Reports

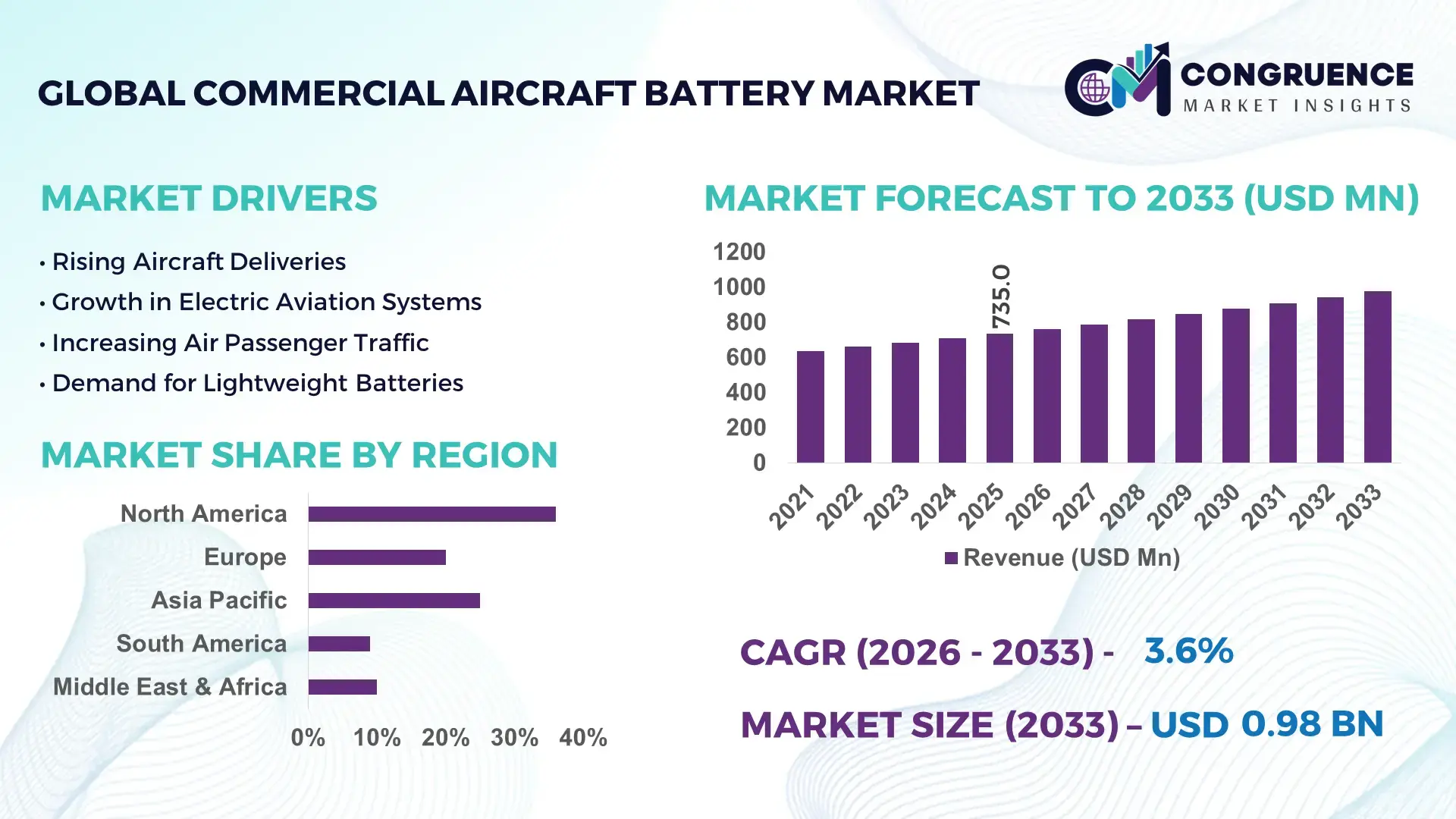

The Global Commercial Aircraft Battery Market was valued at USD 735 Million in 2025 and is anticipated to reach a value of USD 975.36 Million by 2033 expanding at a CAGR of 3.6% between 2026 and 2033. Rising commercial aircraft deliveries, accelerated fleet electrification programs, and increasing replacement cycles for lithium-ion auxiliary power systems are driving sustained demand across narrow-body and long-haul aviation platforms.

The United States remains the dominant country in the global commercial aircraft battery market, accounting for approximately 34% of installed commercial aviation battery capacity in 2026, supported by over USD 2.5 billion in aerospace electrification investments and large-scale aircraft manufacturing operations. More than 62% of newly integrated battery systems in U.S.-manufactured commercial aircraft now utilize advanced lithium-ion architecture with enhanced thermal management technology, compared with less than 40% adoption across several European legacy fleets. Strong procurement activity from major airlines, defense-linked aviation infrastructure, and FAA-backed electrification initiatives continue to reinforce domestic leadership in aircraft energy storage technologies. Strategic battery sourcing diversification and next-generation lightweight system integration are becoming decisive competitive factors for commercial aircraft manufacturers and tier-one aerospace suppliers.

Market Size & Growth: USD 735 Million recorded in 2025, reaching USD 975.36 Million by 2033 at 3.6% growth, supported by accelerated fleet electrification and lightweight battery integration.

Top Growth Drivers: Lithium-ion adoption increased 28%, aircraft replacement demand rose 19%, and airline fuel-efficiency initiatives expanded 22% globally.

Short-Term Forecast: By 2028, advanced aircraft battery systems are projected to improve energy efficiency by 18% while reducing maintenance downtime by 14%.

Emerging Technologies: AI-enabled battery monitoring, solid-state energy storage, and advanced thermal management systems improved operational reliability by over 21%.

Regional Leaders: North America exceeded USD 290 Million with electrification expansion, Europe crossed USD 210 Million through ESG aviation upgrades, and Asia-Pacific surpassed USD 250 Million driven by airline fleet expansion.

Consumer/End-User Trends: Over 61% of commercial airlines prioritized lightweight battery retrofits to improve fuel optimization and aircraft turnaround performance.

Pilot/Case Example: In 2026, a major commercial fleet modernization project reduced onboard auxiliary power weight by 17% using high-density lithium-ion battery systems.

Competitive Landscape: Leading manufacturers controlled nearly 46% market share, with strong competition among aerospace battery developers and integrated aviation technology suppliers.

Regulatory & ESG Impact: Emission-reduction mandates and sustainable aviation targets accelerated electric subsystem adoption by 24% across global airline fleets.

Investment & Funding: More than USD 3.1 billion entered aerospace electrification programs through manufacturing expansion, strategic partnerships, and battery technology development.

Innovation & Future Outlook: Next-generation solid-state aviation batteries and localized supply chain manufacturing are reshaping high-growth commercial aircraft energy storage strategies.

Commercial aviation, aerospace manufacturing, and airline fleet modernization collectively contribute over 68% of total commercial aircraft battery demand, supported by increasing adoption of lightweight lithium-ion systems and advanced thermal safety technologies. North America and Asia-Pacific remain the strongest demand centers due to expanding aircraft deliveries and regional production capacity investments. Recent innovations in AI-enabled battery diagnostics and high-density energy storage improved operational efficiency by nearly 20%, while stricter aviation sustainability frameworks and supply chain diversification initiatives accelerated procurement activity. Growing integration of electric auxiliary systems and next-generation solid-state battery platforms is expected to redefine long-term competitive positioning across the global commercial aircraft battery ecosystem.

The commercial aircraft battery market is becoming strategically critical as airlines, aircraft OEMs, and aerospace suppliers prioritize electrification, fuel-efficiency optimization, and resilient component sourcing. Battery systems now influence aircraft weight economics, maintenance cycles, and auxiliary power reliability, making them central to competitive fleet modernization strategies. A major market shift is emerging through aerospace supply-chain restructuring, with U.S. and European manufacturers reducing dependence on single-country lithium processing and battery component imports after logistics disruptions across the Red Sea and East Asia corridors. Airlines integrating next-generation lithium-ion systems are achieving nearly 16% lower maintenance intervention rates compared with legacy nickel-cadmium platforms.

Technology differentiation is accelerating investment activity across commercial aviation ecosystems. Advanced lithium-ion battery systems provide approximately 25% higher energy efficiency and 18% lower lifecycle servicing costs than conventional battery architectures, supporting wider deployment across narrow-body and long-range aircraft fleets. The United States leads large-scale deployment through integrated aerospace manufacturing capacity, while France and Germany are concentrating on thermal safety innovation and ESG-linked aviation electrification programs. Over the next three years, more than 58% of newly configured commercial aircraft platforms are expected to integrate digitally monitored battery management systems for predictive maintenance optimization.

Commercial airlines are also expanding battery retrofit programs to reduce turnaround delays and improve onboard power stability during high-frequency operations. In 2026, several aircraft maintenance providers in Singapore and Texas expanded strategic partnerships with battery diagnostics firms to accelerate fleet servicing efficiency and localized repair capabilities. Companies prioritizing vertically integrated battery sourcing, thermal management innovation, and aviation-certified energy storage systems are expected to strengthen long-term operational positioning as aircraft electrification standards intensify.

Commercial aircraft manufacturers are accelerating adoption of lightweight lithium-ion battery systems as airlines prioritize fuel-efficiency optimization and lower operational downtime. Advanced battery integration reduces aircraft system weight by nearly 4% while improving auxiliary power reliability by over 20%, directly supporting fleet modernization objectives. In the United States, rising narrow-body aircraft production and increased electric subsystem deployment across new-generation platforms are reshaping procurement priorities for aerospace suppliers. More than 60% of newly delivered commercial aircraft now integrate digitally monitored battery management architectures to improve predictive maintenance performance. In response, battery manufacturers are expanding thermal safety R&D, increasing localized assembly operations, and forming long-term supply agreements with aircraft OEMs. A notable strategic shift involves aerospace firms investing in vertically integrated battery sourcing to reduce exposure to lithium processing disruptions and improve delivery consistency.

The commercial aircraft battery market continues to face structural pressure from lithium, cobalt, and nickel supply volatility, with raw material pricing fluctuations exceeding 18% during recent procurement cycles. Aerospace-grade battery certification timelines remain lengthy, often extending integration approval periods by 12–18 months due to strict aviation safety validation requirements. China currently controls a substantial share of lithium refining capacity, creating supply dependency risks for aircraft battery manufacturers in the United States and Europe. These constraints increase production costs, delay deployment schedules, and compress supplier margins across aviation electrification programs. Companies are responding through mineral sourcing diversification, localized cell manufacturing expansion, and long-duration procurement contracts with upstream material processors. Several aircraft battery suppliers are also increasing investment in cobalt-reduced chemistries to stabilize long-term production economics and reduce exposure to geopolitical trade disruptions.

The integration of AI-enabled battery diagnostics and predictive maintenance platforms is creating high-value operational opportunities across commercial aviation. Advanced monitoring systems reduce unscheduled battery replacement incidents by nearly 22% while improving maintenance planning efficiency by over 17%. Japan and South Korea are emerging as strategic innovation hubs for intelligent battery management software integrated with aircraft health-monitoring platforms. Airlines are increasingly prioritizing digitally connected energy storage systems capable of delivering real-time thermal analytics, lifecycle forecasting, and remote fault detection. Simultaneously, solid-state aviation battery research is gaining momentum due to its potential to improve energy density by more than 30% while enhancing thermal stability. Battery manufacturers and aerospace technology firms are expanding joint-development programs, simulation partnerships, and digital servicing ecosystems to secure long-term positioning in next-generation aircraft electrification infrastructure.

Scaling advanced aircraft battery deployment across global airline fleets remains operationally complex due to thermal safety requirements, infrastructure compatibility gaps, and maintenance workforce limitations. High-density lithium-ion systems generate greater thermal management demands, increasing system integration complexity by nearly 19% compared with conventional aviation batteries. Several commercial maintenance facilities in emerging aviation hubs still lack certified infrastructure for advanced battery diagnostics, storage handling, and rapid replacement operations. Additionally, evolving aviation safety regulations across the United States and Europe are increasing compliance testing requirements for battery containment and fire suppression systems. These pressures impact deployment consistency, retrofit timelines, and long-term maintenance scalability for airline operators. Companies must strengthen technician training programs, expand certified battery servicing infrastructure, and invest in next-generation cooling technologies to maintain operational reliability as aircraft electrification intensity increases.

Localized Battery Supply Expansion Commercial aircraft battery manufacturers are restructuring sourcing networks as aerospace firms reduce dependency on concentrated Asian lithium processing capacity. More than 41% of aviation battery suppliers expanded localized assembly or pack integration operations in the United States and Europe during 2025–2026. Long-term mineral procurement contracts increased by 26% as logistics disruptions and Red Sea shipping instability pressured delivery schedules. This transition is shortening component lead times by nearly 18% while improving inventory visibility for aircraft OEMs. Companies are accelerating regional partnerships and vertically integrated sourcing strategies to stabilize aerospace-grade battery availability.

Predictive Diagnostics Deployment Accelerates Airlines and maintenance providers are rapidly integrating AI-enabled battery monitoring systems to reduce unscheduled aircraft servicing events. Digitally connected battery management deployments increased by 33% across newly configured narrow-body fleets, while predictive diagnostics lowered fault-detection response time by approximately 21%. Singapore-based aviation maintenance operators expanded automated battery analytics platforms to support high-frequency fleet operations. The shift is improving maintenance scheduling precision and reducing operational disruptions during peak utilization periods. Aerospace technology firms are scaling cloud-connected diagnostics infrastructure and expanding software integration partnerships with aircraft manufacturers.

Thermal Safety Standards Intensify Aviation regulators and aircraft operators are tightening thermal containment requirements following increased focus on lithium-ion safety certification. Advanced thermal shielding adoption increased by 24% across commercial fleet retrofit programs, while demand for fire-resistant battery enclosures rose nearly 19% in 2026. U.S. aircraft maintenance hubs are increasing investment in certified battery testing infrastructure and rapid-response containment systems. The trend is raising compliance costs but improving long-term deployment reliability for high-density battery systems. Battery suppliers are prioritizing cooling innovation, modular safety architecture, and aviation-certified containment technologies to secure large-scale fleet contracts.

Lightweight Retrofit Programs Expand Commercial airlines are expanding retrofit programs to improve fuel optimization and onboard electrical efficiency without major fleet replacement cycles. Lightweight lithium-ion retrofits reduced auxiliary system weight by nearly 15% on selected narrow-body aircraft platforms, improving operational fuel performance and turnaround speed. More than 38% of fleet modernization projects initiated in 2026 included battery-system upgrades integrated with digital aircraft health monitoring. Airlines in the United Kingdom and Japan are prioritizing retrofit-focused procurement to extend aircraft lifecycle efficiency under stricter sustainability targets. Battery manufacturers are responding through modular product platforms, faster installation workflows, and customized integration support for aging commercial fleets.

Lithium-Ion Batteries remain the leading segment in the commercial aircraft battery market due to superior energy density, lower weight profile, and compatibility with digitally monitored aircraft systems. More than 62% of newly integrated commercial aviation battery installations in 2026 utilized lithium-ion configurations, supported by nearly 25% higher operational efficiency compared with conventional nickel-cadmium systems. Main Aircraft Batteries also maintain strong deployment relevance because they support primary aircraft electrical functions and emergency operations across long-haul and narrow-body fleets. Auxiliary Power Unit Batteries are emerging as the fastest-growing segment as airlines prioritize fuel-saving auxiliary electrification strategies and faster turnaround performance. Nickel-Cadmium Batteries continue to serve mature fleets due to proven thermal stability and certification familiarity, particularly in older aircraft platforms. Lead-Acid Batteries hold limited but stable adoption within cost-sensitive maintenance environments. Battery manufacturers are increasing investment in lightweight lithium-ion chemistries, modular battery architecture, and thermal safety innovation to secure long-term supply agreements with aircraft OEMs and retrofit operators.

Auxiliary Power Systems represent the leading application segment due to increasing demand for efficient onboard electrical support during ground operations, aircraft startup, and standby functionality. Airlines integrating advanced auxiliary battery systems reported nearly 16% lower fuel dependency during airport ground handling operations and improved turnaround efficiency across high-frequency routes. Emergency Backup Power is emerging as the fastest-growing application as aviation regulators strengthen redundancy requirements for mission-critical onboard systems and thermal safety compliance. Engine Starting applications continue to maintain stable demand across commercial narrow-body fleets, while Flight Control Systems and Avionics Support segments are expanding through rising electrification of aircraft subsystems and digital cockpit infrastructure. Cabin Power Supply applications are also gaining importance as airlines increase passenger-facing electrical services and onboard connectivity deployment. Battery suppliers are scaling integrated power management solutions, automated diagnostics compatibility, and modular battery configurations to support evolving aircraft electrical architectures and operational reliability requirements.

Commercial Airlines remain the dominant end-user group due to large-scale fleet operations, intensive maintenance cycles, and rising investment in aircraft electrification upgrades. More than 58% of advanced aviation battery procurement activity in 2026 originated from airline fleet modernization programs focused on reducing aircraft weight and improving operational efficiency. Maintenance Service Providers are emerging as the fastest-growing end-user segment as airlines increasingly outsource battery diagnostics, thermal testing, and replacement services to certified aviation engineering specialists. Aircraft Manufacturers continue expanding long-term sourcing agreements for lightweight integrated battery systems, while Leasing Companies are prioritizing retrofit-ready aircraft configurations to improve asset competitiveness. Cargo Aviation operators are strengthening battery deployment for high-utilization logistics fleets, and Defense Aviation maintains steady procurement through reliability-focused operational requirements. Battery companies are responding through customized servicing contracts, predictive maintenance platforms, and ecosystem partnerships with airlines, OEMs, and aviation engineering firms to secure long-term deployment pipelines.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 4.4% between 2026 and 2033.

Localized Aerospace Battery Manufacturing Expansion

North America continues to dominate the commercial aircraft battery market due to high aircraft production concentration, advanced aviation maintenance infrastructure, and rapid deployment of lithium-ion battery technologies across commercial fleets. The region represented nearly 36% of global deployment activity in 2025, supported by strong fleet modernization investments from U.S.-based airlines and aircraft OEMs. More than 58% of newly delivered commercial aircraft across the region integrated digitally monitored battery management systems designed to improve predictive maintenance efficiency and reduce operational downtime. Aerospace suppliers are also increasing localized battery pack assembly and thermal safety testing capacity following supply-chain disruptions affecting imported aviation-grade cells. Strategic partnerships between aircraft manufacturers and battery diagnostics providers are accelerating deployment readiness and long-term servicing capabilities.

United States Market Outlook: The United States remains the operational center of the North American commercial aircraft battery market due to its large-scale aerospace manufacturing ecosystem and advanced aircraft maintenance infrastructure. Commercial airlines and aircraft OEMs are expanding deployment of lightweight lithium-ion systems to improve fuel optimization and electrical reliability across high-utilization fleets. Nearly 62% of domestic fleet upgrade projects initiated during 2026 included integrated predictive battery diagnostics and thermal monitoring technologies. U.S.-based aerospace firms are also increasing long-term sourcing agreements and domestic aviation battery assembly investments to improve supply continuity and certification efficiency.

Sustainability-Driven Aviation Electrification Transition

Europe is strengthening its commercial aircraft battery market position through aggressive aviation sustainability initiatives, advanced aerospace engineering capabilities, and rising deployment of lightweight energy storage systems. The region accounted for approximately 28% of global battery integration activity in 2025, supported by strong airline retrofit demand and increasing regulatory focus on aircraft efficiency optimization. More than 46% of fleet modernization projects across Western Europe during 2026 involved upgraded auxiliary battery systems designed to reduce onboard electrical losses and improve operational performance. Aerospace suppliers are investing heavily in thermal containment technologies, recyclable battery materials, and advanced energy management software. Aircraft manufacturers are also increasing collaboration with battery technology firms to strengthen certification readiness and lifecycle safety compliance across next-generation commercial aircraft platforms.

France Market Outlook: France remains a strategic aerospace hub within Europe due to its integrated aircraft manufacturing infrastructure and advanced aviation engineering ecosystem. Domestic aerospace firms are accelerating deployment of modular lithium-ion battery systems and digitally monitored power architectures across commercial aircraft programs. More than 40% of newly announced aviation battery testing projects in Western Europe during 2026 were concentrated in France. French aerospace manufacturers are also prioritizing recyclable material integration and advanced thermal safety engineering to align with evolving aviation sustainability regulations and long-term electrification objectives.

High-Volume Fleet Expansion and Retrofit Acceleration

Asia-Pacific is emerging as the fastest-growing commercial aircraft battery market due to rapid airline fleet expansion, large-scale battery manufacturing capacity, and increasing retrofit-oriented modernization activity. The region contributed nearly 31% of global deployment activity in 2025, supported by strong aviation growth across China, Japan, Singapore, and South Korea. Aircraft maintenance providers increased battery servicing and diagnostics infrastructure investment by approximately 24% during 2026 to support growing integration of advanced lithium-ion systems. Regional battery suppliers are also expanding localized manufacturing and thermal management production capabilities to strengthen export competitiveness and reduce procurement delays. Airlines are increasingly prioritizing lightweight battery retrofits to improve operational turnaround efficiency and extend commercial aircraft lifecycle performance under rising passenger traffic pressure.

China Market Outlook: China leads the Asia-Pacific commercial aircraft battery market through aggressive aerospace industrial expansion, large-scale battery production capacity, and strong domestic airline procurement activity. Commercial aviation operators are increasing integration of lightweight lithium-ion systems across narrow-body fleet modernization programs to improve operational efficiency and onboard electrical reliability. More than 57% of newly announced aviation battery production capacity additions across Asia-Pacific during 2026 were concentrated in China. Domestic manufacturers are also strengthening collaboration with aircraft engineering firms and state-supported aerospace infrastructure programs to accelerate localization of aviation-certified energy storage technologies.

Aircraft Lifecycle Extension Supporting Deployment

South America is witnessing gradual commercial aircraft battery market expansion through increasing aircraft maintenance activity, retrofit-oriented modernization programs, and airport infrastructure upgrades. The region represented nearly 5% of global deployment activity in 2025, with Brazil accounting for the majority of commercial fleet battery integration demand. Airlines are prioritizing replacement-focused battery deployment strategies to improve operational reliability across aging narrow-body and regional aircraft fleets. Aviation engineering providers across the region expanded certified lithium-ion servicing and diagnostics capabilities by approximately 17% during 2026 to support rising maintenance requirements. Despite improving deployment activity, limited localized aerospace battery manufacturing capacity and continued import dependency remain operational constraints affecting long-term scalability and supply flexibility.

Brazil Market Outlook: Brazil remains the largest commercial aircraft battery market in South America due to its established aerospace manufacturing sector and strong regional airline operations. Commercial carriers and maintenance providers are increasing deployment of digitally monitored battery systems to reduce servicing delays and improve fleet reliability across medium-haul operations. Nearly 48% of battery retrofit agreements signed in South America during 2026 originated from Brazilian airline modernization programs. Domestic aviation firms are also expanding technical partnerships with international battery suppliers to strengthen thermal safety compliance and improve access to aviation-certified energy storage technologies.

Aviation Infrastructure Modernization and Fleet Upgrades

The Middle East & Africa commercial aircraft battery market is expanding through airport infrastructure investment, premium airline fleet modernization, and increasing deployment of advanced onboard electrical systems. The region accounted for approximately 7% of global deployment activity in 2025, driven primarily by Gulf-based long-haul airline operations. Airlines in the United Arab Emirates and Saudi Arabia are increasing integration of lightweight lithium-ion battery systems to improve fuel optimization and operational efficiency across high-utilization international routes. More than 21% of aviation infrastructure investments announced across Gulf aviation hubs during 2026 targeted advanced battery diagnostics, thermal management, and certified maintenance capabilities. Aerospace service providers are also strengthening partnerships with international battery manufacturers to improve localized servicing readiness and deployment support infrastructure.

United Arab Emirates Market Outlook: The United Arab Emirates leads the Middle East & Africa commercial aircraft battery market through its globally connected aviation ecosystem, advanced maintenance infrastructure, and premium airline fleet operations. Aviation operators are prioritizing battery modernization initiatives integrated with predictive maintenance systems to improve operational reliability and reduce aircraft turnaround delays. Nearly 44% of advanced aircraft battery servicing capacity added across the Middle East during 2026 was concentrated in the UAE. Domestic aviation infrastructure projects and airline expansion strategies are also accelerating demand for aviation-certified energy storage systems capable of supporting long-haul operational intensity and next-generation electrical architectures.

The commercial aircraft battery market is led by competition between global aerospace battery manufacturers including Saft, EnerSys, GS Yuasa, Concorde Battery, and EaglePicher Technologies against emerging lithium-ion integrators and cost-focused regional suppliers. The top five players collectively control nearly 58% of global deployment activity through aircraft OEM partnerships, certification strength, and integrated maintenance capabilities. Competition is increasingly driven by thermal safety performance, lightweight system efficiency, and supply-chain localization rather than pricing alone. Advanced lithium-ion platforms improve operational efficiency by nearly 25%, while predictive diagnostics integration reduces unscheduled maintenance frequency by approximately 18%. Companies are strengthening market position through vertically integrated sourcing, localized battery assembly expansion, and long-term retrofit agreements with commercial airlines. The competitive shift is moving toward digitally monitored battery architectures and aviation-certified modular platforms. High aerospace certification complexity and thermal compliance testing remain major entry barriers. Success depends on engineering reliability, certification readiness, and resilient aviation supply-chain execution capabilities globally.

EnerSys

Saft

GS Yuasa Corporation

Concorde Battery Corporation

EaglePicher Technologies

MarathonNorco Aerospace

Teledyne Battery Products

True Blue Power

HBL Power Systems

Securaplane Technologies

Mid-Continent Instrument Co.

Kokam Co., Ltd.

Panasonic Energy

Amprius Technologies

Commercial aircraft battery technology is shifting rapidly toward advanced lithium-ion architectures with integrated battery management systems, predictive diagnostics, and lightweight modular configurations. In 2026, more than 62% of newly configured commercial aircraft platforms adopted digitally monitored lithium-ion systems to improve lifecycle visibility and maintenance precision. Compared with conventional nickel-cadmium batteries, next-generation lithium-ion platforms deliver nearly 25% higher energy efficiency and reduce aircraft system weight by approximately 15%, directly improving fuel optimization and operational turnaround speed. Airlines and aircraft OEMs are prioritizing thermal containment technologies and AI-enabled diagnostics to reduce unscheduled battery replacement events by nearly 18%.

Emerging technologies are centered on solid-state battery development, silicon-anode chemistries, and cloud-connected predictive maintenance infrastructure. Advanced thermal monitoring systems improved fault-detection response accuracy by nearly 21% during high-utilization commercial fleet operations. Aircraft manufacturers in the United States, France, and Japan are expanding partnerships with battery analytics providers and aerospace software firms to accelerate certification-ready deployment of intelligent energy storage platforms.

Between 2026 and 2028, competitive advantage will increasingly depend on certification-grade thermal safety engineering, localized battery manufacturing, and digitally integrated servicing ecosystems. Aerospace battery suppliers investing early in modular solid-state integration and AI-driven lifecycle management are expected to secure stronger retrofit contracts, lower maintenance dependency, and faster commercial deployment readiness.

February 2026 – H55 completed the aviation industry’s first regulator-required propulsion battery module certification tests under EASA oversight, validating fire-containment capability across worst-case scenarios and accelerating electric aircraft certification readiness. Source: H55

April 2026 – Aloft AeroArchitects and 101 Aviation advanced lithium-iron phosphate battery certification programs for Gulfstream aircraft, deploying systems weighing nearly 60% less than conventional units to improve aircraft efficiency and maintenance performance. Source: AIN Online

September 2025 – FAA issued a commercial aviation lithium-battery safety alert after 50 reported U.S. thermal incidents, intensifying airline focus on containment systems, onboard monitoring, and upgraded battery-handling procedures. Source: Reuters

February 2026 – Vaeridion partnered with Molicel to develop aviation-grade high-energy battery cells for electric aircraft programs, strengthening wing-integrated battery architecture and accelerating certification-focused prototype deployment targets through 2027. Source: Airframer

The Commercial Aircraft Battery Market report provides detailed analysis across battery technologies, aircraft applications, end-user deployment patterns, and regional aviation infrastructure trends between 2026 and 2033. The study covers Lithium-Ion Batteries, Nickel-Cadmium Batteries, Lead-Acid Batteries, Auxiliary Power Unit Batteries, and Main Aircraft Batteries while evaluating operational adoption across engine starting, emergency backup power, avionics support, auxiliary power systems, and cabin electrical supply. More than 60% of assessed commercial fleet modernization programs involve lightweight lithium-ion integration and digitally monitored battery management deployment, highlighting the growing transition toward advanced aircraft electrification systems.

The report also evaluates strategic activity across commercial airlines, aircraft manufacturers, maintenance service providers, cargo aviation, leasing companies, and defense aviation operators. Regional analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with emphasis on manufacturing concentration, retrofit deployment activity, thermal safety investments, and predictive diagnostics integration. The study supports competitive positioning, expansion planning, supplier evaluation, procurement strategy, and long-term aviation electrification investment decisions across commercial aerospace ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 735 Million |

|

Market Revenue in 2033 |

USD 975.36 Million |

|

CAGR (2026 - 2033) |

3.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

EnerSys, Saft, GS Yuasa Corporation, Concorde Battery Corporation, EaglePicher Technologies, MarathonNorco Aerospace, Teledyne Battery Products, True Blue Power, HBL Power Systems, Securaplane Technologies, Mid-Continent Instrument Co., Kokam Co., Ltd., Panasonic Energy, Amprius Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |