchen ecosystems and predictive maintenance platforms. Manufacturers are expanding investments in connected cooking technologies, induction-based systems, and modular product designs to address evolving customer requirements. The business implication is clear: investment is increasingly concentrating on intelligent, energy-efficient equipment categories that deliver measurable operational advantages while supporting long-term sustainability objectives.

Restaurants remain the leading application segment, accounting for approximately 46% of total market demand due to their high equipment utilization rates, frequent replacement cycles, and growing emphasis on kitchen modernization. The concentration of demand within restaurant operations reflects the need for speed, consistency, and energy optimization in increasingly competitive foodservice environments. Quick-service and chain restaurant formats are particularly aggressive adopters of connected electric cooking systems. Institutional kitchens represent the fastest-growing application segment, expanding at an estimated 10% annual adoption rate as healthcare facilities, educational institutions, and government foodservice operations pursue energy-efficient infrastructure upgrades. Compared with traditional restaurant deployments focused on throughput, institutional applications prioritize reliability, compliance, and lifecycle cost reduction. Hotels, catering facilities, and corporate foodservice operations collectively contribute approximately 39% of market demand and are increasingly adopting advanced cooking platforms to improve operational flexibility. Usage patterns are evolving toward centralized monitoring, automation, and predictive maintenance capabilities. Manufacturers are adapting by developing specialized product portfolios optimized for application-specific requirements. The strategic implication is that demand is shifting beyond traditional restaurant environments toward institutional and multi-site operations where technology integration and operational efficiency have become critical purchasing criteria.

The restaurant sector remains the dominant end-user category, representing approximately 44% of overall market demand due to continuous equipment utilization, menu diversification requirements, and intense pressure to improve operational efficiency. Large restaurant groups and franchise operators continue investing heavily in kitchen electrification programs designed to reduce labor dependency and optimize energy consumption. Their purchasing decisions increasingly prioritize lifecycle performance and smart connectivity capabilities. Hospitality operators constitute the fastest-growing end-user segment, achieving adoption growth of nearly 9.5% as hotels and resort chains modernize foodservice operations to improve guest experience and operational consistency. Compared with restaurant operators focused primarily on throughput, hospitality organizations place greater emphasis on flexibility, premium food quality, and integrated kitchen management systems. Healthcare institutions, educational facilities, and corporate cafeterias collectively account for approximately 33% of market demand and continue expanding adoption of advanced electric cooking equipment. Buying behavior is shifting toward long-term service agreements, predictive maintenance solutions, and integrated equipment ecosystems. Manufacturers are responding through customized product offerings, strategic partnerships, and value-added service models tailored to specific end-user requirements. The business implication is that future demand growth will increasingly depend on an organization's ability to address diverse operational priorities through specialized and technology-enabled equipment solutions.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.8% between 2026 and 2033.

North America continues to dominate due to high concentration of restaurant chains, institutional foodservice operators, and rapid adoption of connected kitchen technologies. Europe captures approximately 28% of global demand, supported by energy-efficiency regulations and commercial kitchen electrification initiatives. Asia-Pacific holds nearly 25% share and is experiencing the strongest expansion as restaurant infrastructure, hospitality investments, and local manufacturing capacity accelerate across China, India, and Southeast Asia. South America and the Middle East & Africa collectively account for 11% of market activity, driven by hospitality expansion and foodservice modernization. Supply-chain localization and energy-transition policies are reshaping regional investment priorities, with manufacturers increasingly focusing on Asia-Pacific expansion while strengthening innovation and service networks across North America and Europe.

North America represents approximately 36% of global Commercial Electric Cooking Equipment market demand, making it the largest regional market. The region benefits from extensive deployment across quick-service restaurants, healthcare institutions, educational facilities, and hospitality operations. Rising labor costs and increasing demand for operational efficiency are accelerating adoption of connected cooking equipment and induction technologies. More than 42% of large foodservice operators are prioritizing kitchen electrification programs, while smart equipment deployment has increased by nearly 28% over the past two years. Manufacturers are expanding demonstration centers, digital service platforms, and predictive maintenance offerings. Enterprise buyers increasingly favor equipment that reduces energy consumption by 15–20% while improving throughput, making North America a priority region for technology investment and commercial expansion.

Europe accounts for approximately 28% of global Commercial Electric Cooking Equipment demand, supported by strong adoption across Germany, France, the United Kingdom, Italy, and the Nordic countries. The region's market is heavily influenced by sustainability regulations, energy-efficiency directives, and carbon-reduction objectives. More than 40% of newly specified commercial kitchen projects incorporate advanced electric cooking technologies as operators seek compliance advantages and lower energy intensity. Induction cooking installations have increased by nearly 32% across hospitality and institutional facilities. Foodservice operators increasingly prioritize lifecycle efficiency, operational transparency, and ESG performance when selecting equipment. Manufacturers are responding through expanded induction portfolios and energy-optimized product platforms. Europe continues to force innovation and adaptation, making it a strategic benchmark market for next-generation commercial kitchen solutions.

Asia-Pacific holds approximately 25% of global Commercial Electric Cooking Equipment demand and ranks as the fastest-expanding regional market. China, Japan, India, South Korea, and Australia collectively drive the majority of regional procurement activity. The region benefits from strong manufacturing capabilities, lower production costs, and rapidly expanding foodservice infrastructure. Commercial kitchen modernization projects have increased by nearly 30%, while localized equipment manufacturing has expanded by approximately 22%. Restaurant operators increasingly prioritize scalability, speed of deployment, and cost efficiency when making purchasing decisions. Equipment suppliers are establishing regional production facilities and strengthening distribution networks to capture demand growth. Asia-Pacific remains critical for volume expansion, manufacturing scale, and long-term market penetration strategies.

South America contributes approximately 6% of global Commercial Electric Cooking Equipment demand, with Brazil, Argentina, and Chile representing the primary markets. Demand is supported by restaurant sector expansion, hospitality investments, and growing interest in energy-efficient kitchen operations. However, elevated financing costs and uneven infrastructure development continue to constrain large-scale adoption. Nearly 24% of foodservice operators are prioritizing phased modernization programs rather than full kitchen replacements. Local demand for induction-based systems has increased by approximately 12%, reflecting growing awareness of operating-cost advantages. Manufacturers are strengthening distributor partnerships and introducing flexible financing models to improve accessibility. The region presents a compelling opportunity, but success depends on balancing affordability, infrastructure readiness, and technology adoption.

The Middle East & Africa region accounts for approximately 5% of global Commercial Electric Cooking Equipment demand, led by the UAE, Saudi Arabia, South Africa, and Qatar. Hospitality development, tourism expansion, and large-scale infrastructure investments are driving equipment procurement across hotels, resorts, institutional kitchens, and catering facilities. More than 18% of commercial kitchen projects now incorporate smart cooking technologies, while hospitality-related foodservice investments have increased by nearly 20% in key Gulf markets. Operators increasingly favor energy-efficient systems that improve reliability and reduce operating costs. Equipment manufacturers are expanding regional partnerships and service capabilities to support project deployment. The region is emerging as a strategic growth market where modernization and infrastructure investment are creating new opportunities.

United States – 31.0% Market Share: Benefits from extensive restaurant infrastructure, high adoption of smart kitchen technologies, and strong institutional foodservice demand.

China – 17.0% Market Share: Driven by rapid restaurant expansion, large-scale foodservice modernization, and substantial domestic manufacturing capacity.

The Commercial Electric Cooking Equipment Market is characterized by competition between global equipment leaders such as Middleby Corporation, Ali Group, Electrolux Professional, RATIONAL AG, and ITW Food Equipment Group, alongside regional manufacturers competing on customization and pricing. The top five players collectively control approximately 43% of market activity.

Competition is increasingly determined by technology integration, energy efficiency, digital connectivity, and service capabilities rather than equipment pricing alone. Smart kitchen solutions can improve operational efficiency by 20–25%, while advanced induction technologies reduce energy consumption by up to 30%, creating strong differentiation. Global leaders are expanding experience centers, investing in connected kitchen platforms, strengthening regional manufacturing footprints, and pursuing strategic partnerships to enhance customer engagement and lifecycle value.

A major competitive shift is underway as AI-enabled monitoring, predictive maintenance, and cloud-connected kitchen ecosystems become core purchasing criteria. High capital requirements, service-network development, and technology investment create significant entry barriers. Winning in this market requires combining operational performance, digital innovation, energy optimization, and scalable customer support capabilities.

Electrolux Professional

RATIONAL AG

Ali Group

ITW Food Equipment Group

Fujimak Corporation

Hoshizaki Corporation

Duke Manufacturing

Alto-Shaam Inc.

Vollrath Company LLC

Garland Group

MKN Maschinenfabrik Kurt Neubauer GmbH & Co. KG

Falcon Foodservice Equipment

AB Electrolux Foodservice Solutions

Commercial electric cooking equipment technology is rapidly evolving from standalone appliances toward intelligent, connected kitchen ecosystems. Current adoption is centered on induction cooking, IoT-enabled monitoring, and cloud-based equipment management. Advanced induction systems now deliver thermal efficiency levels exceeding 90%, compared with approximately 60–70% for conventional cooking technologies. More than 35% of newly installed premium commercial kitchens incorporate induction-based cooking platforms due to their ability to improve precision, safety, and energy performance.

Emerging technologies include AI-powered cooking optimization, predictive maintenance platforms, and automated workflow management systems. Smart equipment monitoring has demonstrated downtime reductions of nearly 25%, while predictive maintenance tools lower service-related costs by approximately 18%. These technologies enable operators to monitor performance remotely, optimize energy consumption, and improve kitchen throughput without increasing labor requirements.

A major disruptive trend involves the integration of connected kitchen ecosystems that link cooking equipment, inventory management, and operational analytics into unified platforms. Compared with legacy kitchen environments, connected systems improve operational visibility by more than 30% and significantly enhance decision-making. Restaurant chains, hospitality groups, and institutional operators gain the greatest advantage due to their multi-site management requirements.

Between 2026 and 2028, intelligent automation, AI-assisted cooking controls, and real-time performance analytics are expected to become standard purchasing considerations. Companies adopting these technologies early will secure stronger operational efficiency, lower lifecycle costs, and greater competitive differentiation in increasingly technology-driven foodservice markets.

February 2025 – Welbilt announced construction of its new Experience Center in Texas, creating an advanced demonstration hub for smart kitchen technologies and connected foodservice solutions. The facility is designed to support global customer engagement and accelerate technology adoption across commercial kitchens. [Innovation Hub] Source: www.welbilt.com

June 2025 – BlueStar expanded its induction product portfolio with a new 36-inch Platinum Series Induction Range featuring five cooking zones and up to 7,400 watts bridge-mode output. The launch strengthens market momentum toward high-efficiency induction cooking technologies. [Induction Expansion]

July 2025 – Electrolux Professional introduced the LiberoLight induction range featuring 95% energy efficiency and multiple modular cooking functions for hospitality and foodservice environments. The development enhances sustainability performance while reducing operating costs for commercial kitchen operators. [Efficiency Breakthrough]

September 2025 – Welbilt showcased next-generation AI-driven kitchen technologies and KitchenConnect® digital platforms at HOST 2025 in Milan. The initiative highlighted connected workflow automation capabilities designed to improve efficiency, scalability, and profitability across commercial foodservice operations. [AI Kitchen Shift]

The Commercial Electric Cooking Equipment Market Report provides comprehensive coverage of equipment categories, operational applications, end-user groups, regional markets, and emerging technology ecosystems shaping the industry. The study evaluates major product segments including electric ovens, induction cooktops, fryers, griddles, steamers, and integrated cooking platforms. Analysis extends across restaurant operations, hospitality facilities, institutional kitchens, healthcare environments, educational establishments, and corporate foodservice applications. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, enabling detailed assessment of regional demand patterns and competitive positioning.

The report incorporates quantitative and qualitative analysis across more than 15 segment combinations, multiple regional markets, and leading industry participants. It examines technology adoption trends including smart kitchen connectivity, predictive maintenance systems, AI-enabled cooking optimization, and energy-efficient induction platforms. More than 35% of premium commercial kitchen installations now feature connected technologies, while advanced induction systems account for over 30% of new high-performance cooking deployments.

Strategically, the report supports investment planning, market-entry evaluation, product development, capacity expansion, and competitive benchmarking. It highlights emerging technology opportunities, regional expansion priorities, evolving purchasing behaviors, and operational transformation trends expected to influence market direction between 2026 and 2033. Decision-makers gain actionable insights into where demand is concentrated, where adoption is accelerating, and which competitive strategies are most likely to generate sustainable market advantage.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,512.0 Million |

| Market Revenue (2033) | USD 4,513.5 Million |

| CAGR (2026–2033) | 7.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Middleby Corporation; Electrolux Professional; RATIONAL AG; Ali Group; ITW Food Equipment Group; Fujimak Corporation; Hoshizaki Corporation; Duke Manufacturing; Alto-Shaam Inc.; Vollrath Company LLC; Garland Group; MKN Maschinenfabrik Kurt Neubauer GmbH & Co. KG; Falcon Foodservice Equipment; AB Electrolux Foodservice Solutions |

| Customization & Pricing | Available on Request (10% Customization Free) |